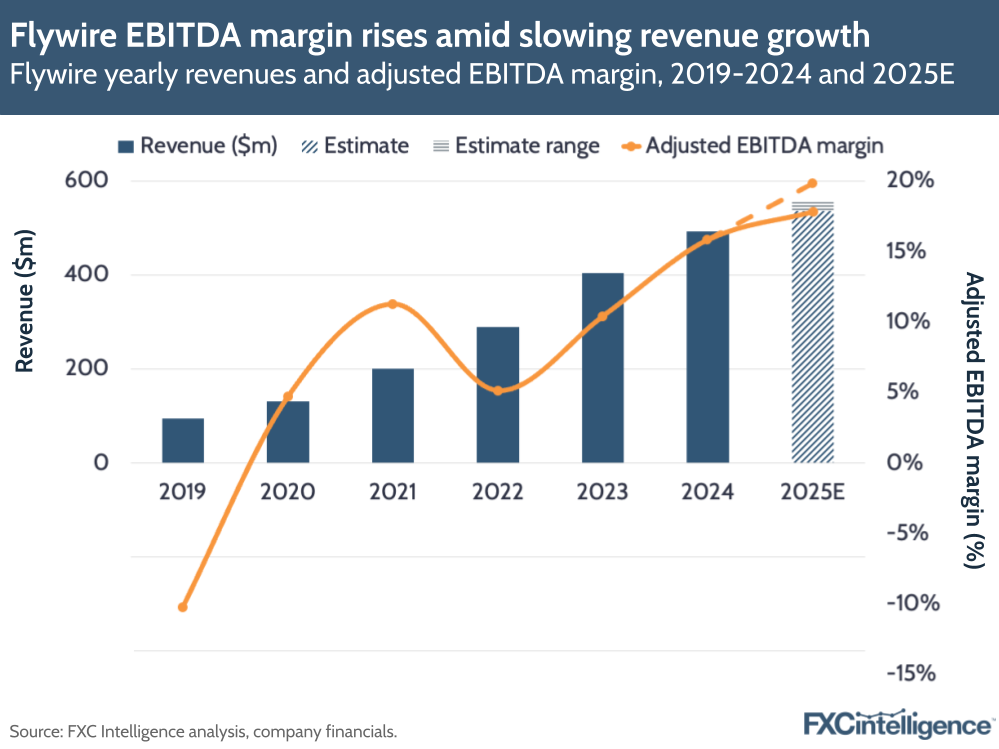

Payments processor Flywire saw revenue rise 17% to $118m in Q4 2024, driving full-year growth of 22% to $492m. This was behind expectations for the year, mainly due to a slowdown in Flywire’s core education segment as a result of changes to student visa policies in Canada.

As part of an ongoing strategy to expand its travel vertical, Flywire announced it is acquiring Sertifi – a software and payments platform focused on hospitality businesses – for $330m. The company also mentioned a restructure that it said would impact approximately 10% of its employees as it seeks to cut costs while targeting growth through investments. Investors responded negatively, with Flywire’s share price falling significantly the day after its earnings.

