Flywire has reportedly been exploring a potential sale to private equity investors. As the company revises its revenue guidance downward and announces its latest B2B payments acquisition amid its Q2 2024 results, we discuss the historic performance of Flywire, its sale potential and its strategy going forward.

Last week, reports emerged that Flywire was exploring a potential sale alongside investment bankers at Qatalyst Partners, with potential buyers including private equity firms. Talks were still at an early stage with no deal certain, according Reuters, citing unnamed sources close to the matter.

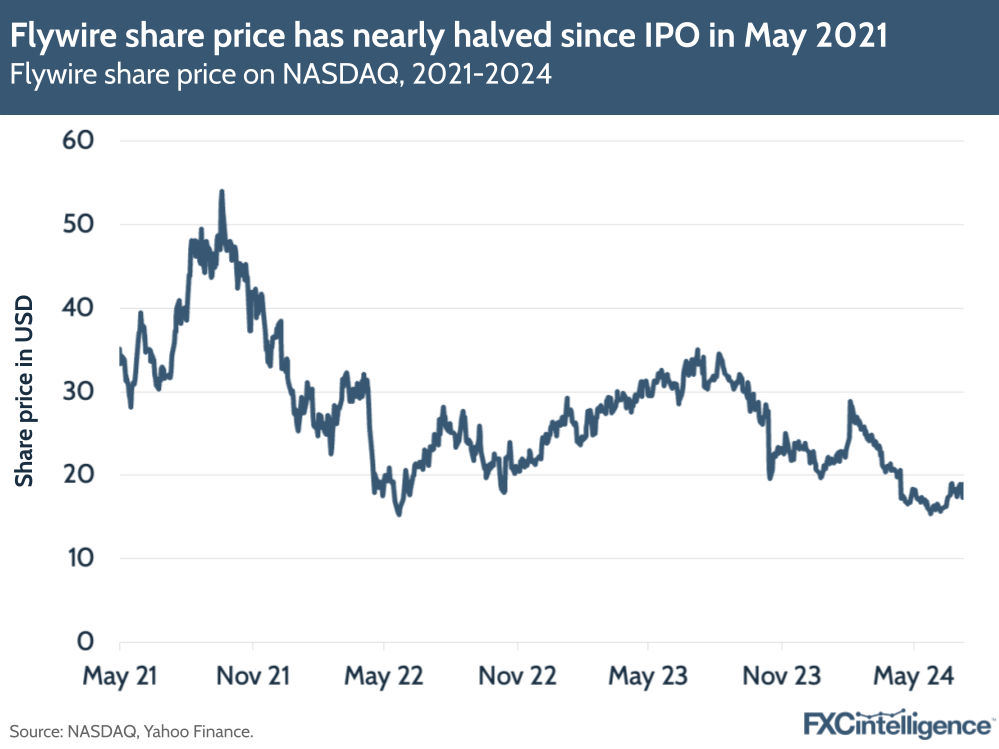

Flywire has not formally confirmed or denied whether it is exploring a sale, and there was no direct mention of the news in its Q2 2024 earnings call this week. However, some have speculated that the company’s declining share price since its IPO in 2021 could be a factor.

The company did, however, announce its own purchase of another company – accounts receivable SaaS business Invoiced – to help bolster its B2B payments segment.

