This month, Mastercard and Visa both released their latest earnings results – covering Visa’s Q3 2024 and Mastercard’s Q2 2024 – with cross-border payments continuing to play a major role in delivering volumes for both companies.

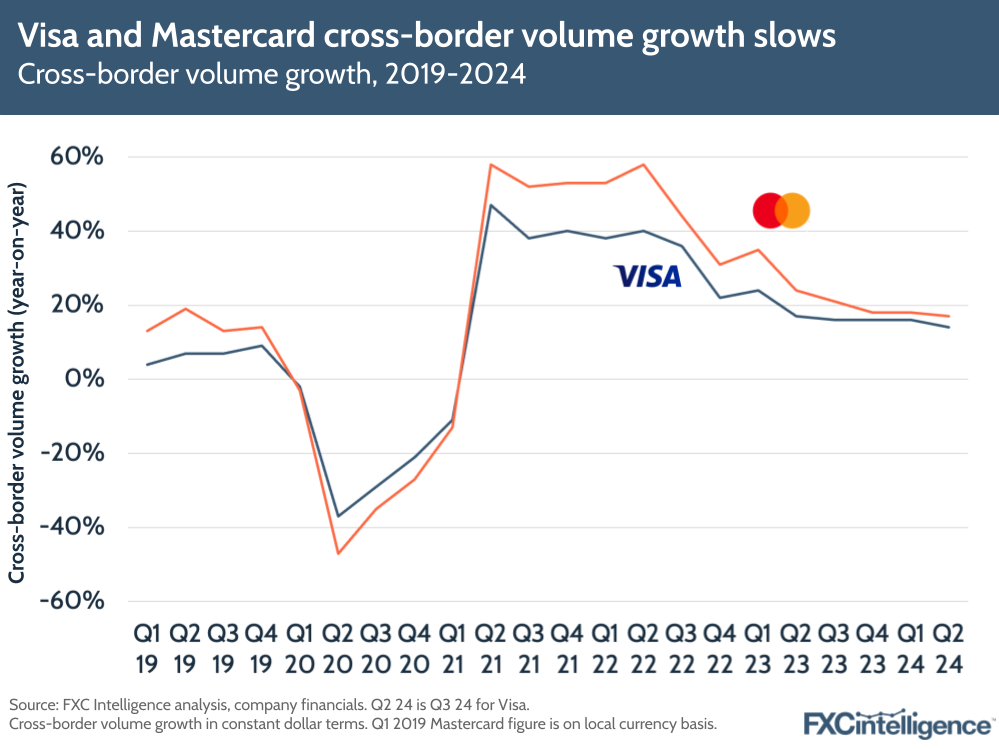

Both companies have seen revenues grow during the quarter – 10% for Visa, 11% for Mastercard. Cross-border volumes rose during the quarter, though at a slower pace than previous quarters, with Visa seeing 14% growth while Mastercard saw a rise of 17%.

Mastercard spoke about building out its portfolio with new partnerships to help expand in markets worldwide as well as key trends such as open banking and AI, while Visa highlighted successes from its Visa Direct cross-border platform, travel trends and the ongoing Olympic Games in Paris.

