USDC stablecoin maker Circle has made its S-1 IPO filing public, giving an unprecedented view into how the company is being run. We take an in-depth look to get a sense of how the stablecoin major is growing and what its cross-border payments priorities are.

Four years after it made its first attempt to go public via a SPAC merger, and a year after its second attempt via a private IPO filing, stablecoin major Circle has made its IPO prospectus public.

Whether this latest bid to become a public company ultimately proves to be successful remains to be seen – Circle is rumoured to be pausing its IPO efforts amid the unfolding US tariffs, just as Klarna and eToro have – however the S-1 document still provides an unprecedented opportunity to review the financials of the most significant US stablecoin player currently operating.

In this report, we review the numbers and key discussion points covered in Circle’s IPO prospectus, comparing them to those in its previous SPAC report where relevant, to get a sense of how the company is developing, where it is generating revenue and what its strategy is for its future growth.

Circle’s evolution as a business

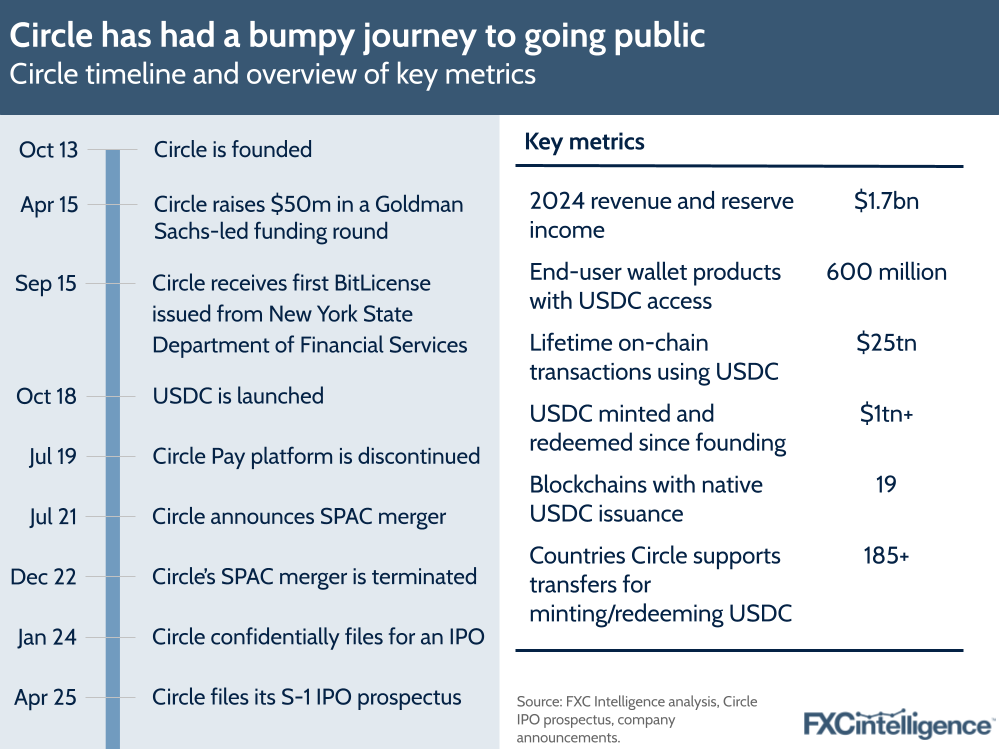

Now approaching its twelfth birthday, Circle has seen solid growth as a business, although its journey has not been without its challenges.

When it launched, the company’s proposition was quite different from its current iteration, focusing on providing consumers with a digital wallet for bitcoin that was pitched as a more accessible way to get into crypto than many of its contemporaries.

However, this evolved when the company became the first recipient of a New York State Department of Financial Services BitLicense in 2015. This enabled it to launch Circle Pay, which added the ability for consumers to hold, send and receive both US dollars and Bitcoin, a service which the company marketed as a low-cost form of cross-border P2P payments. In 2017, having shifted away from the Bitcoin part of the offering, Circle’s website led with the line: “Send money like a text. No fees. No borders. No one else is doing this.”

By 2018, however, the company began to pivot. Buoyed by total investment of more than $240m, it bought the Poloniex cryptocurrency exchange, as well as equity crowdfunding platform SeedInvest, before forming the Centre Consortium, a joint venture between it and cryptocurrency major Coinbase. The goal of this consortium was to launch non-volatile cryptoassets in the form of stablecoins and its first and primary release was USDC, which made its debut in October of that year.

In its release announcing the launch, Circle said that USDC was designed to provide a much-needed “safe, transparent and trustworthy layer for fiat to operate over open blockchains and within smart contracts”.

Adoption was fairly rapid, with USDC seeing a market cap of more than $300m within the first three months of its release, and the company quickly shifted its focus to stablecoins, closing Circle Pay and spinning out Poloniex later in 2019.

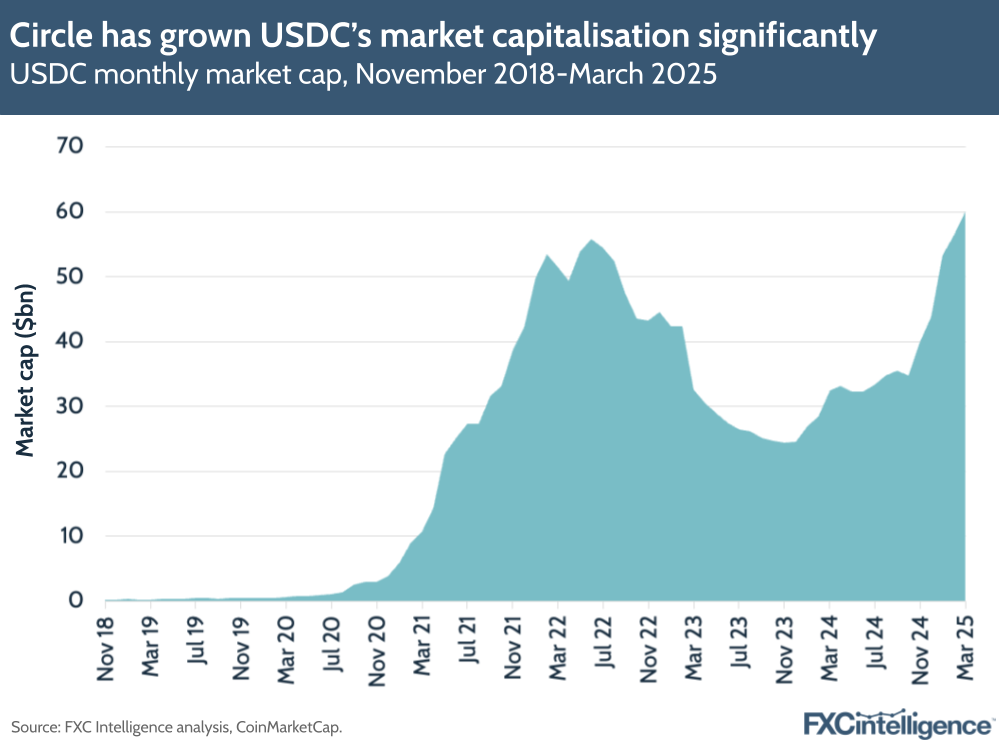

As the pandemic hit, USDC surged, with its market cap passing the billion-dollar mark for the first time in July 2020, and then $10bn in March 2021. Meanwhile, it was attracting growing attention from mainstream financial institutions, with Visa announcing its support for settlements using the stablecoin that same month.

