Corpay’s FY and Q4 2024 earnings saw solid top-line results, with its Corporate Payments division providing strong growth that is set to continue into 2025. Corpay Cross-Border Solutions Group President Mark Frey shares his insights on the performance and what’s in store for the year ahead.

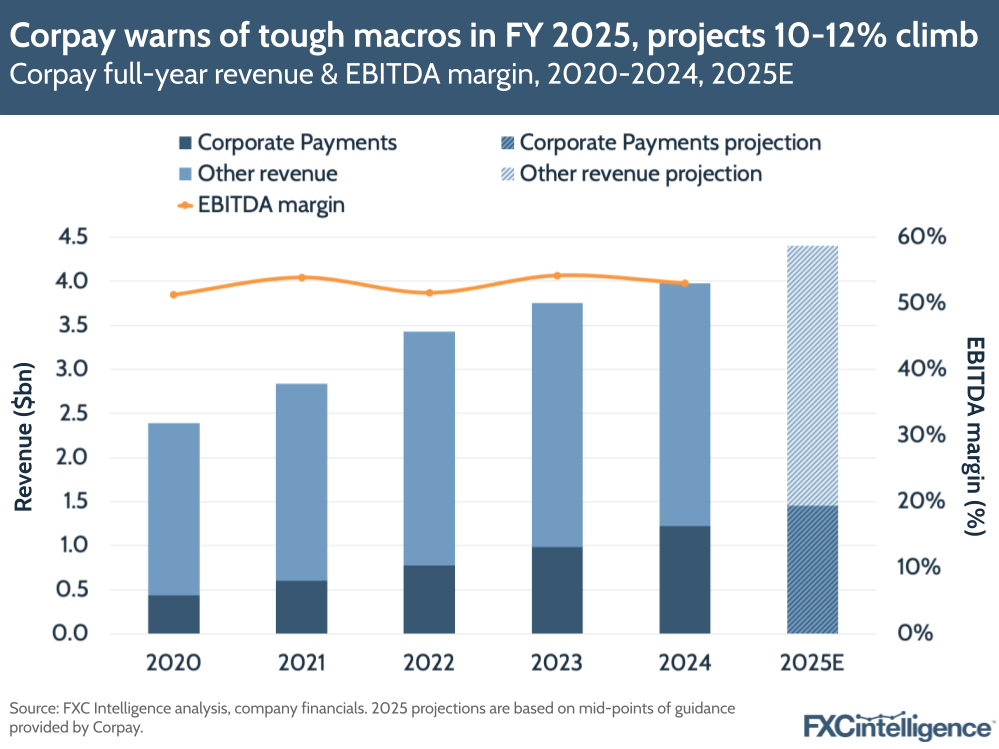

Corpay, formerly Fleetcor, reported a solid FY 2024, with full-year revenue increasing 6% to $4bn, aided by a Q4 2024 that improved on previous quarters, with 10% YoY revenue growth to $1bn.