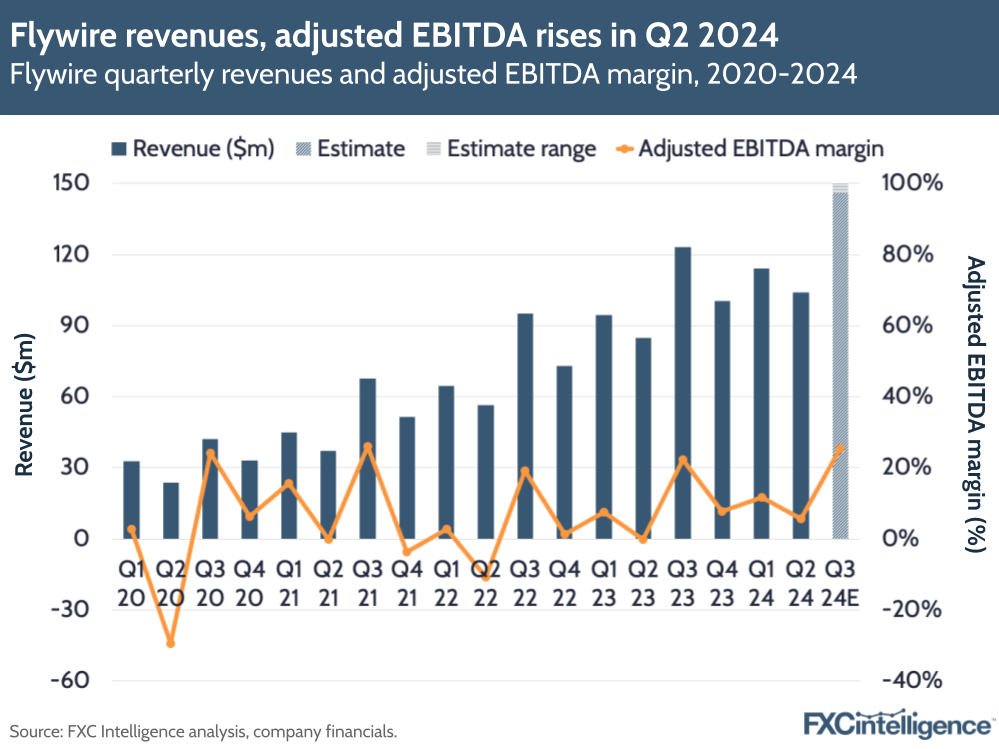

Flywire saw revenues rise 22% to $103.7m in Q2, driving an adjusted EBITDA margin of 5.6%. However, it once again revised down its revenue expectations for FY 2024, from $491m-519m to $483m-506m on the back of an anticipated revenue impact due to student visa policy changes in Canada.

In this report, we explore what could be driving the reported sale, Flywire’s current market position and historic performance.

Flywire’s position in the market

Flywire is a global payments company that has evolved to serve the international payments space across four main verticals: education, B2B, travel and healthcare.

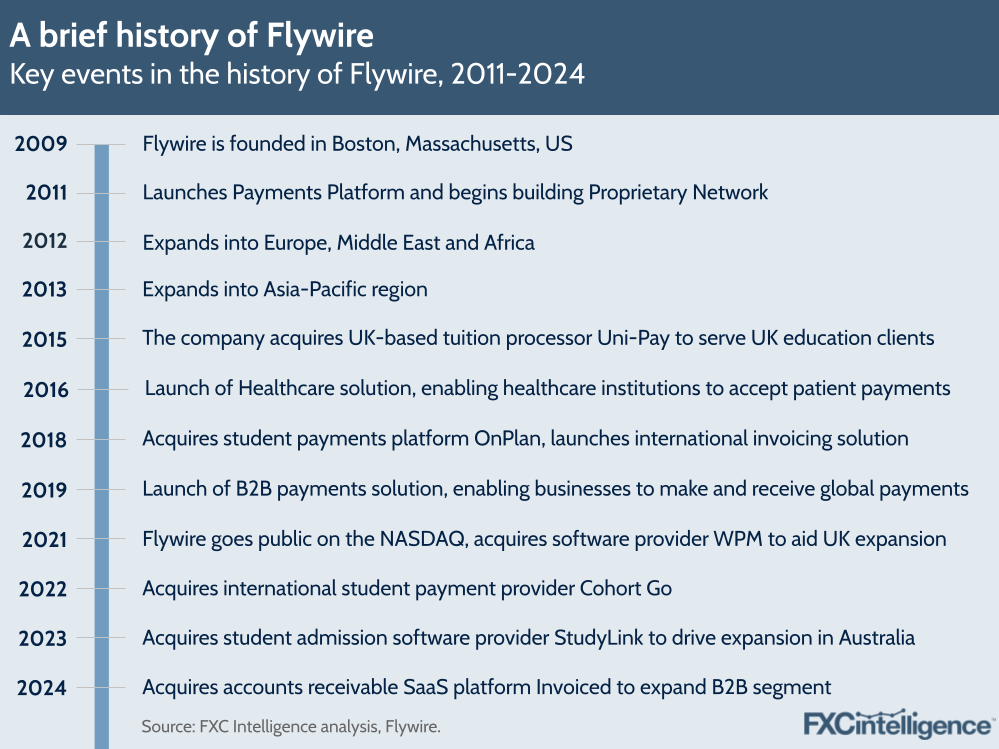

Originally called PeerTransfer, the company was founded in 2009 by Iker Marcaide, an entrepreneur who discovered how difficult it was to make international payments while applying to Boston’s MIT Sloan School of Management. In 2013, the CEO role passed to Mike Massaro, with PeerTransfer being renamed Flywire in 2015 to better reflect the company’s “expanding global footprint”.

