Western Union has announced its Q2 2024 earnings, with uneven results where regional and other headwinds have offset key gains to produce a top-line dip.

The company saw revenue drop by -9% YoY to $1.07bn, while consumer-to-consumer revenue reduced by -10% to $965m. The company also reported a drop in operating margin to 17.9% – almost three percentage points lower than Q2 2023 – while cross-border principal also saw a decline.

However, declines were focused on specific regions, led by Iraq where the company is lapping short-term gains. These declines also hide underlying growth in some areas, most notably in the company’s digital business.

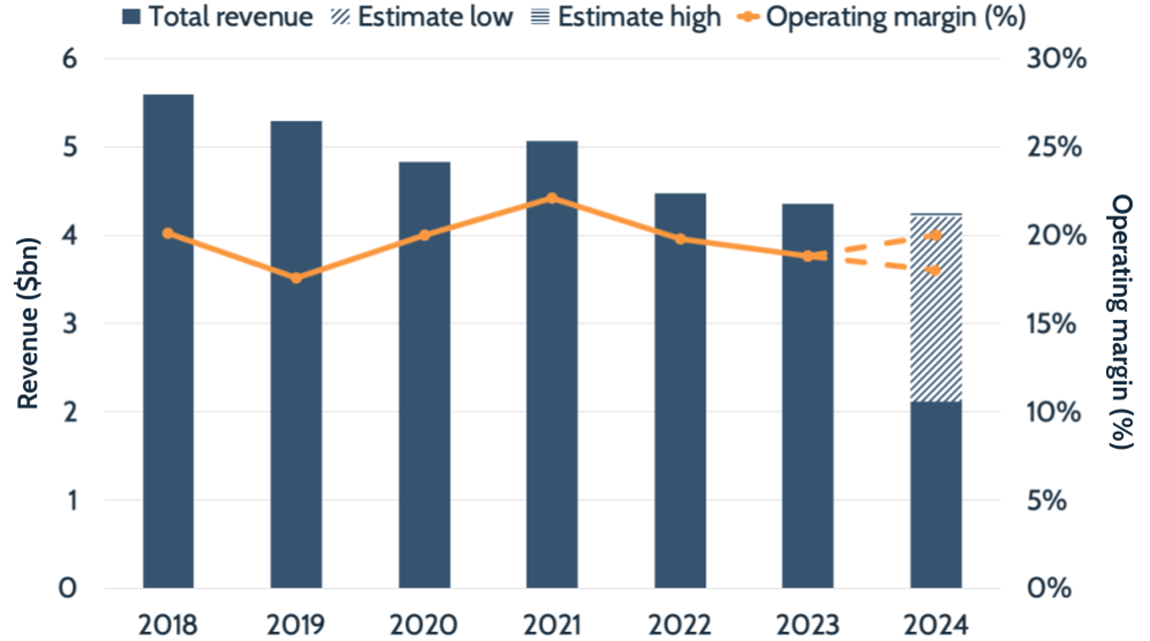

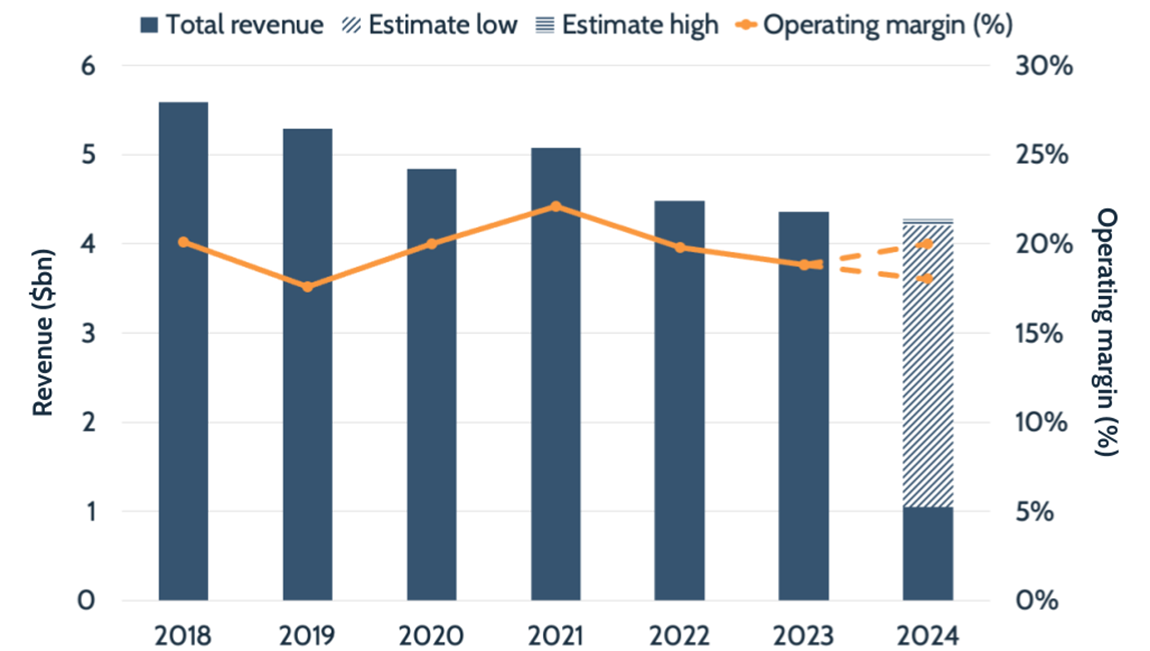

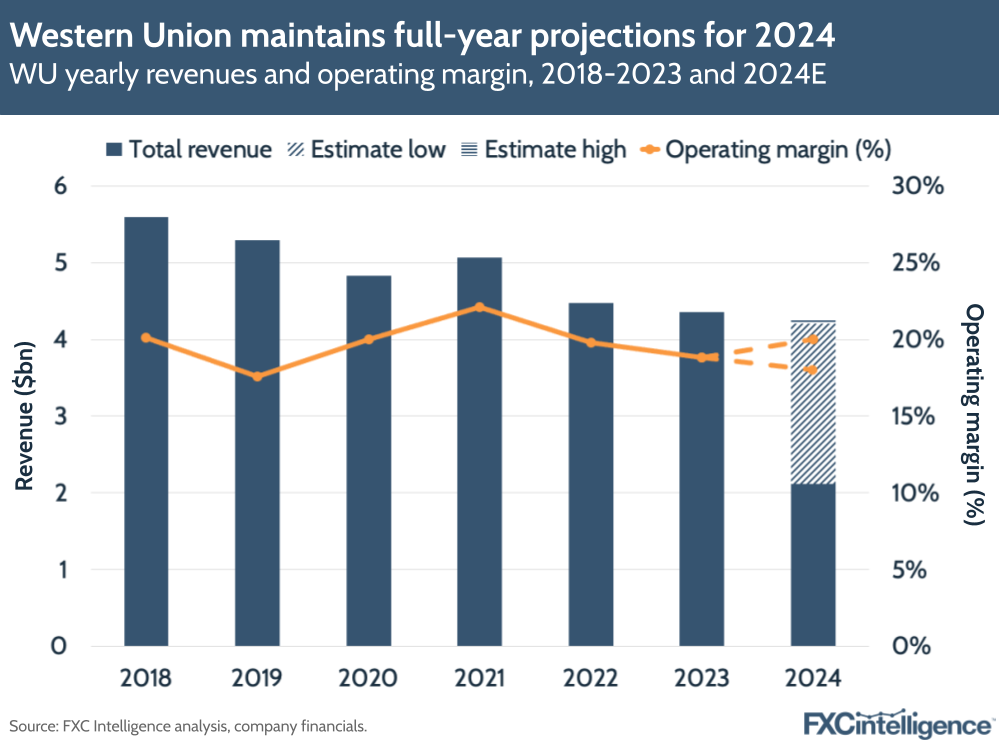

Despite the results, Western Union reaffirmed its previous FY 2024 projections, having previously increased these in Q1 2024. The company continues to expect GAAP revenue of $4.1bn-4.2bn for the year, with an operating margin of 18-20%.

It continues to focus on its Evolve 2025 strategy, which places an increased focus on long-term growth over short-term gains as it updates both its retail and digital offering. The company also reports that it has begun to gain global market share again, citing World Bank data, after a period where it was seeing sustained declines, although has not specified which corridors are driving this.

It is also shifting to focus less on absolute increases in endpoints and more on improving customer experience, which has prompted an increase in the number of direct connections with banks, wallets and real-time payout networks, rather than using aggregators.

CEO Devin McGranahan also pointed to the “stability” Western Union has now achieved in its core operating business, adding that the company could “execute an M&A transaction” within “three or four quarters” off the back of this.

Iraq proves to be key headwind for Western Union in Q2 2024

Western Union cited several headwinds as the cause for its revenue decline in Q2 2024, among which was the sale of Western Union Business Solutions, now operating as Convera. However, the company only saw $14.3m revenue from this in Q2 2023 as the sale process was already well under way, making this a relatively minor contributor to the overall decline.

