Over the years, the European Central Bank has rolled out several initiatives within the Single Euro Payments Area to promote digital payments. But how far has the region moved towards a cashless transition, and what are the main drivers in this shift?

The Eurozone is an important area for outbound cross-border payments, with major senders such as Germany, Spain, Italy and France providing a significant contribution to global remittance outflows. In addition, with the advantage of a single currency, the Eurozone has taken significant steps towards harmonisation of payments.

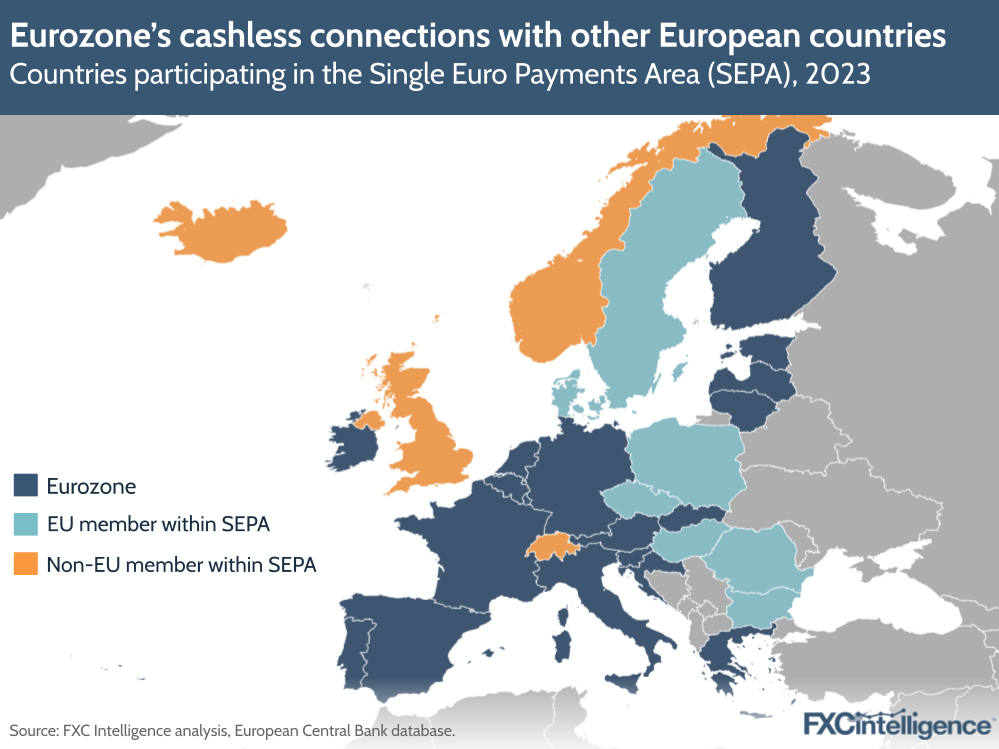

The Single Euro Payments Area (SEPA) was launched in 2008, enabling customers to make cashless euro payments anywhere within the European Union (EU) and select non-EU countries. By standardising processes across all participating territories, the initial goal was to remove administrative differences between national and cross-border payments, forming a unified approach to payments systems.

In collaboration with European banking institutions, the European Payments Council and other public authorities, SEPA has since developed into four schemes: SEPA Credit Transfer (SCT), SEPA Direct Debit Core (SDD), SEPA Direct Debit B2B (SDD B2B) and Instant Credit Transfer (SCT Inst).

