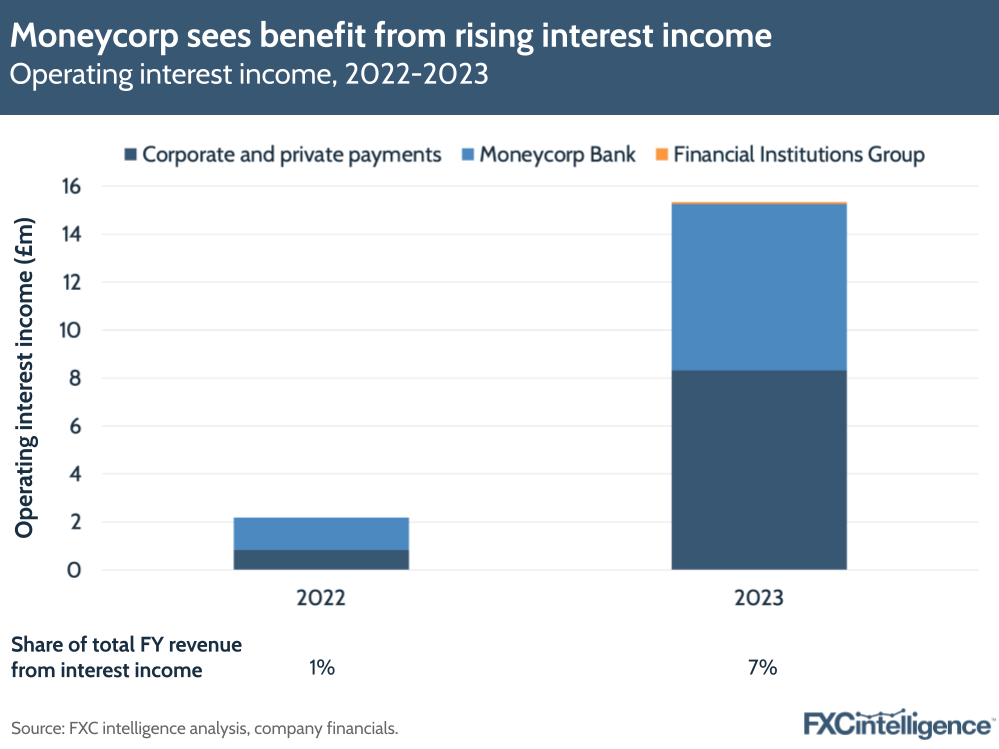

Impacts from higher interest rates have been a common theme for cross-border payments companies of late, and Moneycorp is no exception. Alongside record revenues, the corporate payments platform noted a 600% rise in interest incomes to £15m in its FY 2023 annual results (published this September), which made up 7% of the company’s total revenues for the year, compared to 1% in 2022.

