How has 2024 been for B2B2X players who provide cross-border payments networks? We look at the key trends and revisit charts from across the year.

From a network perspective, there have arguably never been more players serving more companies in the cross-border payments space than today. While infrastructure has been significantly streamlined compared to previous eras, in-house cross-border payments networks are increasingly being harnessed by growing numbers of companies to provide infrastructure alternatives to the traditional Swift-enabled correspondent banking system for other cross-border payments players.

These companies, often referred to as B2B2X providers, serve a wide variety of use cases, with the rise of embedded finance creating growing needs for such solutions across a broad range of verticals.

B2B2X solutions have been evolving for some time and 2024 continues that trend, from improvements in reach and complexity for key networks to entirely new technology types driving change in the space. In this piece, we review some of the key trends across the year for B2B2X, and consider how they could drive further change in years to come.

Evolving B2B2X partnerships

Partnerships are critical across cross-border payments, and nowhere is this more true than in the B2B2X space. Many companies announce client partnerships that showcase their broadening reach and growth in the space, with different companies using different providers depending on the region, application or use case. Many companies also partner in some areas with organisations that they are competing with in others.

For example, Temenos, which itself provides software as a service (SaaS) solutions focused around banking and payments for organisations including ABN AMRO and the Bank of Shanghai, announced this year that it had partnered with both Visa Direct and Mastercard Move. In both cases, these were integrated with Temenos Payments Hub, enabling the rails and endpoints of both platforms to be accessed via Temenos’ own payments ecosystem by its clients.

