Citi reported its softest growth in cross-border payments transaction value in Q4 2024 since it began reporting the metric. But what is behind this development, and is it impacting revenue?

Citi has reported its Q4 and FY 2024 earnings, with a headline swing to profit that drove a stock price jump. However, the story for Citi’s cross-border payments specifically is more nuanced.

Sitting within the company’s Payments unit, which is part of Treasury and Trade Solutions under Citi’s Services division, cross-border payments is at one level a key priority for the bank. In its Q4 2024 earnings presentation, the company reaffirmed its vision to “be the preeminent banking partner for institutions with cross-border needs, a global leader in wealth management and a valued personal bank in our home market”.

However, the latest data on cross-border payments transaction value shows softer YoY growth for FY 2024 than in previous years, with particularly slow growth in Q4 2024. This is despite recent wins for the unit, including the Q3 2024 launch of a partnership with Mastercard Move to enable near-instant payments to its B2B2X player’s global debit card network.

In this report, we unpack the available data related to Citi’s cross-border payments offering, exploring potential drivers for the slowing transaction growth and the potential impact on revenue.

Citi’s slowing cross-border payments transaction value

Reported as a key metric for Treasury and Trade Solutions, Citi defines its cross-border transaction value, the one datapoint it consistently reports directly on cross-border payments, as “the total value of cross-border FX Payments processed through Citi’s proprietary Worldlink and Cross Border Funds Transfer platforms, including payments from Consumer, Corporate, Financial Institution and Public Sector clients”.

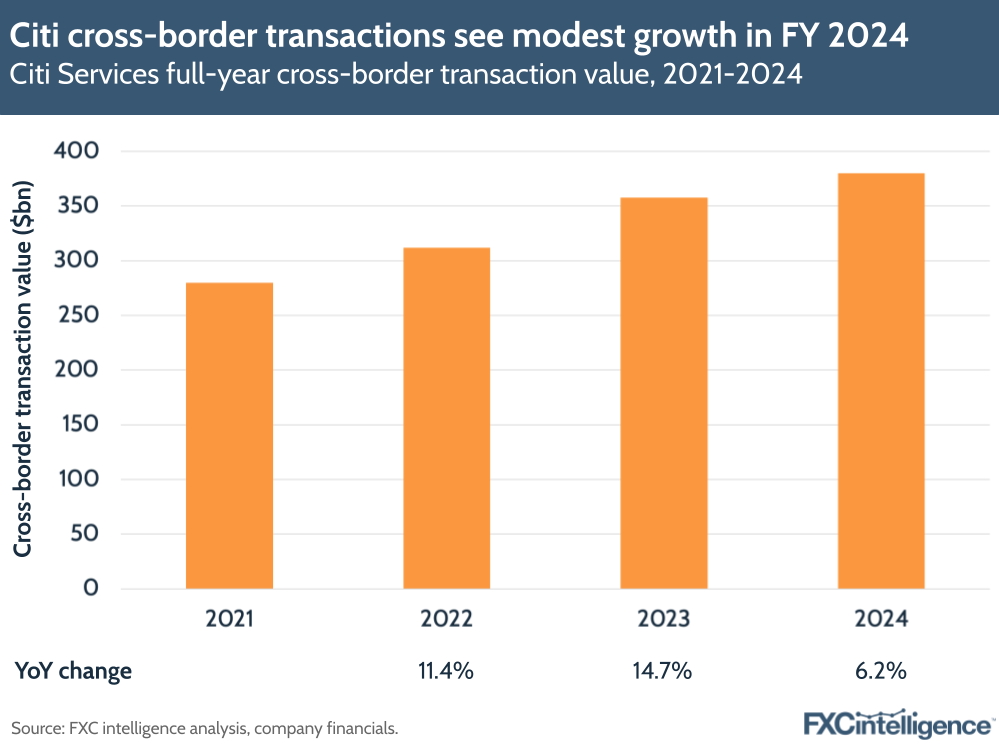

For FY 2024, it saw this reach $380bn, which represents a 6% increase on 2023’s $358bn. However, this is slower than the company saw over the past few years, with 2023 and 2022 seeing YoY increases of 15% and 11% respectively.