Highlights from Visa’s Q3 2024 results

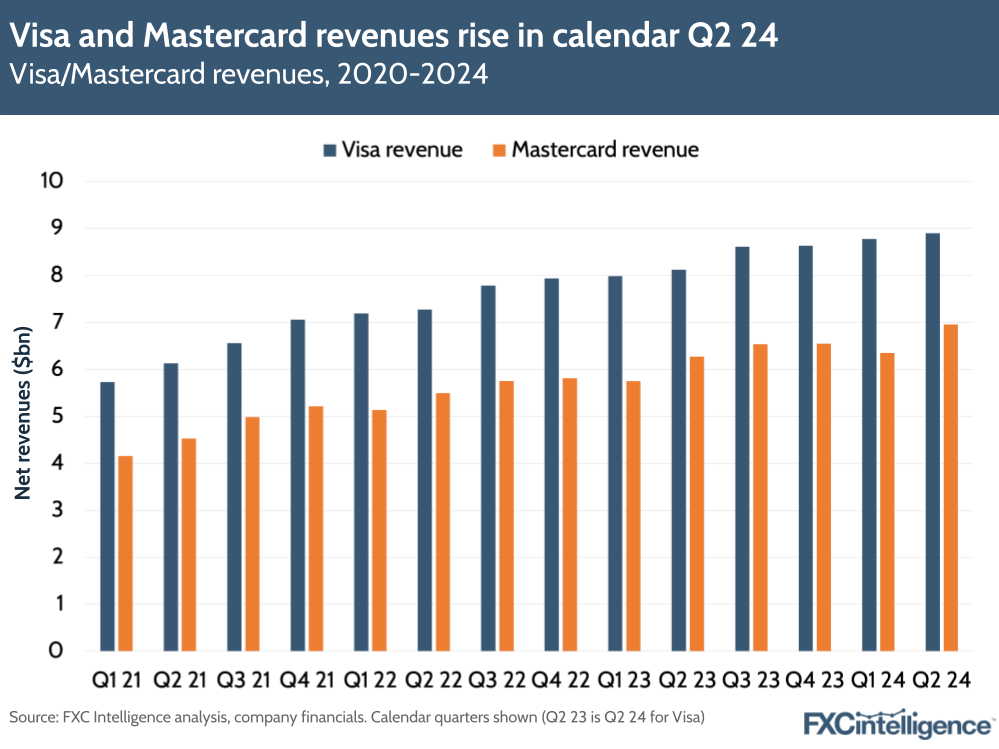

- Visa’s revenues rose by 10% to $8.9bn in its Q3 2024 results.

- Payments volume rose by 7% YoY, while processed transactions over the same period grew by 10%. Visa expects payments volume and processed transactions to grow at a similar rate to Q3 in Q4.

- Cross-border volumes remain a key driver for Visa, with cross-border volumes both in total and excluding intra-Europe transactions rising by 14%.

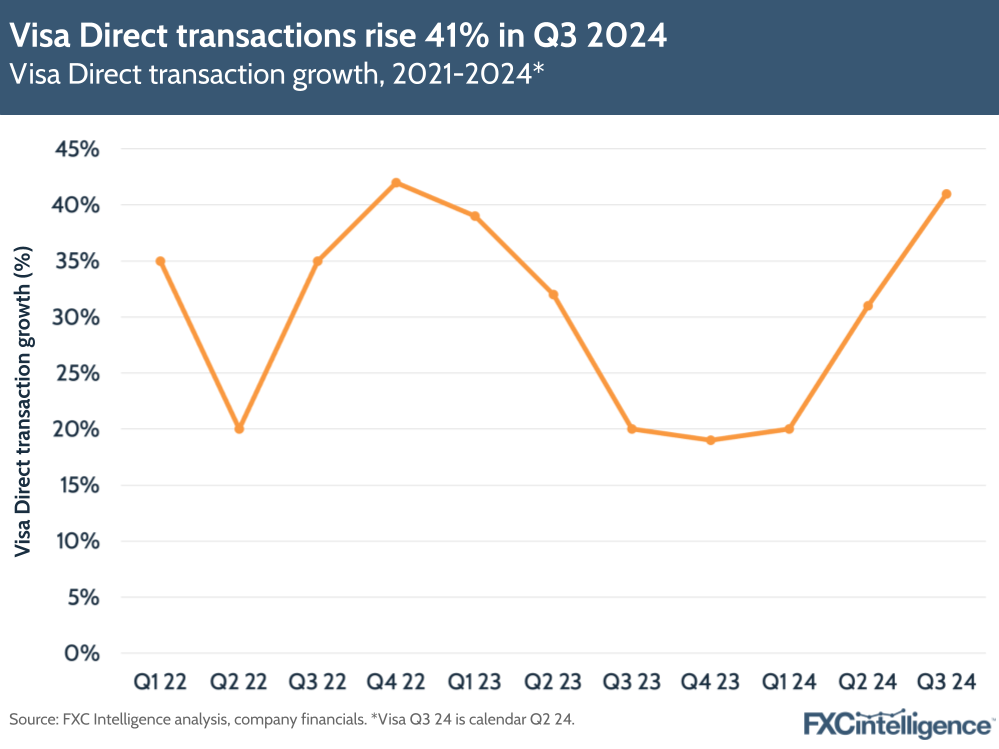

- Visa Direct transactions grew 41% year over year, to 2.6 billion, aided by growth in LatAm, particularly P2P apps.

