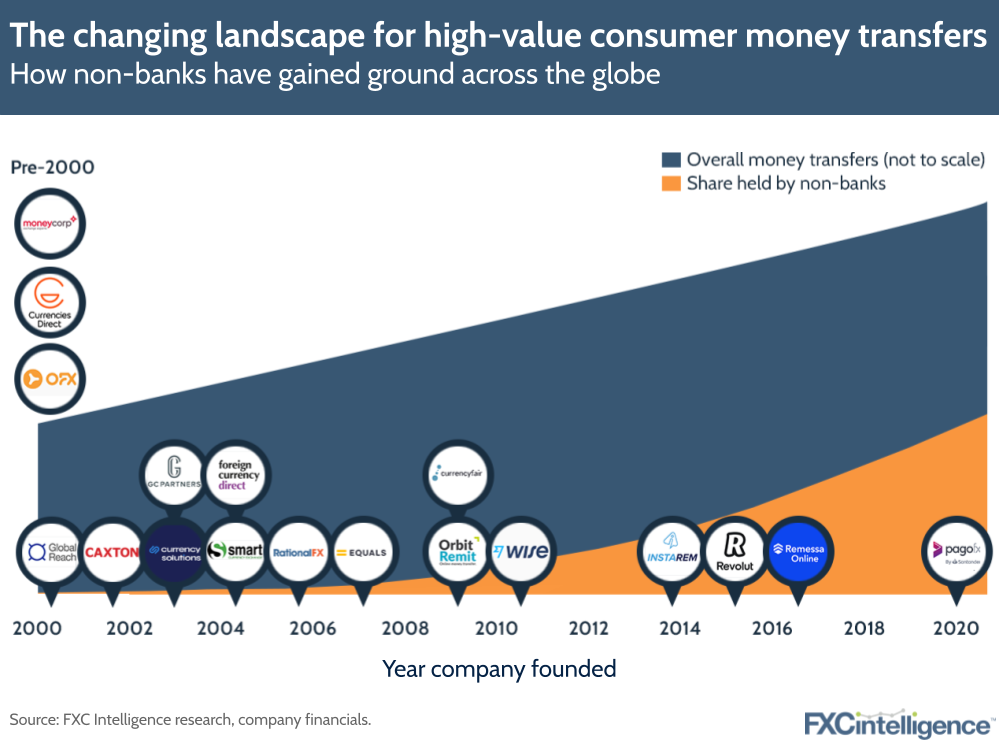

In the past few decades, the behaviour of high-end consumer money transfer customers – such as expats, overseas property buyers and investors – has changed significantly as, pandemic aside, the world has become much more open. Banks, who have for the most part have not updated their core offerings, have been losing increasing amounts of business to non-bank money transfers providers, which have proliferated over the past two decades. But who is taking the most share and why?

Determining precise numbers in such a notoriously opaque market is an immense challenge, but we’ve been able to estimate much of the shift using the financial models we have built for many of the leading money transfers players.

What the numbers show is a consistent erosion of banks’ share of the industry over the past two decades (no news to our readers), which has been super-charged by a number of high-profile players that are grabbing significant numbers of customers. Since 2015, we estimate the players in the chart above have cumulatively grown their revenues over five-fold, but much of the growth can be accounted for by a small number of players.

Wise, for example, has seen revenue grow at a compound annual rate of 65% over the last five years and Currencies Direct has more than doubled. Some of the more traditional phone-based brokers, on the other hand, have struggled to find much growth over the past five years, having had great runs before that.

There have broadly been two successful models to serve higher-end customers. The traditional phone-based brokers have continued to retain high-end dealers to work directly with high-value clients offering 1-1 service, simple (but profitable) hedging products and a white-glove service. Clients are typically sourced via referrals and partnership models passing on the trust of the client to the broker.

The second model led by Wise is digital and mobile-first, and has been hugely successful for the lower-value payments part of this customer segment. Speed, a range of funding methods, a multicurrency account and, of course, price have served as the differentiators to those banks.

These gaps are not lost on the banks, and many are working to improve their offerings across the board. Banks remain the primary financial institution for most clients and the value of this trust can be seen in the price premiums that remain. If banks can close some of their product gaps, the resulting competitive dynamics will be fascinating to see played out. We’ll be watching…

How are these companies competing with banks on price and capability?