CAB Payments saw incomes decline in H1 2024 on the back of major headwinds in some of its core markets. As the company looks to diversify, we take an in-depth look at their strategy and its position in the market going forward.

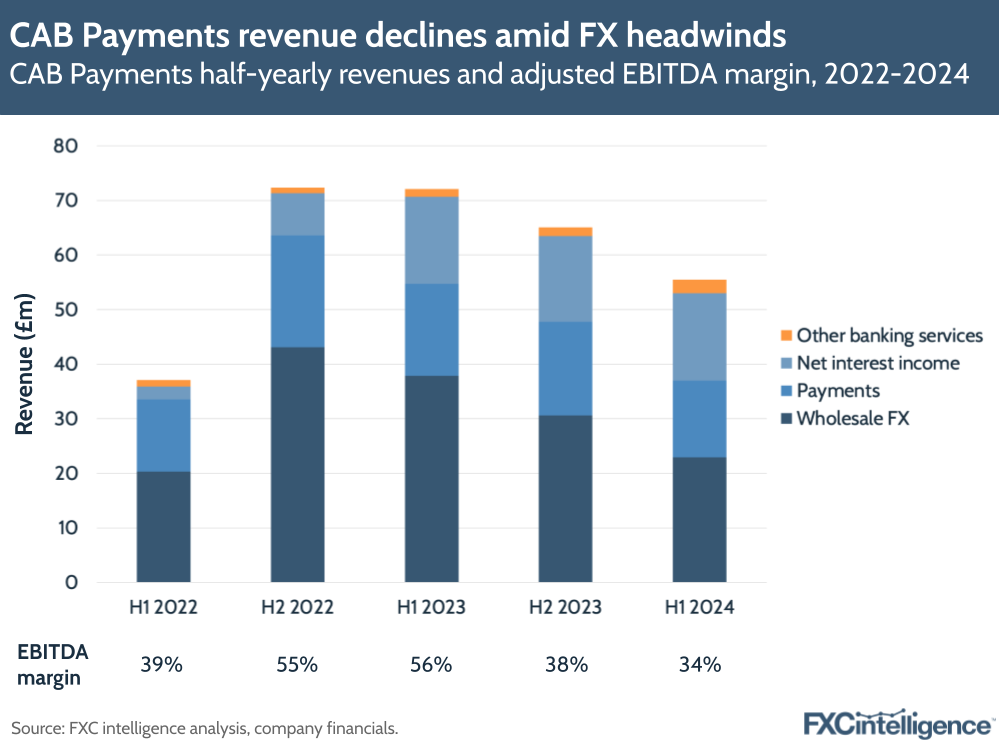

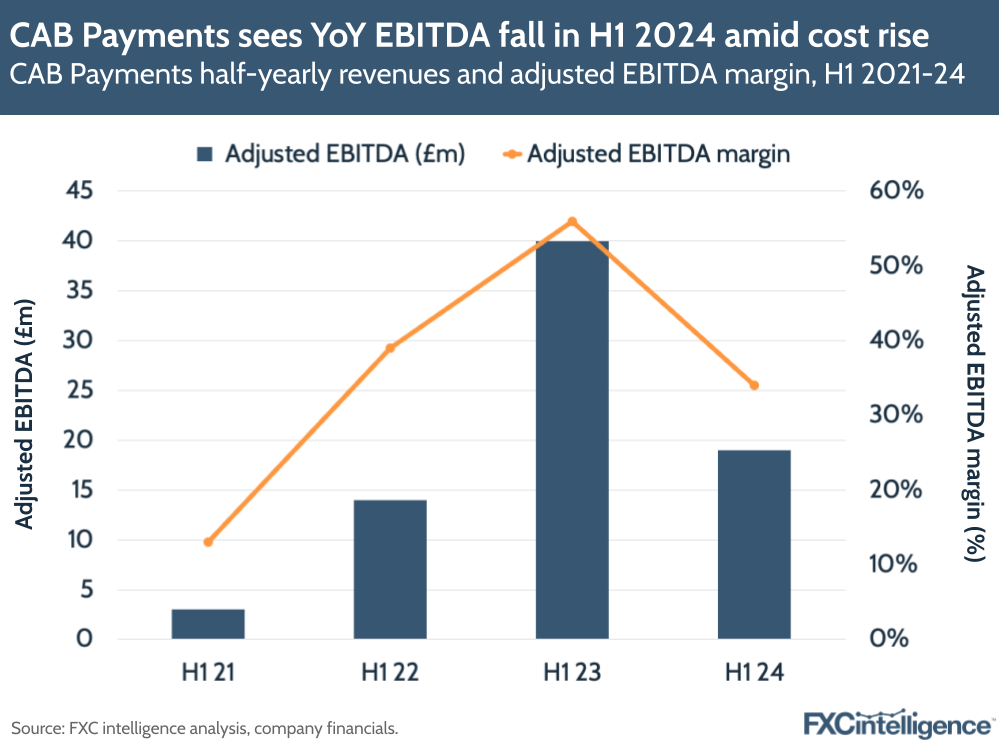

Last week, B2B cross-border payments provider CAB Payments’ released its interim results (following a July trading update), which highlighted that the company’s growth continues to be stifled by policy shifts surrounding several wayward currencies in its target markets. CAB shared that its total income had fallen by 22% to £56m, while its adjusted EBITDA declined by 53% to £19m, giving a margin of 34% (down from 56% last year).