- Commercial volumes were up 7% year-over-year in constant dollars.

- Visa’s share price fell by 4% after revenue fell short of expectations.

Highlights from Mastercard’s Q2 2024 results

- Mastercard saw Q2 2024 net revenue rise by 11% on a GAAP basis (13% on a currency-neutral basis) to $7bn, prompting its share price to rise by 3%.

- The company’s payment network net revenue increased 7% overall, or 9% on a currency-neutral basis.

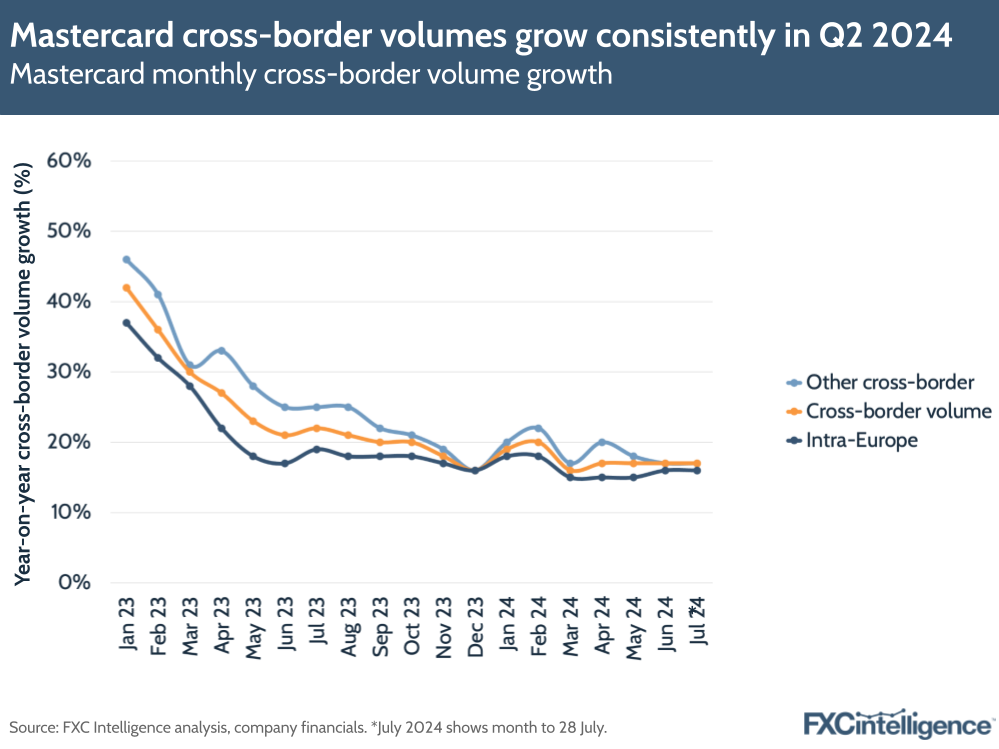

- Gross dollar volume was up by 9%, while cross-border volumes grew by 17%.

- Cross-border card-not present growth grew by 20%, while cross-border travel volumes grew by 15%.

- The company also saw more demand for value-added services and solutions, with net revenues for this area increasing by 18%, or 19% on a currency-neutral basis.

- Mastercard maintained that it will grow net revenues at the high end of a low double-digit range in Q3 2024, excluding acquisitions.

- Mastercard Move – the company’s wider portfolio of money transfer solutions, which includes its Cross-Border Services offering – expanded through a new deal with Nigeria-based Access Bank.

Visa’s cross-border volumes driven by ecommerce, Visa Direct

Visa’s cross-border volumes have continued to rise on the back of ecommerce growth. In particular, cross-border card-not-present volume growth was in the mid-teens, bolstered by retail (but excluding travel and adjusted for purchases made with crypto).

Cross-border travel volume growth was up in the mid-teens, or 157% indexed to 2019. While Visa said that the inbound Asia-Pacific Index improved by nine percentage points to 151% against 2019, outbound travel in Asia is recovering slower than anticipated at the beginning of the year, increasing by less than 1% (to 125% of 2019).