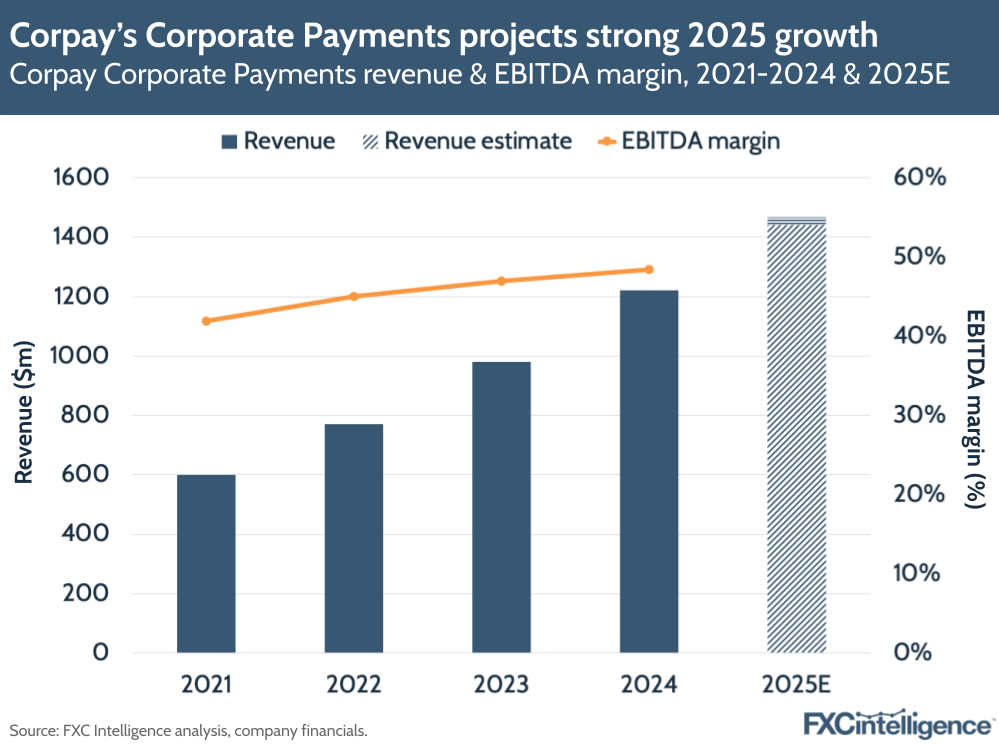

However, Corpay’s B2B payments-focused Corporate Payments segment has remained a consistent shining light for the company, with 38% revenue growth to $346m in Q4, while FY 2024 saw 26% YoY revenue growth to deliver the segment’s first billion-dollar-plus year, at $1.2bn.

While the company continues to face a challenging macroeconomic environment, it has laid out several core priorities for the year ahead, including a streamlining of the portfolio to deepen its focus on corporate payments while shedding extraneous assets. This is in addition to a deeper regional push, with greater investment in its US sales, while expanding its payables business into the UK and Europe.

It is also making a number of moves to better challenge banks for business, including broadening its payables business to the enterprise segment and expanding its multicurrency account product, the latter of which CEO Ronald Clarke described as a “game changer” for competing with banking players.

With this in mind, we spoke to Mark Frey, Group President of Corpay Cross-Border Solutions, to find out what the priorities will be for Corporate Payments over the next 12 months and beyond.

Corporate Payments’ leading role in Corpay’s Q4 and FY 2024 performance

Daniel Webber:

Let’s start with the big picture. Corpay had a solid year, but Corporate Payments was particularly strong and is very much at the heart of Corpay’s direction. Talk us through that.

Mark Frey:

It was a very strong quarter for Corporate Payments, for both the domestic payables business in the US as well as the cross-border business. Strong returns on the quarter, especially in cross-border, and a very good full-year result for both organisations.

It is also very clear, in terms of the strategy that we’ve laid out, that the business is shifting to more and more of a corporate payments focus, even within the other segments. The vehicle mobility payments business is increasingly becoming more corporate payments-oriented. You’re going to see an extension of that in Europe, and you will continue to see that in the Americas as well.

The overall strategy will continue to move more towards a corporate payments orientation, both organically in terms of the way that we build the individual lines of business, but also in the acquisitions and partnerships that we pursue as well.

Daniel Webber:

Let’s dig into the numbers: there was strong Q4 revenue across Corporate Payments, cross-border revenue growth and sales growth, growing faster than the market. What’s been underpinning that?

Mark Frey:

There are a few key things, when I look at our financial model, that really stand out. Number one: we acquire customers very capably, very well and very efficiently. We sell about 20%-plus of our base each and every year, so that allows us to continue to grow quite nicely.

We’ve got a relatively balanced business between our risk management solutions, our cross-border payment value proposition and now the treasury services and current account capabilities that we can offer to customers as well.

The other key part that we do well compared to the market is we retain customers and revenue quite capably as well, so we don’t really have a material level of client attrition within our business. We keep virtually 99-99.5% of our business from one calendar year to the next, which means when we sell net new at 20%-plus, we’re able to effectively grow at 20% plus. In that construct, it’s a very simple financial model that we’ve been able to fine-tune over the years, and is relatively consistent in terms of how it goes forward.

Daniel Webber:

Those retention numbers are higher than your corporate peers. What is keeping them sticky?

Mark Frey:

It is the technology in many respects that keeps them sticky – that’s the feedback that we hear from our customers. They certainly appreciate the dedicated white glove service that we offer to corporate customers as well.

