B2B payments providers saw mixed results this year but have continued to tap into the global payments opportunity. Below is our roundup of key trends for the B2B cross-border payments industry in 2024.

B2B payments remains one of the biggest opportunities for payment providers, with companies sending trillions around the world globally. Payments companies have continued to tap into this opportunity in 2024, with several making acquisitions to expand into emerging markets and launching new products. However, some have faced headwinds due to macroeconomic impacts this year.

Below are some of the key trends for the B2B cross-border payments industry in 2024.

B2B and SME payments present growing opportunity

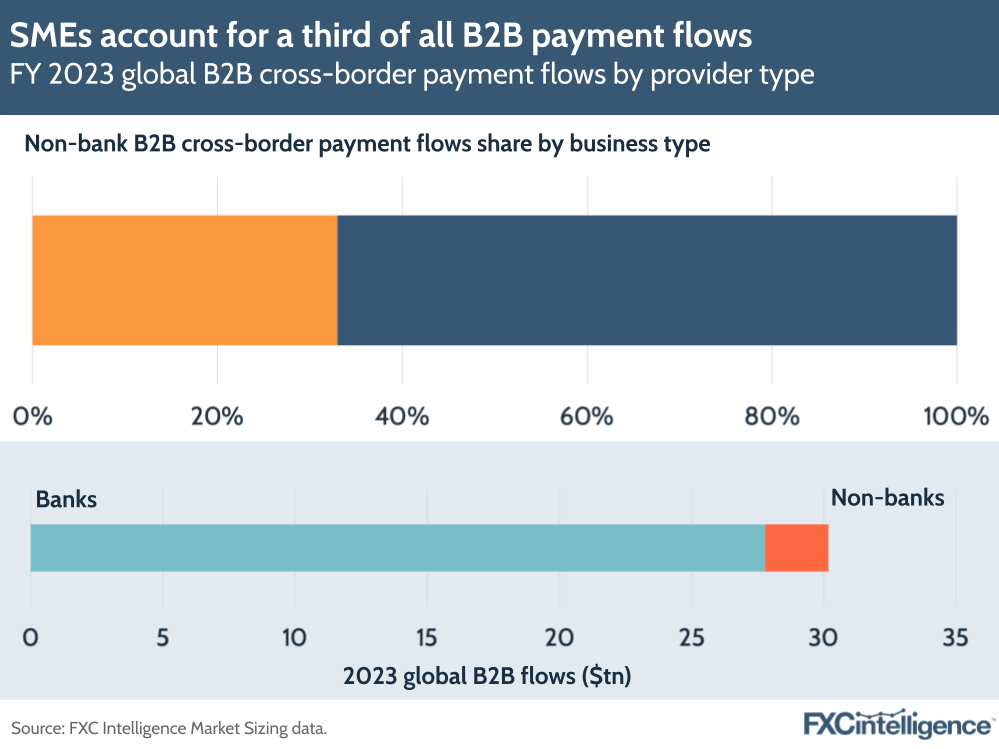

Earlier this year, our in-depth state of banks report found that banks still account for the vast majority of global B2B payment flows. However, standalone B2B payments providers are continuing to position themselves towards taking this opportunity from banks – particularly when it comes to SMEs, which send less money individually but still make up around a third of global payments flows.

Though banks accounted for 92% of B2B payments overall in 2023, they accounted for 76% of SME flows, versus 24% for non-bank providers. This demonstrates the potential that players such as Wise and Payoneer already have for tackling payments demands for smaller businesses.

Some companies that used to have B2B payments as a smaller part of their offering have continued to ramp up their shift to grow in this area. Having completed its acquisition of Paytron, Australian provider OFX now sees corporate payments form 64% of its revenues in its most recent results.

Earlier this year, Fleetcor rebranded as Corpay, highlighting its growing commitment to B2B following major acquisitions, while Flywire acquired Invoiced, marking a departure from other acquisitions focused on education payments. B2B payment providers such as Corpay and Equals have also spoken about positioning themselves as being between large banks and smaller fintechs with less capability, making them agile enough to innovate quickly in the corporate payments space.