Today, Flywire offers a payment platform that facilitates payments across more than 140 currencies and allows clients to accept and settle payments in over 240 countries via a proprietary global payment network made up of leading banks and payment partners worldwide.

Driving this are more than 1,200 employees (or “Flymates”, as the company calls them) across 12 offices globally. As of Q2 2024, the company serves more than 4,000 clients worldwide.

In 2021, the company went public through an IPO on the NASDAQ exchange, with shares debuting at $34 a piece, bringing the company to a $3.5bn valuation. Its goal with the funding was to grow its employee base, expand into new markets and geographies; add more bank accounts and payment methods; and make new acquisitions.

In terms of its wider strategy, Flywire has been broadening its reach through a number of acquisitions, with the majority of these being related to education (Uni-Pay, OnPlan, Cohort Go, StudyLink), and has now added to this with Invoiced. It has also involved the company spreading to new geographies beyond North America, including Europe, the Middle East and Africa (EMEA) and the Asia-Pacific (APAC) region.

However, another goal for Flywire has been to extend its reach with existing clients, with the company reporting 125% average annual dollar-based net retention rate in its full-year 2023 results.

How is Flywire differentiating itself from competitors?

While other players in the payment processing space might have a broader focus (for example, targeting enterprise or SMEs across a variety of industries), Flywire aims to differentiate itself by being the expert in the four specific verticals it serves, each of which feature high-end, complex payments that have historically come with high costs, lack of visibility and a high manual workload to process. These specific industries, Massaro told us after the company’s first set of results as a public company, have been somewhat left behind by innovation that has been seen in ecommerce and retail payments.

The company started out serving education payments – payment acceptance and software solutions for higher education institutions that receive large numbers of international students needing to make payments over borders. It has since extended to offer solutions to support billing and payment acceptance for healthcare, travel and B2B, but the company’s primary focus (and largest source of revenues) remains its education segment.

Another key difference from competitors is that, alongside an integrated payments network, the company offers billing, payment and reconciliation software that is specific to its target verticals and can be embedded into existing workflows for clients or enterprise resource planning systems.

Its revenues are split into two streams: transaction revenue, which covers fees earned from processing payments for clients, and platform and other revenues, which covers software subscription and usage-based fees; commissions from insurance providers; and interest income from customers holding money in accounts with the company.

Transaction fees make up the highest share of revenues, with the company seeing 82% of its FY 2023 revenues from transactions in 2023, and this revenue share has only grown over time.

Analysing Flywire’s share price performance

While Flywire has not spoken out about the sale yet, there has been speculation over whether the company’s share performance since its IPO in 2021 could be a factor.

In the wake of its successful IPO, Flywire’s share price rose substantially, peaking at $53.96 in October 2021 – this was following a quarter in which the company saw 61% revenue growth and positive net income and adjusted EBITDA.

However, the company’s share price dipped in 2022 and despite beating a path to recovery in 2023, saw headwinds from FX rates and changes to student admittance policies. Investors also continued to take note of the company’s bottom line, in particular consistent periods of net loss, as well as rising operating expenses.

Overall, Flywire’s shares have lost nearly half of their value since the company’s IPO in 2021, and have also underperformed this year against the S&P 500 Transaction and Payment Processing index.

As part of its most recent results, the company has released a share repurchase program, with CFO Cosmin Pitigoi saying this was “a direct reflection” of the company’s confidence in the long-term potential of the business. “We believe this program still allows us ample capacity to continue investing organically and to pursue strategic value-enhancing acquisitions,” he added.

Following Flywire’s Q1 2024 results, TimesSquare Capital Management, an equity investment management company, released a report in June (cited from Yahoo Finance) that explained several reasons why it had sold shares of the company: “These included a secondary equity offering without a deal in hand, the CFO announced he was leaving the company, insiders continued to sell shares and we did not gain comfort that last quarter’s shortcomings were only temporary.”

If Flywire is acquired by a private equity investor, this would continue a trend that we’ve seen amongst a number of other players in the cross-border payments space – most notably Canada-based payment processor Nuvei, money transfer player MoneyGram and UK-based payments processor Worldpay.

