Western Union saw another mixed quarter in Q1 2025, with revenue falling -6% YoY to $984m on a reported basis due to slowing contributions from Iraq and changing migration patterns in Latin America. However, the company has continued to drive digital growth and push for diversification, including the acquisition of UK-based money travel provider Eurochange.

Western Union’s Consumer Money Transfers (CMT) segment declined -9% to $873m; excluding Iraq, this was down -2% on an adjusted basis. However, transactions overall grew 3% compared to the previous year, driven partly by strong improvement in the company’s branded digital transactions.

Overall operating income was down by -10% to $186.4m on the back of a -15% drop in operating income for CMT, though the company’s overall operating margin remained flat at 18%.

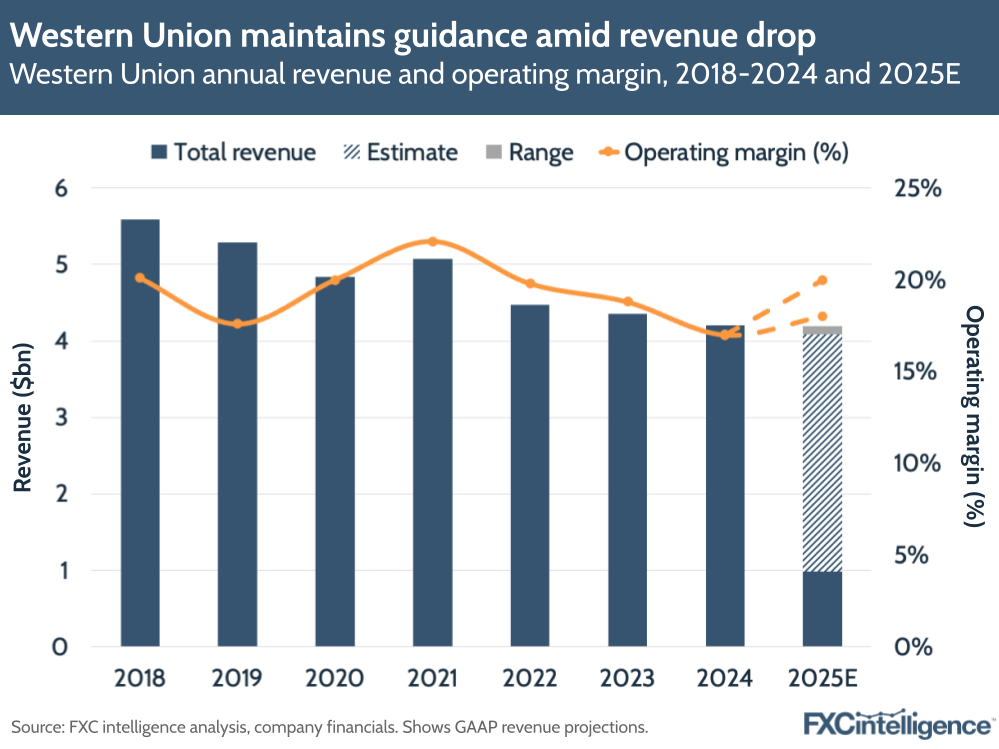

Despite macroeconomic conditions affecting results, Western Union continues to hold firm on it guidance, projecting GAAP revenue decline of around -0.5% to -3% to $4.09bn-4.19bn, though on an adjusted basis it expects revenue to range between a -2% decline and 0.1% growth.

Headwinds in Western Union’s core geographies stymie growth

Western Union continued to see headwinds due to changes in Iraq, where the company had previously reported a suspension on international transfers. This time it reported reduced contributions from the country, as well as a challenging comparison against the leap year, which led to its adjusted revenue decline of -2%.

Other headwinds included a slowdown in North American transaction growth (about 100 basis points lower than Q4 2024), as well as in Latin America and the Caribbean (about 200 basis points lower).