According to Visa, it is seeing a continued impact from some headwinds in Q1 2024. These included macroeconomic weakness in key markets like Australia and Mainland China, as well as some weakness in APAC currencies that is affecting consumer spending in some countries, particularly Japan. This is in addition to airline capacity that is still below 2019 levels, particularly in Mainland China and the North American corridor.

Chief Financial Officer Chris Suh said that ecommerce now makes up 40% of the company’s cross-border business, bolstered by growth in the teens during the pandemic. However, he did say that this growth has now begun to normalise and stabilise back to normal.

“With ecommerce being a bigger portion of the business, that’s a tailwind to the total cross-border growth,” said Suh. “We are confident that that will continue to be healthy relative to the domestic spend.”

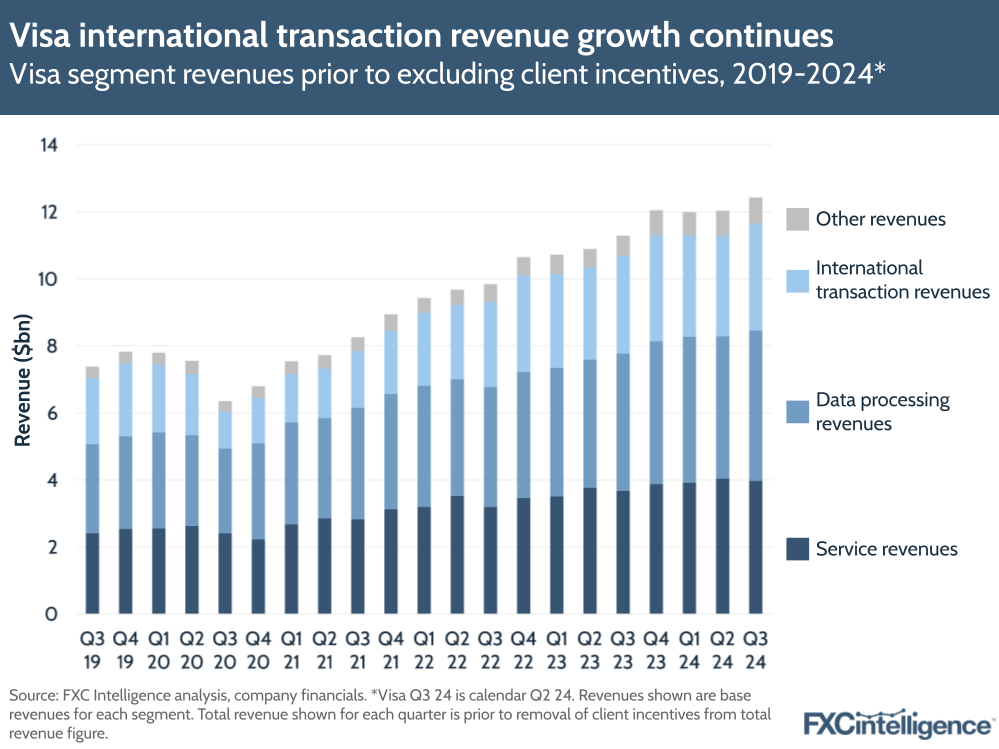

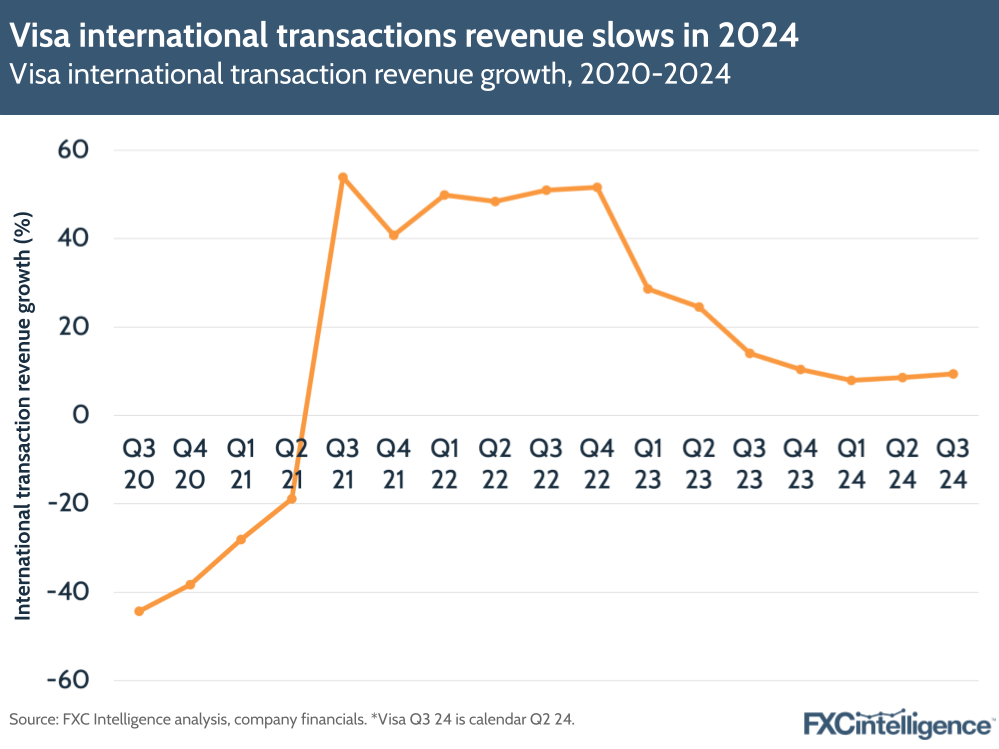

Supporting the “normalisation” post-pandemic, international transaction revenues were up by 9% versus the 14% cross-border volume rise, and this revenue segment continues to rise at a slower rate compared to the same period last year and in 2022.

Meanwhile, service revenues grew by 8% YoY; data processing revenues grew by 9%; and other revenues grew by 31%, driven primarily by consulting and marketing services revenue related to the Olympics, for which Visa is a sponsor and an official payment technology partner.

Suh also said that this growth figure was impacted as the company was lapping a period of higher currency volatility last year.

On the other hand, Visa Direct – the company’s B2B2X offering that allows payment companies to facilitate money transfers to cards and wallets around the world – saw a significant boost to growth this quarter.

Transactions through the platform grew by 41% to 2.6 billion, the fastest growth this service has seen since Q4 2022, with total P2P transactions nearly doubling. Central Europe, the Middle East, Eastern Europe and Africa was a key region driving this.