B2B players were affected by headwinds in 2024

While the majority of B2B players saw revenue growth in 2024, a number of them have seen headwinds this year – largely linked to macroeconomic effects as well as currency and FX impacts from emerging markets. As a result, though growth has been present it has been subdued in some cases compared to previous years.

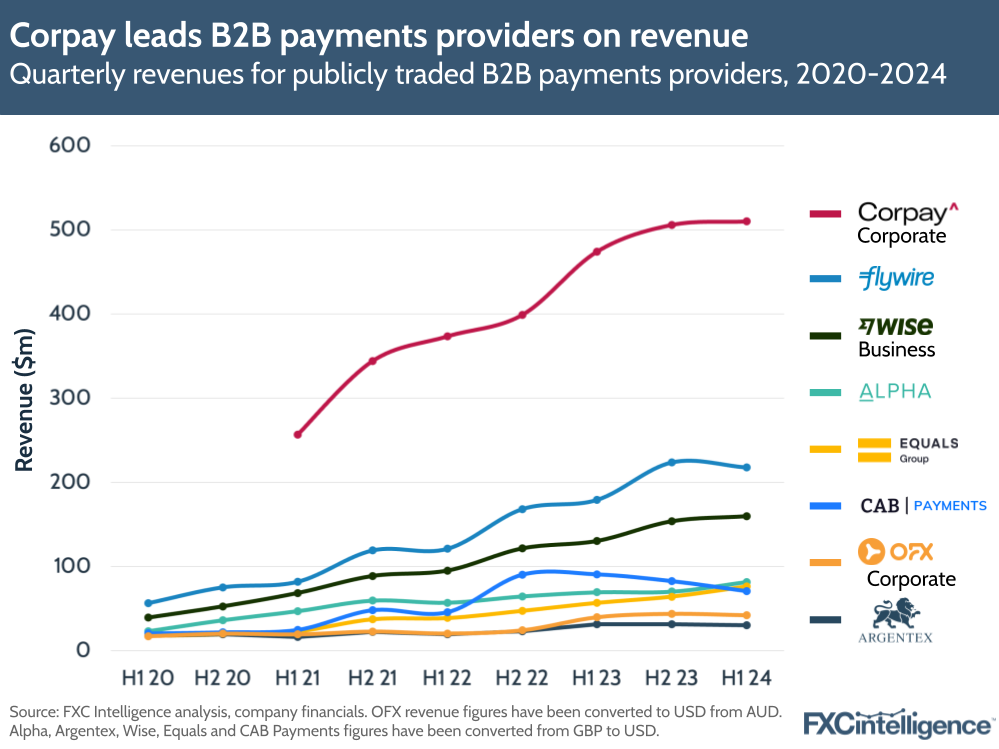

By far the biggest corporate payments player we track in terms of revenue, Corpay saw its first $1bn quarter in Q3 2024, bolstered by 25% growth in its Corporate Payments segment. However, on a half-yearly basis its revenue was lower in H1 2024 at 8%, versus 27% for H1 2023.