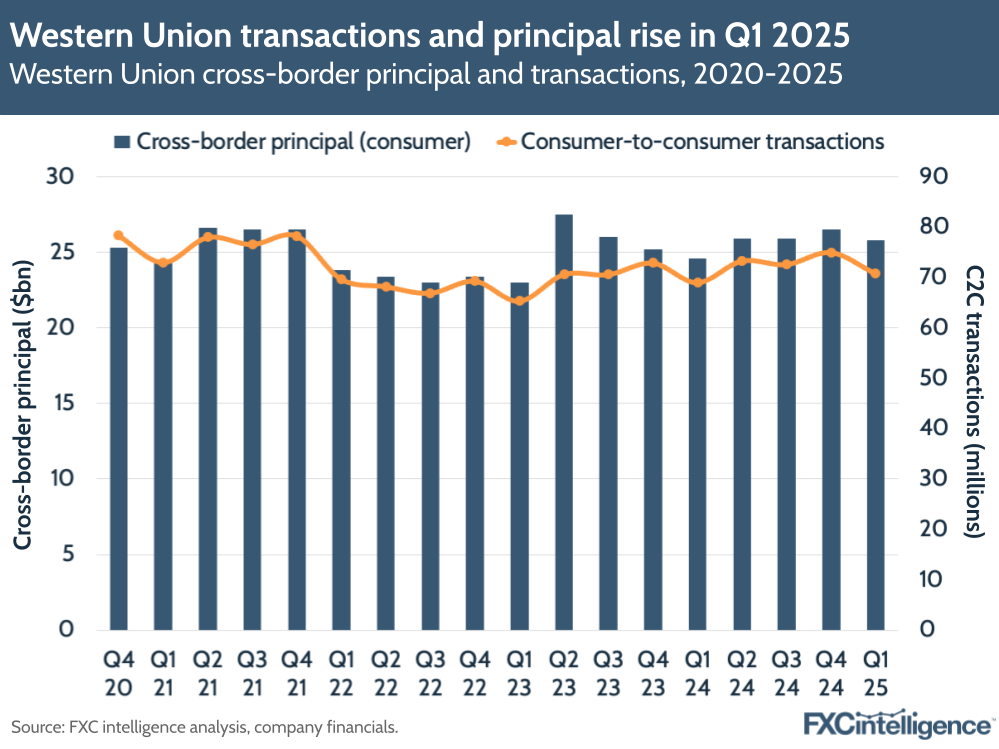

Despite the slowdown, the company saw a 3% rise in transactions, to 70.8 million, that drove a 5% rise in cross-border principal to $25.8bn. The quarter was the third in a row to see 3% transaction growth and the seventh consecutive quarter of 3%+ transaction growth for Western Union, with Western Union CEO McGranahan saying that the company had not delivered this level of consistent transaction growth “in over a decade”.

Amid declining revenue, Western Union is seeing strength in driving efficiency, with cash flow from its operations coming in at $148m, up 50% YoY, and capital expenditures down 30% to $24m.

Western Union’s ongoing shift to digital

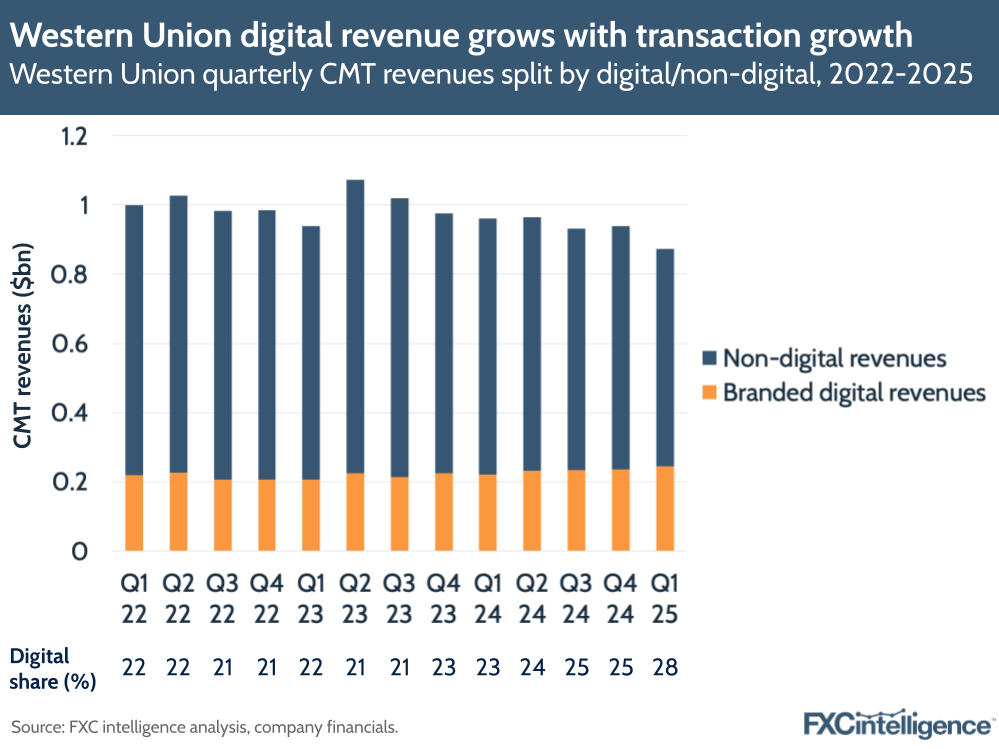

One area where Western Union has continued to drive change is in its branded digital business – its online and mobile channels for transfers.