A number of significant Visa Direct deals were signed during the quarter, including with WorldRemit and Sendwave to aid their remittances services, as well as a renewed partnership with FIS to add “new flows capabilities”.

The company also gave an update on Visa+ – the company’s service that enables money to be sent between domestic P2P and B2C payment applications. The offering is now enabling sends between PayPal and Venmo and new providers continue to join the platform.

Visa also talked once again about the growing penetration of tap-to-pay, which the company sees as being crucial to digitalisation across ecommerce. CEO Ryan McInerney said that eight out of 10 Visa face-to-face transactions round the world are now contactless tap-to-pay, with more than 55 countries now at more than 90% contactless penetration.

The impact of the Paris 2024 Olympics on Visa

Visa has been the exclusive payments technology partner for the 2024 Paris Olympic games and Paralympic Games (having been a partner of the Olympic Movement since 1986).

Beyond providing support to 147 athletes across more than 60 countries and 40 sports, the company also added nearly 100,000 new merchant locations in France ahead of the event, with only Visa debit and credit cards accepted onsite at venues.

The company also launched Visa Go, a mobile app for people visiting the games that gives discounts and allows users to buy prepaid Visa cards, and implemented contactless payment acceptance across 3,500 PoS systems across 32 Olympic venues and 16 Paralympic venues.

McInerney spoke about engagement with Visa through marketing campaigns as well as Olympic and Paralympic-branded Visa cards, which (before the opening ceremony last week) had risen to nearly six million cards compared to five million the previous quarter.

As mentioned above, marketing and consulting revenues were a primary driver in 31% growth to Visa’s Other Services segment in Q3 2024. Though this still only accounts for around 9% of Visa’s revenue share, this segment has grown consistently faster than other segments since Q3 2023 and indicates growing demand for clients for consulting and marketing from the company.