Flywire’s Invoiced acquisition and B2B strategy

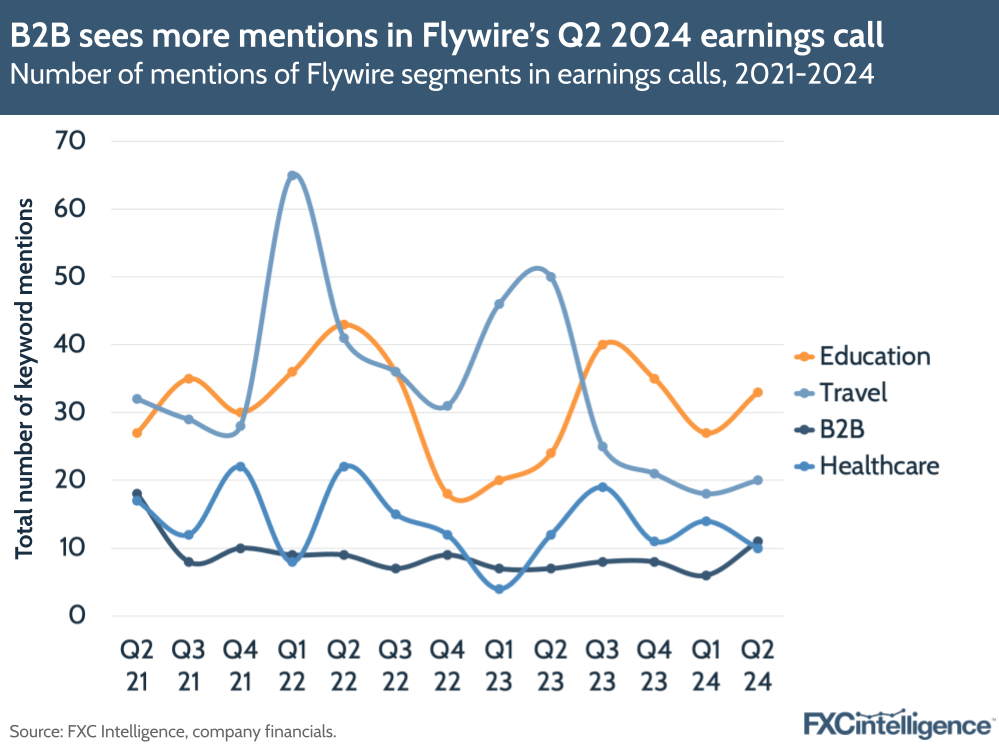

Aside from Flywire’s future as a public company, it continues to build upon its B2B offering with Invoiced – which accompanied a spotlight segment in its earnings call focused entirely on its B2B services.

Flywire is hoping to combine Invoiced’s A/R automation software with its global payment network to help bolster its B2B segment. According to Massaro, the move will complement the existing business and help Flywire to “significantly accelerate” its product roadmap.

Initial gains from the business aren’t a seismic shift to Flywire’s wider business, with the company expected to add approximately $2m of revenue and profits from the company being reinvested this year to grow the combined business.

Having said this, the acquisition marks a departure from more recent acquisitions that have been focused on education payments, and belies a move to take more of the B2B addressable market at a time when other cross-border payment companies are shifting their models to focus more on this space.

Back in its Q4 2023 earnings, Flywire highlighted that it sees the highest total addressable market across its verticals being the B2B market at $10tn. This is substantially higher than the market it sees for education ($660bn), travel ($530bn) and healthcare ($500bn), and we project that B2B payments will be a $50tn business by 2032.

In its most recent SEC filing, Flywire did mention that its strategy going forward is largely influenced by expanding into new clients including B2B payments – however it has caveated this, saying the company is less experienced in this area and that B2B payments carry a higher risk profile than education or healthcare receivables.

It said that the payment volume and resulting revenue from B2B payments is expected to represent less than 10% of total payment volumes and revenue for the foreseeable future, but expects this to grow over time.

Flywire’s earnings performance over time

In an interview given to Yahoo Finance at the time of the company’s IPO in 2021, Massaro said that the company was targeting growth in the medium term (specifically three to five years), with profitability expected in the longer term. The company’s progress over the years has supported this, with consistently solid revenue growth and client expansion – but also with persistent net losses.

Flywire’s revenues rose 22% to $103.7m in Q2, while revenues excluding ancillary services (i.e. printing and mailing services and marketing fees) grew by 26% to $100m. This drove an adjusted EBITDA of $5.8m in the period (up from -$0.1m last year), leading to an expanded EBITDA margin of around 5.6%, up from -0.1% last year.