By contrast, the total non-wholesale cross-border payments market grew by 6% YoY in 2024, and 2% in 2023. This means that Citi has gone from growing significantly ahead of the market in 2023 to in line with it in 2024.

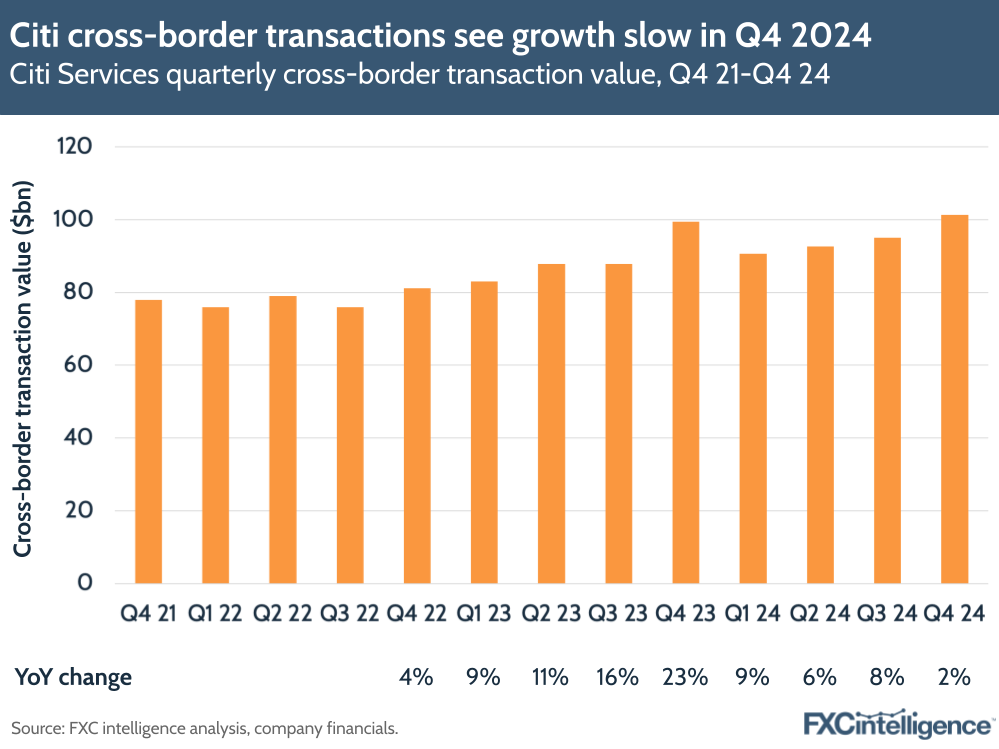

Looking quarterly, Q4 2024 saw cross-border transaction value reach $101.3bn – the first time this figure has passed $100bn in a quarter.

However, this represents just a 2% increase on Q4 2023, and marks a quarter of much slower growth than the rest of the year, with Q1, Q2 and Q3 2024 seeing YoY growth of 9%, 6% and 8% respectively. It is also significantly lower than the figures for 2023, with Q4 2023 cross-border transaction value having seen YoY growth of 23%.

Citi has not provided a direct explanation for this slowing growth in cross-border transaction value.