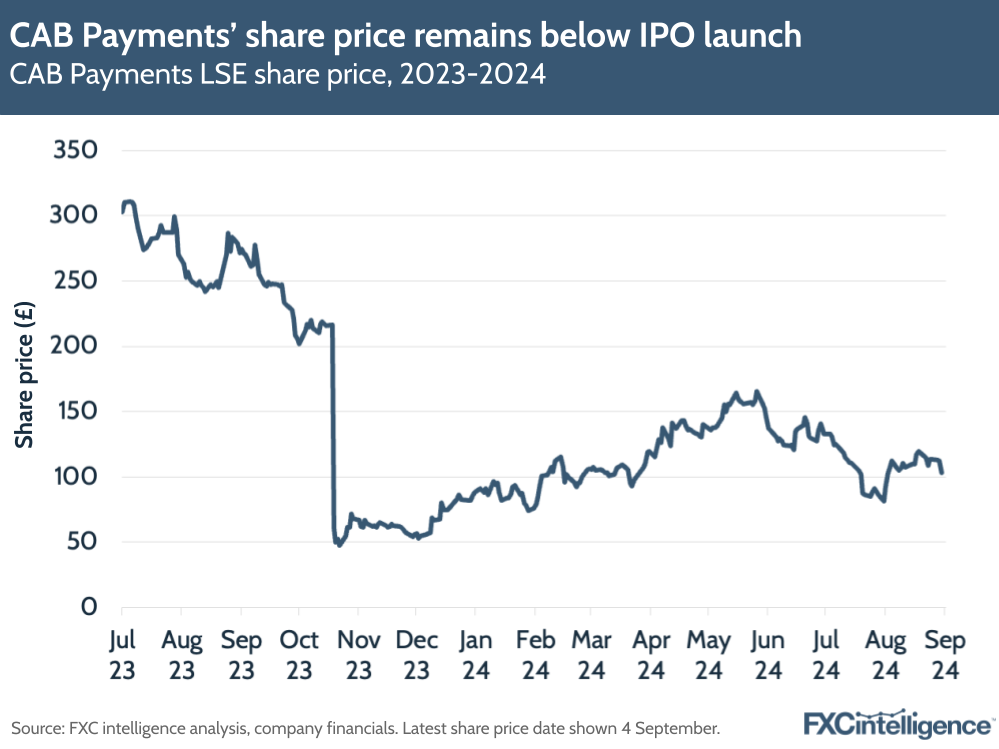

These figures are the latest drop in a rollercoaster year for the UK-based payments provider. After a successful listing made it the toast of the London Stock Exchange in July 2023, central bank interventions in the Nigerian naira (NGN), the West African franc (XOF) and the Central African franc (XAF) caused the cost of trading to rise and volumes to fall in some of its core corridors. The company’s share price fell dramatically as a result and, despite some recovery, it is still down by more than 66% compared to its share price at IPO.

In a presentation alongside these figures, recently anointed CEO Neeraj Kapur spoke more about how the company is now looking to diversify its strategy through expansion into new corridors, investment and building partnerships with other players, as well as growing its average revenue per client to help boost both transactional incomes and net interest incomes.

Though CAB expects gross income to be marginally below FY 2023, Kapur said that he expects operating margins to grow in the second half of the year with higher revenues, while costs will remain “broadly flat to H1, resulting in an overall blended adjusted EBITDA margin in the high 30s for FY 2024”. In this piece, we explore CAB’s diversification strategy, as well as how similar impacts are being seen elsewhere in the industry.