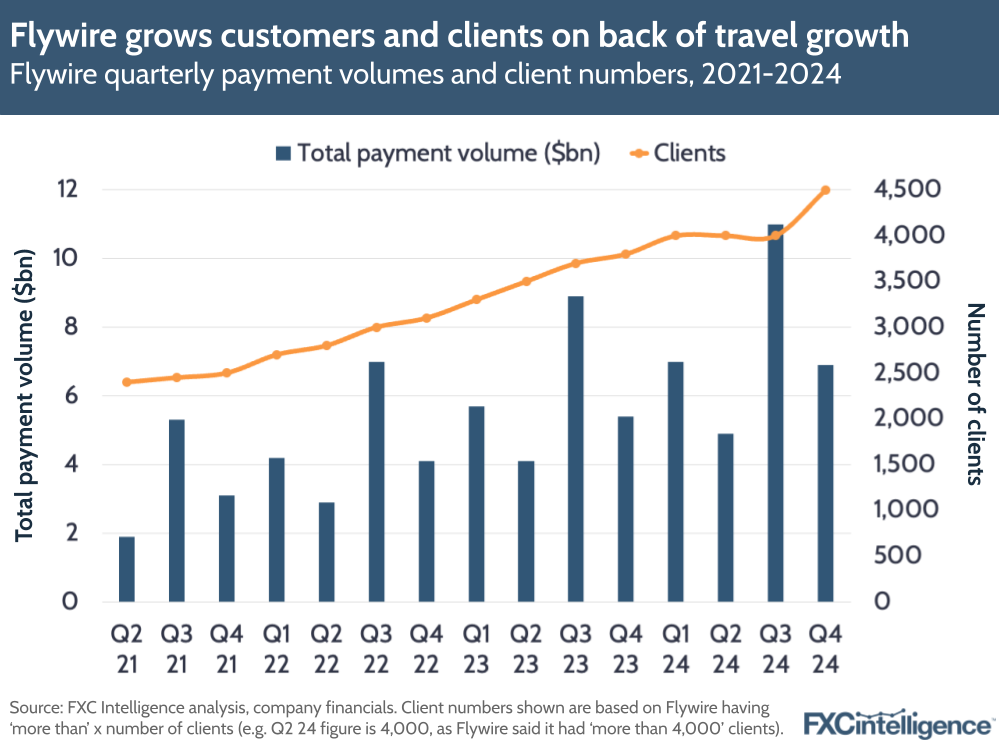

Having said this, Flywire’s EBITDA for the full year rose 85% to $78m – the midpoint of its expectations – and giving a margin of 15.8%. The company also grew its number of clients to over 4,500 (compared to over 3,800 in Q4 2023) and saw total payment volumes increase by 24% to $29.7bn.

Flywire sees education headwinds but strong travel and B2B growth

Flywire has continued to build out its education business, with the company seeing new client wins in the UK and enhancing its relationships in India and China. US education revenues grew 13%, while the rest of EDU (spanning Flywire’s remaining education payment services across other geographies) grew 26% over the year.

However, total revenue growth was impacted more than expected in Q4 by lower volumes as a result of changes made to student visa policies in Australia and Canada that have reduced the number of international students coming to these countries. In particular, Flywire’s Canada business declined 35% in 2024 on the back of the country adding a new cap to its student intake.

Though the company noted the impact of these visa policy changes, Flywire said other countries continue to welcome international students and it continues to push for adoption of its student financial software with a new sales strategy in the US.

On the other hand, Flywire’s travel vertical grew organically by more than 50% in 2024, driven by a 15% rise in new client signings, scaling its sales team and entry to new markets such as Indonesia and Chile. It has also acquired Sertifi – a payment processor focused on luxury hotels. Flywire believes it can cross-sell its products to Sertifi’s customers, creating an incremental multi-billion dollar volume opportunity.

B2B and healthcare accounted for 3% and 6% of revenue share respectively, though the former has grown its share and is now being broken out as a separate vertical from travel. Though its smallest contributor, B2B saw the fastest revenue growth out of all segments at 69%, with Flywire having bolstered the segment through the acquisition of Invoiced earlier in the year.

Travel has now become Flywire’s second-largest segment (when taking education as a whole), with 13% revenue share compared to 7% two years prior. Meanwhile, Flywire’s US education segment has declined its share of annual revenue, from 30% in 2022 to 24% in 2023 and 23% in 2024. Education payments beyond the US are still a core driver, with 54% share in 2024, though this is down from 55% the year before.

Flywire sees shift in revenue mix

Flywire continues to see its strongest growth in transaction-based revenues, which rose 24% and accounted for 83% of total annual revenue, versus 12% growth for platforms and other revenues. However, headwinds and efforts to diversify are also changing Flywire’s geography mix.

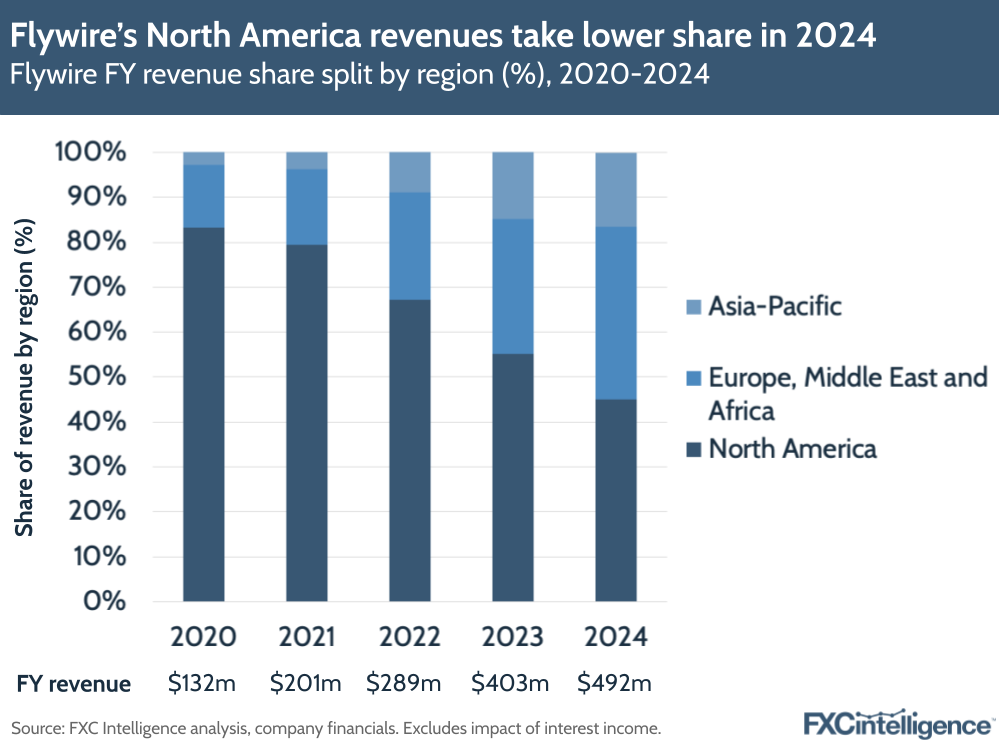

In particular, revenues from North America-based clients declined in 2024 by -0.4% to $222m, meaning this region accounted for less than 50% of Flywire’s revenues for the first time. Meanwhile, Europe, Middle East and Africa (EMEA) revenue rose 56% to $189m, taking 39% of share (up from 30%), while APAC rose 37% to $82m, taking 17% share (up from 15%).