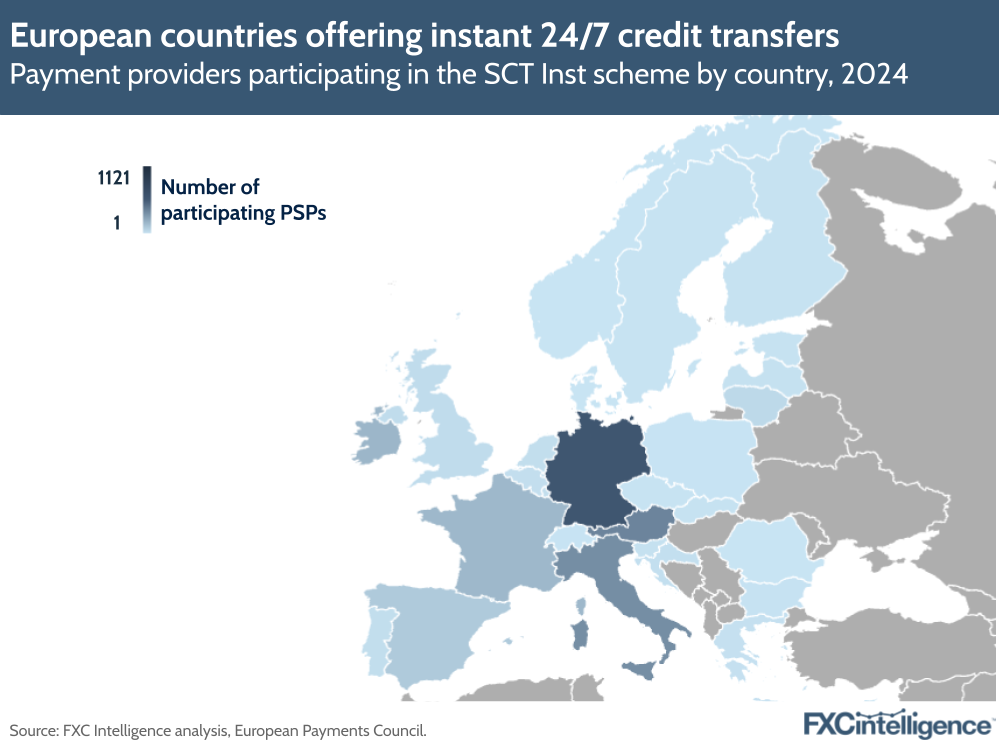

The SCT and SDD, both Core and B2B, schemes are mandatory for payment service providers (PSPs) offering euro credit transfer and direct debit services, while the optional SCT Inst scheme supports instant account-to-account payments. As of 2024, SCT Inst is gaining participation from PSPs across the Eurozone, such as in Austria, Germany and, more recently, Spain.

In parallel, the European Central Bank also published a second progress report on the digital euro project in December, announcing the preparation stage, which invited selected bidders to tender, with an expected outcome in 2025. This project would serve as a foundation for a potential Central Bank Digital Currency (CBDC) within the eurozone.

These payment schemes generally signal a regulatory push for a cashless transition in the Eurozone, or at least an increase in support for cash alternatives. However, the progress of this shift depends on stakeholders beyond the legislative authorities and the key question remains whether consumers and service providers will adapt to the ongoing developments in the Eurozone’s payments landscape.

With this in mind, we explore how far the Eurozone has moved toward cashless payments, analysing key drivers of the transition, including the Covid-19 pandemic, pricing incentives and digital infrastructure.

