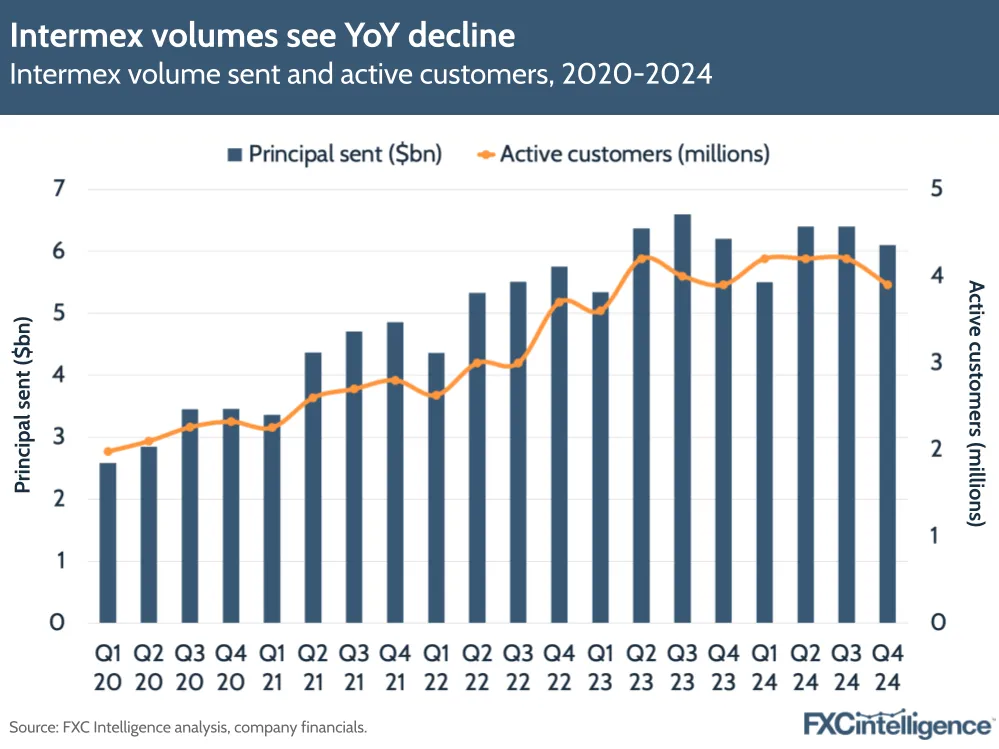

Intermex’s revenue stayed flat at $658.6m in FY 2024, with a slowdown in its core market of Latin America leading to a -0.8% decline in annual principal sent to $24.4bn. However, the company did see a 1% increase in its adjusted EBITDA to $121.3m.

As well as releasing its latest earnings, Intermex held an Investor Day event (its first since March 2022) at which it spoke more about the company’s growth plans, with a strong focus on growing its digital market share. However, investors responded negatively to the company’s stifled growth, with the company’s share price dropping significantly the day after its presentation.

Late last year, Intermex mentioned it was assessing a number of strategic initiatives regarding the company’s future, one of which was a potential sale or merger. However, the company said in a press release announcing its latest earnings that it hadn’t received an offer at a price that gave it a “superior alternative to the long-term stockholder value potentially created by Intermex’s current business model and its strategic plan”, and was suspending its strategic review process.

Now, the company is looking to double down on capturing digital customers through aggressive expansion this year, though CEO Bob Lisy maintained that retail (i.e. cash-based remittances made through its retail money transfer network) is still crucial for the business’ growth going forward, and the company will continue to invest in staff and marketing in 2025.

Intermex sees slowdown in LatAm remittances market

In Q4 2024, Intermex’s revenue declined -4% to $164.8m, with wire transfer and money order fees – the company’s core business from transactions – falling 5% to $137m. Over the full year, wire transfer and money order fees fell -1% to $555m – the first annual decline in this metric that Intermex has seen since it went public in 2018.

Remittance transactions were down 3.2% in Q4 2024 and flat for the full year, totalling 58.8 million. However, the company continued to drive digital growth during the quarter, with revenue driven by digital money transfers increased 48.3%.

Amid growth pressures, Intermex saw adjusted EBITDA of $30.9m in Q4 2024 – driving a margin of 17%. EBITDA was down -7% for the quarter, but the company still saw 1% growth to $121m for the full year – producing a margin of 18%. This was largely because the company’s total operating costs for the full year also remained relatively flat at $564m. Moreover, Intermex noted a 20% CAGR in its revenue in the period from 2015 to 2024, and recorded six million unique customers last year.