Gross profit also increased to $61.9m, resulting in a gross margin of 59.7%, up from last year. Regarding what’s driving profitability, Flywire CFO Cosmin Pitigoi said that despite the company seeing “downward pressure” with more use of credit cards in travel and B2B, the company was seeing “stronger trends” across its main education corridors.

Despite the revenue guidance change for FY 2024 in its results, Flywire raised its adjusted EBITDA guidance for the year to $72m-80m, up from $64m-75m, which would give a margin of 14.9-15.8%. The company mentioned that improving processes through automation will help it see a steady improvement in adjusted EBITDA margin as it scales.

The company’s revenues have grown consistently and at a solid rate, particularly when compared to many other cross-border payment processors we track, though growth has slowed compared to previous years, particularly during the pandemic. This is aligned with a growing demand for digital payments during this period.

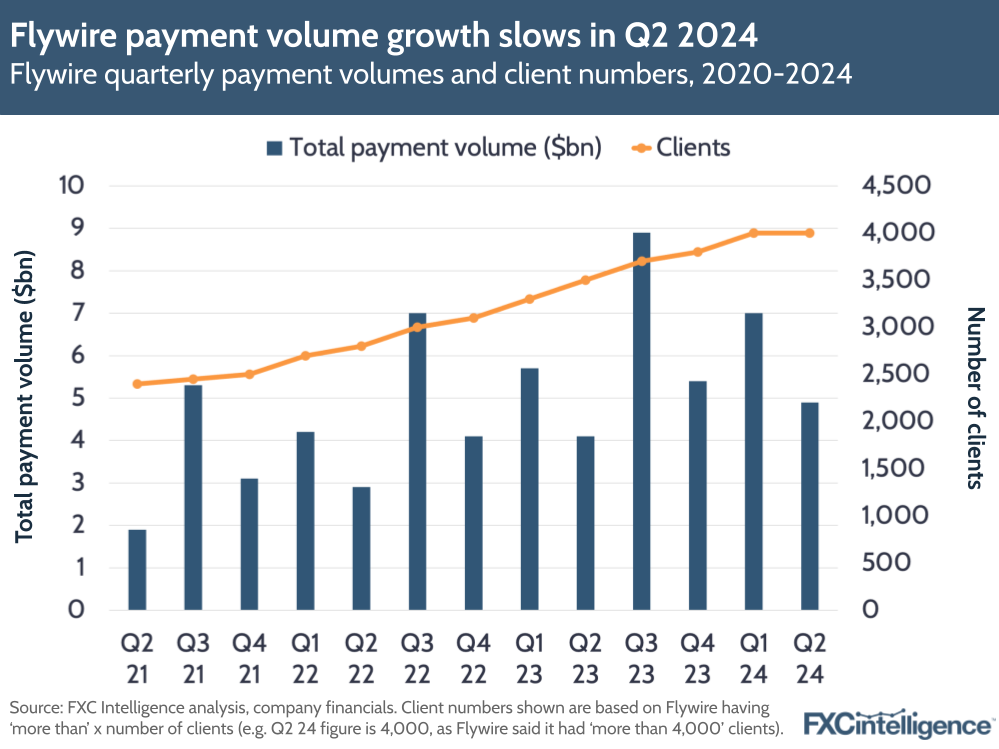

Flywire has noted before that it sees an “inherent seasonality” across its verticals – for example, Q3 is when many payments are made to higher education institutions, leading to higher transactional income during that period.

This seasonality is seen from the company’s total payment volumes. In Q2 2024, Flywire still saw solid growth in volumes, which rose 19% to $4.9bn, though this was slower than previous Q2 growth figures (41% in Q2 2023, 53% in Q2 2022). Meanwhile, the company also managed to add an additional 200 customers during the quarter.

Flywire executives said that they were seeing a “slower-than-expected” recovery in Canada, which created a mid-to-high single digit negative million dollar impact, instead of positive growth in Q2. However, they did note that this was offset by better than expected volumes from UK and Australia, as well as “stronger international corridors performance”.