Inevitably, there will be some customers that will leave us. There will be some customers that will go to the competition, some that will shut down, go out of business, that have to reorganise or that are acquired, but we grow a lot of relationships from one year to the next, where we get more wallet share or we grow alongside those customers as their businesses grow and expand as well.

We see enough lift from our expanding wallet share and our expanding customers to make up for that sort of structural loss, year in, year out, so that it comes in at around 99-100% in terms of overall revenue retention.

Corporate Payments projects strong growth despite macro headwinds in FY 2025 projections

In addition to its solid revenue growth, Corpay saw its Q4 and 2024 EBITDA margin remain at 53%. However, the company pointed to unfavourable macroeconomic conditions that served both as headwinds for the most recent quarter and for its projections for FY 2025.

It in particular cited delayed gift card shipments and challenging FX conditions as headwinds in Q4 2024, although said that these had been partially offset by both a favourable tax rate and unplanned additional revenue from its acquisition of GPS, which closed in December.

However, these challenges are set to become more pronounced in 2025, with CEO Ronald Clarke warning of a “much higher” tax rate, along with “weak international currencies”. As a result, the company is currently targeting FY 2025 revenue of between $4.4bn and $4.5bn, representing an increase of about 10-12%. It also projects sales growth of 20%, however, and is likely to revise its guidance if the macroeconomic environment changes.

By contrast, Corporate Payments’ stronger growth was accompanied by an EBITDA margin of 48% for FY 2024 and 47% for Q4 2024.

Corporate Payments’ outsized performance is expected to continue through 2025, with Corpay projecting the segment to see growth in the high teens to 20%.

Prioritising corporate payments across Corpay

Daniel Webber:

The focus at Corpay is increasingly on simplifying the portfolio to ultimately become more focused on corporate payments. What’s the sweet spot there in terms of fit for Corpay and Corporate Payments?

Mark Frey:

From a Corporate Payments perspective, the way that we think of it is anytime a corporate organisation is required to move money that is not related to payroll specifically.

Whether that be vendor accounts payable (AP), whether that be payments that exist in their ecosystem; if they’re payments-oriented organisations, it is that full suite of payment requirements that we look at from our Corporate Payments organisation – aside from their payroll or their specific HR spend.

Our focus is even within our existing segments outside of Corporate Payments specifically. In vehicle mobility payments we increasingly want to deploy these resources and capabilities against those customer sets as well. So those businesses will become slightly more payment-centric as well and move more towards that corporate payments landscape.