The company also cited the global increase in average cost to send remittances.

More significant, however, is the headwind provided by Iraq, which a year ago produced short-off gains for the company as a result of a change in Iraqi central bank policy.

Although it was expected that this would create challenges for YoY performance, this proved to be a significant headwind this quarter, with revenue from Iraq dropping from $118m in Q2 2023 to $34m in Q2 2024 – a -71% decline.

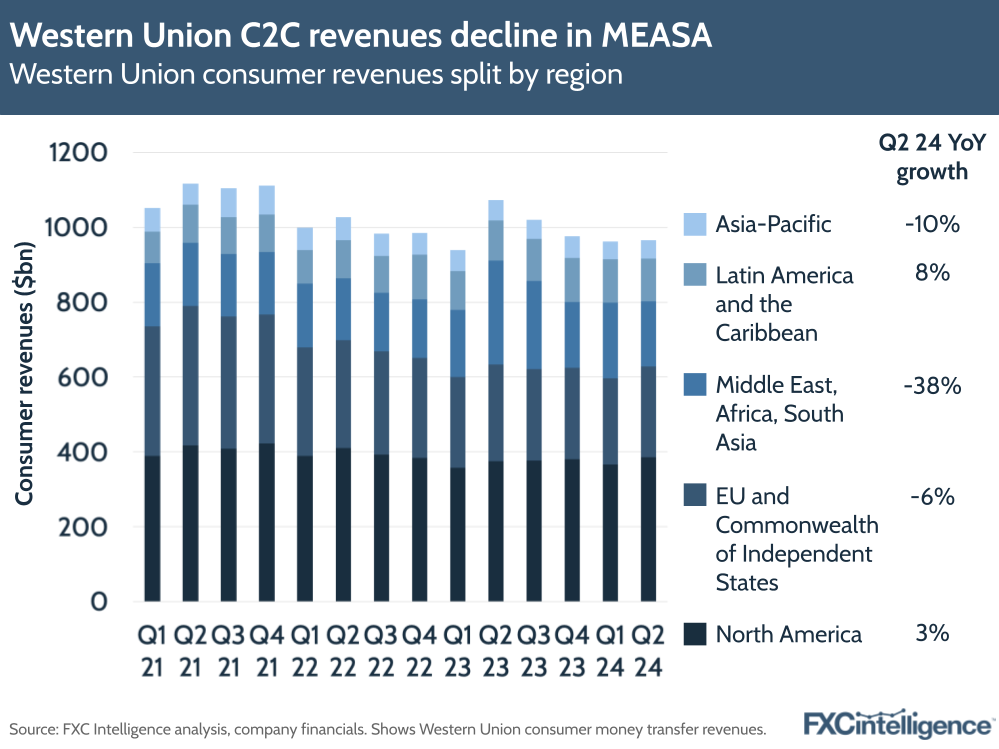

The company reports that Iraq alone reduced Western Union’s adjusted revenue growth rate by -7%, meaning total adjusted revenue growth excluding Iraq was flat in Q2 2024. However, while total revenue excluding Iraq was not as significantly impacted, it still saw a decline of -2% YoY. Iraq also contributed to steep declines in the wider Middle East, Africa and South Asia region, which saw C2C revenues drop by -38%.

Nevertheless, Iraq was by no means the only market to contribute to the company’s top-level decline. Both Asia-Pacific and Europe and the Commonwealth of Independent States both also saw reductions, shrinking by -10% and -6% respectively.

Only two regions, North America and Latin America and the Caribbean, saw increases this quarter, at 3% and 8% respectively, and no regions reached double-digit growth.