Amid this growing enthusiasm for the stablecoin, Circle made its first attempt at a public debut, via a merger with special-purpose acquisition company (SPAC) Concord Acquisition Corp in a deal valuing the company at $4.5bn. As it worked to get the deal over the line, the company also built out its transaction and treasury services offering with business-targeted Circle Account and secured a growing number of deals with cross-border payments players, as well as launching Euro-backed stablecoin EURC. Meanwhile, USDC’s market cap climbed to a then-peak of $55bn in mid-2022.

However, with market enthusiasm for SPACs rapidly failing, the merger crumbled, and was ultimately called off in December 2022. Just a few months later, the company was also hit by the collapse of Silicon Valley Bank (SVB), which at the time held 8% of Circle’s reserves for USDC, briefly causing the stablecoin to lose its peg and drop below a dollar in value.

Circle, along with much of the stablecoin industry, worked to correct misconceptions about the security of the stablecoin, but the incident caused a significant drop in market cap as many users switched away to international-based rival Tether’s USDT.

2023 therefore became a year of readjustment and rebuilding for Circle. The Centre Consortium was dissolved, giving Circle full control over USDC, while Coinbase shifted to a collaboration agreement with the stablecoin company. Circle also sold its main Seedinvest assets, discontinued non-core business areas including consumer accounts and made several redundancies.

Meanwhile, the company worked to generate support for the US stablecoin industry, with CEO Jeremy Allaire urging Congress to regulate the sector, and began to grow its work in government and policymaking spaces, contributing to improved legislation in multiple jurisdictions, as well as touting its work to increase financial inclusion and support Web3-related research.

Circle then filed a confidential IPO document in early 2024, though this ultimately did not translate into anything further, potentially as a result of the challenging economic climate. However, with the now more streamlined company seeing increasingly positive results from its efforts to move in policymaking circles and its market cap finally passing its previous peak in early 2025, Circle has once again taken steps to become a publicly traded company.

Financial position and impact of Coinbase agreement

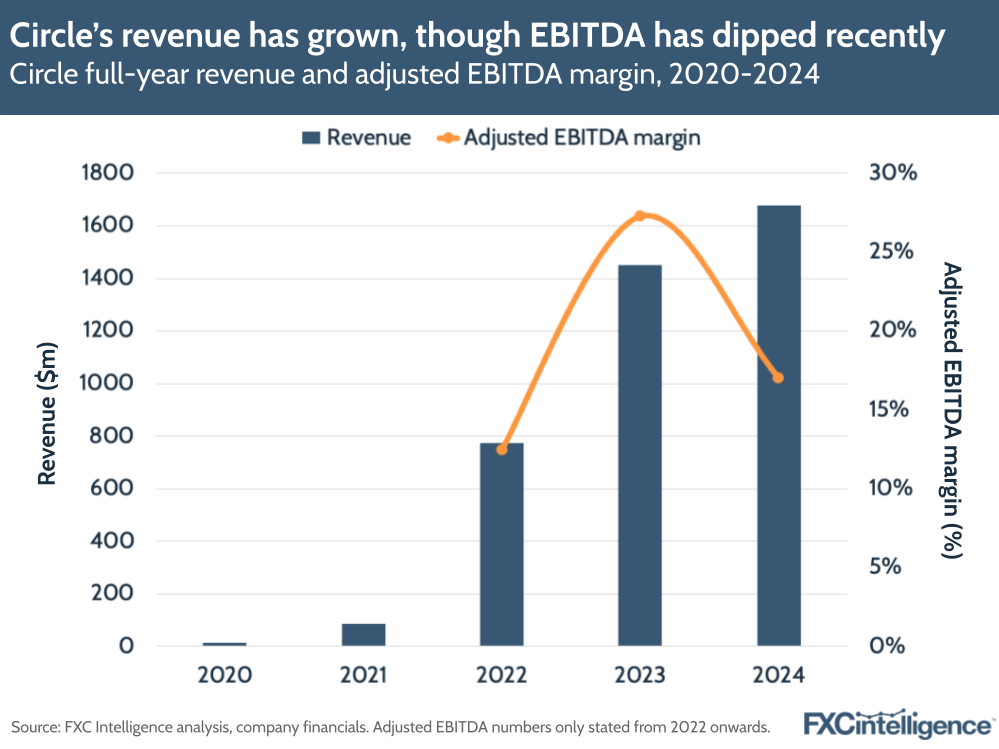

Despite its bumpy journey, Circle has consistently seen strong financial performance. As it scaled during the pandemic, it saw very high revenue growth, which jumped 450% YoY in 2021 and 808% in 2022. Meanwhile in 2023, despite the challenges it faced that year, it still saw revenue increase by 88%, breaking the billion-dollar mark for the first time to reach $1.5bn.

In 2024 its revenue growth was a more reserved 16%, reaching $1.7bn, although this is likely an indicator of a business that is maturing out of its rapid growth stage. Meanwhile, while it had a negative adjusted EBITDA margin in 2021, this has been positive since, and the company has reported net profits since 2023.

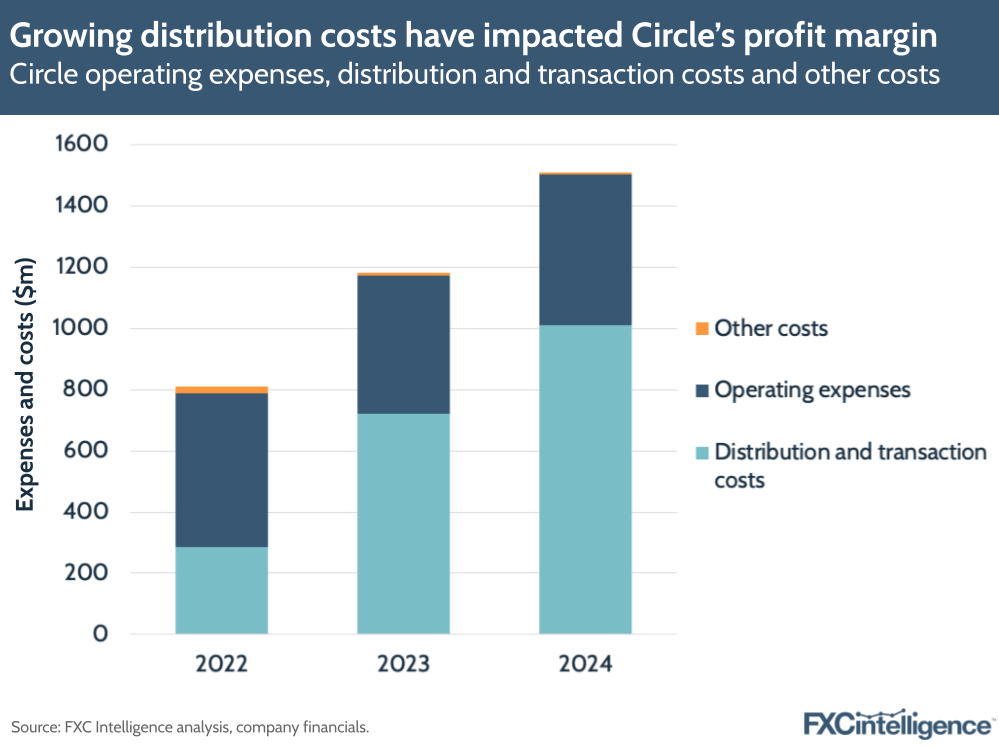

While the company’s revenue climbed between 2023 and 2024, its adjusted EBITDA reduced by -28% to $285m, resulting in a 17% adjusted EBITDA margin, compared to 2023’s 27%. This drop is not the result of rising operating expenses – Circle saw these increase only slightly between 2023 and 2024 after a decline from 2022 – but is instead largely the result of a climb in distribution and transaction costs.

