Several recent valuations have seen key cross-border payments companies’ potential sale price move, although there is still a gap for many between now and their pandemic highs. What does it tell us about the potential IPO landscape over the next year or so?

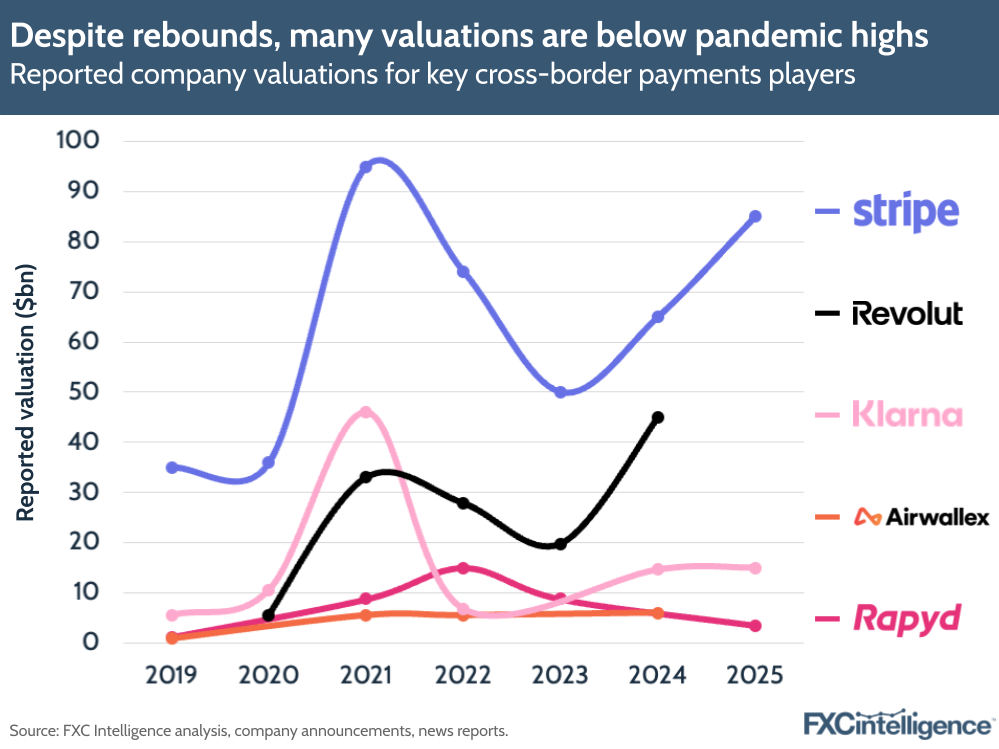

For many mature but not-yet-public fintech companies, there has been a very similar shape to their recent valuations: a steady rise that turned into a rapid jump during the pandemic, followed by a sharp contraction and now some form of rebound.

For some companies in the payments space, that rebound has been very pronounced. Having seen its valuation peak at $95bn in 2021 before dropping to a low of $50bn in 2023, last week Stripe was reported to be in talks for a shareholder sale that could see the company valued at $85bn or more – the closest it has come to its former high.

Revolut, meanwhile, has managed to outperform its 2021 valuation of $33bn. Despite dropping to $19.8bn in 2023, in 2024 it reported that it had received a $45bn valuation following the receipt of its long-awaited UK banking licence.

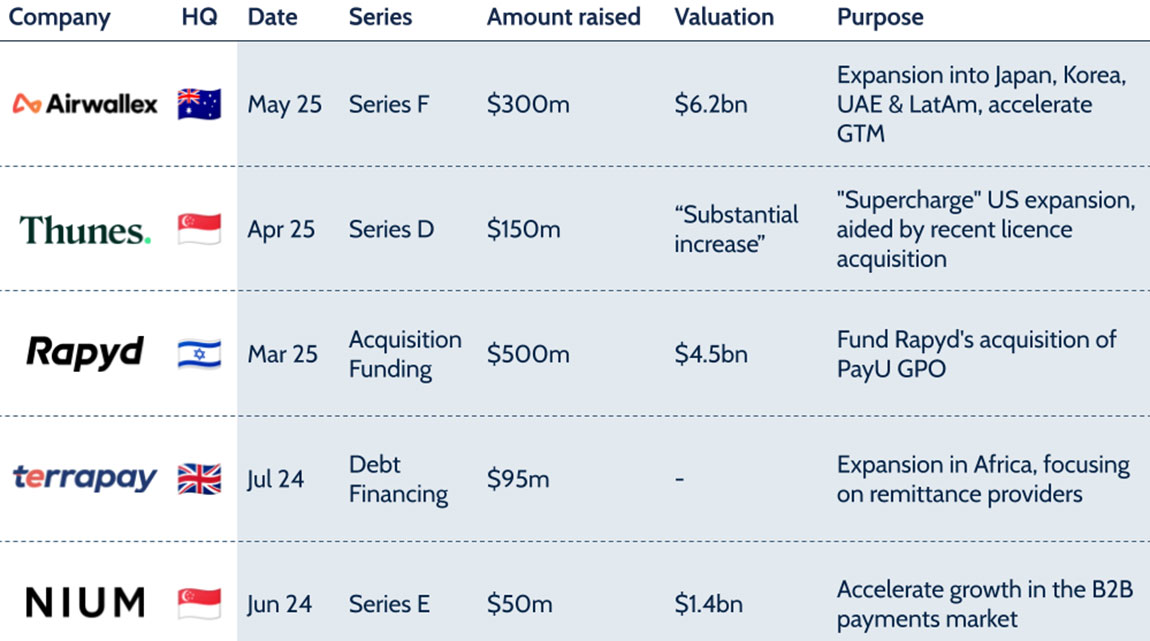

For others, the curve has been more muted. Last week Rapyd was reported to be in talks to raise capital at a $3.5bn valuation, down from its $15bn high in 2022 and still below 2023’s $8.75bn. The company did not announce a valuation in 2024, so it may have been lower at that point, but it still suggests the company has more upward trajectory to come before it considers an IPO.

Meanwhile, it was reported this month that Klarna was targeting a US IPO in April at a valuation of $15bn – well below its 2021 peak of $46bn, although a rebound from its 2022 post-peak low of $6.7bn.

Klarna’s decision to make its public entry well below its previous peak reflects a dilemma many of these now highly mature players are facing. In other circumstances they would have had IPOs several years ago, but those that have not regained previous valuations are now facing an economic reality where the conditions may never put them back at those highs.

Meanwhile, those that have are forced to ask if the current conditions will hold, or if better options lie ahead. For such companies, there will be a temptation to make the move now, particularly given the tough macroeconomic conditions that some public players such as Corpay have flagged in their latest earnings.

Revolut has been the subject of growing speculation about an upcoming IPO, as has Stripe, although the latter’s exploration of a secondary shareholder sale is a strong indicator that this remains some time off. For others, there is still some value to gain before an IPO is likely to look attractive.