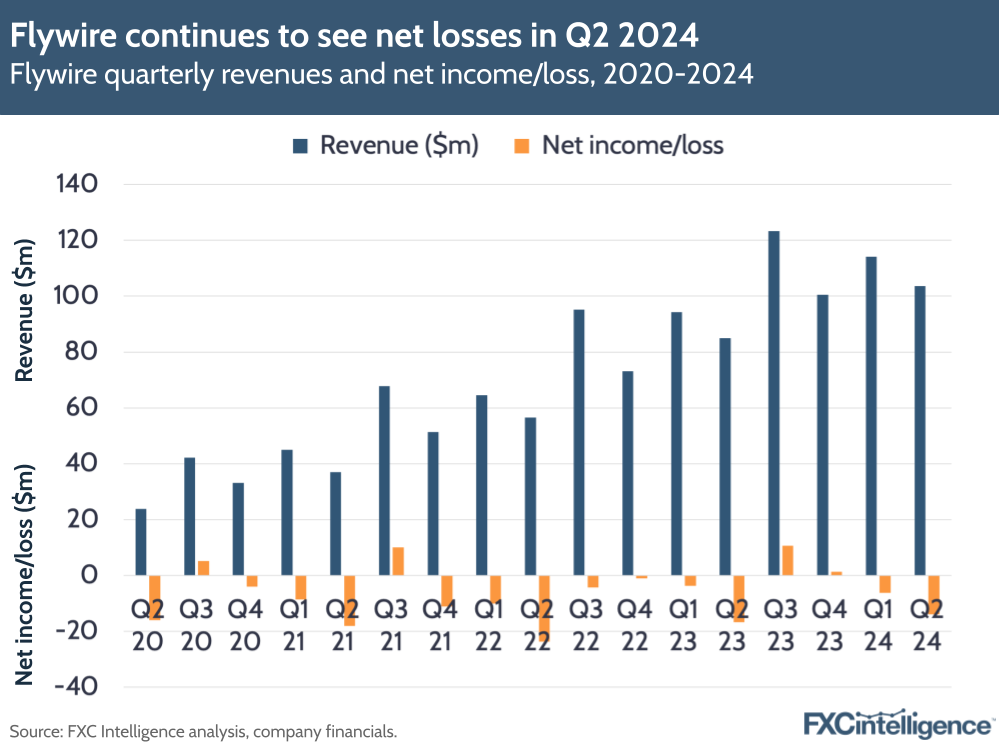

Looking more closely at Flywire’s net income versus losses, we see the seasonality again from the company’s verticals, with Q3 seeing higher revenues and net income, but other quarters seeing the company making a net loss overall.

In Q2 2024, the company’s net loss was -$14m, which was an improvement by approximately $3m compared to the same period last year, and executives noted that a higher income tax provision has amplified its losses in Q2 due to the seasonality of the business. However, they said that this should normalise as the company moves towards profitability.

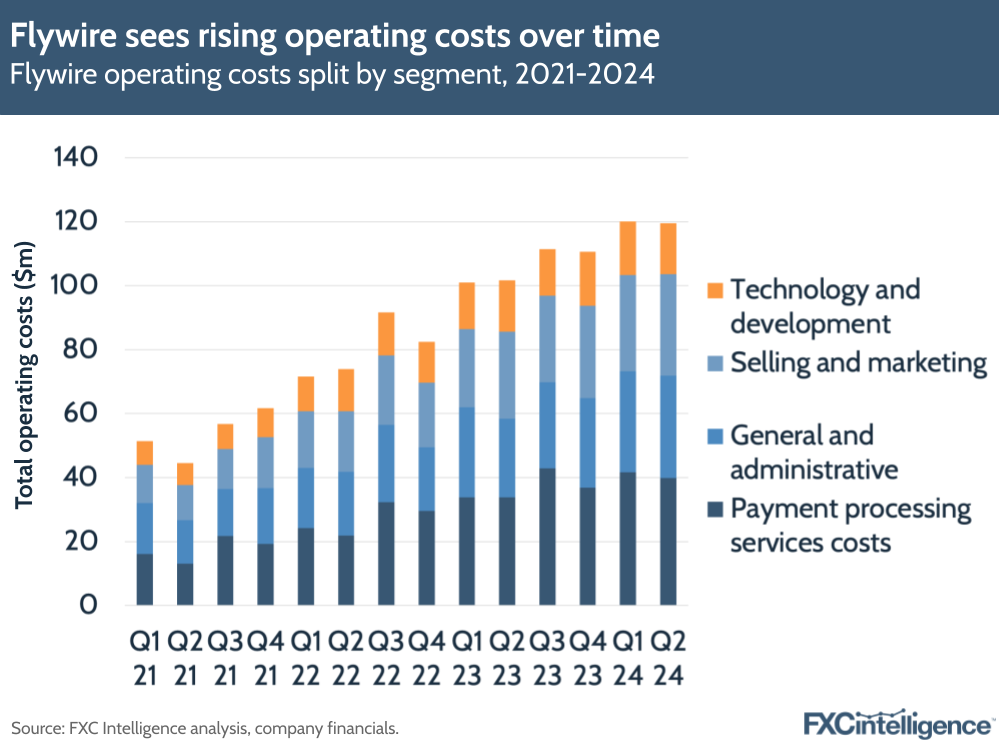

As its transactional income has grown, Flywire has seen operating costs rise, principally across payment processing fees, followed by general and administrative costs (i.e. including things like personnel and office costs), selling and marketing and technology and development.