Corporate Payments takes growing share of Corpay business

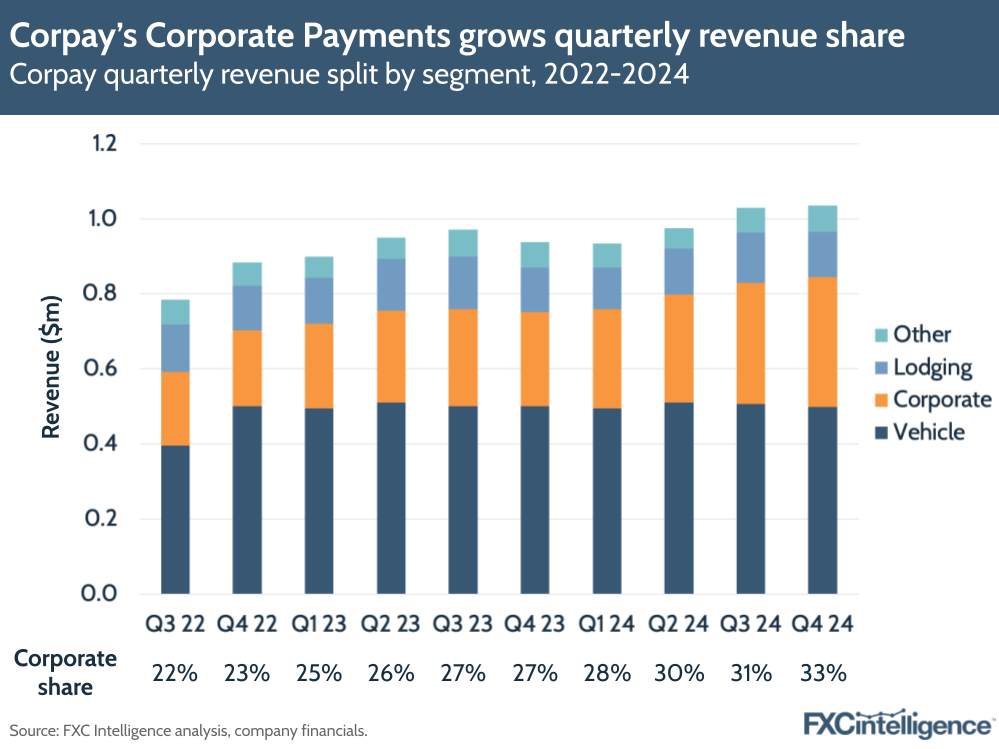

The latest earnings also saw Corporate Payments take its highest share of Corpay’s revenue to date, with the segment accounting for 31% of all revenue in FY 2024 and 33% in Q4 2024.

This is also reflected in the respective revenue growth rates of the different segments. While Corporate Payments grew by 38% in Q4, the next highest growth was in the smallest segment, Other, at 5%. Meanwhile, Lodging Payments grew by less than 1% and Vehicle Payments contracted by half a percent in Q4 versus the same period in previous year.

The strength of Corporate Payments is also reflected in the increasingly central focus Corpay has placed on the segment, including its decision to adopt its name for the full business.

It has also seen it look to increasingly cross-sell between divisions. This has already shown success for its planned enterprise business, with the first enterprise client, which Corpay has now won the full accounts-payable business of, having initially been a Vehicle Payments customer.

The bank-challenging potential of Corpay’s multicurrency accounts

Daniel Webber:

Let’s continue the story on the multicurrency card, which we’ve discussed previously and I know you are excited about. The language in the earnings is that it’s a game changer in competing with the banks. Talk us through how that’s evolving and how it positions versus bank multicurrency products.

Mark Frey:

It has been a very exciting product category for us within cross-border. We’ve seen very good interest in the product, both from the institutional market segments where you have asset managers, funds administrators and firms in that space and global investors that are keen to deploy that solution to stand up virtual bank accounts to support their enterprise, but we see significant interest from our corporate customers as well.

The simple way to think of it is a US-based corporate customer operating predominantly in the US but that has operations, sales and expenses and other jurisdictions around the world. Rather than maintaining bank accounts with Barclays and with Deutsche in the UK and Europe respectively, or National Australia Bank in Australia, and having these disparate relationships where there are subscale economic relationships for these banking partners in far-flung jurisdictions, we can offer a one-stop-shop solution.

Local market access with a virtual account, deployed in-country in many jurisdictions, that’s connected to local payment schemes and rails and still provides them all the day-to-day flexibility to do their day-to-day banking, all supported by a tier-one money center bank partner, whether it be Barclays, J.P. Morgan or various other partners that are enabling this capability for us.

It has truly become differentiating in terms of our ability to service our customers on a global basis, as opposed to the domestic market where their treasury and CFO might historically be housed. We see an opportunity for us to become more involved with our customers, to become more a part of their finance organisation, which we think will lead to stickier customer relationships and more value delivered to those customers over time.

Daniel Webber:

When you call it subscale for banks, there’s typically no credit relationship there and there’s just the payments relationship, right? Which is very valuable to you, but trickier for banks.

Mark Frey:

Very much so, you’re exactly right. If we look at that same example of a US-based corporate, and they have accounts and all these other jurisdictions around the world, typically there is no lending relationship between the US corporate and those various banks around the world.

It’s really just a transactional money movement capability that they’re looking to transact with, and therefore there aren’t great economics for those non-US-based banks to support that corporate entity. Whereas for us, this is core to who we are and the movement of money and managing FX risk exposure is central to our value proposition. So it makes those customers a little closer to us, because we can help manage the cash flows associated with those foreign bank accounts.

There’s one platform that connects to these transactional accounts all around the world. You have full visibility of your balances, inflows and outflow of funds on one platform in this multi-jurisdictional sort of scenario. It’s a much easier way to manage the business for a treasurer or a CFO with much greater visibility, and allows these organisations to manage their cash flow a great deal more efficiently as well.

We’re able to offer this product in virtually all the jurisdictions in which we are onboarding customers today. We’ve launched with 12 initial currencies. That list will quickly expand to a few dozen more over the next couple of quarters.