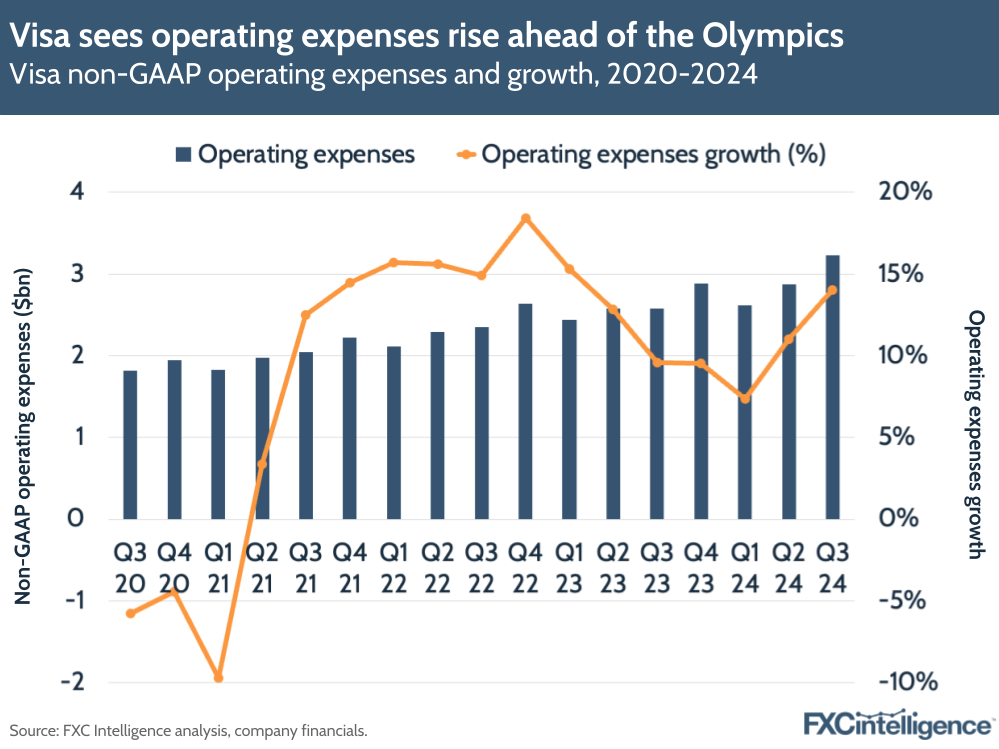

While Visa didn’t break down the impact on card transactions or cross-border volumes, the partnership has added costs for the company. Operating expenses grew 14% (which would be more than $3.2bn, according to our calculations), which the company said was due to increases in general and administrative, personnel and marketing expenses, including spending related to the Olympics.

Sponsorship of sports events has been a big focus for companies in the payments space, with Visa also sponsoring a Formula 1 team alongside Cash App, MoneyGram and Airwallex, as we discussed in our in-depth report on F1 payments sponsorships. We’ll see if Visa explains more of the impact from the Olympics in its next results.

Mastercard grows volumes, expands further into markets

Mastercard cross-border volume growth continues to remain solid at 17%, though this has decelerated slightly since last quarter (18%) and more significantly since the same period last year (24%).

The company noted that cross-border card-not present growth – which covers cross-border ecommerce – grew by 20%, while cross-border travel (which includes both card present and card-not present travel volumes) grew by 15%.

Other cross-border volumes continue to grow at a faster rate than intra-Europe volumes – 18% versus 15% growth, respectively in Q2 2024 – though in June 2024 the growth rates across these two segments came close to converging (16% for intra-Europe, 17% for other cross-border).

When asked about Europe and the country’s activity there, Mastercard executives said that intra-Europe cross-border transactions continue to be lower-yielding than other cross-border volumes.

However, the company is continuing to invest in the region, with executives saying that the pandemic has pressured some countries to “catch up” when it comes to digitalisation. In particular, they noted Germany and Italy as being countries where significant cash creates a significant opportunity to build partnerships and drive opportunity there.