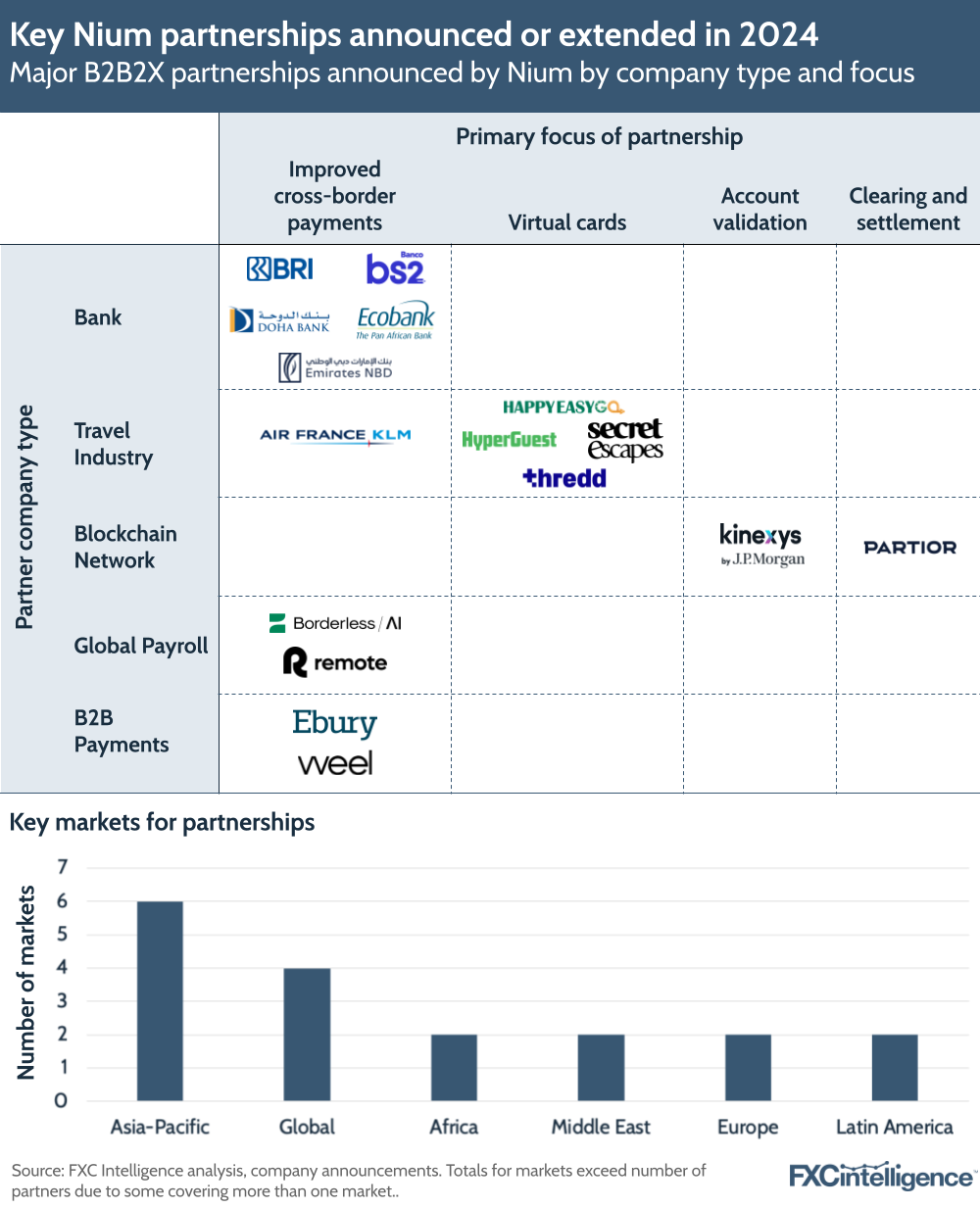

While this is a common form of partnership, many are focused on providing improvements to traditional correspondent banking solutions, which was the case for many of the partnerships announced by Nium this year. The Singapore-headquartered B2B2X player had numerous announcements focused around providing faster and often cheaper cross-border payments for its clients’ customers, many of which are key regional banking players.

With so many potential customers in the B2B2X sector globally, the focus on growing partnerships is only set to continue in the near to medium-term future, although as time goes on we may see use cases begin to shift. It was notable that a small number of Nium’s partnerships were with blockchain-based payment networks, which in places ultimately serve to rival traditional payment networks in this space.

Growing network reach and speed

Across a wide variety of players, there were reports of companies adding to or expanding the networks they offer B2B2X services on. This is ultimately done to make their services more competitive, as it reduces the number of other partners an organisation has to add in order to gain full coverage of its chosen markets and payment types. However, this expansion is often achieved in turn through partnerships.