We see that probably 80-90% of our overall payment flow and transaction flow across our organisation will be applicable to these various accounts.

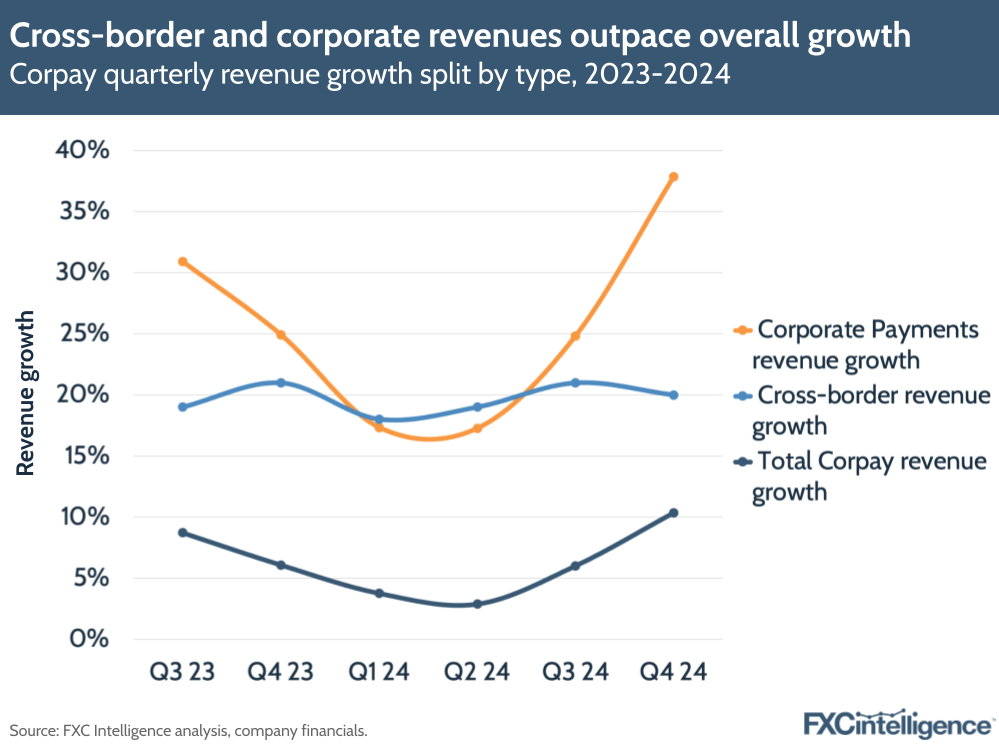

Cross-border continues to outpace overall growth

While Corpay does not break out numbers for its cross-border payments revenue, it does report growth rates, which outperformed the company overall.

Corpay reported that its cross-border payments revenue had risen by 20% YoY in both Q4 and FY 2024, which it said was aided by a 43% increase in sales for Q4 and a 33% increase for FY.

Payables and Corpay’s cross-border payments business

Daniel Webber:

There’s been a lot of talk about payables in your discussion of 2025 strategy. How do those payables parts link into the cross-border parts of the business?

Mark Frey:

We think of the US domestic payables business and the cross-border payments business as related, but two different lines of business.

The US domestic payables business is largely a plastic T&E and purchasing card and virtual card solution, domestically within the US and Canada. So domestic within the North American market, if you will, versus the cross-border payments business, which is very FX-centric and cross-border payments-centric.

There’s an awful lot of collaboration between these two organisations. We share customers that we process virtual card payments for within the domestic business unit, and then we also handle FX or cross-border payments in the cross-border business unit.

There’s historically been a lot of collaboration between the two organisations where invoice pay and Accrualify – before they were acquired by the payables’ division – were partners of cross-border.

We continue to see that trend with the latest acquisitions from Paymerang, and we expect that will continue to be a focus as we go forward.