Performance against Investor Day targets

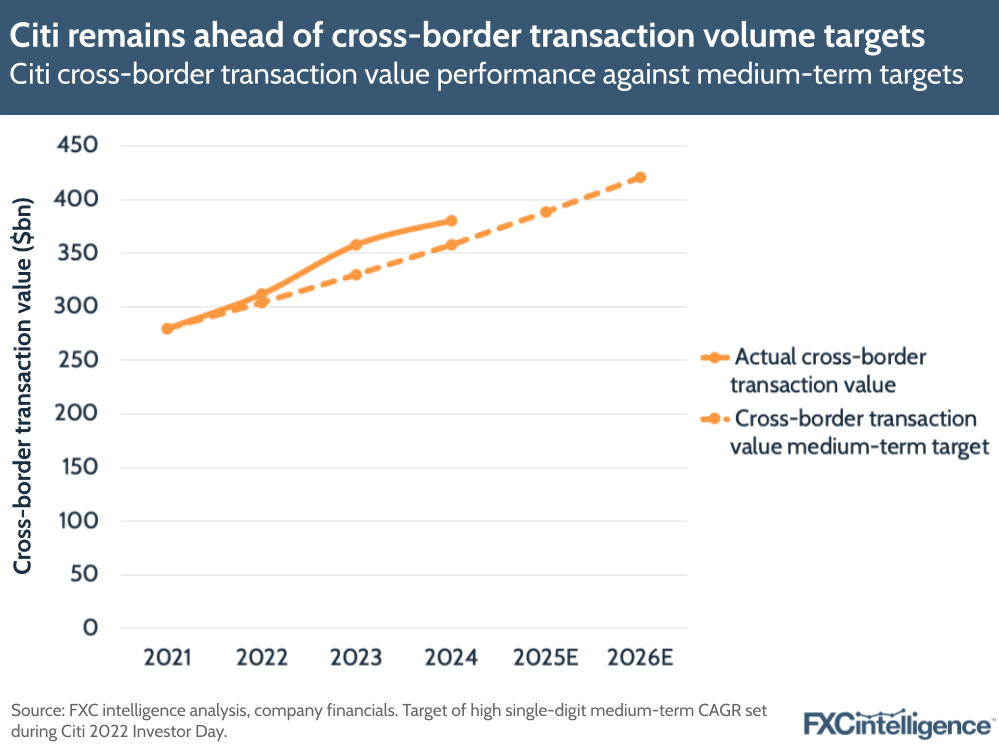

Despite this, Citi remains ahead of medium-term targets laid out at the company’s 2022 Investor Day, which it re-highlighted in its latest earnings. At that time the bank outlined a target of a high single-digit compound annual growth rate (CAGR) in the medium term, however it has performed above this in the years since. Between 2021 and 2023, Citi saw a CAGR of 13% for cross-border payments transaction value, while between 2021 and 2024 the CAGR was 11%.

This indicates that while 2024 saw slower growth in the volume of cross-border transactions than 2023, it remains above the bank’s expectations at a medium-term level.

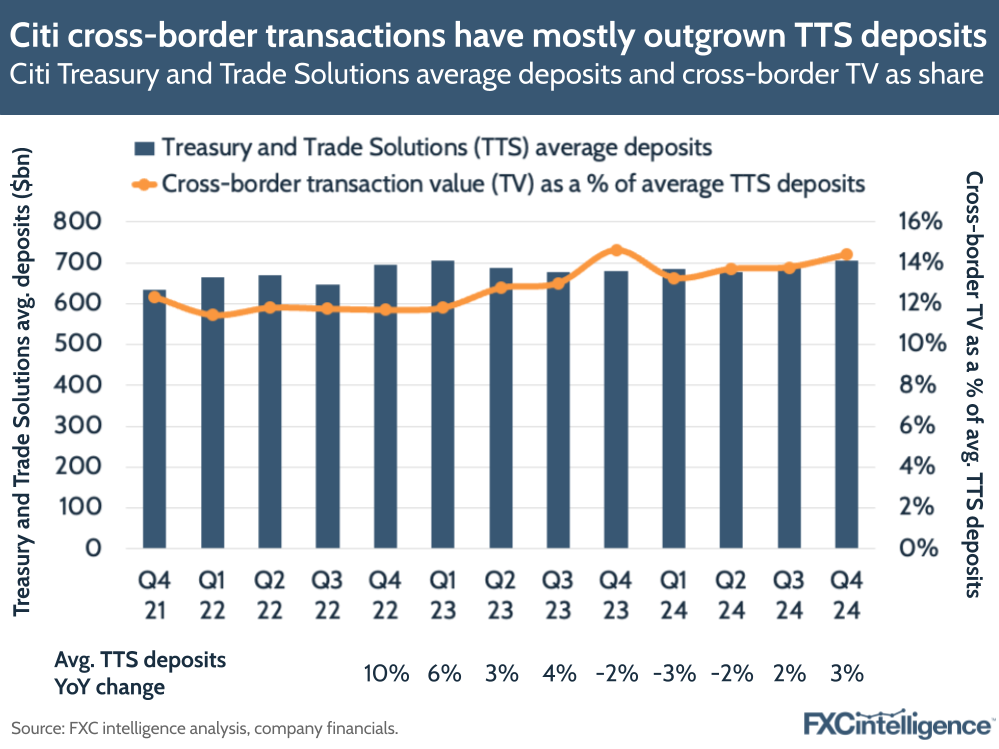

Is there a correlation with deposits?