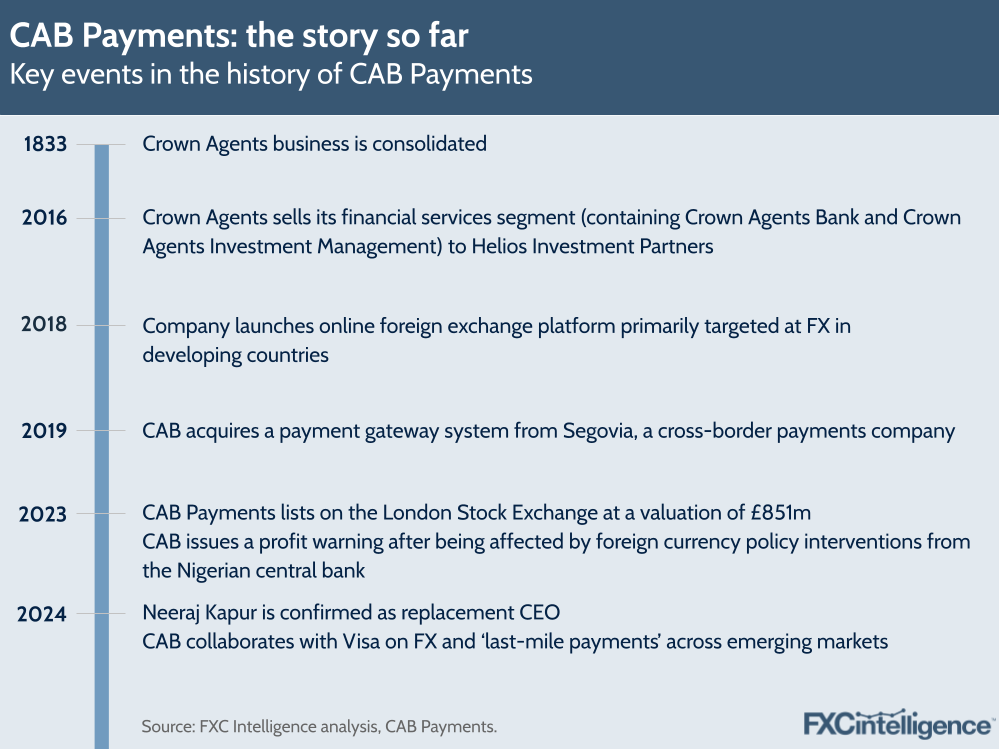

CAB Payments: the story so far

CAB distinguishes itself by focusing specifically on enabling money movement from developed markets into emerging markets in the Global South, particularly to countries within Africa, Asia and Latin America (in CAB’s financials, emerging markets refers to markets outside the G10 nations and Denmark). It does this through its global payment network, which it has built through a network of over 200 trading and liquidity partners and 25 central banks, with funds being moved through 135 bank accounts worldwide.

CAB Payments is the holding company for Crown Agents Bank, a provider of wholesale FX and cross-border payments services that was originally founded in 1833. It facilitates money transfers to over 140 countries and enables payments through more than 100 currencies across over 700 currency pairs. Two of the company’s major revenue streams have been Wholesale FX conversions, where bulk amounts of currency are converted without onward payment to a third party, as well as Payments FX, which includes margins from the foreign currency conversion as well as fees paid by customers to transfer money from one country to another and to third parties.

The company serves primarily blue chip clients, including international development organisations (IDOs), governments, emerging market financial institutions (EMFI) and non-bank fintechs. In its most recent results, CAB Payments talked about how it is “unlocking prosperity” in growing markets – for example, in the 12 months to 20 June 2024, the company enabled £8.6bn of flows into low and lower-middle income countries, as well as £2.9bn of flows for development aid and £1.8bn for remittances.

In July 2023, CAB Payments listed on the London Stock Exchange – it was the biggest IPO in the UK at the time, with the company valued at £851m. However, just a few months afterwards, the company put out a profit warning to investors after seeing a “number of changes to market conditions in some of its key currency corridors”, one of which was in Nigeria. In September 2023, the then-acting governor of Nigeria’s central bank also reportedly criticised CAB Payments as one of several traders forgoing the currency system to create a parallel payments market.

As a result of changing market conditions and central bank intervention, the company downgraded its revenue guidance by 17%, which in turn led to a 72% share drop that October. The share price has been recovering, and is up more than 30% overall since the start of the year at the time of writing, but is still down more than 60% compared to last year. This was exacerbated by further revenue impacts from central bank interventions in the XAF and XOF in the company’s FY 2023 results, announced in March.

CAB Payments is still on the rise, but the company needs to diversify further to grow its resilience against adverse events in major corridors, as its results show in more detail.

CAB’s H1 2024 results and the need to diversify

Many of CAB’s results are unchanged or only slightly updated from its trading update from July 2024, but the figures it has broken out in more detail present some key insights into why the company is looking to diversify against macro impacts.

On the top level, revenues were down 22% to £55.7m in H1 2024, versus 94% growth in H1 2023. On a segment level, Wholesale FX saw the biggest loss – down 39% to £22.9m – and Payments FX fell 33%, though Other Payments (which covers correspondent banking pension payments and final mile mobile payments) rose by 11%.

The company’s combined Payments segment (containing Payments FX and Other Payments) fell by 16% to £14.1m. Transaction-related revenues overall fell by 32% to £37m, while non-transactional revenues (containing interest income from cash management and other banking services) grew by 13% to £19m.

When normalising against headwinds in the NGN, XAF and XOF, the company saw 11% growth in gross income and 12% growth in transactional income, as well as 14% growth across Wholesale FX and Payments FX income. However, the results overall give an indication of the continued reliance on the success of corridors in Africa.

