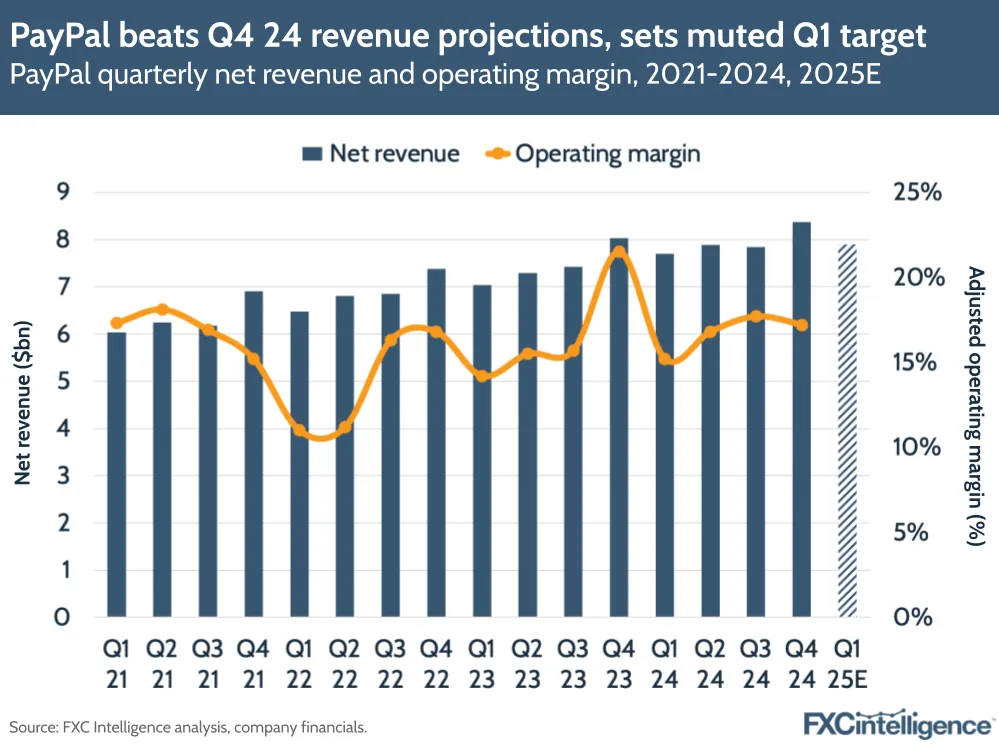

PayPal has announced its Q4 2024 earnings, closing out the “transition year” that saw it refocus the business to prioritise profitable growth. And while the company beat the muted expectations it set for itself a quarter ago, its projections for Q1 2025 have prompted the share price to tumble, despite some promising signs from several divisions, including its P2P payments brands.

PayPal’s better-than-expected results saw it deliver a 4% increase in net revenues to $8.4bn for Q4 2024, while FY 2024 saw this metric grow by 7% to $31.8bn. However, GAAP operating income did shrink by 17% YoY to $1.4bn in Q4, resulting in a 431 basis point drop in operating margin to 17.2%. Operating margin also contracted slightly for FY 2024, with a 14 basis point reduction to 16.7%.

