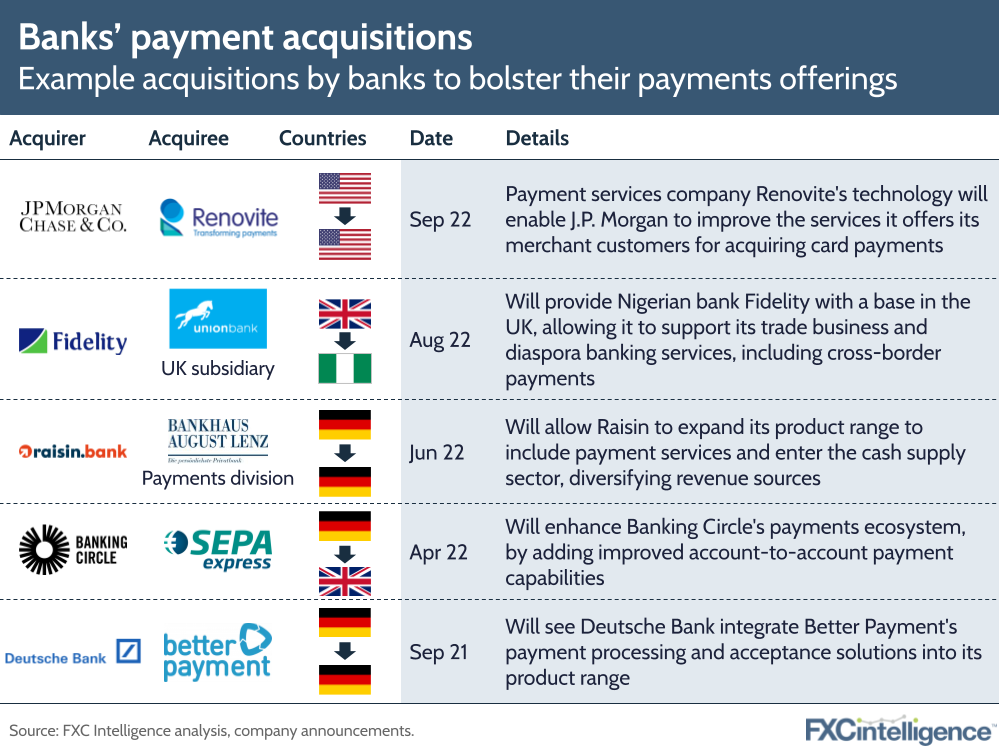

Last week J.P. Morgan announced that it was acquiring paytech Renovite Technologies, in an acquisition designed to boost the technological capabilities of the banking giant. But how important are acquisitions to banks looking to innovate in payments?

J.P. Morgan’s acquisition of Renovite is key to its goal of building a “next-generation merchant acquiring platform”, as well as helping to modernise the bank’s payments services and support its ongoing move to cloud-based solutions. It will see the paytech company, which specialises in merchant acquiring solutions, become part of J.P. Morgan Payments and help increase the speed at which it can help clients add additional payment capabilities.

The acquisition is the latest in a number that have given banks additional payment capabilities, suggesting that the space represents an area of potential expansion. For some, the expansion is regional, such as Nigerian bank Fidelity, which has increased its access to diaspora customers with its acquisition of the UK arm of Union Bank.

For others, however, the acquisition is largely technological, such as Deutsche Bank’s acquisition of Better Payment Germany. In both cases, as with J.P. Morgan’s acquisition, the deal has introduced new capabilities and enhanced the service the banks can provide their customers.

However, while this may be a means for banks to improve their competitive offering in the payments space, there are potential challenges. The recent blocking of UBS’s acquisition of robo-advisor Wealthfront, reminiscent of the blocking of Visa’s Plaid acquisition, suggests an increasing scrutiny from US regulators over fintech acquisitions by banks.

This is reflected by a warning issued by Michael Hsu, Acting Comptroller of the Currency, last week, where he raised concerns about the increasing interconnectedness of banks and fintechs and the potential for “crisis” if there was not adequate regulation of fintechs working closely with banks.