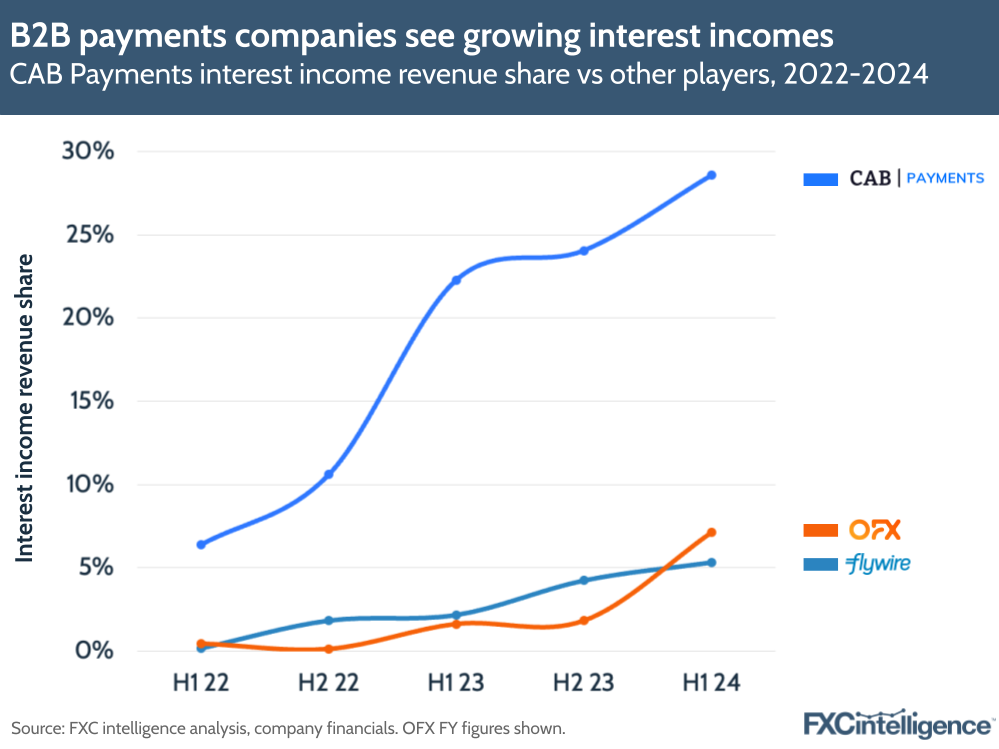

The remaining corporate payments players we tracked – including Wise’s business segment, Alpha, Equals, CAB Payments, OFX and Flywire – all saw lower revenue growth or even declines in H1 2024, with CAB Payments and OFX seeing a particularly stark difference compared to the same period last year. CAB Payments’s -22% income decline in H1 2024 was due to continued fallout from central bank interventions in several African currencies, while OFX saw a slowdown on larger value transactions due to later-than-expected changes in interest rates.

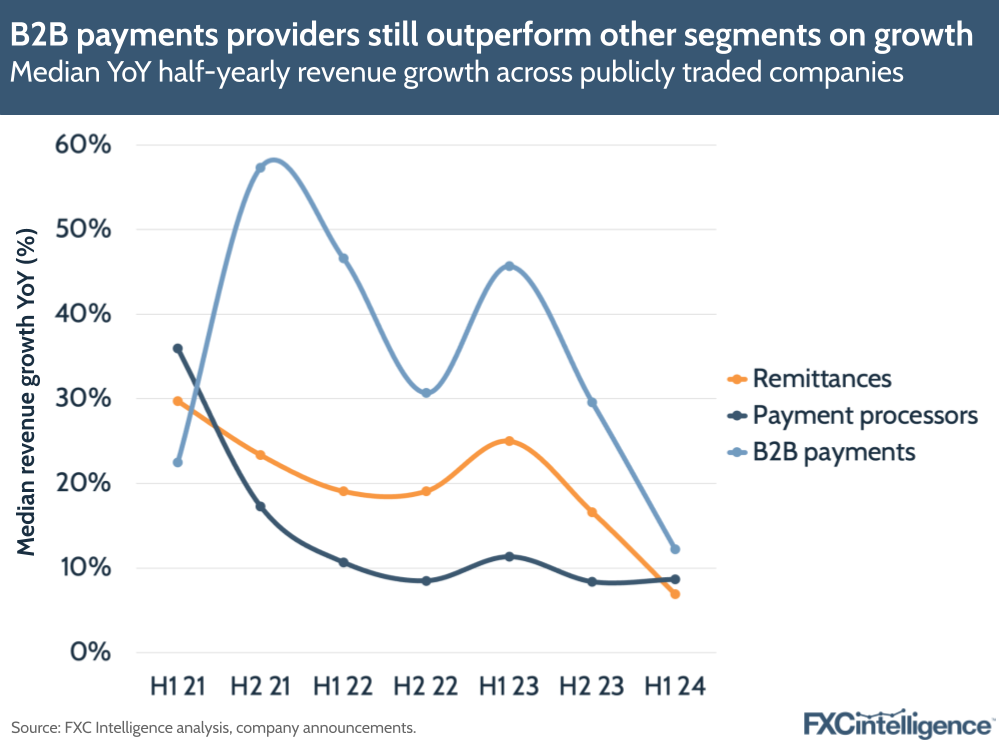

Against different cross-border payments companies – including remittances providers and payment processors – B2B payments providers on average are still performing well in terms of revenue growth, but the median growth across these providers has declined to 12% in H1 2024, compared with 46% in H1 2023.