Western Union sees drop in send amounts despite transaction rise

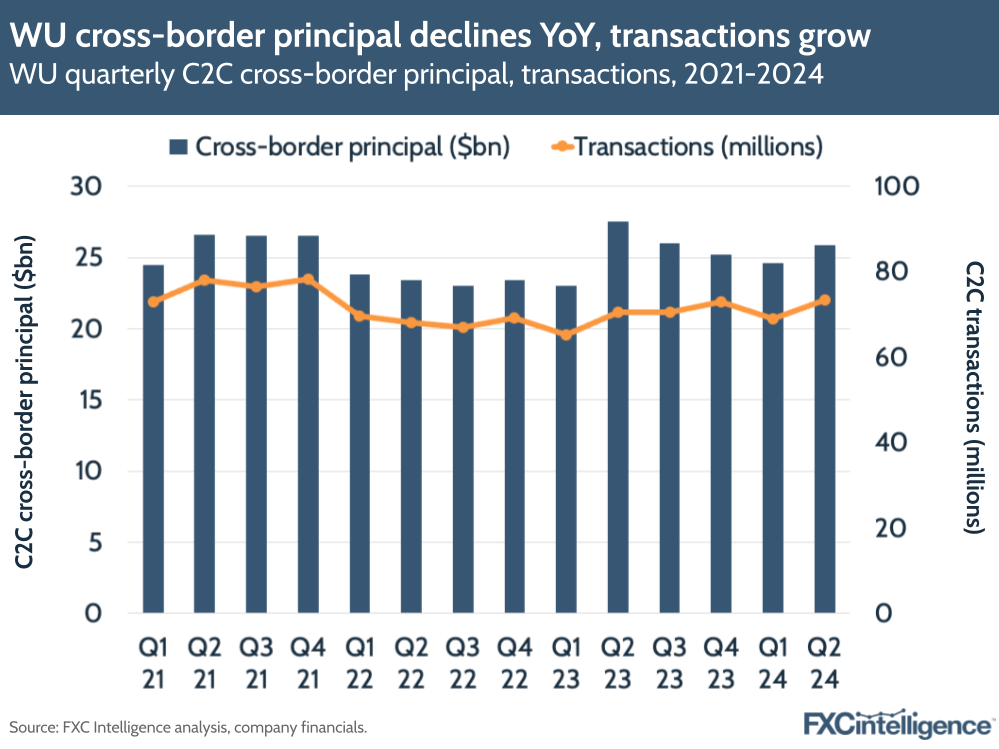

Q2 2024 also saw C2C cross-border principal decline -6% YoY to $25.9bn, bringing an end to a four-quarter growth streak. However, transactions saw a 4% rise – 5% excluding Iraq.

This is the sixth quarter in which the company has seen a YoY growth in transactions and is also the first period of sustained transaction growth since 2018, except for the period comparing to Covid-related declines.

However, this means that although the company is seeing customers send more frequently, they are doing so with lower average send amounts, and while this has only been the case this quarter, this will be a key metric to monitor to see if it becomes a longer-term trend.

Digital sees gains despite wider declines

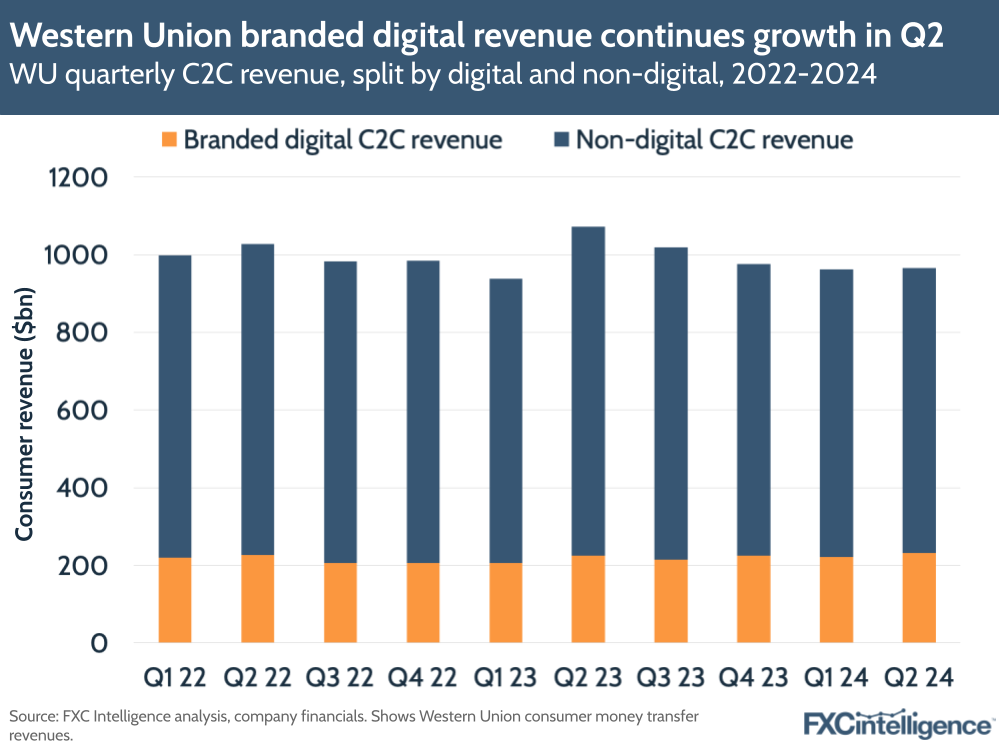

One of the strongest areas for Western Union in Q2 2024 is its digital business, where the company has previously stumbled.