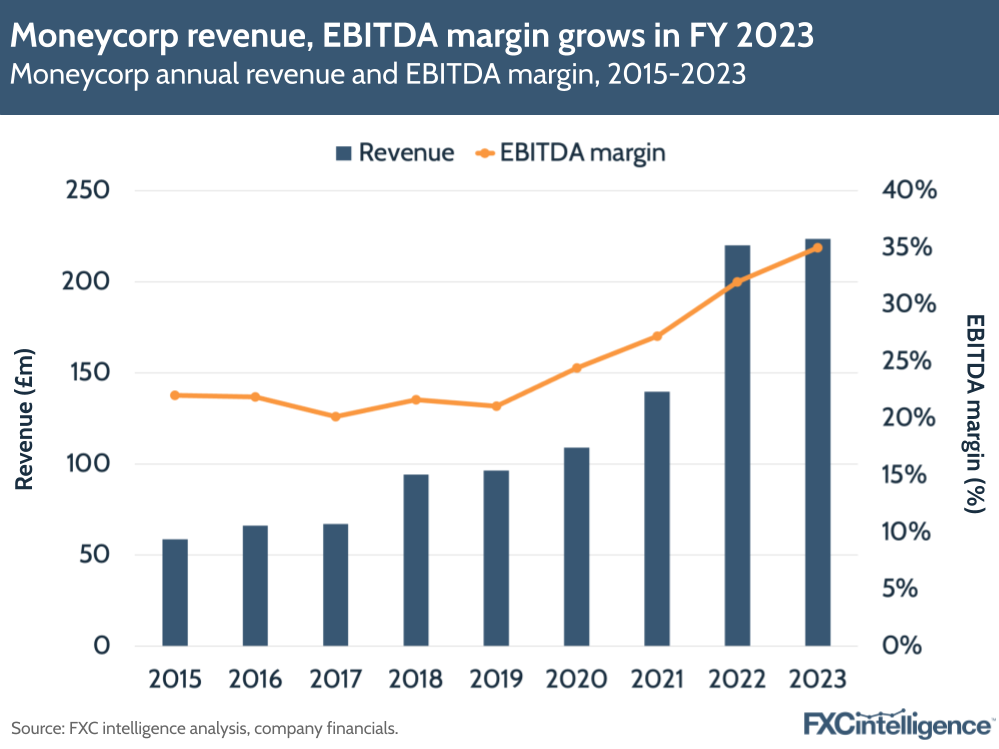

While the vast majority of the company’s 2023 revenue stemmed from financial instruments and contracts with customers, the rise in interest income helped the company achieve 2% revenue growth to £224m, as opposed to 58% growth last year. The company said that the growth slowdown was due to a more “normalised” market environment compared to 2022, with lower volatility leading to a 3% decline in trading volumes. It also noted that the company had seen a compound annual growth rate of 27% in the period from 2021-2023.

Interest incomes and cost management help drive the company’s EBITDA up 11% to £78m, against 85% growth in 2022. The company’s EBITDA margin was higher this year at 35%, compared to 32% last year, despite a 53% rise in capex investment to £19m.

On FY 2024, the company “remains cautiously optimistic”, saying slowing inflation and falling interest rates will provide a better environment for global ecommerce, while elections and geopolitical events may drive currency volatility. The company also saw some key leadership changes last year, with Velizar Tarashev joining as Group CEO in July 2023, with Richard Brice onboarded as Group CFO in December 2023.

In this report, we take a closer look at Moneycorp’s mix, including a specific look at how changing revenue mix, interest rates and inflation have impacted the company in 2023.

Why volumes declined for Moneycorp

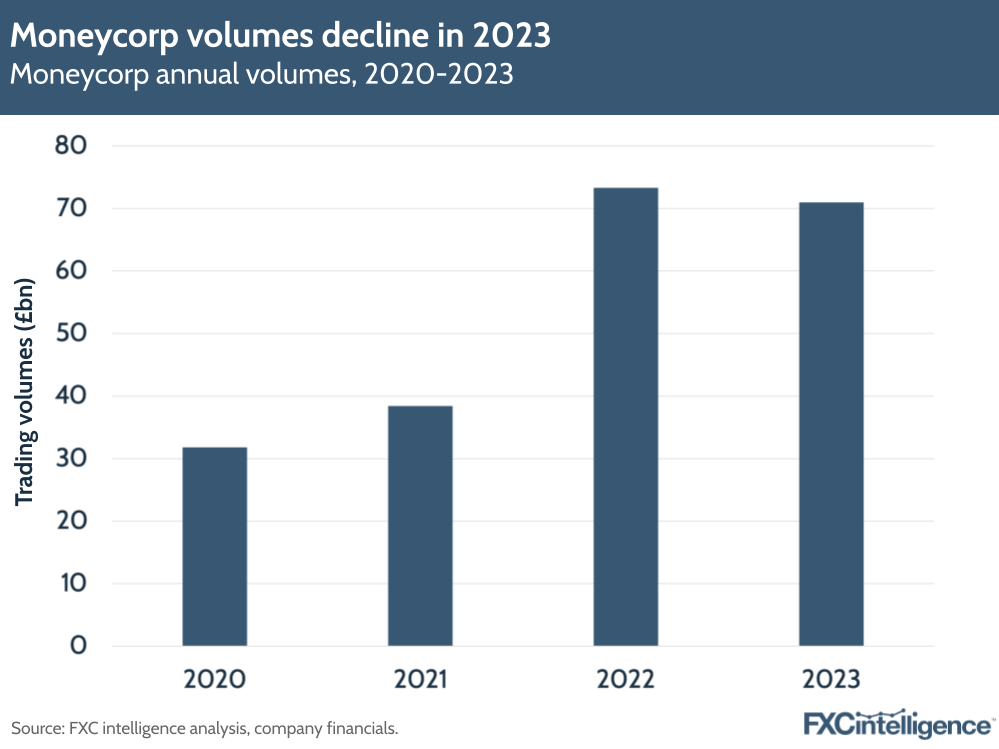

In 2023, Moneycorp’s trading volumes fell by 3% to £71bn, which the company said was due to a more normalised environment in 2023 compared to 2022. The effects of this were particularly felt in Moneycorp’s corporate payments segment, which serves clients across the UK, Europe, North America and Brazil.