The company’s branded digital business grew adjusted revenue by 8% and now forms 28% of CMT revenues – up from 23% in Q1 2024. This was the eighth quarter of double-digit transaction growth for Western Union’s digital business, driven primarily by rising transactions in Europe, the Middle East and APAC.

As a counterpoint, Western Union mentioned branded digital revenue growth was “muted’ by the relaunch of a loyalty program in the US, and expects this to continue in the second quarter. However, Western Union Executive VP and CFO Matthew Cagwin said the program will drive customer retention over time. The same is true of Western Union’s payout to account business, which saw 35% growth in Q1 2025, and though it comes with higher margins, provides for “much stickier customer relationships”.

It is worth noting that this growing share comes alongside weaker retail results in the Americas, where Western Union is underperforming as a result of slowing migration trends. However, Europe has been stronger, ultimately driving transaction growth for the quarter.

Western Union’s continued success in digital versus the decline in CMT revenues shows how digital transfers remain crucial for the company continuing as a leader in the space. However, the company is still trying to win back gains in the retail market.

“We continue to believe there are numerous compelling opportunities for our retail business to recapture share, and we look forward to executing on those opportunities as we work to return our retail business to growth,” said Cagwin during the earnings call.

Diversifying Western Union’s business is key to growth

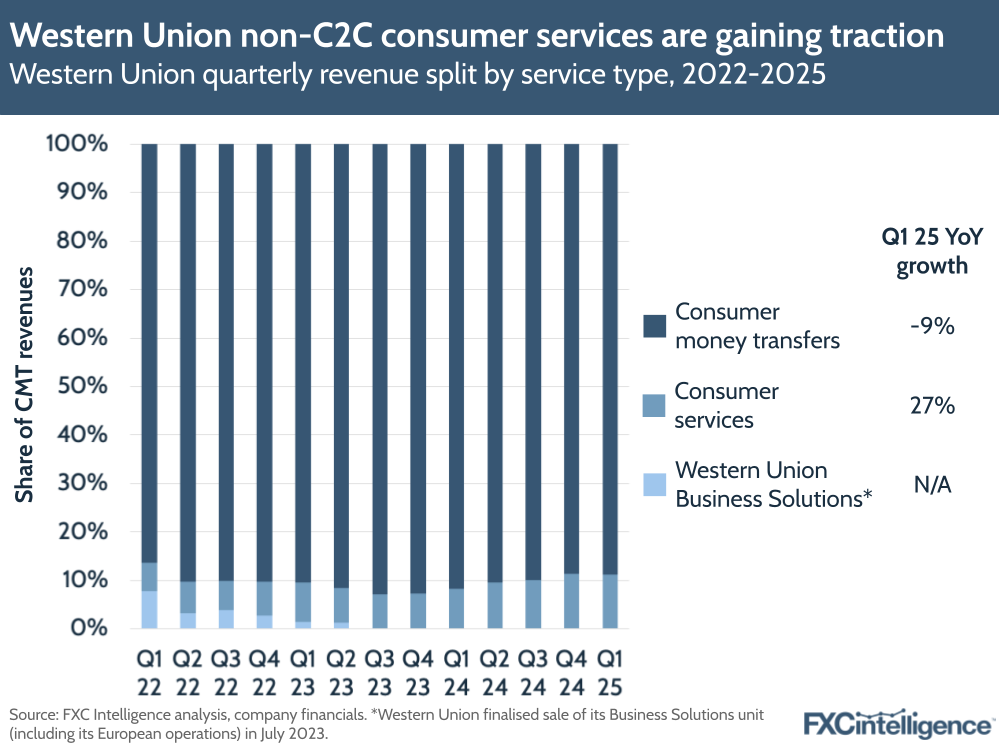

CMT still makes up the bulk of Western Union’s operations, with around 89% of the share of Western Union’s total revenue for the quarter, but the company’s separate consumer services segment continued to see solid growth in Q1 2025 at 27% YoY.

This was on a GAAP basis however, with this segment declining -3% YoY due to softness in consumer bill payments in Argentina and a delayed media contract. That being said, on a GAAP basis Consumer Services made up 11% of Western Union’s revenues in Q1 2025, versus 8% the previous year.

The addition of Eurochange – which currently has 200 owned locations and 100 partner locations in the UK – won’t have a seismic impact on revenue initially, but will help the company expand its FX services and could accelerate its money transfer business. Based on trailing 12-month revenue, the company believes Eurochange will add roughly 1% revenue growth to Western Union’s annual figures this year.