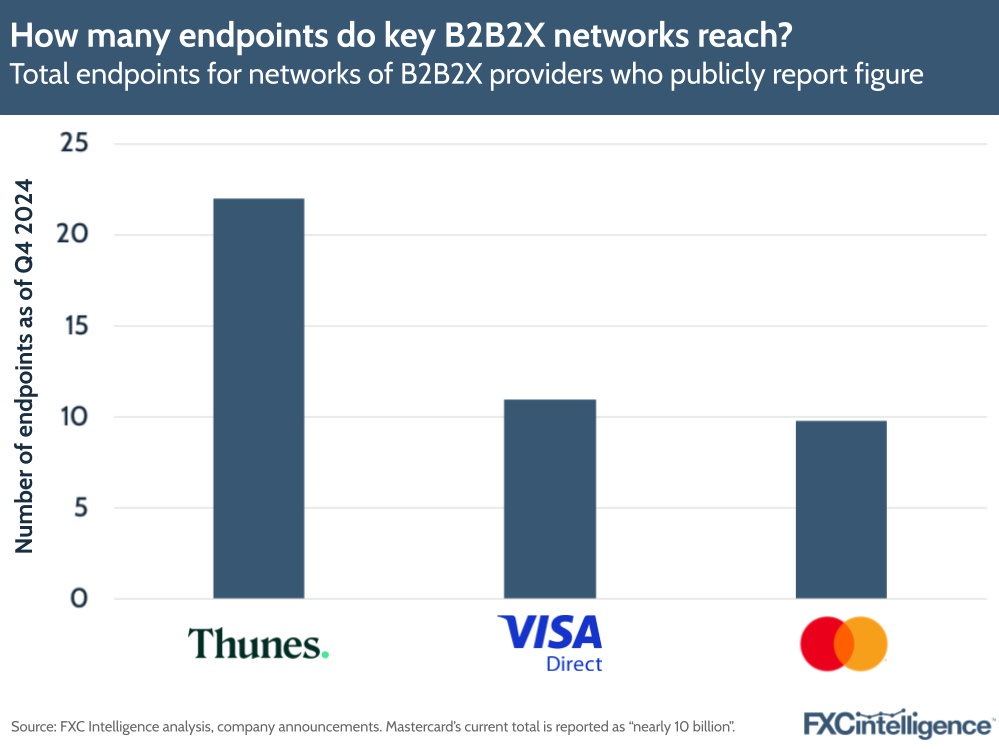

For example, as of Q4 2024, Thunes’ network endpoints totaled 22 billion, as a result of the launch of its Pay-to-Cards solution. Prior to this, the organisation could pay out to seven billion mobile wallets and bank accounts, however this launch added the ability to pay out to 15 billion cards, including Mastercard, Visa and UnionPay. This was in part enabled by a partnership between Visa and Thunes announced earlier in the year, which saw Thunes integrate Visa Direct’s push-to-card solution. However, the partnership also saw Visa connect to Thunes’ network, allowing it to increase its number of digital wallet and bank accounts. At the end of 2024, Visa Direct’s endpoints surpassed 11 billion, up from 8.5 billion in 2023, more than 7 billion of which are mobile wallets and bank accounts.

Beyond reach, speed has continued to be a focus for many B2B2X players, with real-time payments in particular becoming increasingly key. Earlier in December, Visa Direct announced that from April 2025 it will enable funds transferred to US bank accounts to be available in one minute or less.

Wise Platform, meanwhile, now sees 63% of its payments processed instantly, with key infrastructure expansions, including new licences in Brazil, Japan and Australia, helping to fuel this.