This quarter, branded digital revenues accounted for 24% of C2C revenue – its highest share since Western Union began reporting the metric. Branded digital revenue also increased 5% on a reported and 7% on an adjusted basis in the quarter, totaling $232m.

The company also saw increased gains in digital transactions, which grew 13% YoY – nine percentage points more than transactions overall. Digital transactions now account for 31% of all Western Union transactions.

In support of this, the company is continuing to make improvements to its branded digital offering, where it has already rolled out a new app homepage and a modernised user experience and interface. These updates, supported by increased use of machine learning to boost digital conversion, have contributed to a 13% uplift in conversion rates.

Western Union in particular pointed to Australia as a key example of its success in the digital space, where digital transactions grew 30% YoY in Q2 2024 while revenue increased by 14%. The company also reports Australia having a 20 percentage point-higher conversion rate than any other country in the APAC region.

Consumer services shows growth beyond remittances

Beyond remittances, Western Union has also been growing its consumer services business, which sees it offer solutions including bill payments, digital wallets, retail money orders, foreign exchange and prepaid cards in some markets, including Brazil, Italy, Singapore and the US.

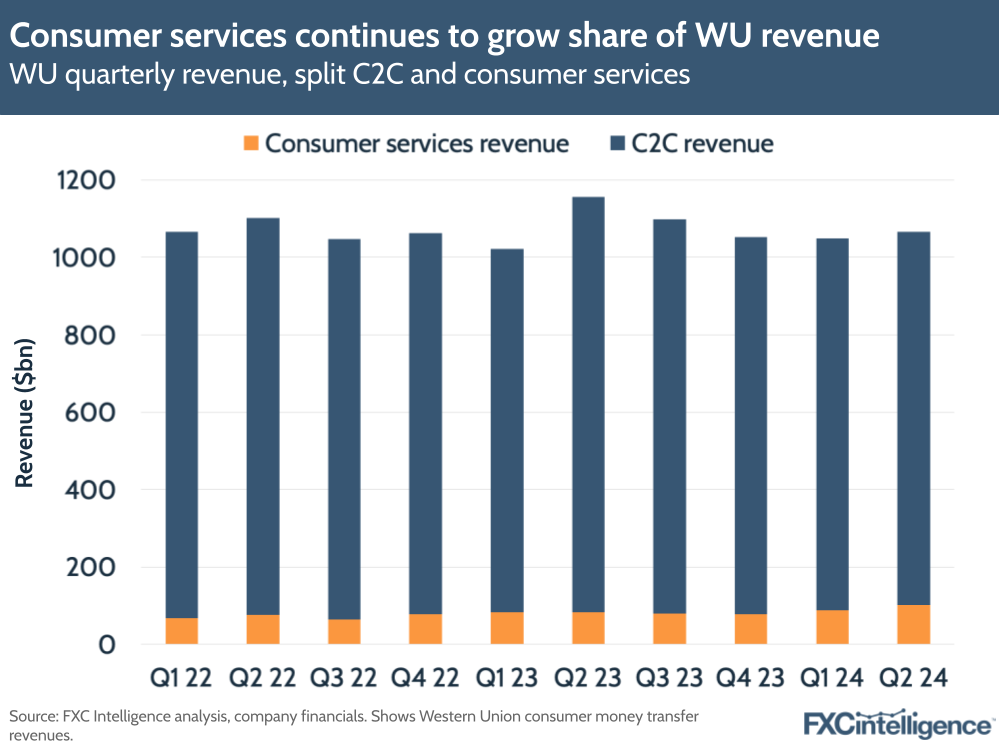

While this represents a much smaller segment of the business than its consumer-to-consumer payment services, it is seeing much more acute growth. Consumer services saw 14% revenue growth on an adjusted basis in Q2 2024 and 21% on a GAAP basis, making this one of the segment’s strongest-growing quarters to date.

The outsized growth relative to the rest of the business also means that consumer services are taking a growing share of the business overall. Consumer services accounted for 9.5% of Western Union’s Q2 2024 revenues, with C2C revenue accounting for the remaining 90.5%.

By contrast, in Q2 2023 consumer services accounted for 7.1% of the company’s revenue, while in Q2 2022 it accounted for 6.7%.

How does Western Union’s pricing compare to other money transfer providers?