Cash circulation in the Eurozone: key trends

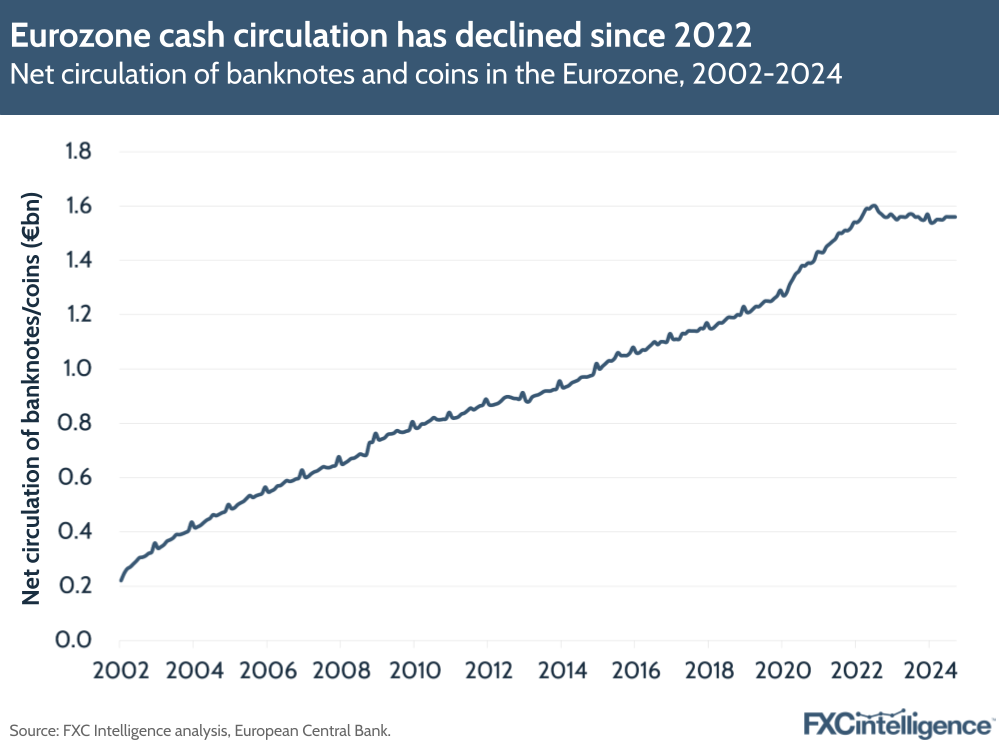

After the euro’s implementation in 1999, the European Central Bank tracked the total number of banknotes and coins circulating in the Eurozone, counted by national central banks under “net cash circulation”.

Looking at the data, the amount of physical cash in the Eurozone grew annually by double digits between 2002 and 2006. This growth continued until 2021, though at a slower rate with mostly single-digit YoY increases. This was followed by increasing slowdown in 2022 and 2023 before a negative annual rate of -1.28% YoY was recorded in January 2024, indicating that fewer banknotes and coins are circulating in the Eurozone compared to the same period in 2023.