Digital’s growing share of Intermex transactions

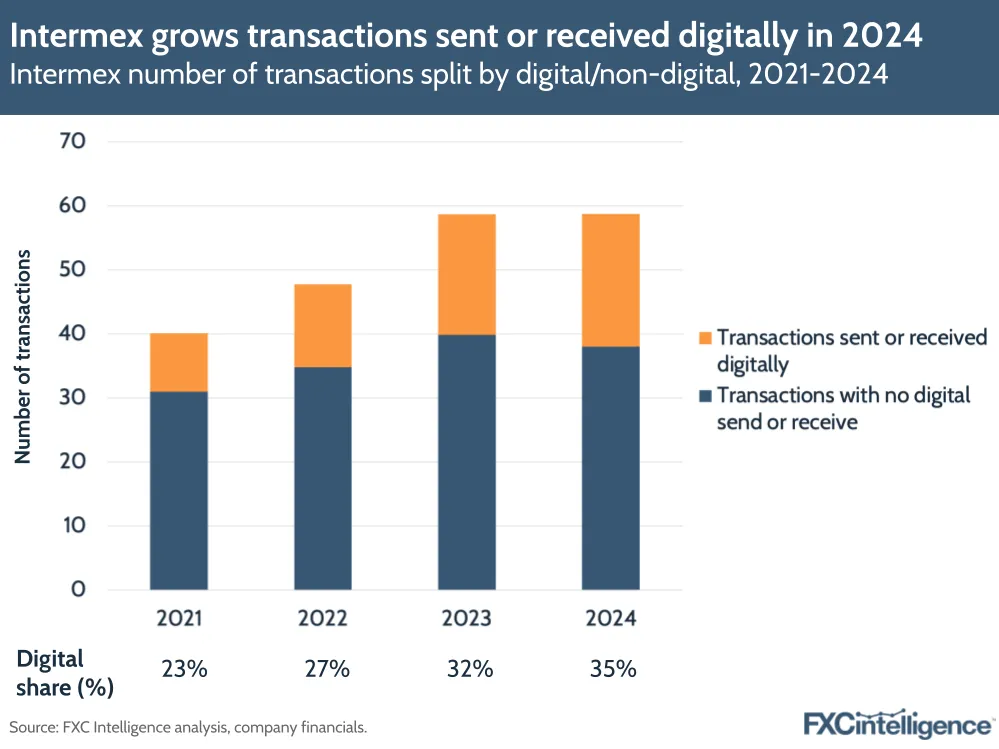

Though Intermex has remained bullish on retail, digital transactions are becoming a growing focus area for the business. In Q4 24, Intermex shared its figure for digitally originated transactions for the first time – reaching 0.8 million – which still only makes up about 5% of the company’s total transactions but is the result of 71.7% growth, versus a -3% decline in transactions for the business overall in the same period.

By comparison, Intermex’s share of transactions that were either sent or received digitally is currently much higher than digitally sent transactions. Based on our calculations spanning transactions across Intermex’s full-year results, the total number of transactions that were either sent or received digitally grew 10% YoY in FY 2024 to 21 million. Meanwhile, transactions with no digital send or receive declined by -5% in 2024 to 38 million.

FY 2024 actually represented a slight slowdown in growth for transactions sent or received digitally in 2022 and 2023. However, Intermex has doubled its number of transactions that contain either digital send/receive since 2021, with these transactions accounting for a 35% share of the company’s transactions in 2024 versus 23% in 2021.

With that said, the company believes retail is the biggest part of the market for the next few years, with this segment contributing $600m+ in annual revenue in 2024. Lisy said to investors that retail continued to show resilience despite the challenging backdrop and the fact that many competitors were stepping back from the segment created an even greater opportunity there – in countries such as Guatemala for example, where Intermex estimate the digital business to be less than 15% of the market.

Having said this, the slow growth in the retail market is propelling a move to digital, and Intermex is now seeking to invest more in marketing to drive digital growth, for example through an improved mobile app for customers. Specifically, the company wants to raise its digital marketing spending from around $1m to $9m in 2025, while spending $3m-3.5m on staffing and retail marketing to help drive profits through its core business that Intermex can then use to fund digital growth in the future.

Diversifying into new markets

Aside from Guatemala, Intermex is embedded in a number of other countries in Latin America, including Mexico, the Dominican Republic, Honduras, El Salvador, Colombia, Ecuador and Nicaragua. Altogether, the company sees its total addressable market for US to LACA transactions being $122bn.

Following its acquisition of La Nacional – and with it, small European remittance business I-Transfer – Intermex has started looking towards Europe, which it sees as a $315bn market (in terms of European transfers to the rest of the world). Having said this, according to CFO Andras Bende, I-Transfer is still only a $20m business, though it is continuing to see growth and the higher share of banked consumers in its market makes the business ripe for digital expansion.

In the meantime, Intermex has factored uncertainty in its key markets and corridors into its 2025 guidance, as well as its change on spending for digital customers and additional spending on staff. It is projecting full year revenues of $657.5m-677.5m, ranging from a small decline to 3% growth, while expecting adjusted EBITDA of $113.8m-117.3m, which would be a decline of between -3% and -6% and give a slightly decreased margin at 17.3%.

Intermex’s continued faith in its retail services are underlined by a strong need for it to push into new business areas and continue to capture a new kind of customer. With market uncertainty affecting its outlook next year, this need could become even more pronounced, particularly as digital money transfer challengers such as Wise begin to grow their operations in the space. It will also be interesting to see whether it readdresses the potential of a sale depending on its ongoing performance.

How is Intermex performing on pricing against other remittances players?