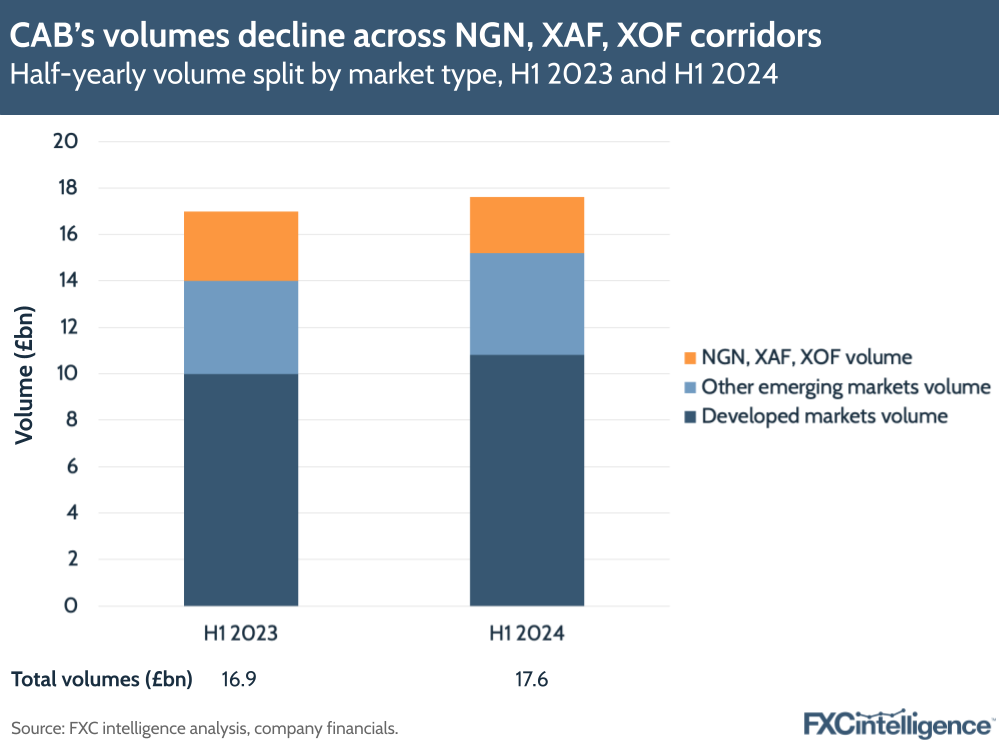

This can be further seen when breaking down the volumes transacted in the currencies CAB describes as dislocated (NGN, XAF and XOF) against other currencies. In total, volumes grew by 4% YoY to £17.6bn in H1 2024, with volumes for NGN, XAF and XOF falling by 20%. Meanwhile, emerging markets volumes declined by 3% (though saw growth of 10% excluding dislocated currencies), while developed market volumes grew 8% – which the company said was due to more collaboration with emerging markets financial institutions.

The company also mentioned that IDOs tend to transact more in H2 but also demonstrated below-trend volumes in H1 2024, due to aid budgets being diverted towards domestic policy and away from cross-border amid changes in the political landscape.

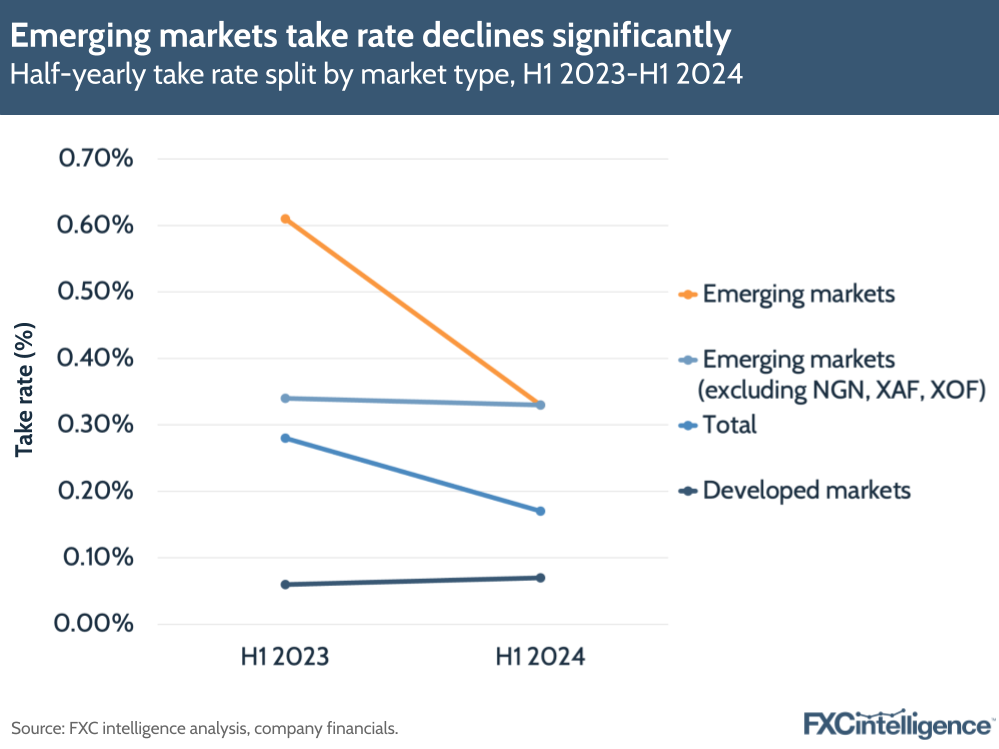

Volume slowdowns also affected CAB’s take rate, which declined from 28 bps to 17 bps over the period, with emerging markets seeing the biggest drop – from 61 bps to 33 bps. Having said this, the company argued the emerging markets take rate would have remained flat at 33 bps (compared to 34 bps in H1 2023) if excluding the affected currencies.