These costs grew by 40% YoY in 2024 – an extra $291m – having already grown by 151% the previous year.

While this is partially the result of an increase in distribution incentives to strategic partners, including a one-time fee to Binance, the vast majority of the increase is due to a significant rise in distribution costs paid to Coinbase. This cost rose by $217m in 2024, following changes to the way it was calculated under the Collaboration Agreement Circle entered with Coinbase in August 2023.

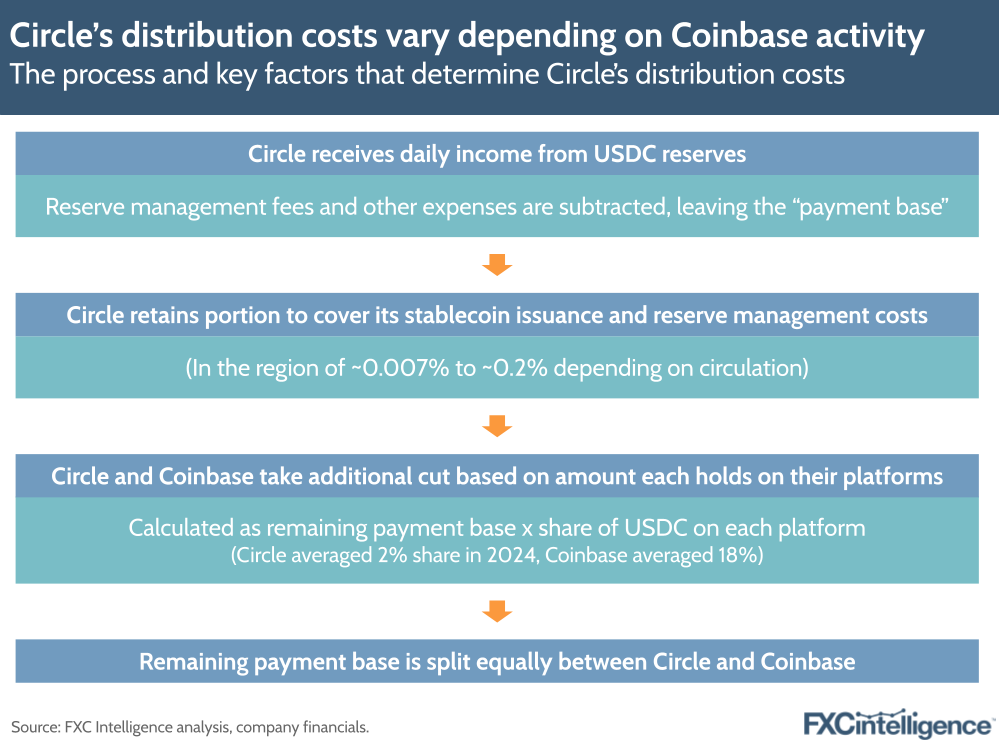

Prior to this, as joint owners of the venture behind USDC, Circle and Coinbase shared revenue generated from USDC’s reserves on a pro-rata basis, depending on the amount distributed by each party. However, when Circle took full control of UDSC it shifted to a model where it retains revenue but pays out distribution costs to Coinbase that vary depending on how much of the stablecoin is held on the crypto player’s platform.

This means that the more USDC Coinbase holds on its platform, the greater Circle’s distribution costs, with the stablecoin player warning in its IPO prospectus that its “distribution costs are impacted by the actions and policies of Coinbase and their effects on the amount of USDC in circulation held on Coinbase’s platform”, adding that this is something that it does not “control or oversee”.

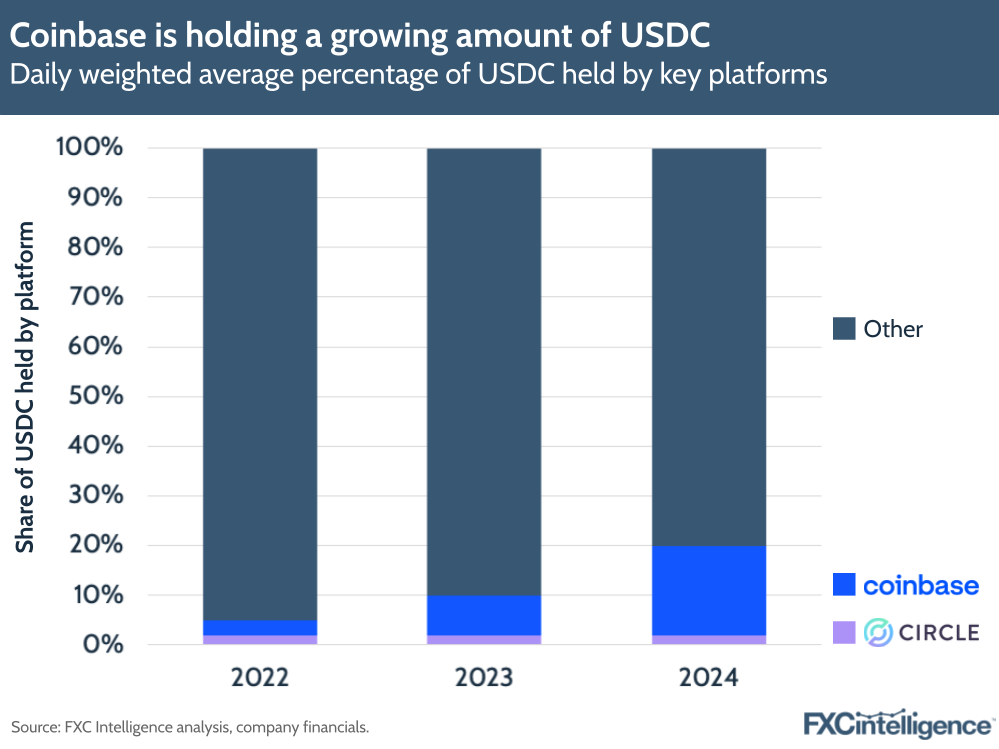

Notably, the amount of USDC held on Coinbase’s platform has grown and appears to be continuing to grow. In 2024 it grew the share it held from a daily weighted average of 8% to 18%, and by 31 December 2024 this share had increased to 20%.