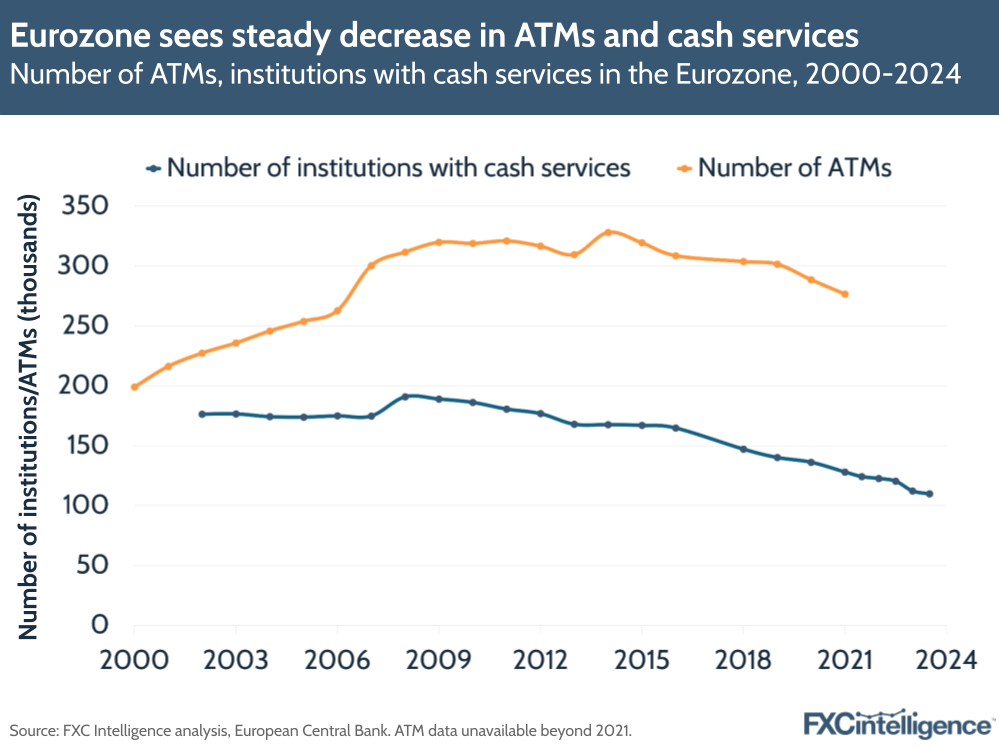

Similarly, the number of credit institutions (including their branches) providing cash services in the Eurozone has declined since 2022, with a YoY decrease of -3% in H1 2023 and -9% in H2 2023. In the first half of 2024, there were only 109,888 institutions providing cash services, a -35% decrease from the first half of 2014.

The number of ATMs in the Eurozone also shows a declining trend, peaking at 328,056 in 2014 and decreasing steadily since then.

While all three metrics reflect a significant decline in cash availability, this shift could be influenced by many factors beyond reduced demand for cash, such as changes in Eurozone membership and macroeconomic conditions; it remains important, therefore, to examine the cashless transition from the consumer’s perspective.

Exploring cashless payments in the Eurozone

The European Central Bank also collects data on e-money from Monetary Financial Institutions (MFIs) – which includes central banks, credit institutions, money market funds (MMFs) and e-money institutions – and their balance sheet statistics, defining it as “an electronic store of monetary value on a technical device”.