Historically, emerging markets currencies have made up the main share of CAB’s FX and cross-currency income (85% in FY 2023). In other words, the company’s main contributor to revenues for Wholesale FX (which includes bulk FX conversion fees without onward payment) and Payments FX (which includes foreign margin fees as well as fees for transfers to other countries) has been transactions where the selling currency comes from an emerging market.

However, in terms of actual volumes, more than half of the company’s FX and cross-currency income (60% in FY 2023) stems from transactions where the selling currency comes from a developed market, while lower volumes are transacted in currencies from emerging markets. This means that the company tends to have a higher take rate on transactions involving emerging markets currencies compared to developed market currencies. For example, this was 0.55% in emerging markets versus 0.06% in developed markets across FY 2023.

Amid this decline, the company is still making a profit but is feeling the impact of lower revenues versus growing costs due to annualised hires, more investment in tech and its growing global footprint (particularly in the EU and US). For example, staff costs grew 12%, while admin costs (largely linked to a new London HQ) grew by 30% and depreciation and amortisation grew 27%. As a result, EBITDA fell 53% in H1 2024, giving a significantly lower margin of 34% compared to 56% in H1 2023.

Unsurprisingly, CAB has taken steps to caveat its performance, saying that it still managed to see volume growth despite, according to the company’s analysis, market-wide payment flows in CAB’s core Sub-Saharan Africa market being down approximately 5% YoY and global flows being down 10% (it is worth noting that our own market sizing data does not reflect such a decline in the B2B market). However, it is evident that the company needs to change its strategy to reflect more diversity across geographies.

During the H1 2024 presentation, Kapur laid out the company’s new “execution-focused” approach to building a more diversified, sustainable company, which consisted of four pillars: strengthening the breadth and depth of its network; deepening the company’s existing relationships while expanding its client base; driving FX and payment volumes using its banking licence; and investing in technology and balance sheet management.

Growing and strengthening CAB’s network

CAB’s existing network has grown consistently, with the company expanding its total number of payment partners and liquidity providers to 358 (up from 331 at the end of 2023). In H1 2024, the number of payment partners grew 16%, while liquidity providers grew 8%, but Kapur wants these numbers to grow much faster to increase the company’s reach. He also noted that the network remains consistently focused on Sub-Saharan African markets, all being managed centrally from London, leaving the company over-concentrated.

A key goal therefore is to grow CAB’s overall number of providers, but also to form a stronger network by partnering with providers that can offer high-volume payment solutions, as well as investing in an on-the-ground presence in new and existing geographies. In addition to growth in MENA and LatAm regions, Kapur also mentioned broadening opportunities for business in Europe, where CAB recently acquired a payments licence, and said the company would soon enter the US market.