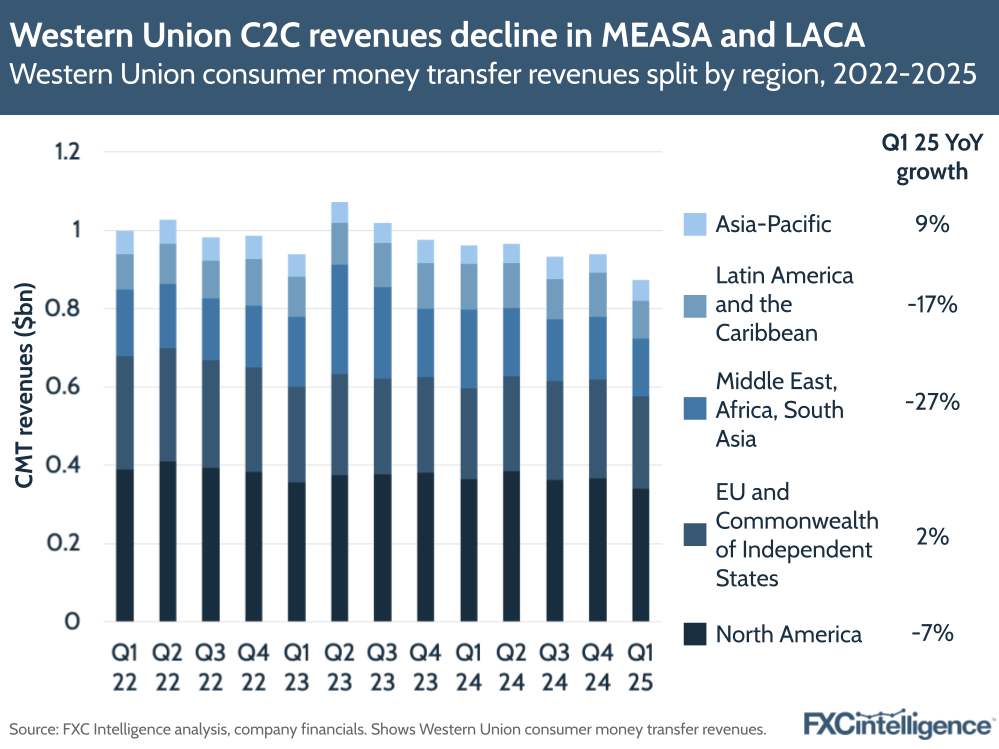

Elsewhere, Western Union broke down its C2C revenues by geographic share, with North America revenues continuing to take the highest share at 39% in Q1 2025, followed by Europe and the Commonwealth of Independent States (EU & CIS) at 27%; the Middle East, Africa and South Asia (MEASA) at 17%; Latin America and the Caribbean (LACA) at 11% and the APAC region at 6%.

Based on revenue calculated from these shares, North America revenues declined by around -7% to $340m in Q1 2025, likely due to the slowdown in migration patterns that the company said had led to a volume decline in Mexico, though excluding Mexico transactions from the US to Latin America were up 2%.

As McGranahan mentioned during the earnings call, currency fluctuations on the US dollar (such as the ones that have rocked the market in April) can also play a role on consumers choosing to send money back home from the US, as a weaker dollar buys fewer pesos.

“The benefit of a weaker US dollar on inbound is not nearly as much as the implication of it on the outbound,” he said.

Equally, Western Union mentioned that migration between Latin American countries has also slowed during the quarter, which may have been reflected in LACA revenue declining -17%. Based on revenue share, MEASA saw the biggest decline at -27%, which may have been impacted by a reduced contribution from Iraq, though Western Union mentioned seeing “a lot of momentum” in the Middle East on the back of recent partnerships.

Excluding Iraq, Western Union said that Europe, the Middle East and APAC all saw double-digit transactions in Q1, with these three regions together accounting for 50% of CMT revenue. EU & CIS revenues rose 2%, while APAC revenues rose 9%.

Contrary to its American business, Western Union also noted a shift to positive growth for its retail business in Europe, where it had previously seen a blow from its suspended service in Russia, which it hopes to bolster through added FX services through Eurochange in the UK.

Looking back now at Western Union’s Evolve 2025 strategy – launched in October 2022 as a path to profitable growth – it is clear to see that macroeconomic impacts have made its journey to growth a lot harder. Back in October 2022, it had forecast 2% revenue growth by 2025, for example, which the company will achieve if its revenues reach the higher end of its adjusted range for 2025.

Continuing to build traction in markets outside the Americas and growing its digital business will be key for Western Union as it competes with other players in the market.

How does Western Union’s FX pricing compare to other money transfer providers?