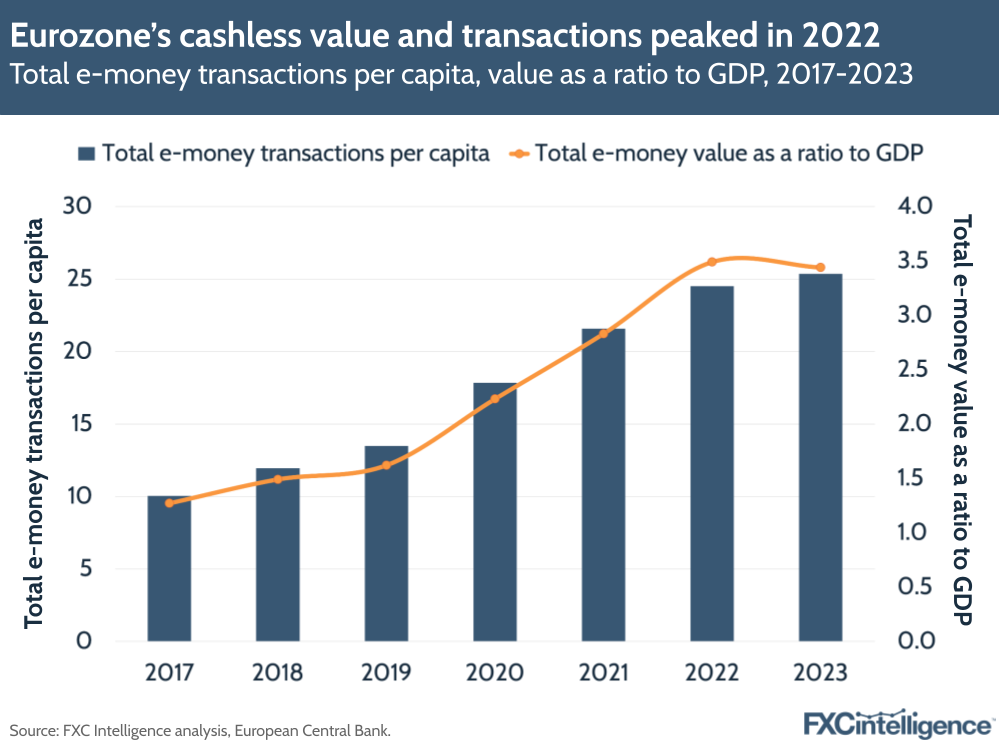

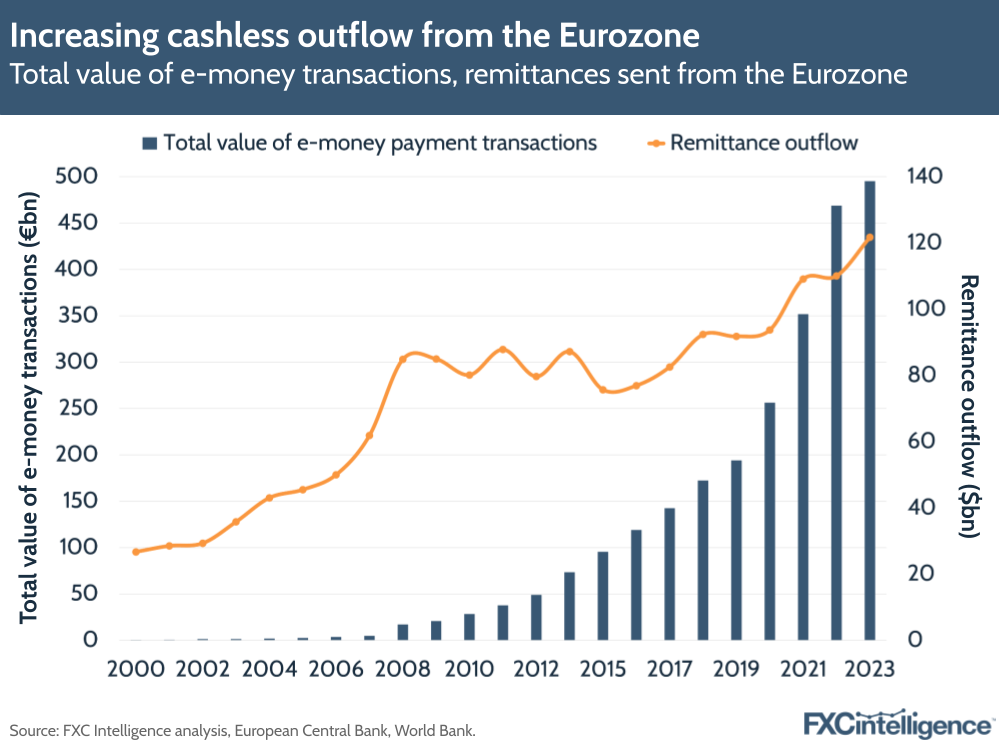

The e-money data shows that both the number and value of cashless transactions in the Eurozone grew significantly between 2019 and 2022. When measured relative to the population, e-money transactions increased annually by double digits until 2022, with the highest growth rate of 32.25% in 2020. The transaction growth rate, as measured per capita, then dropped and only increased by 3.47% YoY in 2023.

The value of e-money transactions, when measured as a ratio to GDP, also saw a similar trend, peaking in 2022 before falling in 2023. As a ratio to the Eurozone’s GDP, the e-money value reached the highest growth rate in 2020, with 37.7% YoY increase. This was followed by a continued decline in annual growth rate, which turned negative in 2023, representing a decrease in the total value of e-money transactions within the Eurozone.

The Eurozone’s data on e-money outbound highlights a similar trend. The value of e-money transactions sent from the Eurozone saw YoY growth of 32-37% between 2020 and 2022, before slowing to 5.63% in 2023.

Overall, the data signals a forward shift in cashless transitions, particularly in 2022. Across all metrics, there was a significant increase in e-money usage between 2019 and 2022, followed by a slowdown in 2023. This pattern could reflect the demand for digital payments during the Covid-19 pandemic.

The World Bank reported that about 10% of adults in Europe and Central Asia who used an account to make or receive a digital payment made digital merchant payments for the first time during the Covid-19 pandemic. The World Bank further reports that, between 2017 and 2020, the annual number of cashless transactions per person globally increased from 91 to 135, emphasising the acceleration of cashless transition.

However, the European Central Bank’s data shows that e-money usage stopped growing after 2022. The e-money value and transaction metrics indicate a flat or declining trend in the post-pandemic period, raising the question of how much the cashless transition’s acceleration was a temporary shift, buoyed by the pandemic environment.