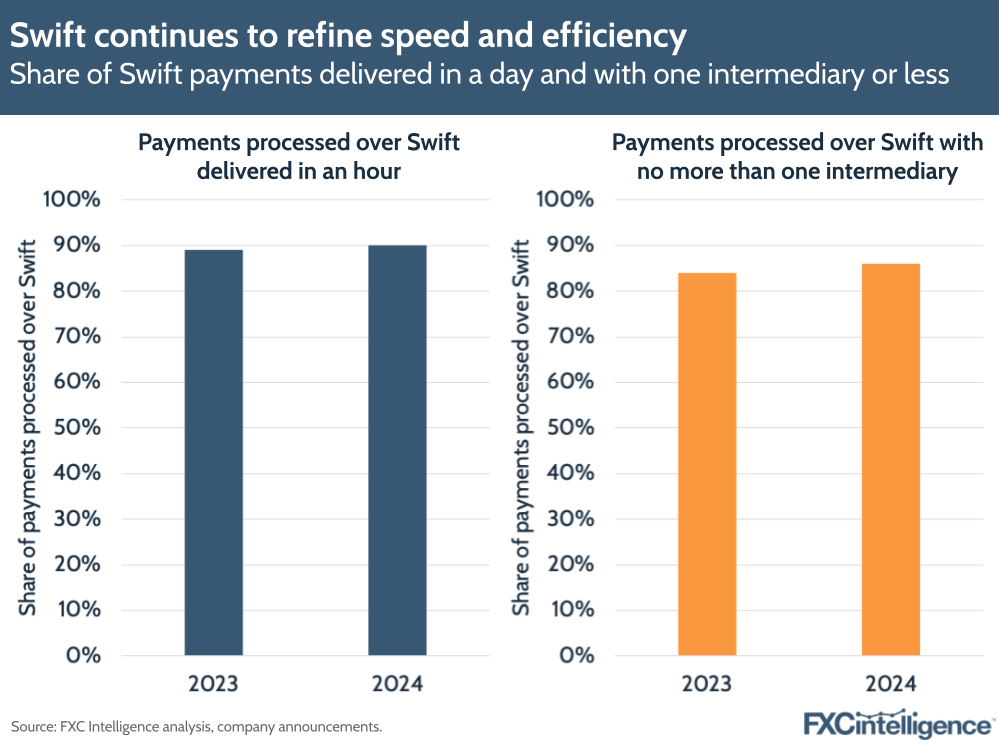

Meanwhile, responding to the Financial Stability Board’s latest update to the G20 cross-border roadmap targets on speed, Swift also shared updated data on its network processing speed, with 90% of cross-border payments sent over its network arriving within an hour, up from 89% in 2023.

Underpinning this is increases in network efficiency. It has also seen an increase in the number of payments on the network being conducted directly between two institutions or via a single intermediary, which grew from 84% in 2023 to 86% in 2024.

The evolving digital wallet interoperability opportunity

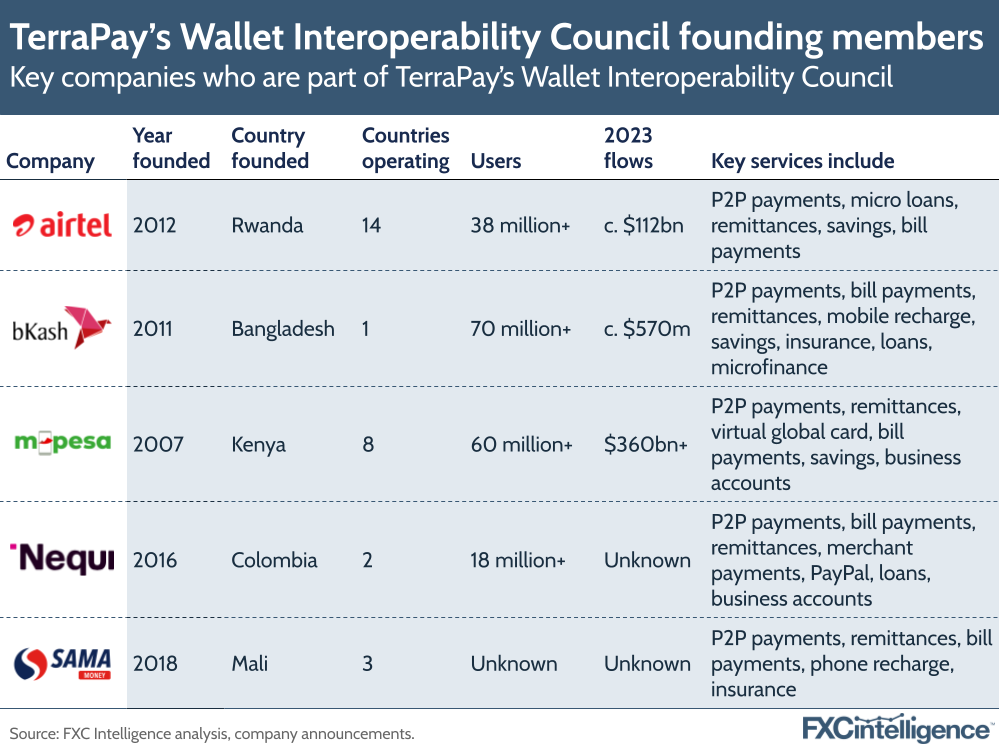

Beyond the speed and capabilities of B2B2X networks, there has also been an increased focus on bringing cross-border payments capabilities to domestic-focused solutions, particularly digital wallets. This year has seen several initiatives launched to increase the interoperability and connectivity of digital wallets, including TerraPay’s Wallet Interoperability Council, whose founding members include some of Africa and South Asia’s biggest digital wallets, including Airtel, M-Pesa and bKash.