While it does not publish consistent data on revenue associated with cross-border payments, Citi does publish average deposits across key divisions, including Treasury and Trade Solutions (TTS). Given that there is a potential correlation between the amounts held by clients in this division and the amounts they send as cross-border transactions, it is interesting to note that cross-border transaction value as a share of TTS average deposits has generally climbed over the past few years, although Q4 2024 is below the share in Q4 2023.

This indicates that cross-border transaction volume has in general seen stronger growth than TTS average deposits, particularly given that the latter has had several quarters with YoY decline. However, it is worth noting that in Q4 2024 TTS deposits saw stronger YoY growth, at 3% compared to cross-border transaction value’s 2%.

How is Citi’s cross-border revenue performing?

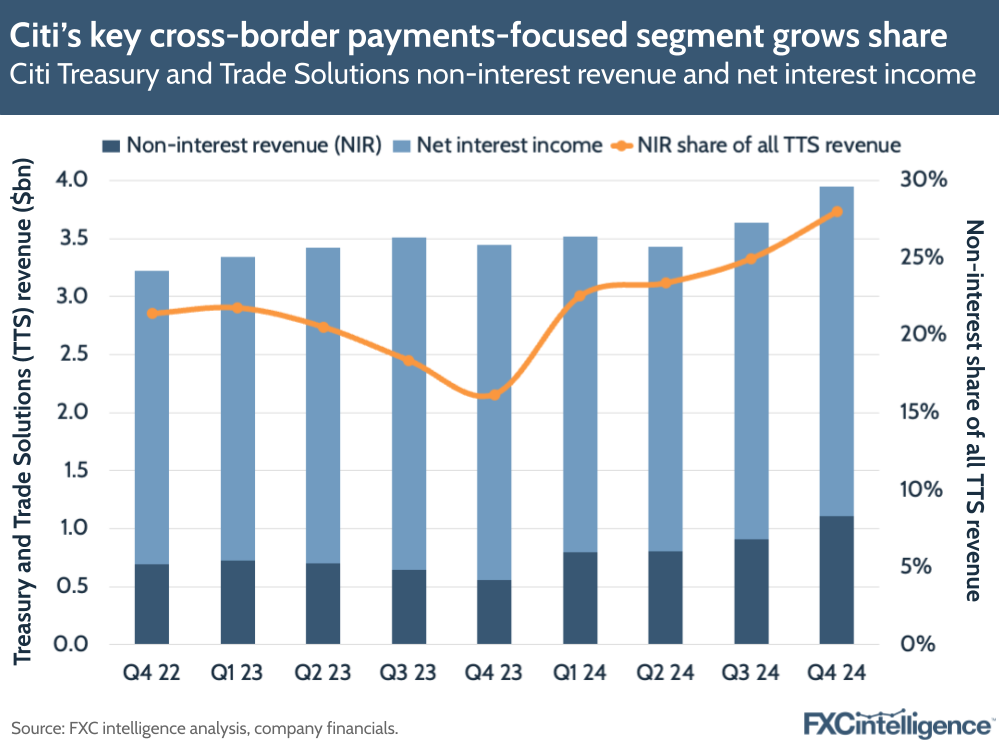

While Citi does not directly report revenue for either cross-border payments or its wider Payments division, it does report some metrics that provide a sense of this. Treasury and Trade Solutions, of which Payments is a part, saw revenue reach $3.9bn in Q4 2024, a 15% increase on Q4 2024.

TTS accounted for 76% of all Services revenue, and is reported as two sub-segments: net interest income (NII) and non-interest revenue (NIR). While NII reflects revenue earned from interest, such as that from customer balances, NIR includes revenue earned from fees and other income incurred from delivering cross-border transactions.

Although a far smaller segment than NII, NIR was the biggest driver of growth within TTS this quarter, seeing a 98% YoY increase to $1.1bn. This has also seen its share of TTS revenue climb significantly – to a high of 28%.