In Q2 2024, total operating costs rose by 17%. However it should be noted that as payment processing costs make up the majority of total operating costs, this growth is down compared to previous years when the company’s payment processing volumes were growing at a faster rate.

Flywire’s expansion into new geographies

A big part of Flywire’s strategy has been moving into new geographies, as shown by its acquisitions of UK-based Uni-Pay and Australia based StudyLink, as well as partnerships with State Bank of India and WhatsApp in China. More recently, in July, Flywire also partnered with HDFC Credila to streamline cross-border education loan payments from India.

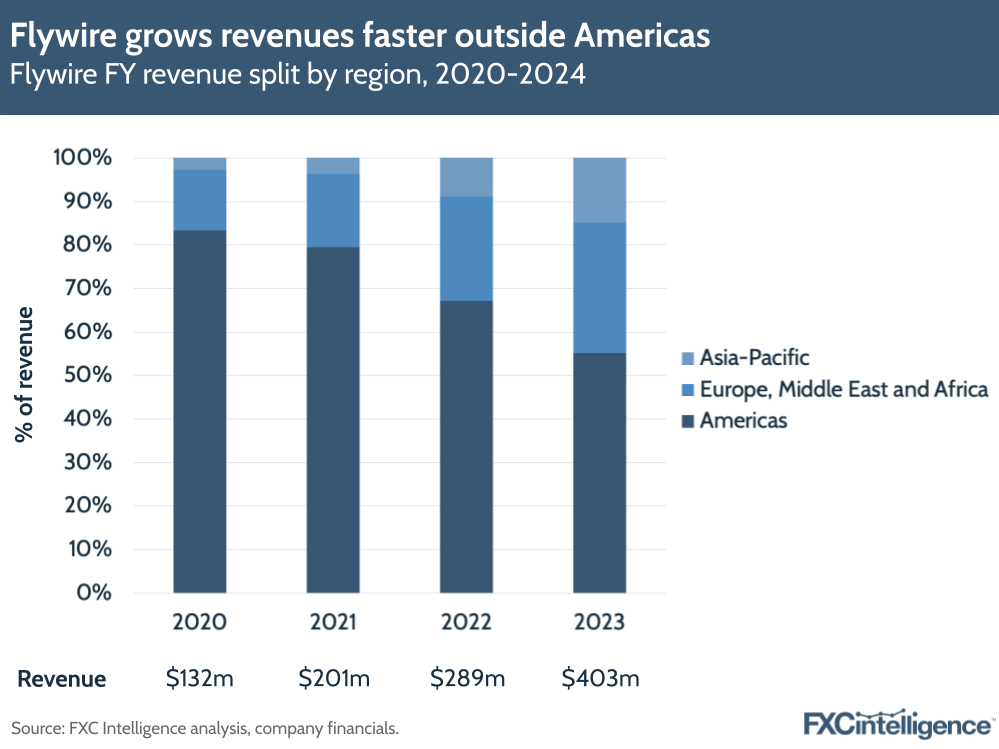

This move into new markets is reflected in Flywire’s annual results for 2023, in which the company broke down its revenue streams across the geographies it serves, including the Americas (US and Canada), EMEA and APAC regions.

In the Americas segment, Flywire is still growing but that growth has slowed as Flywire has become a more mature player in this market. Meanwhile, in EMEA and APAC, there is still a lot more room to grow. In terms of revenue growth, APAC grew by 132% in 2023 while EMEA grew by 75% and Americas grew by 14%.

The Americas segment still accounted for the company’s highest revenue share in 2023 at 55.2%, though this has declined from 83.3% since 2020. In the same time period, the EMEA segment has grown from 14% to 30% revenue share, while APAC has grown from just 2.7% share to 14.8% share.