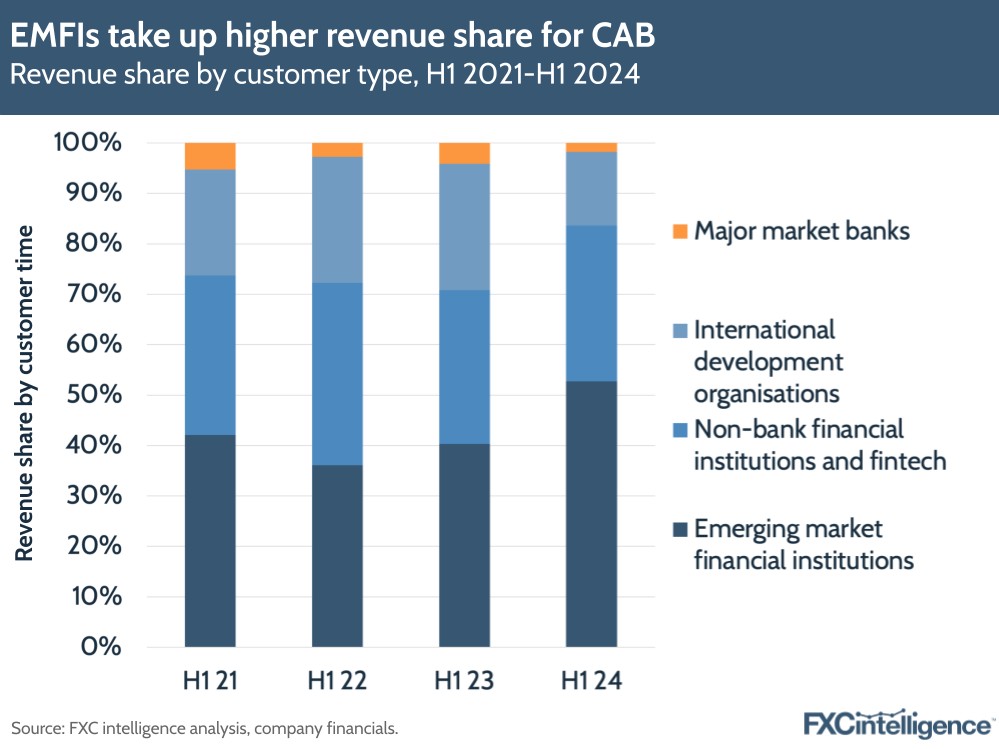

Looking at client growth, Kapur noted that the company grew its client base to 526, spread across major market banks, development organisations, non-bank financial institutions and fintechs. Over time, the company has seen EMFIs grow their share of revenue, making up 52% of its income revenue share in H1 24, while major market banks account for a very small share of revenues at 2%. It should be noted that this is reflective of the fact that EMFI revenue remained constant while CAB’s overall revenue shrunk.

Even though they present a good growth opportunity, Kapur said the long sales cycle for major banks meant it would de-emphasise the contribution of these banks to growth. However, the company is still seeing 66% of its customers generating less than £100,000 annum, which the company considers to be the tail end of the customers it is targeting. Monetising these customers (or exiting them if they can’t meet the quota) will therefore be a big focus going forwards.

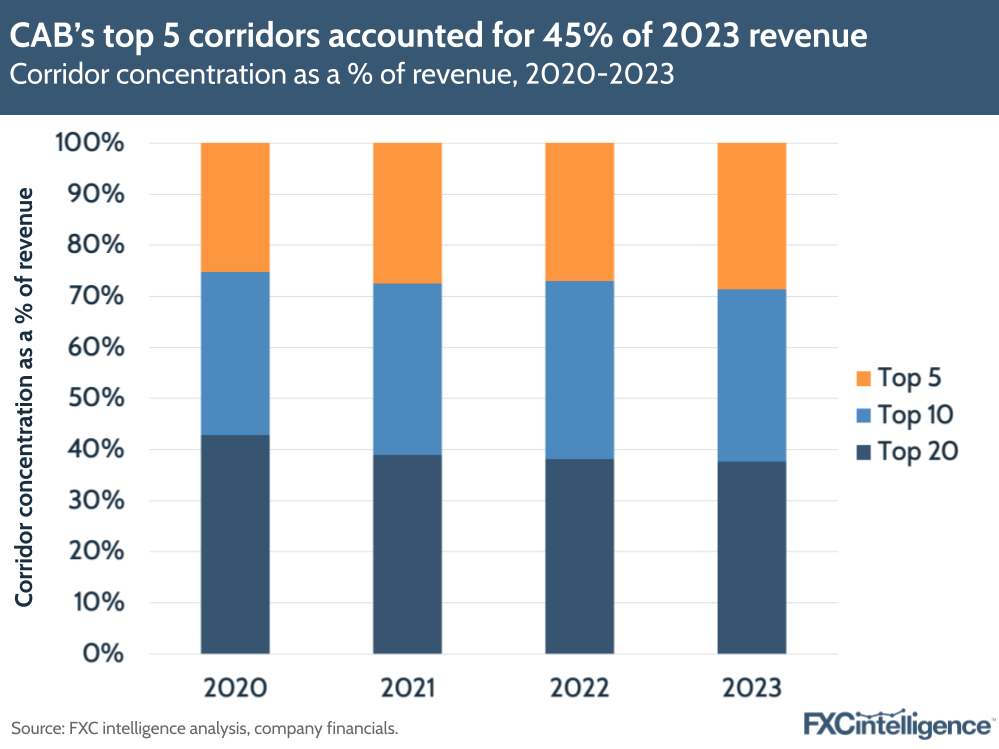

In addition, the company needs to ensure it targets customers operating over a wider array of currencies so that it isn’t too focused on corridors that are susceptible to volatility. In H1 2024, the company saw its top five currencies account for 32% of overall income, down from 49% in H1 2023 and 45% for 2023 overall. However, there is still more progress to be made, with the company hoping to offset dislocated currency impacts through expansion.

The impact of interest income on CAB’s revenues

On the company’s third pillar, CAB wants to accelerate FX and payments volume growth through its trade finance and liquidity as a service products – both of which are backed by the fact that CAB Payments is a licensed bank, unlike other fintech players operating in the region (though other players, most notably Revolut, have been chasing the acquisition of more licences recently).

By offering higher internal risk limits on these products for some of its biggest and most trustworthy clients, the company is trying to encourage higher volumes of trading through its platform, which would in turn grow its payment flows. It would also serve to boost interest incomes, which the company generates on the back of its customer deposits.