How Circle makes its money: Reliance on reserve revenues

Comparing financials from Circle’s 2021 S-4 document for its proposed SPAC merger and the S-1 IPO prospectus it has published this year provides some significant insights into how much the company’s financial makeup has transformed.

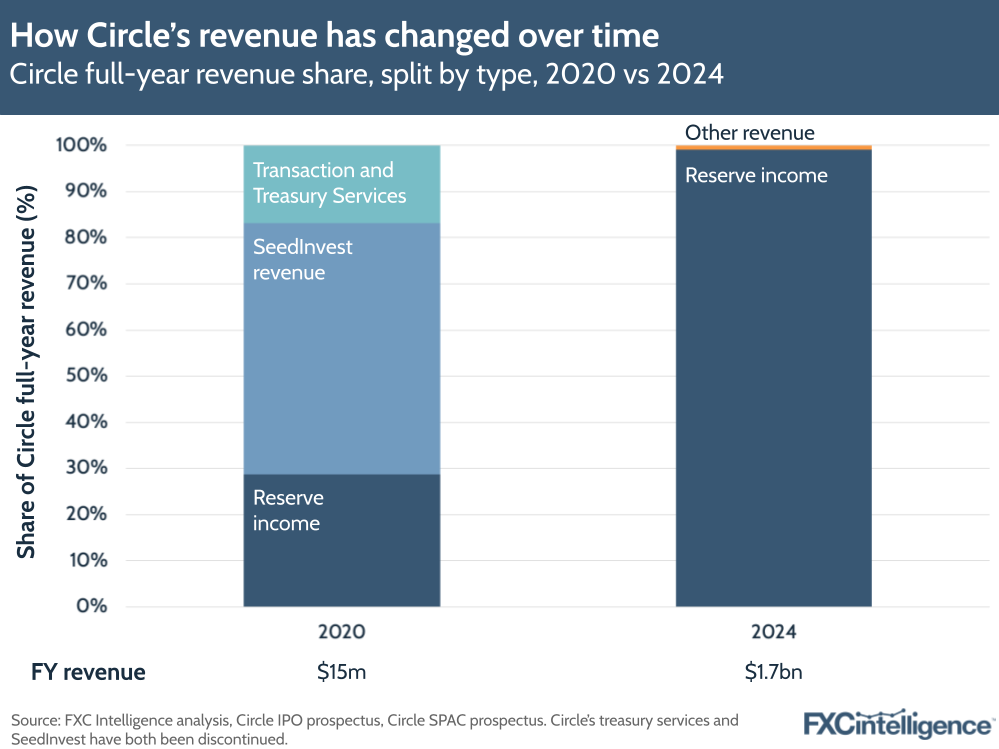

In 2020, its crowdfunding platform SeedInvest accounted for 55% of its revenue, while reserve income accounted for just 29%, with Transaction and Treasury Services making up the remaining 17%.

However, with the company having divested most SeedInvest operations and ceased all activities relating to it in early 2023, this is no longer a contributor to its 2024 revenue, nor is Transaction and Treasury Services, which covered its now-discontinued USDC payments processing business and Circle Yield product, as well as its consumer accounts.

As a result, reserve income – interest income from the reserves Circle holds to underpin its stablecoins, mostly USDC – now accounts for 99% of the company’s revenue.

This means that the company’s profit is directly linked to growing use of USDC and very little else, allowing it to build all its activities around this single goal. However, it also has the potential to expose the company to risk, most notably around the rate of return it gets on the assets, and how those may be impacted by changes to interest rates.

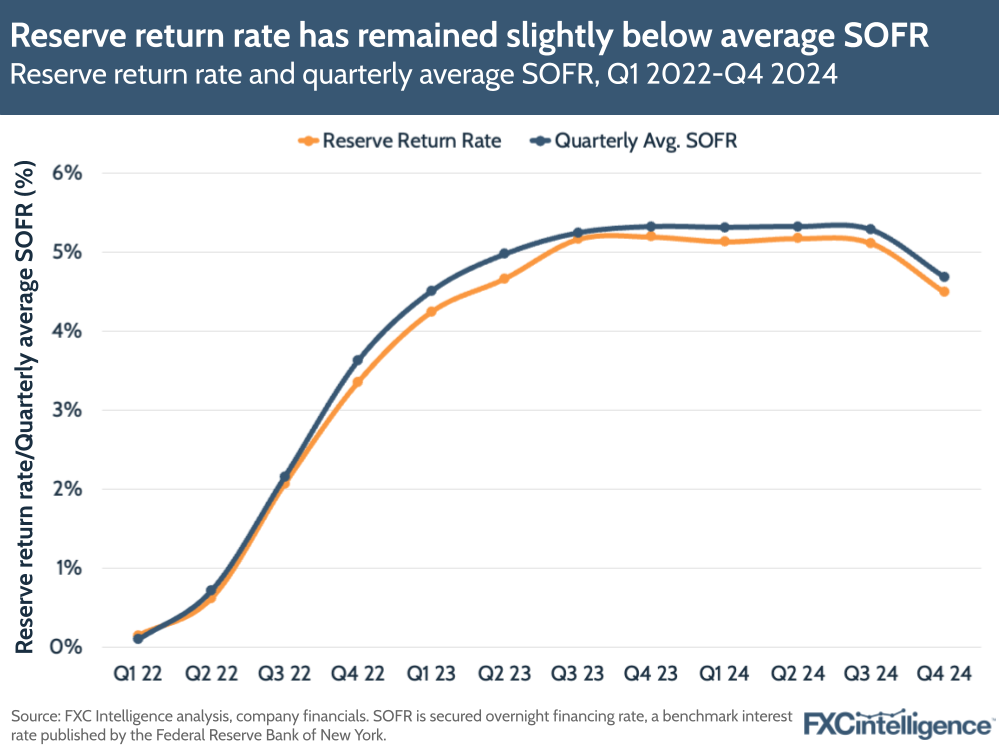

Circle has highlighted that it has historically earned reserve income at a return rate that is slightly below the secured overnight financing rate (SOFR) – a benchmark interest rate often used to reflect the cost of borrowing cash overnight.

This is likely due to the fact that the reserves are in highly liquid and safe assets. Circle’s reserves are held partially in cash at reserve banks, but largely in a reserve fund that combines short-dated US Treasuries, overnight US Treasury repurchase agreements and cash.