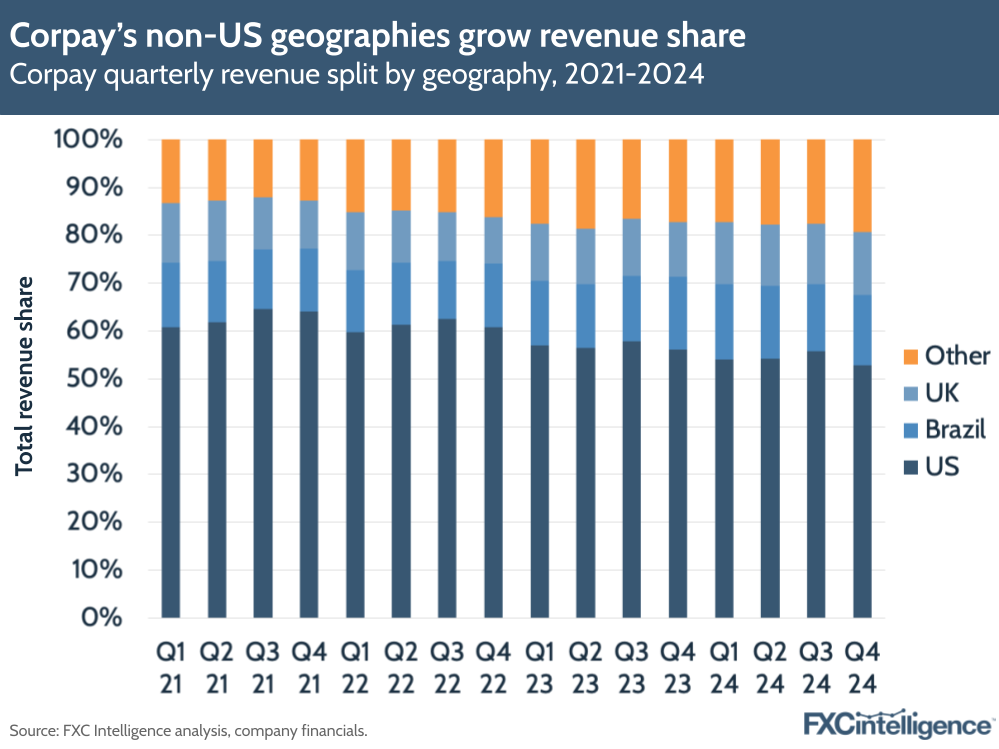

Non-US geographies drive Corpay’s 2024 growth

Non-US revenue continues to take a growing share for Corpay, accounting for 47% in Q4 2024, compared to 43% in Q4 2023 and 39% in Q4 2022. This has been aided in particular by strong growth in the UK, which grew 27% in the latest quarter, and Other, which covers all non-US markets excluding the UK and Brazil, which grew by 24%. By contrast, Brazil grew 6% and the US by 4%.

While the company does plan to expand its payables offerings in the UK and Europe, it has also highlighted the US as an area where it needs to improve its growth, with Clarke promising a “step-change improvement in USA sales production” via investments in both in-person and remote sales.

M&A pipeline and strategic acquisition priorities

Daniel Webber:

You’re also planning to continue to add more M&As, and we know you’re very good at this: from day one it’s fully integrated and it’s onto the next part. What’s your focus for the next M&A piece?

Mark Frey:

It is a clear part of our strategy. We say, corporately, that we would choose to deploy our free cash flow with respect to accretive acquisitions, first and foremost, and we would look at buybacks as a secondary source or a secondary use of capital.

So this is very much part of the strategy: we have a very well-defined inorganic growth strategy based on acquisition. We’ve said, very clearly, that we want to continue to focus on the corporate payment space, and yes, I absolutely think we’ll continue to be active, in part because it’s been a very successful part of our overall journey.

While we grow organically 20% year-on-year, we could not have scaled the business as quickly as we have without those acquisitions. We’ve also been able to fine-tune the process for us to be able to go a little bit faster, for us to be able to grow the target companies post-acquisition faster than what we did originally.

We are continuing to improve our overall processes and somewhat doubling down on this as part of our go-forward strategy.