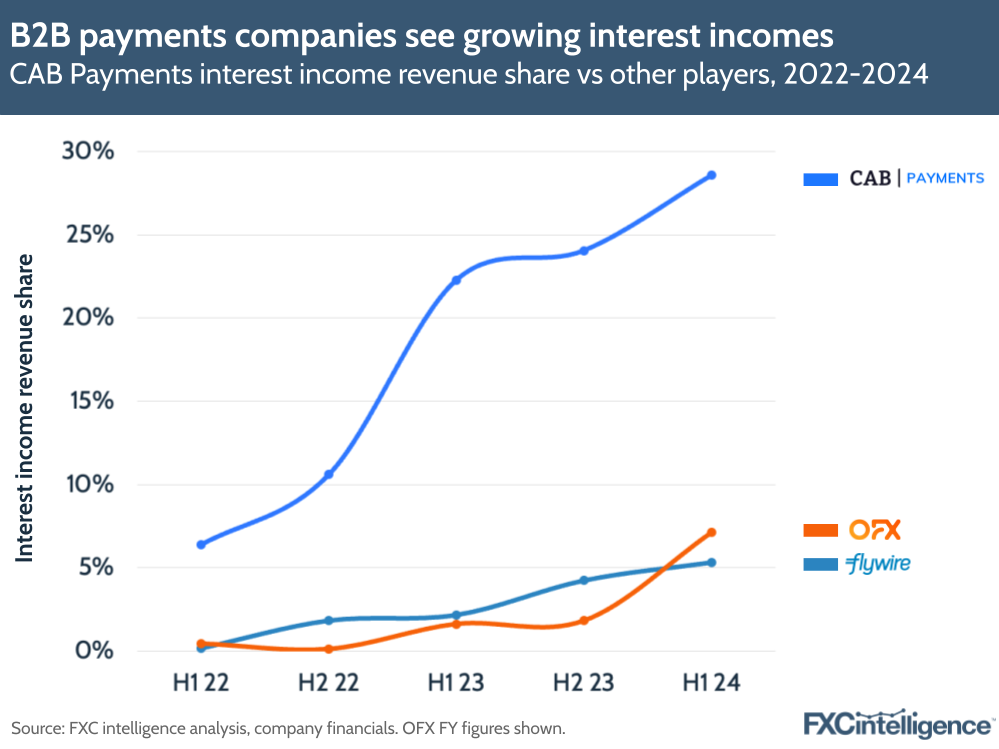

During 2023, CAB had mentioned that it had seen higher incomes due to “higher swap curves and an increased spread, as a result of the lower rates paid on deposit liabilities”, and had expected this income stream to decline in 2024. However, due to its growing balance sheet and changing expectations around rate cuts in the US and UK, interest income from cash management grew by 2% to £16.2m.

This means that net interest income accounted for 29% of CAB Payments overall revenue share for H1 2024, up from 22% in H1 2023 and 6% in H1 2022. For the first time on a half-yearly basis, interest income accounted for a higher share of revenue than the company’s payments division – which sat at 25%.

Although this shift in revenue share has been driven by the massive dip in Wholesale FX revenues (which still accounted for 41% of revenues in H1 2024), the ongoing strength of interest has been reflected by other players in the cross-border payments industry.

In a recent report, we noted that companies like Revolut, Wise and Payoneer are holding significantly higher customer balances in their accounts than in previous years while benefitting from high interest rates. We also highlighted that OFX and Flywire – two players that are looking to further grow their B2B money transfer divisions – are seeing interest incomes accounting for significantly higher share of revenues over time. For CAB Payments, its NGN struggles have made this effect more pronounced.

A concern that has been raised for some players has been the extent to which interest incomes could wane in the future as banks cut rates, with the Bank of England and Bank of Canada already making cuts this year and the US expected to do so imminently. CAB Payments currently includes net interest income in its EBITDA margin as it is reinvested to “generate returns for the shareholder” but if rates are cut, customers will need to hold higher amounts in accounts with the company for CAB to generate the same income.

CEO Neeraj Kapur said during the H1 2024 earnings presentation that net interest income would continue to be meaningful for the company going forward. In fact, CAB is trying to grow its transactional and interest income by increasing the limits for volumes that can be transacted through its liquidity and trade finance products. Rates continue to be high at the moment, but while this action could drive further payment flows, the company’s other steps to diversify will also be very important to ensure it doesn’t become too dependent on interest-related revenue streams.

Investing in new products and the Visa partnership

For its final pillar, the company talked about its aims for investment opportunities going forward. Interestingly, CAB’s banking model actually works against it in this area, with a significant proportion of its total capital (£89m out of £113m, as of June 2024) going towards meeting regulatory requirements.

Having said this, the company is looking to invest more in new products and enhancements, such as FX derivatives, next-gen payment rails and straight-through processing. Similar to other players in payments, the company is using AI to help it improve efficiencies in screening, processing and updating its core payment APIs, which it says will allow the company to process much higher volumes at lower costs.

CAB has also recently partnered with Visa to integrate its offering with Visa Direct, which will grow its reach and help it deliver lower-value, higher-volume payments more effectively in emerging markets, where the high risk of such payments can incur additional costs.

Visa Direct has been taken up by a number of players across the cross-border space, with recent major additions including digital challenger Revolut and UK bank Standard Chartered, as well as international messaging platform Swift to help streamline B2B payments.

How have other players been affected by emerging markets’ volatility?