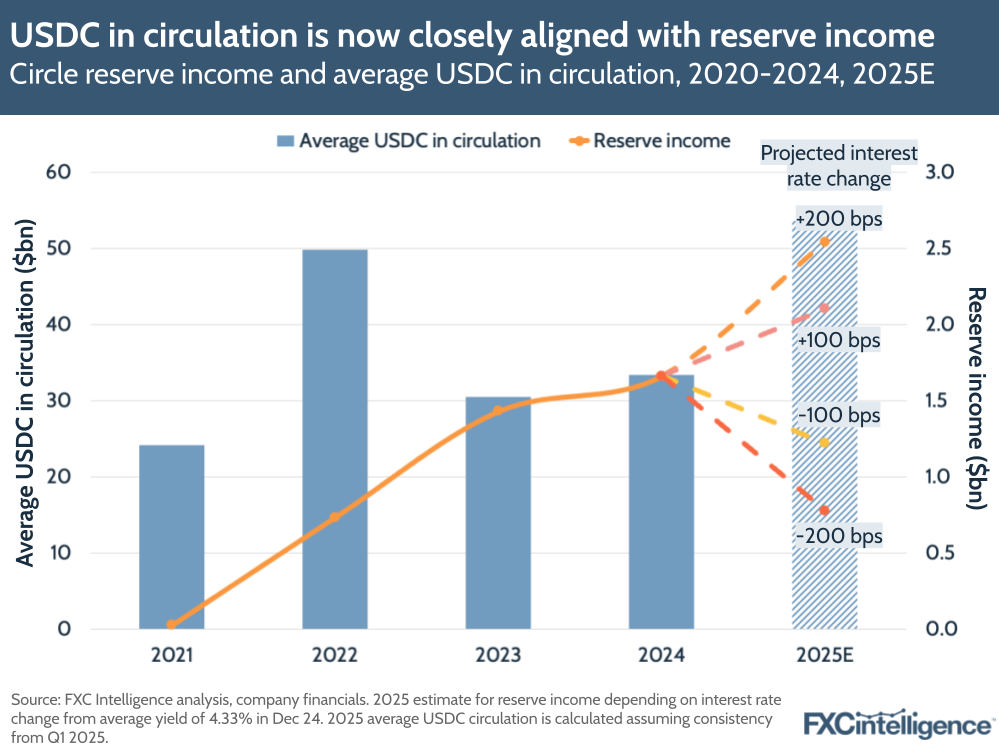

While the Coinbase agreement has seen Circle’s costs increase, it has also helped enable the company’s reserve income to much more closely align with the average USDC in circulation since 2023.

As a result, the biggest variation in predicted reserve income beyond the market cap of USDC stems from variations in interest rates, with Circle providing estimates for 2025 reserve income and costs based on potential changes in interest rates.

For example, the company estimates that if there was a 200 bps rise in interest rates in 2025, it would see an additional $882m in reserve income but incur an additional $468m in distribution and transaction costs, for a net income increase of $414m. Meanwhile, a 200 bps reduction would incur the same in reverse, for a net income reduction of -$414m.

This is particularly key in light of the recent tariffs as, depending on how things evolve, interest rates could be impacted in a number of ways. The potential increase in the cost of imported goods in the US may contribute to overall inflation, prompting the Federal Reserve to increase interest rates in response, which would be positive for Circle.

However, the ongoing uncertainty and potential global trade war that is unfolding is also raising concerns about an economic downturn in the US and even a full recession. If this becomes more pronounced, the Fed may opt to cut interest rates to stimulate the economy, which would have a negative impact on Circle’s reserve income. Federal Reserve Chair Jerome Powell has said that the Fed is “going to have to wait and see how this plays out” before making adjustments, meaning there remains significant uncertainty in how Circle will ultimately be affected by the tariffs.

Increasing adoption and use of USDC

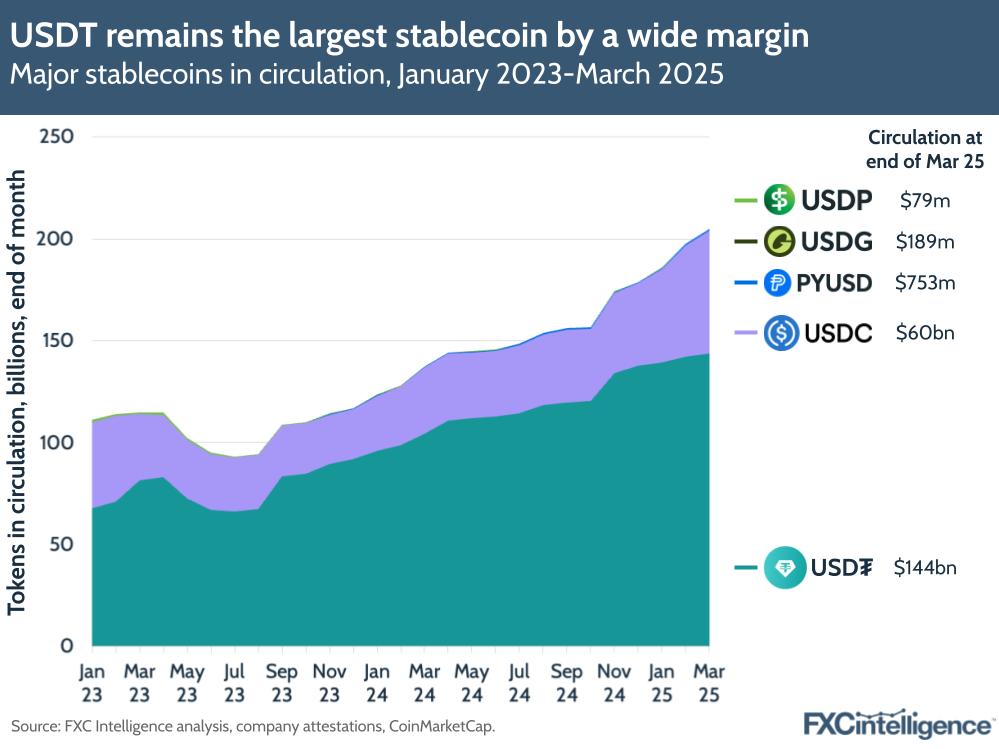

Beyond reserve income, growing adoption of its stablecoins, particularly USDC, is a clear priority for Circle. This is something it has been showing success in: the company has seen the number of tokens in circulation grow sharply over the past six months, to reach a new market cap high of $60bn in March 2025. By contrast, EURC is currently at an all-time-high market cap of $180m.

However, USDC is designed to serve as a “bridge between the fiat and digital assets ecosystems”, as the company puts it, allowing companies to operate in the digital currencies space and to make use of the capabilities of blockchain-related systems without needing to hold volatile cryptoassets.

For many, this will include moving money in and out of USDC on a regular basis, either converting it to fiat currencies or to cryptocurrencies, particularly for those using the stablecoin to store value in between trading.