On the other hand, B2B payments players are seeing some benefits from macroeconomic impacts this year too. CAB Payments, OFX and Flywire have seen interest income account for higher shares of revenue over time as a result of higher interest rates as well as a slowdown in revenue growth for these companies.

Expanding payments infrastructure to new markets

This year has seen many B2B players continuing their expansion into new markets, with a common theme being addressing payment demands in emerging markets where financial inclusion is still growing and existing legacy banking infrastructure isn’t set up to support the needs of businesses. The year has also seen the growing use of currency pairs not involving USD as B2B companies increasingly seek to serve localised payments.

Corpay, for example, has positioned itself as enabling access to the Southern Hemisphere in the emerging market world for Tier 1 banks, as the company’s infrastructure allows its customers to send localised payments throughout Africa, Latin America and much of developing Asia. Similarly, Payoneer – which offers a scalable payments platform for SMBs, particularly in emerging markets – reported significant market expansion in APAC and LatAm countries in its most recent earnings.

On the other hand, some B2B players have continued to target more developed markets. Beyond its home market of Australia, OFX has sought out growth opportunities in North America and Europe, while UK-based Equals has continued the European expansion it began last year through its acquisition of Oonex.

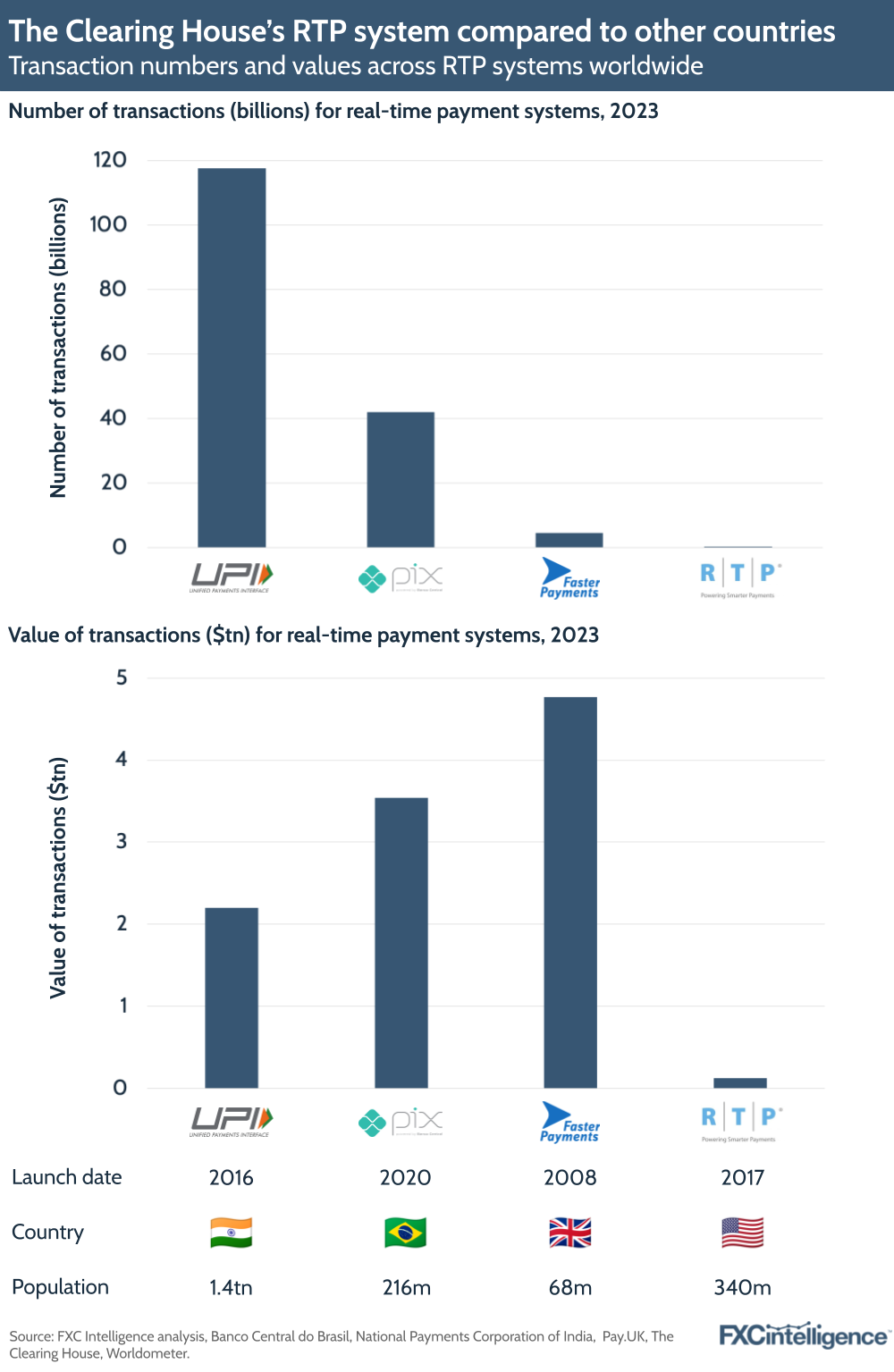

As well as expanding to new areas, delivering faster and more cost-effective payments for businesses has become more important as payment providers attempt to grow their share of the market, as more and more countries build expectations by launching and expanding real-time payment systems including India’s UPI, Brazil’s Pix and the US’s FedNow. There have also been a number of initiatives and ongoing projects to enable instant payments across borders, though some systems are further along in the process than others.

Earlier this year, B2B payments providers told us that integrating real-time payment methods would be a significant part of their strategy, not just as companies try to speed up payments but so that those payments are more transparent. Real-time payment methods – in particular, those aligned with the ISO 20022 standard – will allow users to more closely monitor the progress of payments.

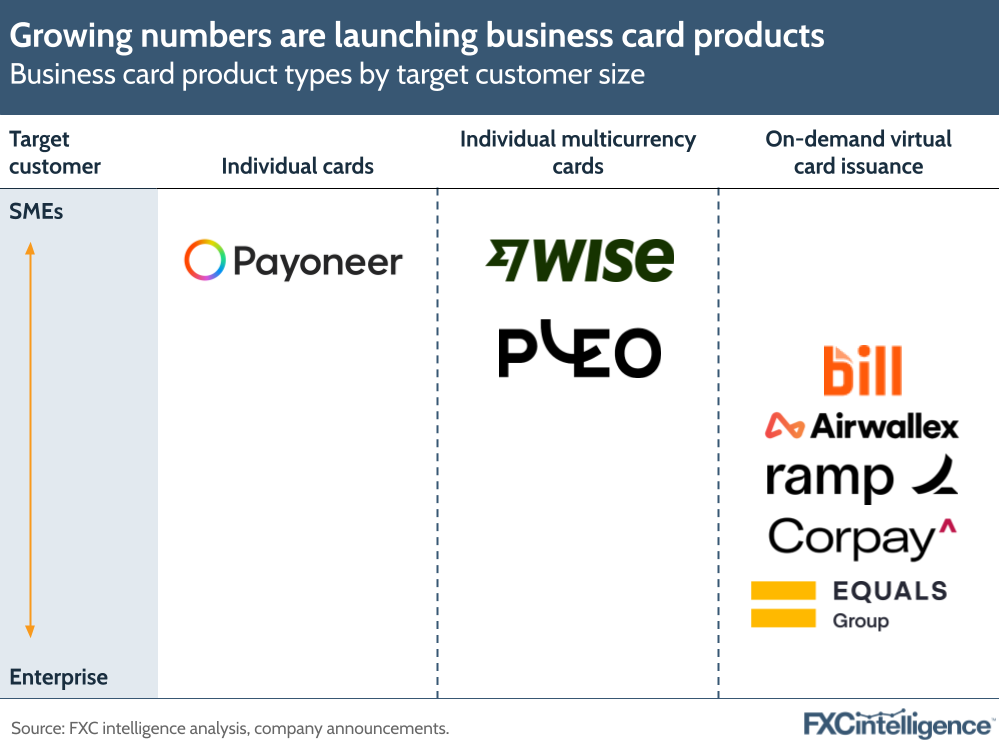

Multicurrency payment cards and accounts are on the rise

B2B payments providers have been launching new card products to serve both SMEs and the enterprise markets. Multicurrency cards allow users to hold and transact in several different currencies, and while their use is not exclusive to B2B, it is notable that players in the space are gravitating towards them.