Pricing incentive: cashless money transfers

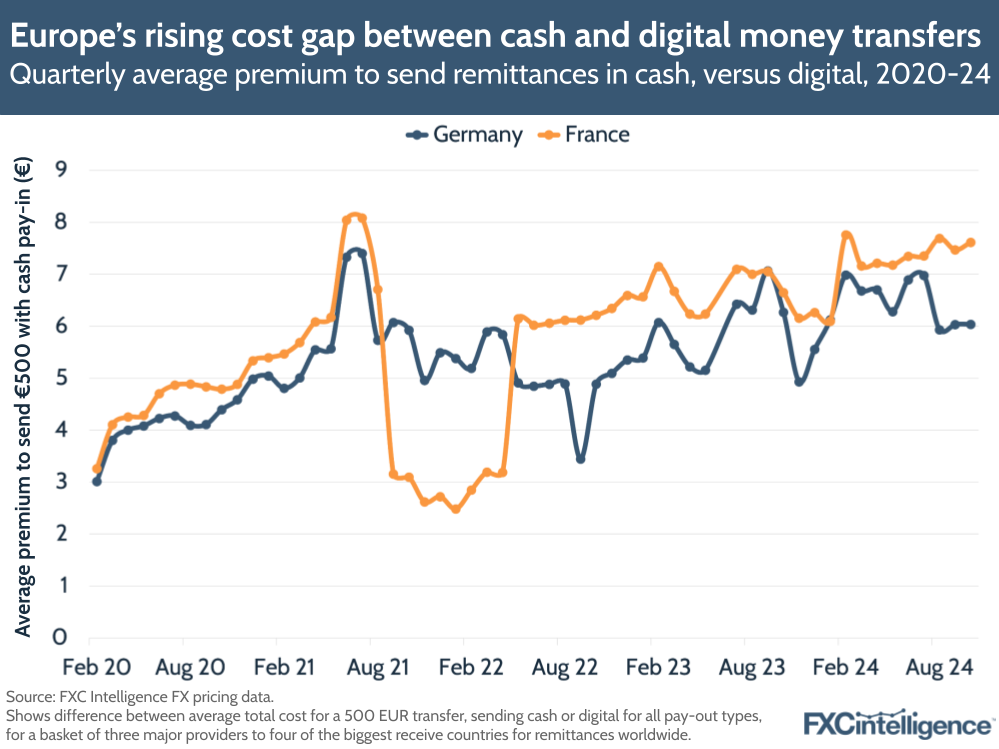

In the money transfers space, digital transactions have been increasingly dominating the market and this is reflected in FXC Intelligence data. When looking at the average cross-border pricing across three major money transfer providers to four major remittance markets worldwide, the data highlights an increasing difference between the total costs to send money transfers initiated in cash, and those sent as digital transactions (which includes bank account, credit/debit card and mobile wallet).

This rising difference mainly comes from higher cash fee rates, particularly in France and Germany. In France, the cash rate in October 2024 is 70.2% higher than in February 2020, while in Germany, the rate has risen by 44.7% over the same period. With flat growth in digital rates, the gap between cash and digital fees increased by more than 50% in both countries from 2020 to 2024.

The increase in fees for cash pay-ins is likely to be a reflection of the cashless transition driving demand for digital money transfers. This is likely to have reduced the volume of remittances sent in cash in the region, driving up the cost to deliver each cash-based transfer.

This is also reflected in the efforts major remittances companies have made to expand their investments in digitalisation. In 2022 for example, Western Union announced its Evolve 2025 strategy, a business plan focused on transitioning towards digital money transfers. At the same time, digital-only money transfer companies such as Wise, Remitly and Revolut have seen significant growth in recent years.

How are remittance players varying pricing by pay-in and pay-out type?