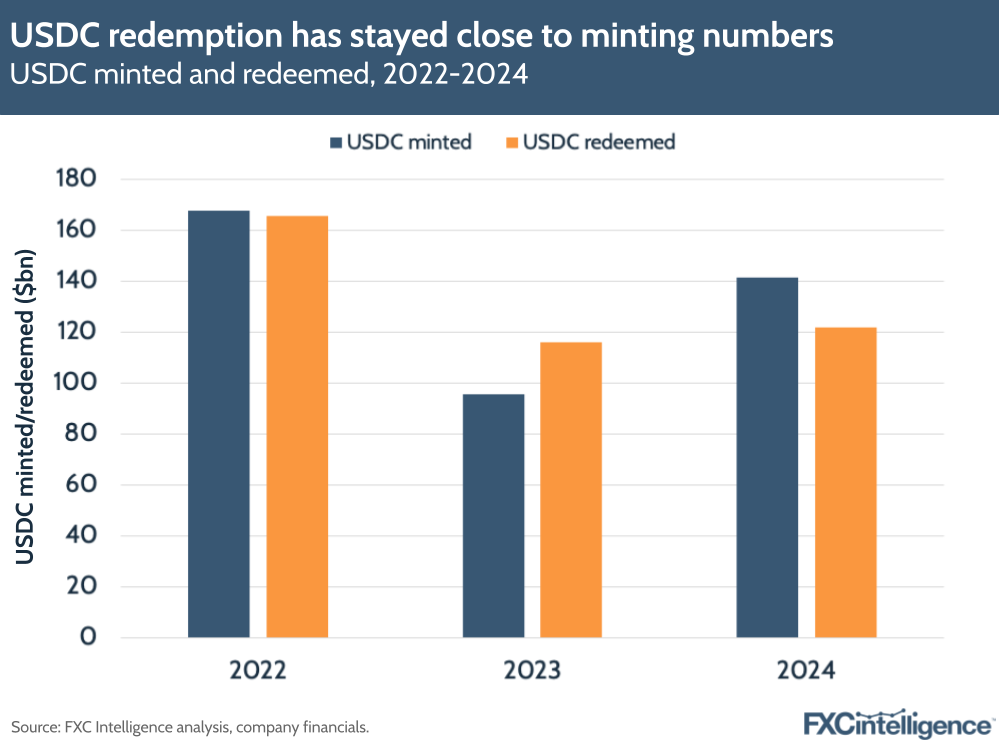

Whenever USDC is purchased, a new virtual token, or coin, is ‘minted’, while when it is redeemed that coin is destroyed or ‘burned’. As a result, data on minting and redemption of USDC gives a sense of how much value is being moved in and out of the stablecoin each year.

In 2023, when the collapse of SVB caused many to move their money away from USDC, Circle saw more of the stablecoin redeemed than minted. However, in 2024 this trend reversed, with more value being moved into the stablecoin than out of it.

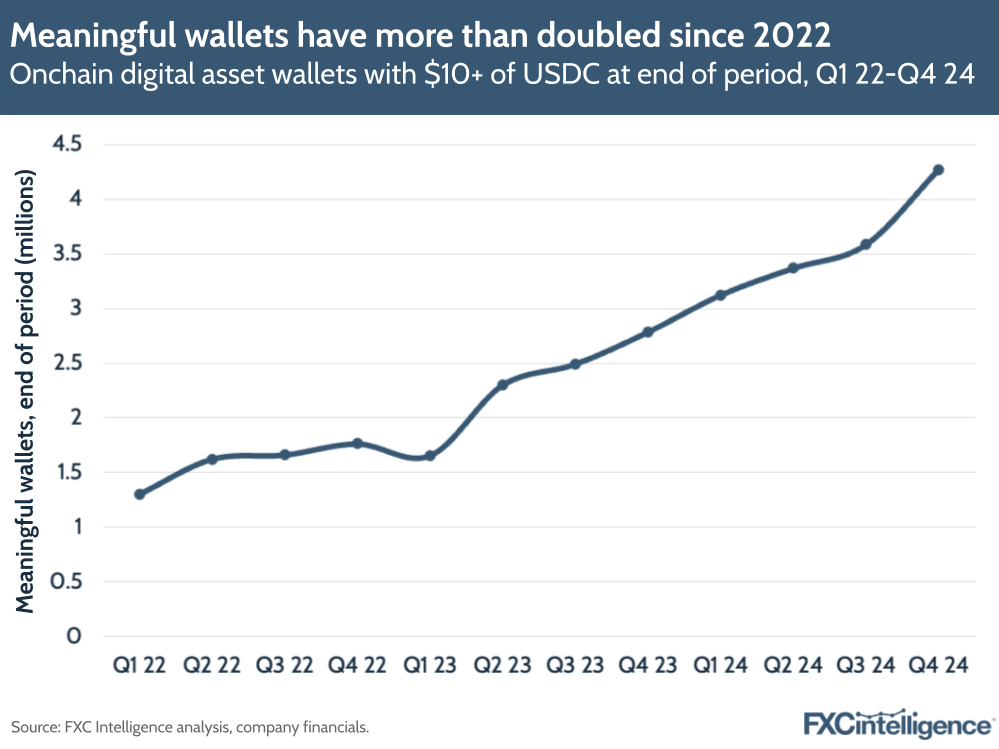

Alongside this, Circle’s tracking of ‘meaningful wallets’ also provides a key metric for USDC adoption trends. Also referred to by the shortened term MeWs, these are on-chain digital asset wallets that contain at least $10 of USDC. While they do not provide an indication of the number of unique users holding a meaningful quantity of the stablecoin – it is commonplace for users to have multiple wallets – they do provide a sense of the growing use of the stablecoin between the points that it is minted and burned.

Here, Circle has identified significant growth in MeWs, which climbed from 1.3 million in Q1 2022 to 4.3 million in Q4 2024. Notably, they also showed a quick recovery from the impact of the SVB collapse, with only Q1 2023 seeing a decline in MeWs before Q2 2023 returned to growth, at a sharper trajectory than had been seen across 2022.

Circle’s place in the wider stablecoin market

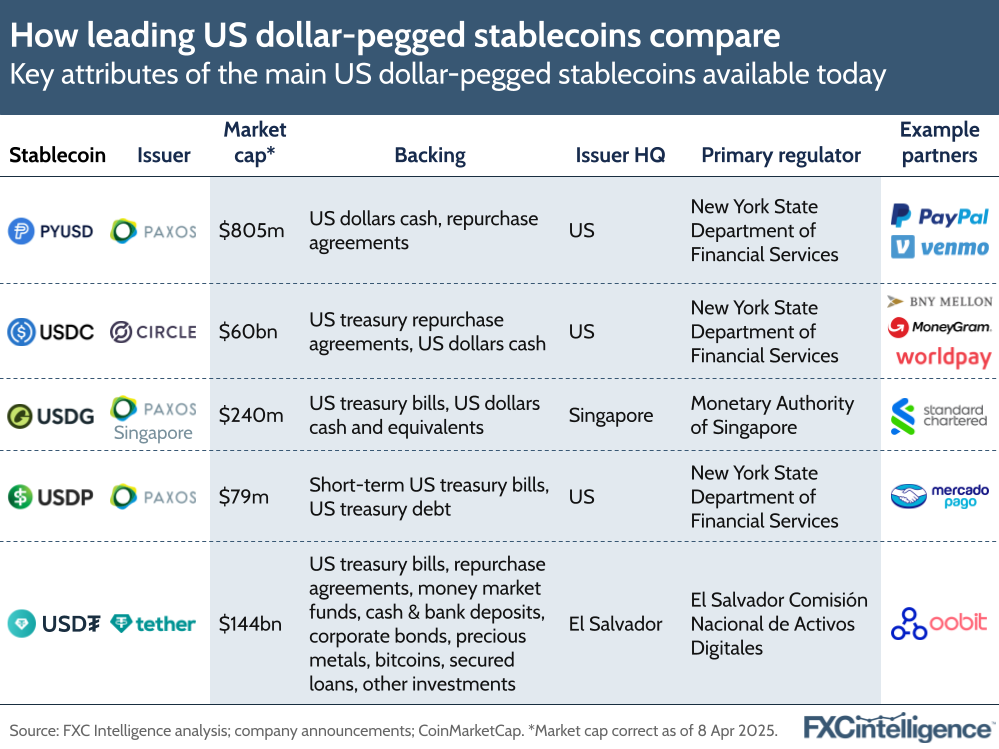

While USDC is one of the biggest names in the stablecoin space, it is by no means the only US-based stablecoin on the market. Paxos is the other major stablecoin issuer headquartered in the US and is behind its own USDP, as well as PayPal’s PYUSD stablecoin. Its Singaporean arm also recently launched USDG, a US-backed stablecoin specifically designed to be compliant with the Monetary Authority of Singapore’s upcoming stablecoin framework.