CAB Payments is one of several players to see ongoing potential in emerging markets. Uruguay-based processor dLocal, for example, began in LatAm markets such as Brazil and Mexico, as seen in LatAm countries accounting for 81% of its Q2 2024 revenues, but has since expanded into Africa and Asia.

Meanwhile, US-based Payoneer also continues to see high potential and growth in these regions, with APAC accounting for 15% of its Q2 24 revenues, LatAm accounting for 10% and South Asia, Middle East and North Africa accounting for 11%.

But while emerging market currency corridors present valuable opportunities, potential volatility in some of these markets can impact companies’ bottom lines. The Nigerian naira is a particular example of this and has continued to struggle in 2024, having lost 36% of its official value in June 2023 after the central bank removed trade restrictions on the currency. Foreign exchange scarcity for the NGN has also been a persistent problem for Nigeria, which in turn drives up the cost of exchanging naira into US dollars.

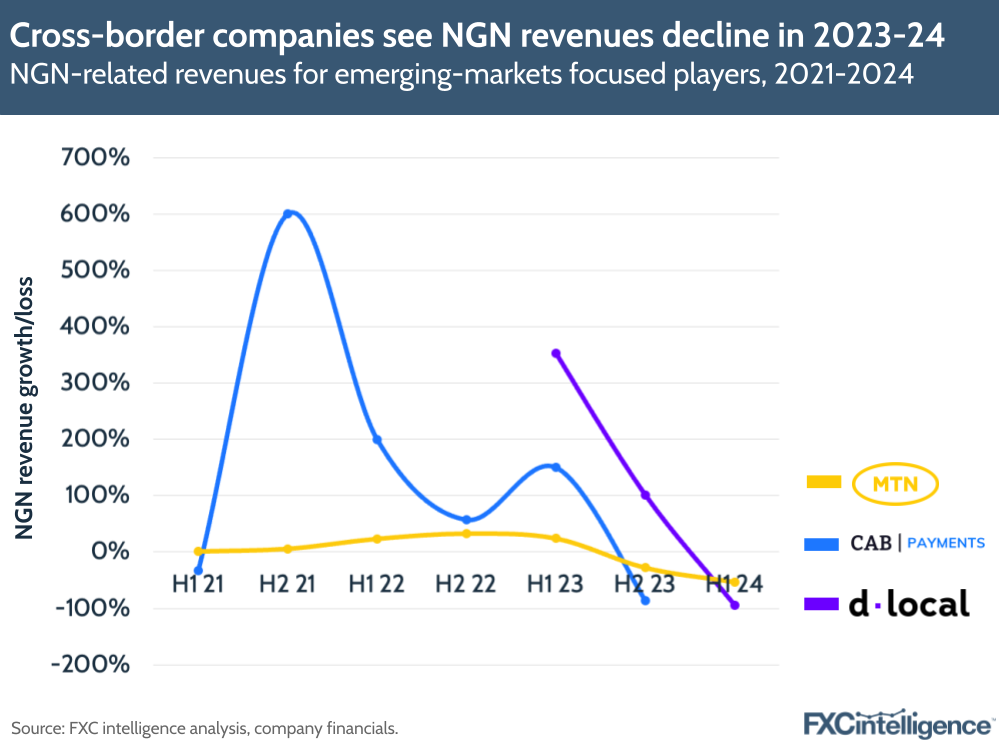

In CAB’s case, the volatility is demonstrated in changes for NGN-related revenues specifically. The company saw 150% growth in NGN revenues in H1 2023, though in the second half of last year its NGN revenue had dropped by 86%, meaning it accounted for a 5% share of total revenues in H2 2023, compared to 30% in H2 2022. In H1 2024, CAB didn’t report NGN incomes separately but alongside XAF and XOF, which altogether accounted for £8m in H1 2024, down from £29m in H1 2023.

Meanwhile, MTN Group – which claims to be Africa’s largest mobile network operator and has a significant fintech division – saw revenues decline by 21% in H1 2024 on the back of a 53% drop in Nigeria revenues due to the currency devaluation, with NGN’s share in MTN Group’s revenues falling from 40% to 24%.

Similarly, dLocal has borne the brunt of naira values falling, with its Nigeria revenues falling 95% in Q2 2024, driving a 5% YoY revenue decline in dLocal’s Africa and Asia segment. However, the company did note that despite a hit to revenue, its total payment volumes still rose 38% in Q2 2024 due to its diversification across multiple low-risk, high-reputation verticals.

This supports CAB’s plan to diversify not only its revenue streams, but also ensure that it is continuing to innovate when it comes to providing new products and services to get the most out of its customers. When it comes to moving to new geographies, it is also following the lead of companies like Intermex, which is a consumer-facing business but has also been expanding to Europe with the aim of capitalising on digital opportunity while offsetting recent FX headwinds in its core market Mexico.

Going forward, CAB’s focus on expanding its network will be crucial for making it more resilient, though with its European licence only just acquired and expansion into the US still pending, it will continue to see its main cross-border income streams coming from these markets for some time. Partnerships with big players like Visa could be instrumental in helping the company grow quickly, while strategic investment will be key in the coming months to show investors that the company can be resilient.