Digital infrastructure in the Eurozone

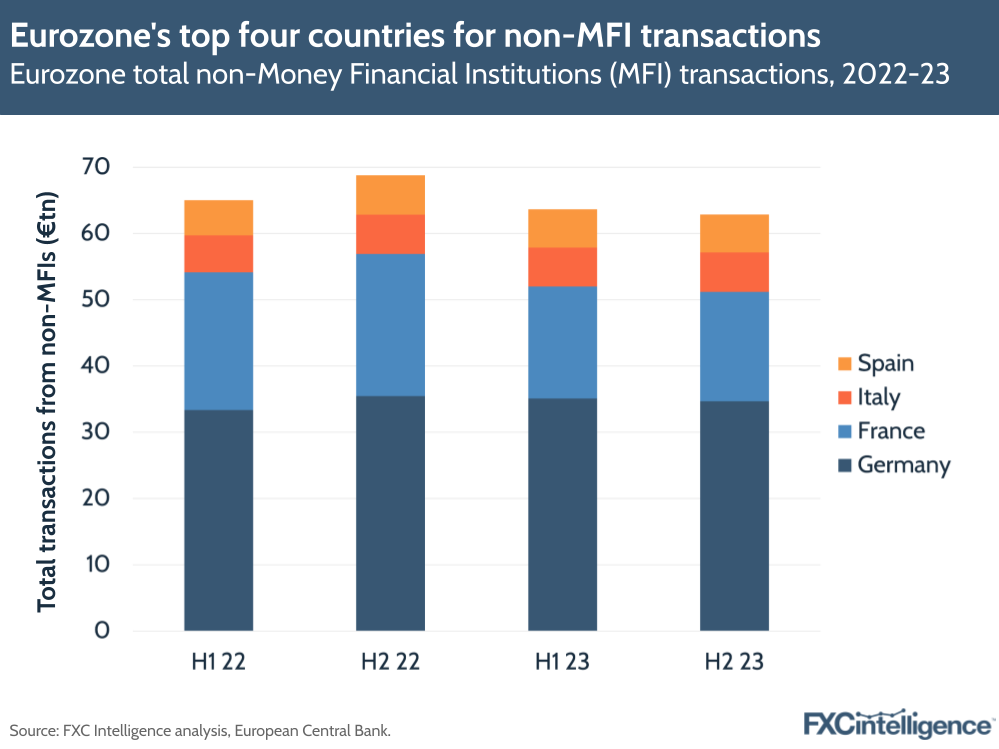

Looking geographically, the European Central Bank reported the top four non-MFI senders to countries outside the Eurozone as Germany, France, Italy and Spain. Among these countries, Germany dominated the space in H2 2023 (the most recently available data), accounting for 31% (€34.7tn) of total transaction values in the Eurozone.