Meanwhile, a number of companies have also begun issuing virtual cards, which similarly provide greater control and visibility of employee transactions while reducing the risk of card theft/fraud.

Unlike Payoneer’s card product – which supports business payments across one of four currencies – business spending platform Pleo’s multicurrency cards enable spending across more than 50 currencies. In addition to giving companies more control over spending, multicurrency cards can also allow them to avoid high FX fees and enable easier transactions without the company needing separate accounts for each currency.

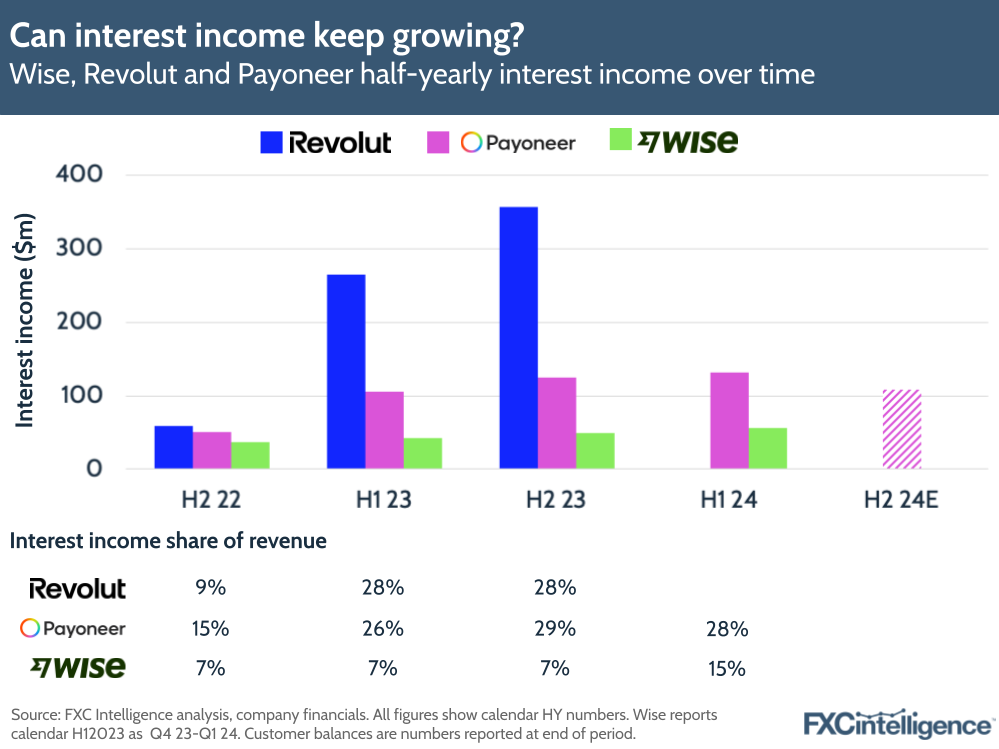

Linked to multicurrency cards is the impact that customer accounts have continued to have on B2B payment providers, particularly Revolut, Payoneer and Wise, which have seen customer balances rise significantly over time. In a high interest rate environment, the amount of interest accrued from customers has also risen, though this has started to slow in 2024 as the rate of inflation has slowed and countries around the world have begun reducing rates.

Having said this, not everyone we have spoken to this year has been convinced by the multicurrency account opportunity. Rapyd CEO Arik Shtilman told us that though it has promise for businesses that struggle to open a bank account, it comes with high regulatory scrutiny and companies can risk exposure to falling interest rates having a sizeable impact on income.

Global payroll sees surge in activity

There has been significantly more activity from global payroll companies in 2024, with several partnerships, investments and acquisitions extending the reach of businesses in the space to enable payouts to employees globally.

The growing global payroll activity may have surged as a result of changing work habits both during and after the Covid-19 pandemic – not just in terms of flexibility but also in where they choose to locate globally. The pandemic shone a light on the need for businesses to provide streamlined and effective payment systems, particularly to emerging markets.