While changes in impact from Argentina’s currency devaluation were the primary driver of this significant growth, Citi also cited the 2% increase in cross-border transaction value, as well as a 10% increase in US dollar clearing volume, as key drivers, pointing to “continued strength in underlying fee drivers”.

The impact of Argentina’s currency devaluation

Argentina’s currency devaluation does, however, add significant distortion to Citi’s TTS NIR growth rates.

For the Services division overall, which covers both Treasury and Trade Solutions and Securities Services, non-interest revenues were reported as $1.7bn in Q4 2024, up 61% on Q4 2023’s $1.1bn. However, excluding losses as a result of the Argentina currency devaluation, Services NIR totalled $1.8bn in Q4 2024, up 8% on Q4 2023’s $1.7bn.

This difference is because while a year ago the currency devaluation presented significant losses for Services NIR, with an impact of $579m, in Q4 2024 this headwind was far less severe, at $51m.

Payments’ potential revenue

The relative strength of NIR growth, even excluding the impact of Argentina, suggests that payments are having a greater impact on TTS revenue than the growth in cross-border payments transaction value suggests.

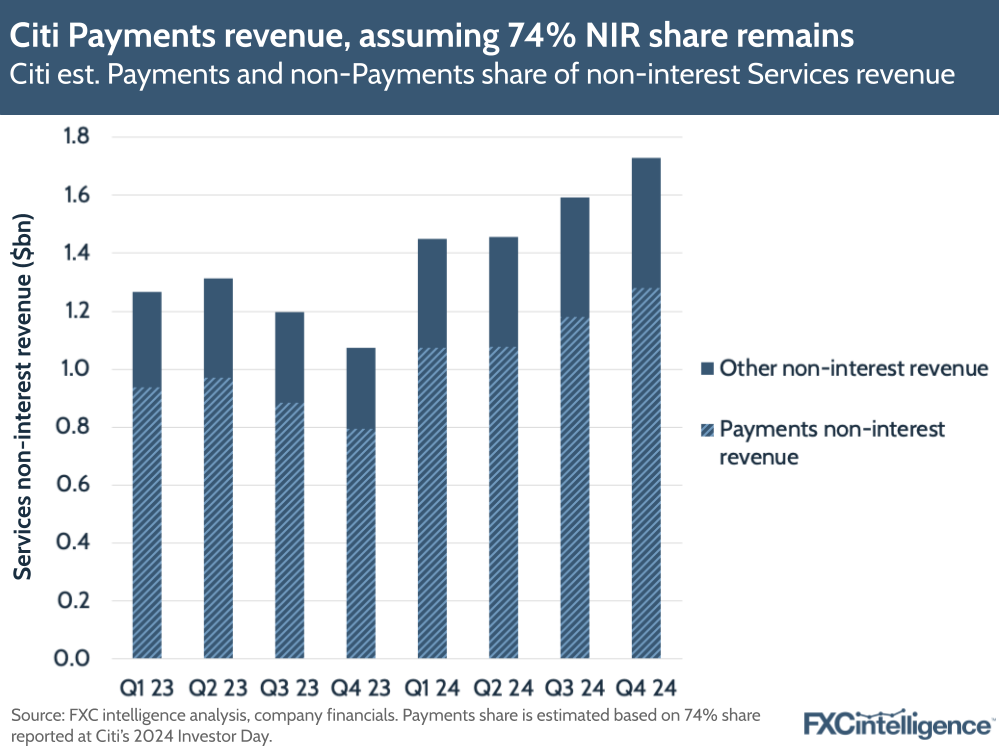

A year ago, Citi reported that cross-border payments revenue had grown 23% YoY, although did not report a number associated with this, and this year has not opted to re-state this datapoint. Similarly, at the start of 2024 the company held a Services-specific Investor Day that included a variety of more detailed metrics on Payments in particular.

Among these was the fact that Payments as a whole accounted for around 74% of Services non-interest revenue. This covers domestic payments & payment acceptance, commercial cards and clearing alongside cross-border payments, and while the latter is likely to be a key contributor, it is unlikely to be the majority.

However, if we assume that this share has remained consistent across 2024, this would put Payments revenue at around $1.3bn for Q4 2024 and around $4.6bn for FY 2024 – a 28% YoY increase on FY 2023.