Similarly, the company is growing investment and partnerships in Africa, where it has more than tripled acceptance locations in the last five years. In particular, the company has been looking to expand the reach of Mastercard Move – its portfolio of solutions for money transfers – making a new deal with Nigeria-based Access Bank to expand opportunities for cross-border payments for African businesses and consumers. Mastercard said the aim was to expand the programme to more markets in LatAm and APAC.

Mastercard executives didn’t directly reference Cross-Border Services, its global payments infrastructure that enables financial institutions to facilitate money transfers for people and businesses and which is contained within Mastercard Move. However, this segment has seen notable partnerships this quarter, including with Nairobi-based Equity Bank and core banking systems provider Datapro in LatAm.

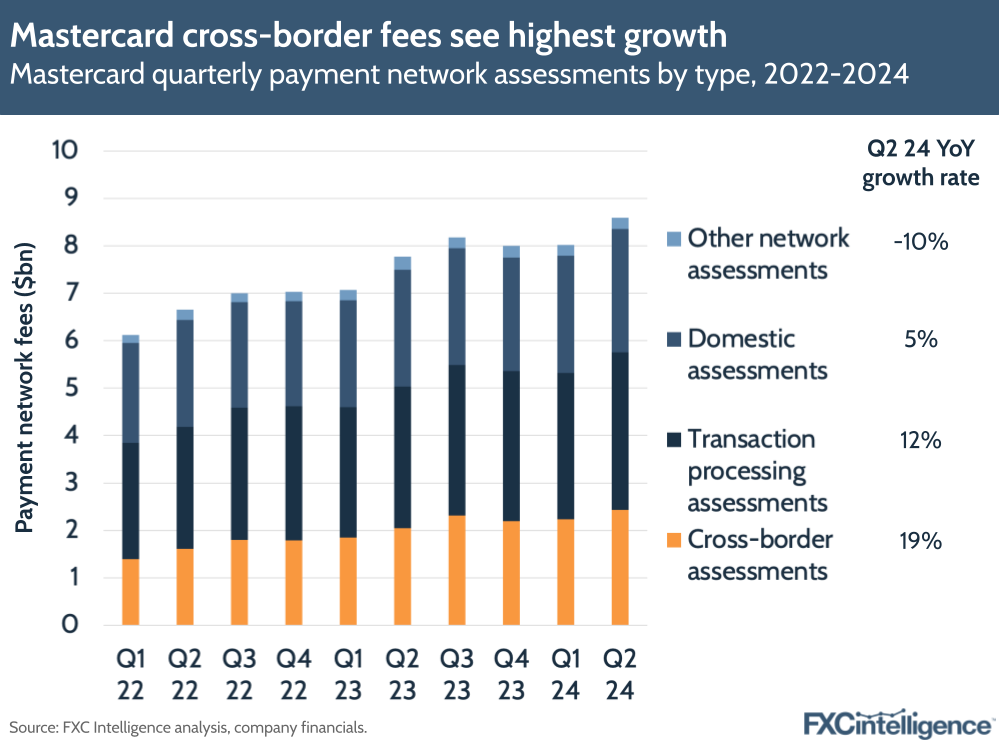

On assessments – the fees that Mastercard charges across transactions – these once again grew the fastest for the cross-border segment at 19%, followed by transaction processing assessments at 12%, while domestic assessments grew by 5%.

Though still smaller than the other segments, cross-border fees could soon be higher than domestic assessments if they continue to grow at a rapid rate. When asked about why domestic fee growth is slowing versus cross-border, executives said part of this could be due to their geographic mix and differences in growth in certain regions versus others.

Driving contactless spending and digitalisation

Reflecting a similar sentiment from Visa, Mastercard spoke at length about how it was looking to scale up contactless transactions across countries, with the company once again bringing up tokenisation – the process of replacing sensitive data in transactions (e.g. account numbers) with tokens to help simplify transactions at checkout.

The company also repeatedly talked about healthy consumer spending during the call, with strong labour markets as well as wage growth being seen globally, despite concerns around inflation and prices persisting. Executives also mentioned that moving towards a digital economy is helping empower more low and middle-income customers to spend more.

Rounding out other trends, open banking’s progress in the US was also mentioned, with executives saying that they continue to see the key use cases on this as being around lending, account opening and verification, but also acknowledged there were still difficulties around customers getting money back from transactions in a way that there isn’t with cards.