Both EMEA and APAC saw strong travel growth, while the former (along with the UK) saw 50% YoY revenue growth in the education segment and helped combat headwinds in other regions.

Flywire’s 2025 outlook and restructure

Going forward, Flywire said that it anticipates FX-neutral GAAP revenue growth of 9-13% YoY, which would bring its revenue to $536m-556m. It also expects its EBITDA margin to rise between 200 bps and 400 bps, giving a margin between 17.8% and 19.8%, which by our calculation would give a 23-42% increase in EBITDA to $96m-110m.

The company did mention that it expects Sertifi to add $35m-40m to its full year revenues in 2025 (highlighting the importance of this acquisition for its growth), with gross margins similar to Flywire’s core business for the year. It expects Sertifi to have positive adjusted EBITDA, but that this percentage will be lower than Flywire’s overall adjusted EBITDA margin as Flywire invests to grow the combined business.

This represents a more conservative outlook than 2024, with the company continuing to expect strong growth in EMEA education, travel and B2B, but a 30% decline in Canada and Australia, where new visa rules are beginning to affect demand.

The company also said it was taking a review of its products and services to target efficiencies and cut costs, including the aforementioned restructure that it said would impact approximately 10% of its workforce (in total, Flywire’s workforce spans 1,300 employees, according to the latest figures on its website).

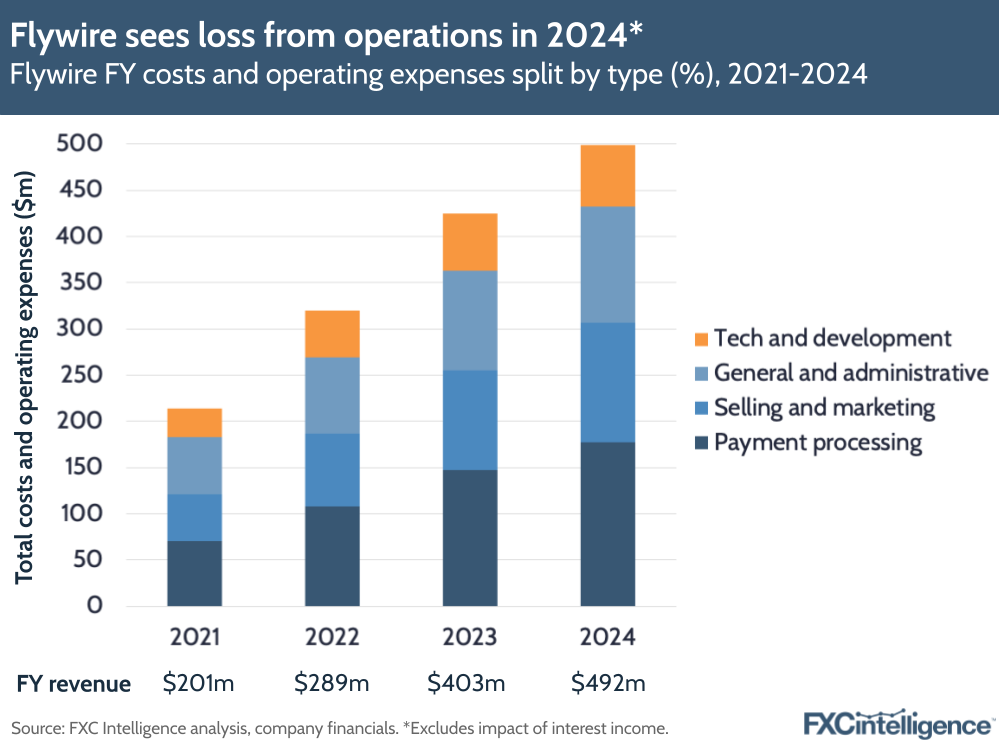

The costs of deploying Flywire’s services have continued to rise over time, with total operating costs rising 18% in 2024 to reach $499m. When excluding the impact of interest income – which helped drive net income of $2.9m for the company in 2024 – Flywire’s total operating costs continued to outweigh revenue during this period.

With profitability clearly front of mind for Flywire, the company has already begun diversifying its mix to frontload new geographies and markets beyond its core education offering. Given its more conservative estimates for 2025, it is likely to still be feeling the impact of headwinds in this segment for some earnings calls to come.