Corpay continues to prioritise acquisitions

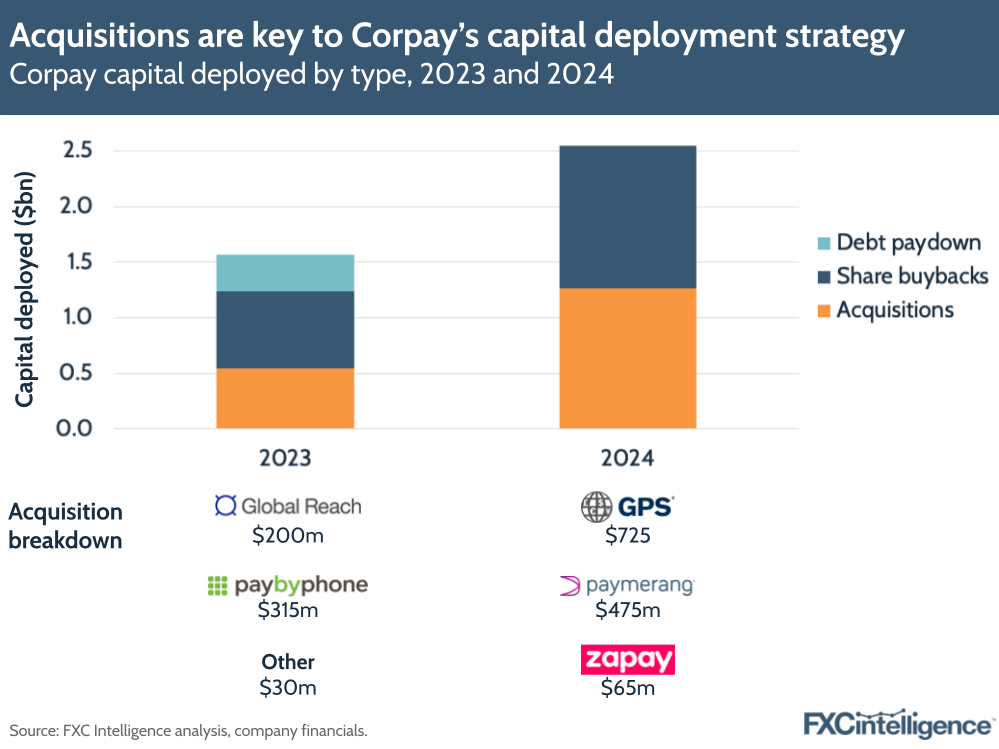

In 2024, Corpay deployed $2.6bn in capital, which it split 50:50 to repurchase 4.2 million shares, as well as acquiring three companies, GPS, Paymerang and Zapay, for a combined $1.3bn. This represents a significant jump on 2023, when the company deployed a total of $1.6bn across debt paydowns, share buybacks and acquisitions, including acquiring Global Reach.

In 2025 Corpay plans to “go deeper versus wider”, according to Clarke, in a move that will see it look to sell 2-3 “non-core assets” that don’t fit with its central corporate payments focus, as well as adding more corporate payment assets through continued M&As. The company has already announced its first M&A of the year, Brazilian vehicle payment provider Gringo, in a deal designed to bolster its car debts offering.

In addition, the company also plans to continue share repurchases, with nearly $1.3bn authorised for this activity.

The path to $5bn Corporate Payments revenue

Daniel Webber:

Corporate Payments crossed $1bn of revenue in 2024. How do you think about the path to $5bn or $10bn of revenue?

Mark Frey:

To a certain extent, we take it $1bn at a time. In terms of talking about billions, we do see that we want to continue to grow organically in the high teens to 20% in the cross-border business, year-on-year, so as we approach a billion-dollar revenue company, that begins to compound quite aggressively over time.

We do think that there are a number of highly attractive organisations that would fit within the mold of what we’re looking to achieve not only in terms of acquisitions of portfolio of customers, but capabilities that we can bolt on and integrate to our core value proposition.

We do think that there are a number of attractive opportunities, and we think that there’s no reason why we can’t continue to scale the business at a similar pace to what we have over the last number of years. We will continue to execute the strategy, because we’re encouraged by the results, quite frankly.

We’re not seeing diminishing returns from the sales effort. The sales effort continues to keep pace with the top line and bottom-line growth of the business. We continue to eke out a little bit of operational leverage in the business, even as we’re getting close to 60% operational EBITDA margins within cross-border. We will continue to try and eke out that operational leverage.

Of course, it does get more challenging, as trying to maintain growth in and around 20% from a top-line perspective and trying to add between three to five points of operational leverage to the bottom line each year. That does get more challenging as the margins continue to improve, and we do believe that that will plateau at some stage, because we also are investing in technology for the future and trying to build a platform that will continue to scale.

Daniel Webber:

Mark, thank you.

Mark Frey:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.