Back in 2022, high market volatility meant that a large number of the company’s corporate clients needed cross-border payments and risk management products to protect against exposure from volatility in the markets. The UK’s mini-budget, for example, resulted in the GBP to decline in value to near parity with the USD and led to a much higher amount of trades to USD.

As a result, client flows through the business increased 13% to £18.8bn that year, resulting in 26% growth in corporate payment flows to £87.3m. Contributing to this were 24% growth in UK revenues, 33% growth in North America and 46% growth in Europe, though Brazil revenues declined -14%.

However, the combined effect of a normalised FX market and rising interests and inflation meant that clients weren’t transacting as much through Moneycorp’s platform. The company saw reduced flows of £15.1bn in 2023, while payment revenues for this segment overall remained flat in 2023. Considerably more muted growth was also obvious at a regional level, with the UK, North America and Europe seeing respective growth of 1%, 5% and 12%; meanwhile, Brazil revenues fell -56%.

Moneycorp continues to deal largely in USD, which made up 84% of the company’s flow in 2023. The company continues to see demand for USD worldwide, with Federal Reserve figures cited showing the proportion of USD held internationally at 46% as of 2021. The focus on this safe haven currency – which tends to see major investment during periods of volatility – is tied to the company’s revenue growth.

While volumes continued to go down, the company still managed to deliver EBITDA growth of 11%, though this was down from 85% growth last year and 45% growth in 2021. Moneycorp put this down to cost management and a reduction in trading costs, which in its corporate payments segment, for example, led to a 14% rise in its EBITDA contribution to £40.5m.

Moneycorp’s shifting mix

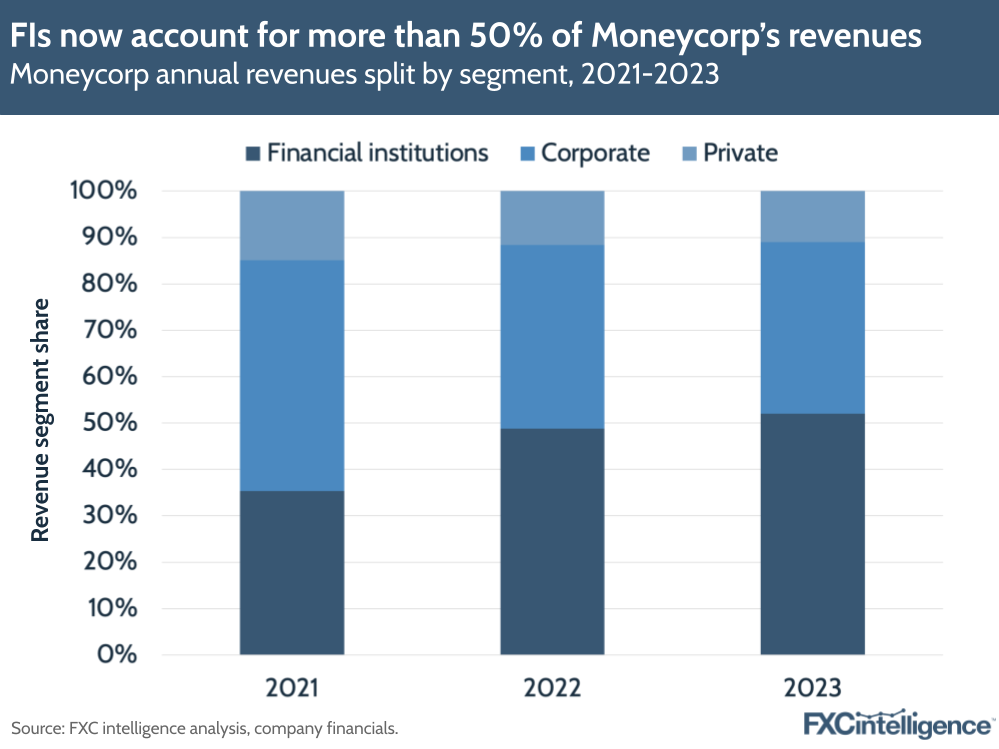

Though it originally started out as a retail-focused bureau de change, Moneycorp has been shifting its revenue streams away from private customers over the last decade. It is now an international payments and FX platform, with cross-border payment flows for financial institutions having become the biggest revenue contributor, followed by corporate payments and then private payments focused on high-net-worth individuals.