Tether, which was headquartered in the British Virgin Islands until its recent move to El Salvador, is also a key stablecoin player, with USDT being its most popular. Several other companies have also begun to launch their own stablecoins, including Ripple’s RLUSD, which was integrated into its cross-border payments platform at the start of April after being launched last year. Meanwhile, Stripe recently acquired stablecoin platform Bridge, raising speculation about whether the company, which currently uses USDC among others, will launch its own US dollar-backed stablecoin.

In terms of circulation, however, most stablecoins remain extremely small in terms of use compared to USDC and USDT, with the latter leading in terms of market capitalisation by a wide margin. While prior to SVB’s collapse USDC was approaching parity with USDT, the latter now has more than twice the market cap of the former.

However, there are some areas where USDC has an advantage over USDT. While USDT has gained traction among end-users as a store of value between crypto trades, and is seeing adoption in some emerging markets where stablecoins are being explored as an alternative to volatile fiat currencies, USDC has a much stronger position among Western institutional users.

This is because its regulatory position and backing make it a much easier choice in terms of compliance. While USDC is solely backed by highly liquid mainstream financial assets, and is regulated by a US regular, USDT does not have the same direct regulatory oversight and is partly backed by Bitcoin, precious metals and a variety of other investments. It also provides less transparency: although like Circle it publishes reserve reports for its stablecoin, Tether only produces these once a quarter, rather than the once-a-month cadence of Circle and Paxos.

Growing Circle: Target markets and growth priorities

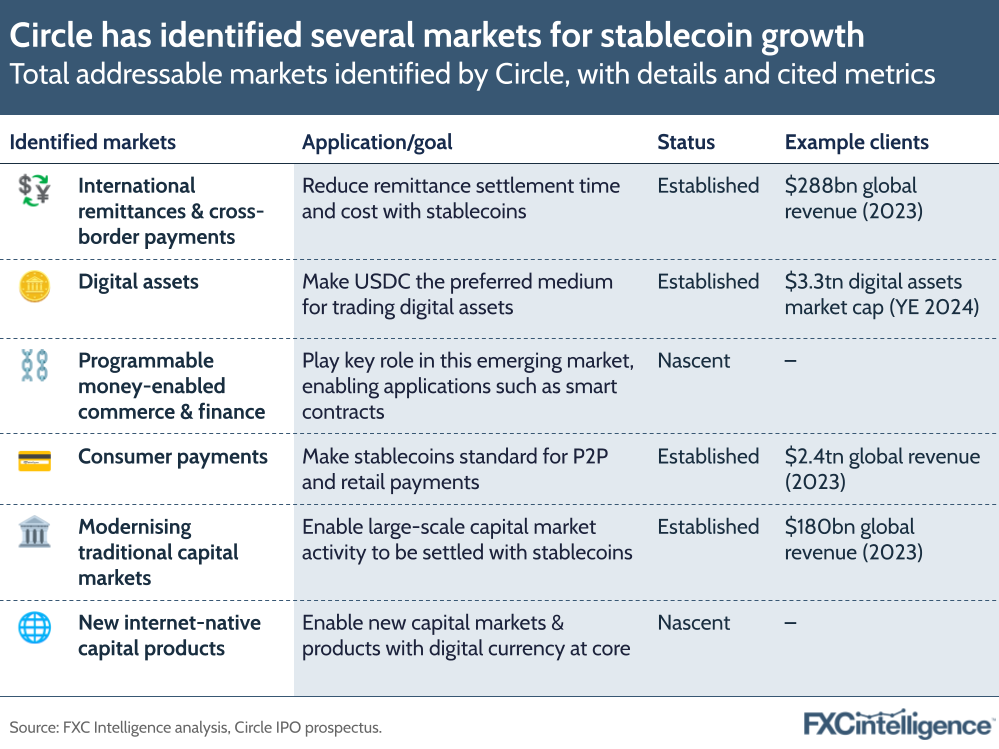

While Circle is ultimately looking to continue to grow use of its stablecoins, how it is approaching this is more complex, as it sees applications across a wide range of use cases. Stablecoins have potential in a variety of markets, with the company identifying multiple verticals where it sees potential for growing use of USDC.

Some of these are well-established. While it remains a minority solution in the wider market, Circle has already seen growing adoption for international remittances and cross-border payments, with previous examples including a partnership with MoneyGram to send remittances using USDC on the Stellar network, while Félix and BCRemit are examples of smaller remittance players using the technology.

USDC is also being used on the working capital side of the cross-border space; Arf uses the stablecoin to provide short-term working capital to remittance providers and Thunes and Circle launched a stablecoin liquidity management solution in October.

Similarly, use of USDC for retail payments has also seen limited but growing support, with Stripe going live with USDC stablecoin payments in 2024, while the company is well-established in digital assets trading, including being the preferred dollar stablecoin on Coinbase, the largest US-based cryptocurrency exchange. It also entered a strategic partnership with Binance in December to deepen its use on the exchange.

In more nascent markets, the company is also growing interest, with USDC being used by Goldfinch to support loans to emerging markets businesses, while a host of smaller Web3 innovators are developing solutions using the technology.