Breaking down Flywire’s different verticals

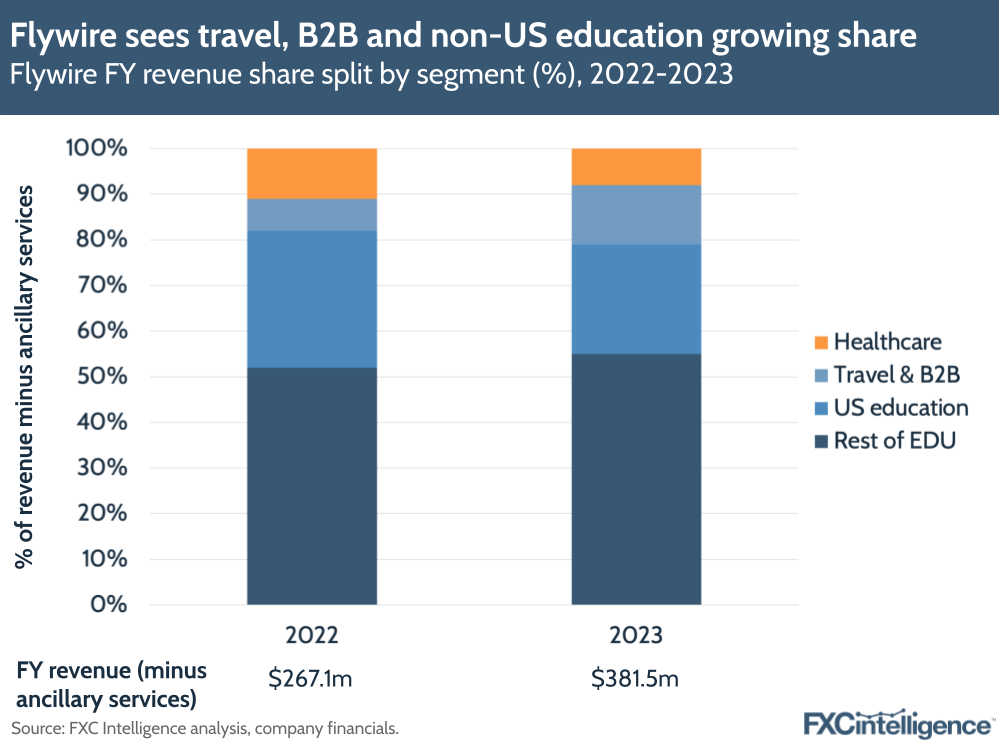

Flywire’s annual segment breakdown further demonstrates the extent to which the company has expanded its reach to markets beyond the US. Education in non-US markets took a 55% share of revenues minus ancillary services in FY 2023, up from 52% in 2022, while US education’s share was down from 30%.

Having said this, on an annual basis the combined Travel and B2B segment grew by 123%, while education grew by 53% and 19% in non-US and US markets respectively. Healthcare meanwhile – an offering launched much earlier than travel and B2B – declined by 1% in 2023.

Travel remains a big contributor to Flywire’s recent growth and has grown over 55% in H1 2024, with APAC travel growing over 75% in the first half of the year. Having said this, education is still key for Flywire, with the company serving more than 2,950 education institutions as of its Q2 2024 results, compared to more than 90 healthcare systems and 1,100 clients split across its travel and B2B segments.

For Q2, the company saw an increase in new clients signed and an increase in pipeline value creation compared to Q2 of last year. However, as the company has noted in previous reports, its education business may be adversely affected by decreases in enrollment or tuition, increased limitations on issuances of visas to international students, or higher operating expenses for clients.

The company saw the impact of this in Canada earlier this year, with the Canadian government announcing it will set a cap on international student permits for the years 2024 and 2025 as a result of housing shortages. In Q2, it noted a modest ramp in international students enrolling in colleges and associated revenues better than Q1, but regulatory announcements and uncertainty have generally come in below its previous expectations. Canadian student policies have therefore impacted revenue growth and the company expected this weakness to persist in the next half of the year.

Flywire did mention some offsets for this however, including an expanded partnership with Global University Systems Canada – a network of 40 higher education institutions – and strong transaction volumes through the University of Toronto, which went live with Flywire last year.

Moves in Canada are being reflected in other countries – for example, the UK recently released new visa rules that have seen international students in the UK having job offers rescinded after changes to visas made hiring them too expensive. The seasonality and changeability of education could be a decisive factor in Flywire’s strategies to further expand travel and B2B – its newer segments.

While Flywire’s diversification into new countries and partnerships are helping drive into new areas, investors will increasingly be looking to see if the company is able to build upon its foundations and overcome potential setbacks and uncertainties around its core markets going forward.