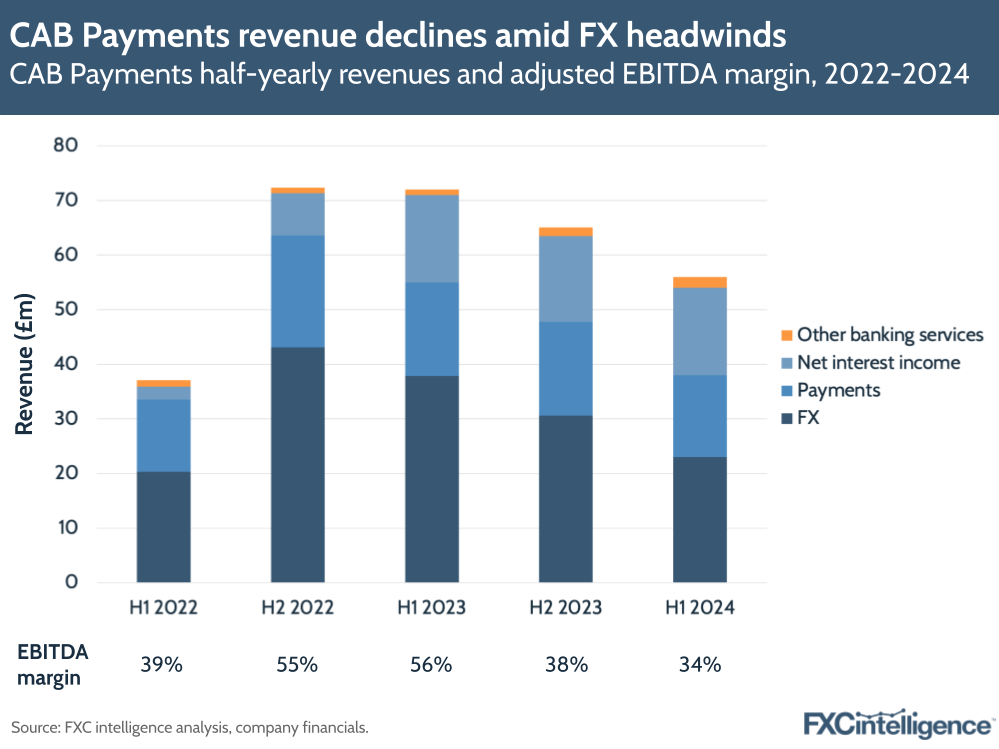

Just over a year after its IPO, UK-based B2B payments provider CAB Payments has released a trading update for H1 2024, during which headwinds in Africa impacted revenues. The company’s gross revenue declined 22% to £56m and, while total volumes rose by 4% to £17.6bn, investors responded poorly as CAB’s share price fell by as much as 23% on Thursday.

Newly appointed CEO Neeraj Kapur said the company’s performance in H1 was “resilient” despite a lack of tailwinds from the Nigerian naira – a key currency for the company – as well as continued impacts from central bank intervention in the Central African franc and the West African franc. Market-wide payment flows were down approximately 5% in the group’s core Sub-Saharan Africa market and approximately 10% globally, according to the company’s own analysis.

These factors drove a 39% YoY decline in Wholesale FX revenues to £23m as well as a 30% decline in the Payments FX segment. Within the latter, Payments FX revenues declined by 30% to £7m, while Other Payments rose 8% to £7m. This drove a 15% loss for the company’s wider Payments segment to £15m.

Overall, total transactional income was down 32% to £37m. Adjusted EBITDA remained positive at £19m, creating a margin of 34%, but this is down compared to H1 2023 figures of £40m and 56% respectively, on the back of growing investments in the company’s EU and US offices.

Excluding the impact of the affected currencies, underlying gross revenue growth would be 11%, while Wholesale FX growth would have been 24% and total transactional income would have risen 13% – however, for the wider Payments segment, YoY growth would still have been flat compared to last year, while Payments FX would have seen a 9% drop.

Despite setbacks, the company gave reasons to be confident for the second half of the year. It is diversifying revenues, with its top five currency corridors accounting for 32% of gross revenue versus 49% in H1 2023, while net interest income was up 2%. Net interest income now takes up around 29% of the share of overall revenue – a larger share than the Payments segment’s 27% – which begs a question about the impact of central banks cutting interest rates in the future.

While it didn’t give a clear revenue outlook in this update, CAB Payments expects total gross revenue for 2024 to be “marginally down” compared to last year. However, it expects gross revenue to rise in H2 2024 on the back of seasonal uplifts in volume, expansion into new markets and new products. The company also expects to see double-digit growth in underlying transactions beyond its top three corridors for 2023.

Which African markets see the biggest inbound payment flows?