Regional impacts and performance

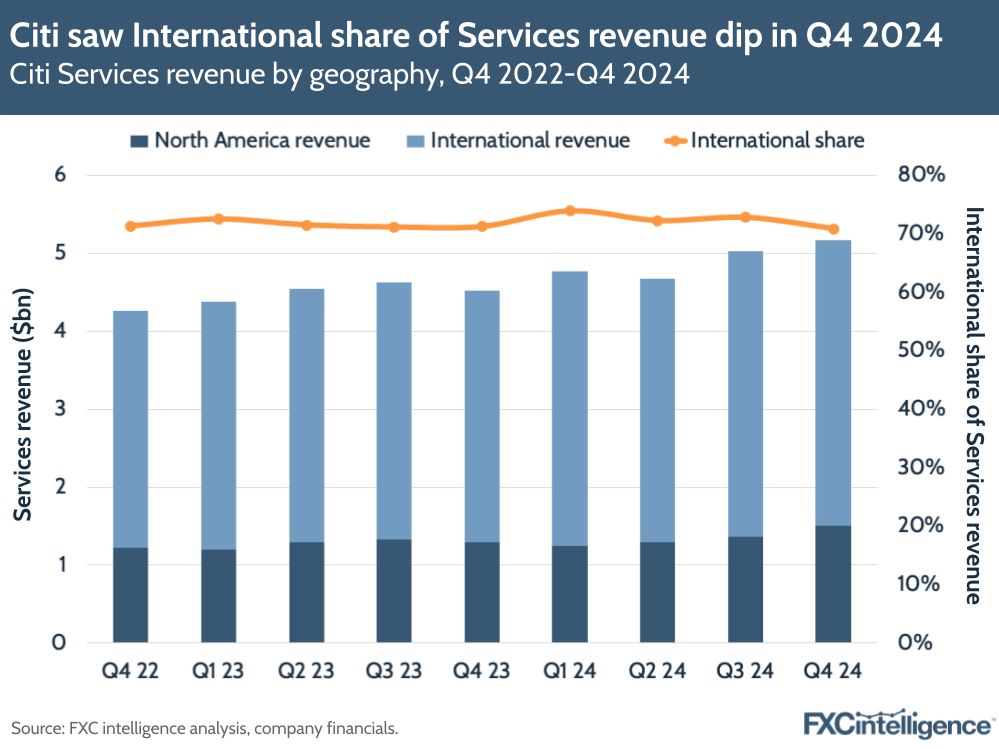

Looking regionally, Citi also reports Services revenue split between North America and International. Here, North America contributed 29% of revenue, at $1.5bn, while International accounted for 71%, at $3.7bn.

However, this represents a slight dip in International share compared to previous quarters, and International saw a 14% YoY increase, versus North America’s 16%.

This correlates with broad commentary provided by Citi CEO Jane Fraser during the company’s earnings call, when she described the US as “at the heart of the macro picture” for the bank as a whole, with growth aided by “a strong, innovative corporate sector”. By contrast, she also highlighted “slower than expected” growth for China, and underachievement in Europe, although did point to some emerging markets as “bright spots”.

This correlates with the outsized growth in US dollar clearing volume, which includes both domestic and cross-border payments, relative to cross-border transaction value.

Implications for 2025 and beyond

While it is not clear how cross-border payments performed in terms of revenue in the latest quarter, it may be that its revenue growth was greater than its growth in transaction value, particularly given that it continues to be cited as a key driver of TTS non-interest revenue.

If this is the case, it suggests that Citi is achieving a greater take rate for the cross-border volume it is processing than it has in the past, likely due to higher fees associated with its range of cross-border payments solutions.

For Citi, if it is to continue to build on its strength in cross-border payments, this is likely to remain a priority for 2025, as will bringing cross-border transaction value growth rates back into the mid-to-high single-digits, if not the double digits.

However, for all that Citi places cross-border payments at the heart of its focus, it may also wish to continue to prioritise this area in its future discussion of the company. Despite being central to the value statement shared in the earnings presentation, “cross-border” only saw a single mention in the Q4 earnings call itself and at no point did the company directly address either the slowing growth or its potential drivers.