The impacts from interest rates are strongly linked to Moneycorp’s evolution into a B2B player, which continued in 2023. The company said that, overall, 90% of its revenues in 2023 were derived from B2B activities, with 36% of revenues from client flows originating from Europe, Middle East and Africa (EMEA) excluding the UK; 27% coming from the UK; 22% from North America; 11% from APAC; and 4% from South America.

In 2023, the company’s financial institutions segment accounted for over 50% of revenues for the first time (52%, against 49% in 2022), while corporate payments had a 37% share and private payments accounted for 11%. Financial institutions grew by 7% to £114m during the year, while its corporate payments segment was flat at £87m and private payments declined 13% to £22m. FI payments business growth was driven by rising client flow to £54.1m (3% growth), with particular strength in the APAC region.

These figures are related to client flow revenues and exclude interest income, but they highlight the extent of the company’s shift towards the B2B payment sphere and banking products, where interest incomes are having an impact. The company’s financial payments institution itself consists of two main business units: Financial Institutions Group (FIG), which specialises in wholesale money movement, and Moneycorp Bank, the company’s licensed bank in Gibraltar, which offers payment and FX services.

FIG’s EMEA and APAC businesses are still core drivers of revenues in the FI business, growing 2% to £94m and 10% to £10m respectively, but Moneycorp Bank grew substantially faster than both businesses with a 77% increase to £10m. This was driven by the high interest rate environment, as well as increased revenue from Moneycorp Bank’s Markets in Financial Instruments Directive products.

By contrast, the company’s private payments unit delivered £10m in EBITDA and £22.1m in revenue (declines of -18% and -13% respectively); Moneycorp again put this down to increased inflation and interest rates, which affected high-value purchases such as international property purchases abroad in particular. However, the company expects this to improve as the overall market improves.

Current and future interest rate impacts

Looking specifically at interest rate incomes, the company breaks these out across its combined corporate and private segments, its FIG segment and Moneycorp Bank. Total growth in operating interest income was 603% to £15m, driven principally by 917% growth in the Payments – Corporate and Private segment’s interest income and 408% growth in Moneycorp Bank.

These rises reflect other reports from companies in both the B2B and consumer payments space. For example, in its H1 2024 results, CAB Payments reported net interest income that accounted for 29% of the company’s overall revenues. However, a key difference here is that CAB operates largely with emerging markets currencies that had seen significant volatility in 2023 moving into H1 2024, which had a significant impact on its trading volumes and meant that interest incomes had a higher share of its income over the period.

Australian payments player OFX – which has also shifted to B2B – and education payments focused Flywire saw similar impacts, while Revolut and Wise have seen customers hold growing balances in B2B and consumer multiurrency accounts, which in turn has boosted their interest income.

Moneycorp has acknowledged interest rates in its macro outlook, saying that they continue to be a key driver of exchange rates and performance is linked to how policymakers navigate inflation and growth going forward. Having said this, some central banks have already moved to start cutting rates as inflation slows.

Navigating trends in the cross-border payment space

Aside from inflation, Moneycorp also mentioned a number of trends in the cross-border space, including growing geopolitical tension and a significant number of major elections globally, both of which could result in more currency volatility affecting results in 2024. Moneycorp said it continues to monitor impacts to major currencies, including the USD and GBP, and communicate these to clients.

Other trends the company mentioned included an increase in expectations from regulatory changes; a continued focus on protecting client funds; acceleration of advanced technologies, such as APIs, cloud-native platforms and AI; and a stable demand for physical banknotes in the medium term.

Going forward, Moneycorp said it remains focused on scaling its core platform, expanding to new geographies, adding new licences and future product development. The company noted progress on its expansion to the US, which has begun through a formal application for a banking charter to the US state of Connecticut’s Department of Banking.

The company is currently positioning itself between what it describes as neo-fintechs and traditional banks as a cross-border payments specialist, with both the trustworthiness and security of a bank as well as the advanced technology being used by fintechs. This is seemingly a recognition of the continued disruption of the industry by new players in the cross-border payments space – a trend observed on both the consumer and B2B side.

Interest rates are far from being the main revenue source for Moneycorp, but their sharp growth in 2023 and ongoing uncertainty means this will remain a metric to watch for the company and its competitors in the future.