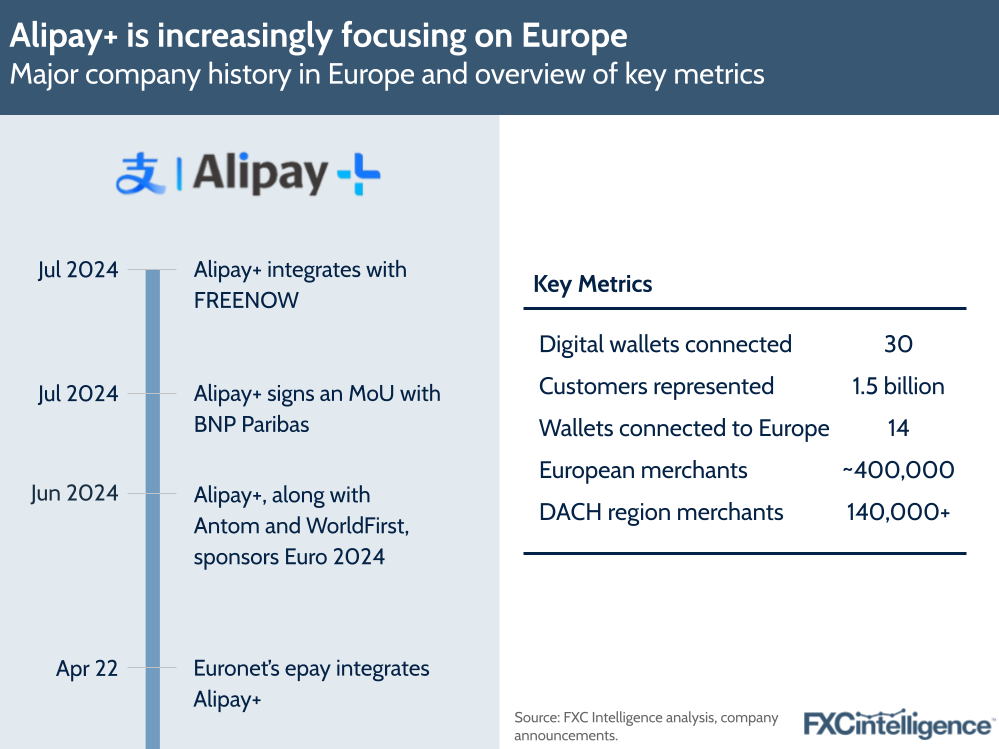

Ant Group’s international B2B2X platform Alipay+ has also been taking on this challenge, with the company connecting a variety of regional digital wallets using the same cross-border infrastructure it uses for its core Alipay wallet. While in the past the company has approached this by directly investing in the development of such regional wallets, recently it has shifted to a more platform-based approach, and in 2024 increasingly focused on Europe to develop its reach.

Domestic infrastructure developments drive connectivity

While many organisations have been driving network enhancements in the cross-border payments space, the improvement of domestic payments infrastructure has also played a role. In many regions, improved infrastructure has not only increased financial access and speed within a country, but has also increased the number of endpoints for cross-border payments networks to connect to.