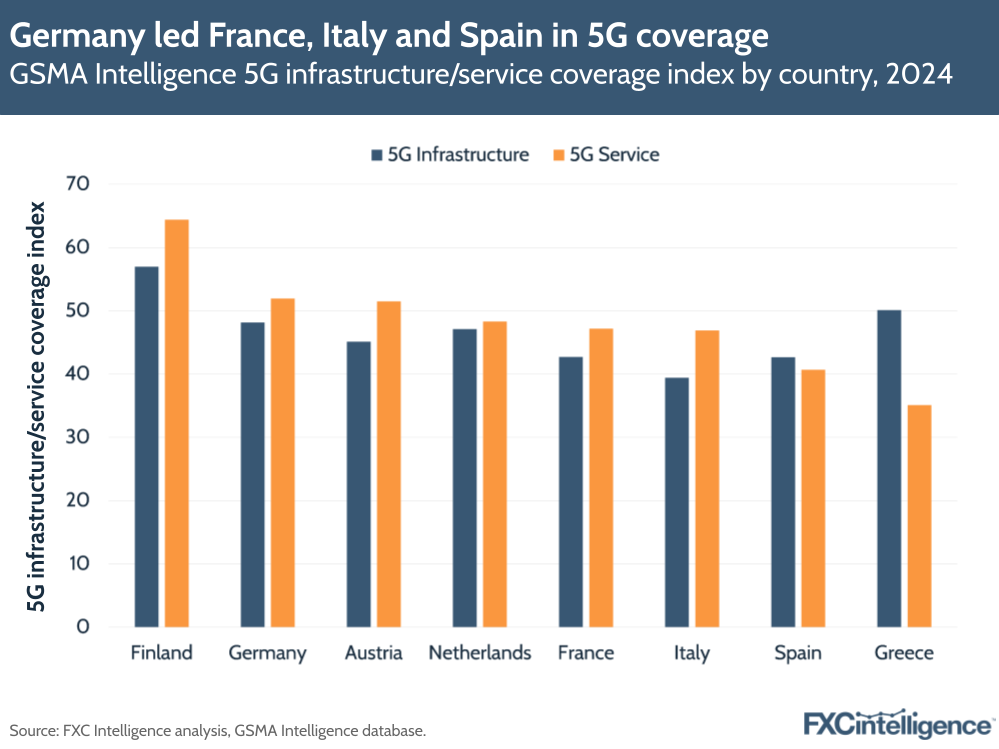

Germany also led France, Italy and Spain in the 5G infrastructure and service index, according to GSMA Intelligence’s report in Q2 2024. Germany scored above average in 5G adoption, coverage and device affordability metrics, which is also reflected in its 5G population coverage of 96.8%. Among the four countries, France came in second for the 5G service index but beat Germany on 5G data affordability, with 76.5%. For Italy and Spain, both countries scored higher than 70% for the affordability of high-speed service.

While there is no direct relationship between the cashless transition and 5G coverage, greater high-speed data availability is likely to encourage consumers to make use of digital options. Notably, the top four non-MFI senders also play a significant role in the digital payments space.

Germany is seeing expanding use of Apple’s Tap-to-Pay system, which enables merchants to accept contactless payments without the need to purchase additional hardware, following a July agreement between the EU and Apple that saw the payment system opened up to access by Apple’s rivals. In June, Viva.com launched a Tap-to-Pay service in Germany and the UK-based payments company MyPOS followed suit by launching Tap-to-Pay products for German merchants. The mobile payments company Mollie also added the Tap-to-Pay function for customers across Italy, France and Germany in early November.

France, meanwhile, is focusing on real-time payments infrastructure. With the European Payments Initiative’s launch of the Wero wallet in October, French customers of BNP Paribas, Société Générale and other major commercial banks can now make instant account-to-account payments with the banks’ subsidiaries in Germany. On the wholesale side, Project Ensemble is also sandboxing its tokenised infrastructure, which would enable instant wholesale payments between euros and Hong Kong dollars.

With the new technologies supporting digital payments, we’re likely to see momentum for the cashless transition from the business side, along with increasing demand for cross-border payments in the Eurozone.

Cashless network beyond the Eurozone

Looking at the bigger picture, the Eurozone has been preparing for the cashless transition over several years. In 2008, SEPA was introduced by the European banking and payments industry, with the support of national governments, the European Commission, the Eurosystem and other public authorities.

The initiative facilitates cross-border euro payments within one to three business days, to both EU and non-EU countries. This includes 27 countries in the Eurozone, as well as participating territories such as the UK, Switzerland and Monaco. The European Payments Council reported that SEPA handled 42.6 billion credit transfers, while also managing 21.6 billion direct debits, in 2022 (the most recently published annual data).

The initiative has evolved into four payment schemes, with the latest SCT Inst scheme enabling instant 24/7 credit transfers across 32 European countries. As of November, a total of 2,627 PSPs are participating in SCT Inst, including Wise, Western Union and Revolut. Germany has the highest participation rate, with 1,121 PSPs, representing 43% of the total participants. Austria and Italy come in second and third place, with shares of 14% and 13% respectively. While SCT Inst is gaining attention among European PSPs, the scheme is still not equally available to account holders across all SEPA countries.

As this cashless transition gains momentum in the Eurozone, the question remains whether this shift will be mirrored outside the region, where many markets lack the centralised authorities driving payment innovations.