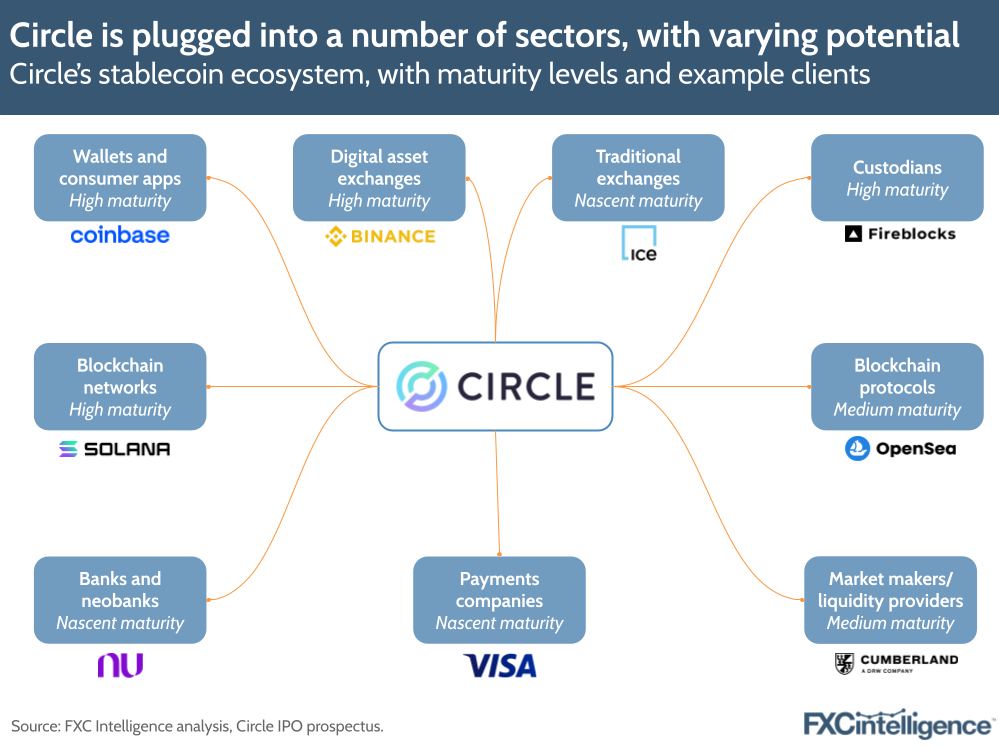

In order to meet the needs of these varying markets, Circle operates within a wider stablecoin ecosystem, which it detailed as part of its prospectus. Here it highlighted how it has a well-established presence working with digital asset wallets and consumer apps, crypto exchanges, blockchain networks and custodians, and has a solid presence in the growing blockchain protocol space and with liquidity providers.

However, it also highlighted that it is still growing its presence with traditional exchanges, as well as banks, neobanks and payments companies.

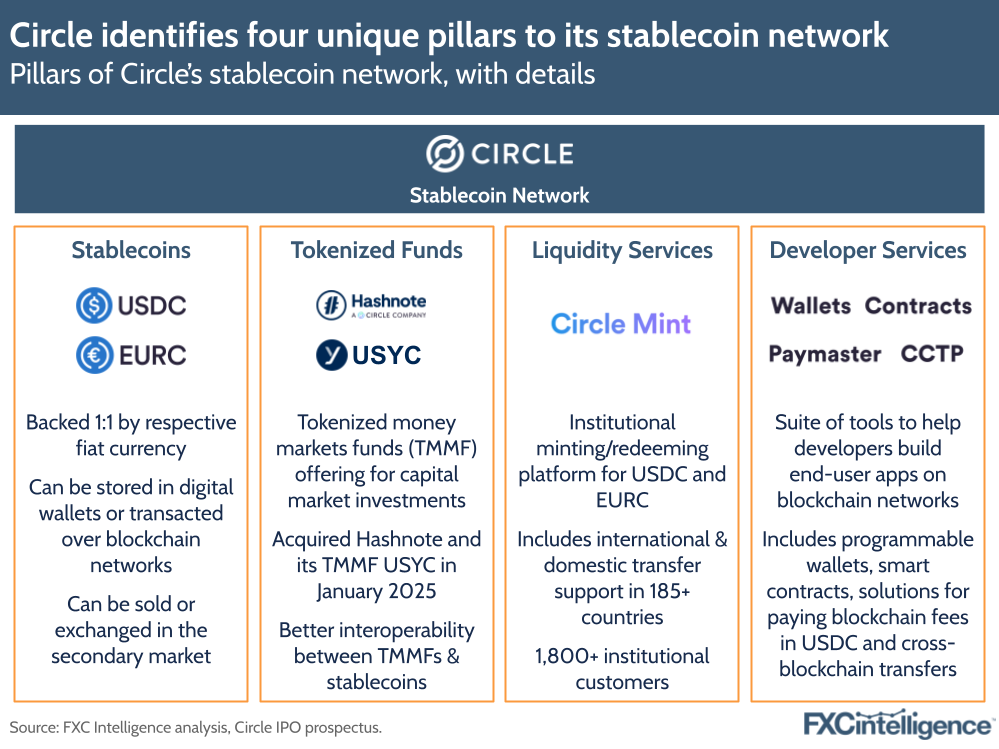

In order to develop its presence in these various markets and sectors of its ecosystem, Circle is building out its capabilities to better support a variety of efforts, and as of Q1 2025 has four pillars that make up the company’s offering.

While its USDC and EURC stablecoins are one key part, Circle has also built out other elements that, for the most part, currently have limited direct revenue contributions but are either designed to boost the supply of stablecoins directly or grow to become significant contributors in the future.

Circle Mint, which forms the company’s liquidity services offering, is perhaps the most mature of the other pillars. It enables institutional customers such as banks, wallet providers and exchanges to mint and redeem the company’s stablecoins directly, with support for international and domestic bank transfers in over 185 countries.

The service, which currently has over 1,800 customers, generates additional revenue for Circle through a tiered redemption fee structure, reported as part of its ‘other revenue’ segment. The company has identified the segment as key to its future growth, saying that “the ability of Circle Mint customers to quickly and confidently move from fiat to Circle stablecoins is essential to the growth of the Circle stablecoin network”.

Alongside this is the newly created Tokenized Funds pillar, which Circle has formed following its acquisition of the world’s largest tokenized money market fund (TMMF) player, Hashnote. A blockchain version of a traditional money market fund, this allows investors to hold and trade shares as digital tokens, which are held in US treasury-based USYC tokens on Hashnote.

By acquiring Hashnote, Circle has the ability to increase interoperability between TMMFs and stablecoins, giving adoption USDC the ability to grow as use of TMMFs climbs.

The fourth pillar, meanwhile, is Circle’s developer service, which consists of a suite of tools designed to make it easier for developers to build products and services on blockchain networks that utilise USDC. As the company has identified commerce and finance using programmable money as a nascent area for it to build a presence in, these tools allow it to embed itself in this sector as it is developed, ensuring it will again grow with the sector.

Among the solutions Circle has provided in this area are programmable wallets, enabling developers to easily integrate digital wallets into web and mobile apps, with around 10 million on-chain wallets having been deployed using the solution, including by Southeast Asian superapp Grab.

Other solutions include smart contracts that can be combined with wallets to support payment applications, as well as Paymaster, a tool to reduce the friction in paying for gas fees to use specific blockchains, and CCTP, a tool to make transferring USDC between different blockchains safe and cost-efficient.

The prospects for Circle as a public company

Although Circle faces a potentially challenging macroeconomic environment in which to build a presence as a public company, when it does finally make its market debut, it will effectively do so as a proxy for stablecoins as an industry.

With reserve income forming almost all of its revenue, the company’s value will be entirely dependent on the continued adoption and growth of USDC. While there is clear headroom for further growth – our data shows non-wholesale cross-border payments alone will have a TAM of $65tn by 2032 – past events show that there is still risk of shocks to the stablecoin market, not to mention the potential impact of an economic downturn.

By building out its presence in emerging use cases for stablecoin and helping nascent Web3 markets to grow, Circle is laying the groundwork for significant future growth, while also continuing to build its presence in established financial markets where the technology’s use is growing but still small.

How big it will ultimately be, and how much of both established and emerging markets it can claim remains to be seen, but the company has demonstrated significant development since its first attempt at going public just a few years ago.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.