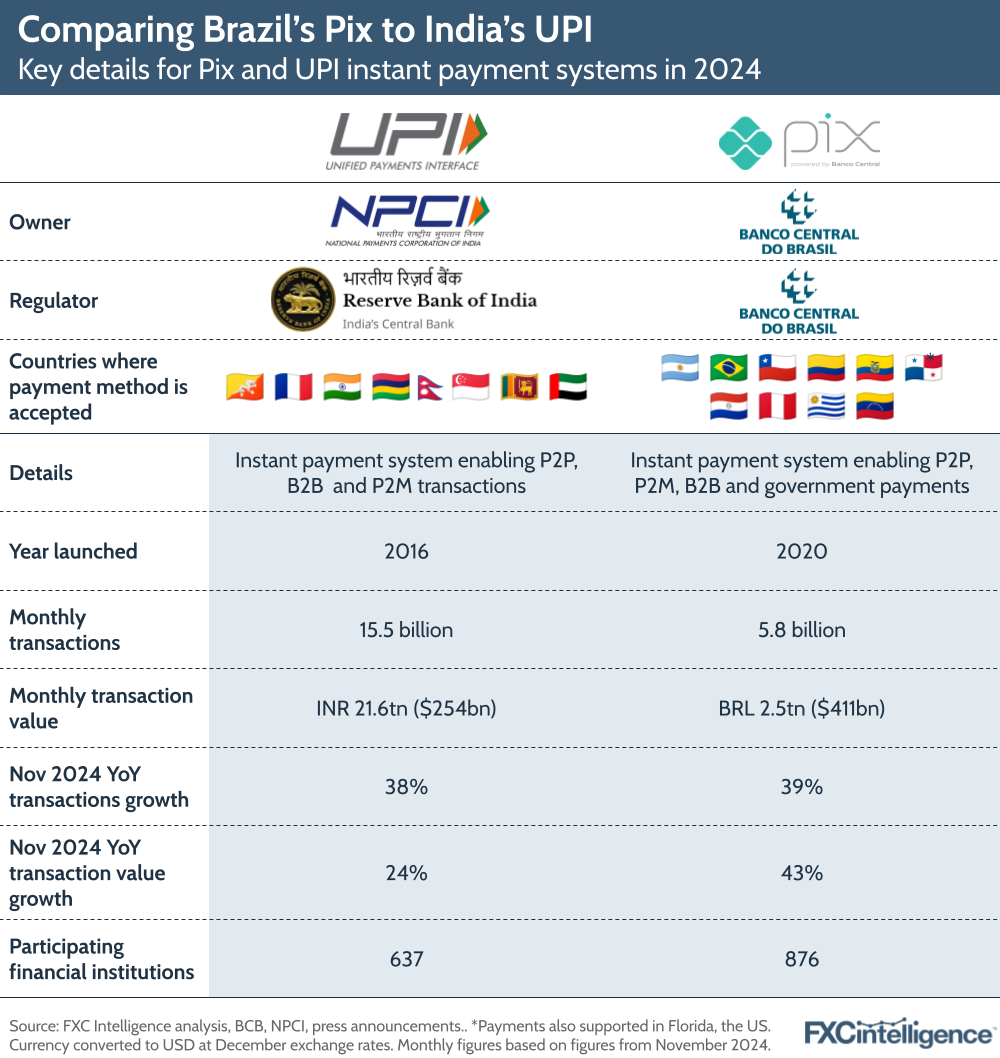

Key regional examples of this are Brazil’s Pix and India’s UPI, which while ultimately domestic, have increasingly seen cross-border connectivity. Having only previously connected to a small number of countries, in December a partnership with PagBrasil and B89 made it possible for Brazilian citizens to use Pix for payments in a further seven Latin American countries, including Colombia, Peru and Venezuela. In both cases, there has also been increased focus on connecting cross-border networks to the payment systems as the networks themselves continue to grow. All flows in November 2024, for example, climbed by 24% year-on-year for UPI and 43% for Pix, while transactions over the same period grew 38% and 29% respectively.

CBDC development continues

On a central bank level, infrastructure developments have also extended past domestic schemes, with central bank digital currencies (CBDCs) remaining in development in many parts of the world – although still some years away from widespread technical implementation.

Our analysis earlier this year showed that while retail CBDCs continue to be the most popular form in development, wholesale CBDCs were a higher share of those being developed for cross-border payments applications.

Crucially, cross-border payments remain a leading driver for many projects in this space, suggesting that we may yet begin to see some real-world impacts from the technology in the years to come.