US-based Deel, for example, has made a number of acquisitions during the year, including people development platform Zavvy, Africa-based payroll provider PaySpace and UK-based money transfer service Atlantic Money. Major payments providers are also helping drive this sector forward, with Visa contributing to a $5m funding round for Kenya-based payroll provider Workpay in August, while in the same month PayPal integrated with payroll provider UKG to enable customers to be paid through its direct deposit system.

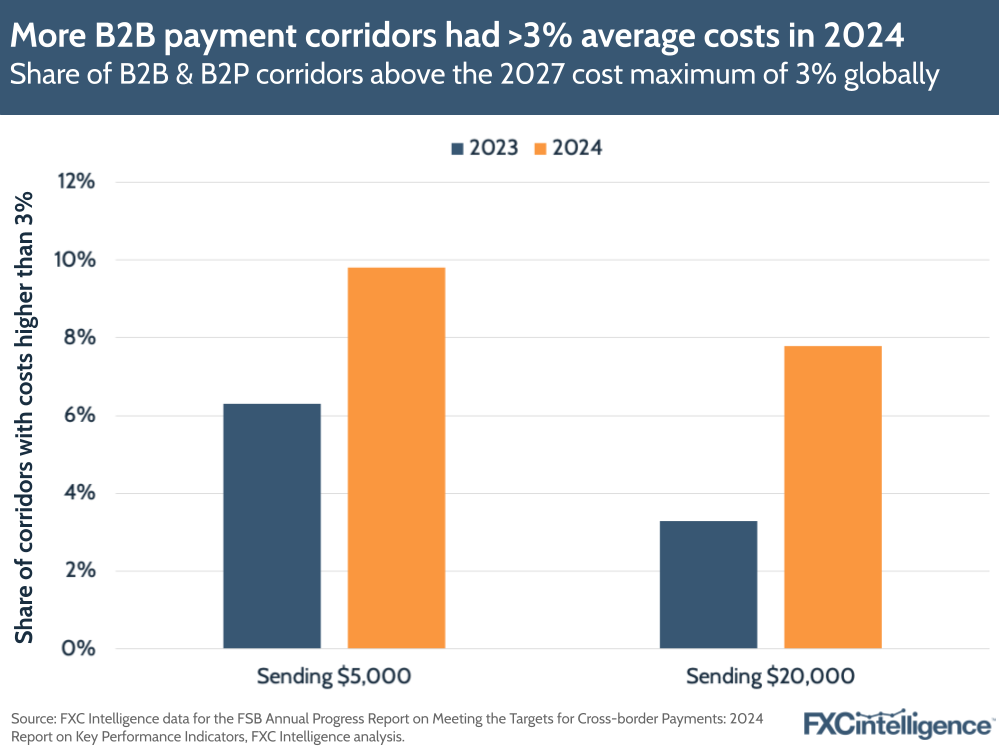

B2B payments pricing is still too high

Our analysis of the FSB’s report into the G20 Roadmap for Enhancing Cross-Border Payments showed that B2B and B2P payments still cost more on average than the G20 wants them to. In particular, the roadmap has required that global average retail cross-border payment costs amount to no more than 1% by the end of 2027, with no corridor seeing average costs above 3%.

Across global payments, B2B saw a 0.1% point rise in 2024 to reach an average of 1.6%, but this is lower than P2P, which grew 0.1% to 2.6%, while P2B remained flat at 2%. We also found that B2B and B2P payments are currently in a stronger position than P2P to meet the 1% target, though it will still require yearly average cost reductions of around 20% across lower send amounts, versus 15% for higher send values.

The segment also saw a higher share of corridors globally that are breaching the 3% average maximum cost, with sends of $5,000 rising to 9.81%, while sends of $20,000 rose to 7.8%. Generally, send costs in regions that contain emerging markets, such as Sub-Saharan Africa and LatAm, have been more expensive for sending B2B and B2P payments globally.

There is still some way to go when it comes to bringing down pricing for B2B payments, but in addition to our market sizing data, these findings highlight the potential for bringing faster, less costly payments to enterprises and SMBs, particularly in countries where weaker infrastructure is currently a roadblock.