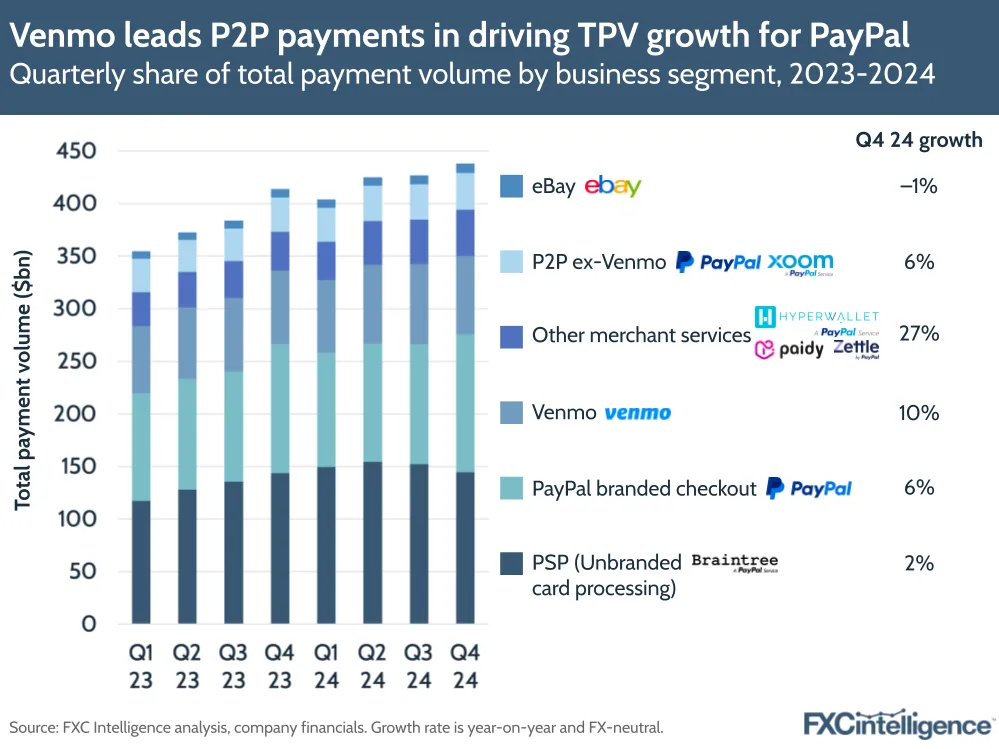

The company pointed to improvements in branded checkout, P2P and its domestic payments brand Venmo as key to its success in 2024. Venmo in particular has shown benefits from the company’s increased focus on monetisation, with more than 20% growth in debit card and Pay with Venmo active accounts in Q4 2024. P2P excluding Venmo, which covers PayPal’s own P2P payments and its money transfers brand Xoom, also saw accelerated growth in Q4, which the company credited to “increased engagement among [its] existing user base”.

PayPal saw its overall total payment volume (TPV) increase by 7% to $437.8bn in Q4 2024, and a 10% increase to $1.7tn in FY 2024. While Other Merchant Services, which covers brands including Hyperwallet, Paidy and Zettle saw the strongest growth in Q4, Venmo saw above-average growth of 10% to $75.6bn, while P2P-ex Venmo grew by 6% on an FX-neutral basis, its strongest growth rate to-date since the company began to reprioritise Xoom.

Meanwhile, PSP (unbranded card processing) was something of a headwind for the company in terms of TPV as it has refocused to prioritise growth in transaction margin dollars for its Braintree brand. This also drove a -3% drop in payment transactions in Q4 2024 for PayPal, although the number of active accounts did increase for the fourth quarter in a row, after a period of quarter-on-quarter declines.

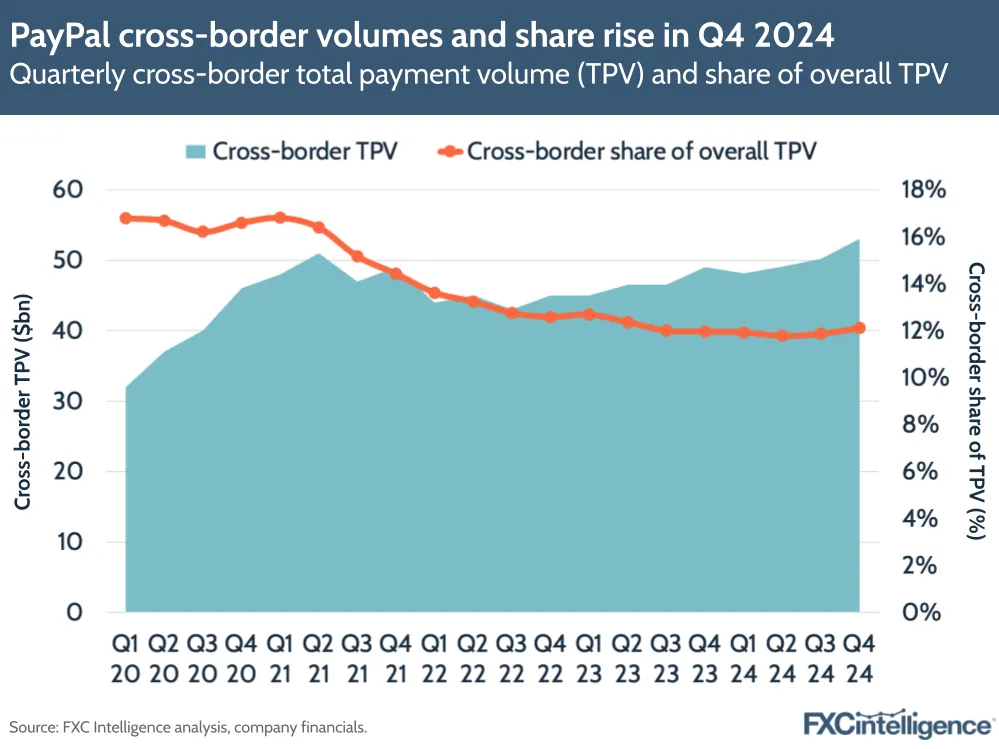

PayPal also saw cross-border TPV, which accounts for transactions where the merchant is in a different market to the buyer, grow at a faster rate than TPV overall. This climbed by 8% year-on-year in Q4, or 9% on an FX-neutral basis, to reach $53bn in Q4 2024.

Despite the results, PayPal opted not to provide FY 2025 projections, and projected “flat to low single-digit” revenue growth for Q1 2025, which it attributed to ongoing transaction margin-related renegotiations associated with Braintree.

However, the company did signal that continued product launches, product growth, partnerships and efficiency drives would be key priorities for 2025. It also indicated that it would be providing greater insights into its strategy for the year at its Investor Day towards the end of this month, which is set to include greater insights about its plans for its P2P payment brands, including Venmo.

We’ll be providing a more detailed analysis of PayPal, and in particular its P2P offerings and other cross-border initiatives, following the Investor Day.

How is PayPal competing with competitors on cross-border payments?