Blockchain’s stablecoin-led infrastructure return

A more immediate impact from the digital currency space is blockchain technology, stablecoins in particular .

While blockchain technology was being used as part of cross-border payments infrastructure several years ago, particularly via Ripple, a collapse in commercial confidence amid several legal cases caused the industry to all but sever ties from it, save for a few niche examples. However, the last few years have begun to prompt a slow re-emergence, which has reached a peak over 2024.

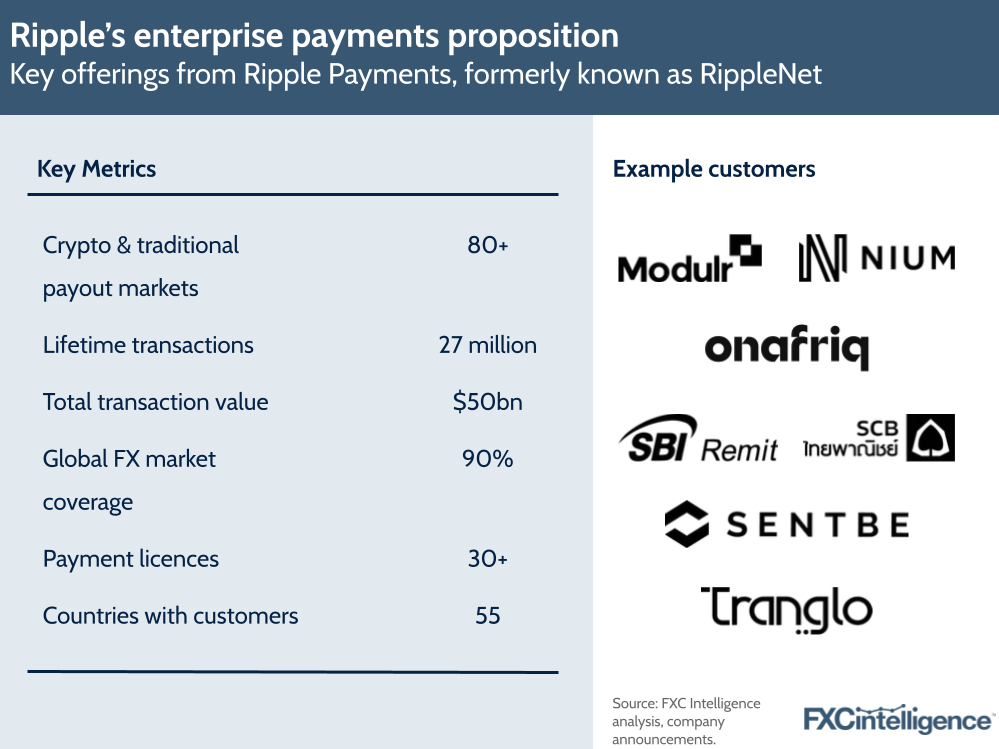

This is in part due to the resolution of several legal cases, including Ripple’s, but it also has been aided by the rise in use of stablecoins as part of the infrastructure, rather than non-fiat-backed digital currencies, which were often previously used. As a result many modern infrastructure-focused blockchain solutions pair a blockchain as the instant rails, while the stablecoin serves as the vehicle for the value being moved. This includes Ripple, which announced it was launching its own stablecoin following the relaunch of Ripple Payments to better serve the mainstream enterprise payments space.

Other players are also making similar moves, with Ant International launching its own stablecoin, while Swift is also partnering with several banks to pilot a stablecoin solution. Paxos, which provides PayPal’s PYUSD stablecoin, has also announced plans to launch a new USD-backed stablecoin.

Circle’s USDC remains a leader in the space, however, with key partnerships with Binance, Nubank and BVNK announced in Q4 alone.

With so many developments in stablecoins already underway, expect this to be a key area for B2B2X and beyond in cross-border payments in 2025.