Latin America is a hotbed of opportunity for the cross-border payments industry, as ecommerce booms and the region increasingly adopts digital payment methods. In this report, we explore key trends and insights for this burgeoning market.

Latin America continues to see developments across the cross-border sphere, from ecommerce to remittances, SMES and international trade, as well as a growing demand to support payments for freelance and gig workers. A growing push towards digitalisation in some countries – spurred in some cases by government backing, in others by fintechs filling the gap – is driving the development of alternative payment methods that are in turn having an impact on cross-border spending.

With digital adoption growing in Latin America, the potential to support payments flows into and out of countries in the region is massive, with an array of opportunities for both homegrown and external players to capture in the space.

However, a number of regulatory challenges – as well as widely varied macroeconomic conditions and currency volatility – are making it harder for the region to move towards the goals of creating faster, more cost-effective and transparent cross-border payments. This report looks in detail at some of the key players in the Latin American payments space, asking where global payments players see the opportunity and what the future of payments may look like in the region.

Latin America cross-border payments: Overview and key players

The five most populous countries in Latin America and the Caribbean (LAC) – Brazil, Mexico, Argentina, Colombia and Peru – account for 72% of the total population of LAC, based on Worldometer’s population figures across countries within the UN’s definition of the LAC region. Moreover, Brazil and Mexico together account for 56% of the region’s total GDP of $7.1tn.

As the two biggest economies, Brazil and Mexico both dominate cross-border trade, which in turn means high B2B flows, and they also see high remittances – particularly Mexico, which is the second-largest recipient of remittances in the world behind India. Having said this, smaller economies are more dependent on remittances, with countries such as Nicaragua, Honduras and El Salvador seeing remittances take up a significantly higher proportion of GDP than across the LAC region on average.

On the ecommerce side, Latin America has experienced a recent boom, driven in part by a rise in internet connectivity and smartphone adoption, as well as the expansion of digital payment solutions. This in turn presents a major opportunity for international payments players to facilitate payments acceptance for merchants and online marketplaces selling wares both to other Latin American markets and internationally.

A mix of macroeconomic factors, government influence and regulations influences the ways that consumers in the region are making payments. In Argentina for example, the prevalence of economic instability and inflation – driven by high public overspending and a reliance on printing money – has led to a major decline in its currency. This in turn has led to growth in buy now, pay later services, with some Argentines even using USD along informal channels. Meanwhile, Brazil, which has adopted real-time payments system Pix, is seeing the vast majority of its population now making payments digitally, with some merchants no longer accepting cash payments at all.

However, one of the strongest themes to emerge is that Latin America’s payments industry is still largely fragmented, both in respect to the varying levels of payments maturation in each country and the regulations that control them.

Reflecting this, the Latin American payments space is a mix of traditional incumbents versus disruptors. Established money transfer providers such as Western Union, MoneyGram and Ria have focused on building out their vast payout networks across Latin America, though these companies are also moving to digitalise there.

The industry has seen a number of homegrown players rise to aid with challenges in the market. On the processor side, two of the biggest are dLocal and Ebanx, while Mercado Libre is the most popular ecommerce player across Latin America. However, it is notable that many of the more well-known players operating in the space are not headquartered in Latin America. Significant market investment has continued this year, with B2B payments player Airwallex securing a payments licence in Brazil and Wise enabling transfers for Mexican citizens across its global network.

Having said this, a key theme across recent earnings from public global payments players operating in Latin America – from processor dLocal to remittances provider Intermex – was a need to diversify outside of Latin America in order to protect against volatility seen both in the region and in emerging markets more generally.

In particular, Intermex noted it is increasingly exploring digital opportunities and growth after a slowdown in the remittance market for Mexico in 2024 affected its core retail-based money transfer revenues. Various factors have been cited as contributing to this slowdown, including a weaker US labour market, fluctuations in the Mexican peso against the US dollar and potential policy changes linked to migration.

While digital payments growth and a rise in cross-border ecommerce activity make Latin America an appealing opportunity, movements to shore up businesses against volatility highlight the need to have deep, real-time insights into flows across these regions and how different players are competing across them.

More data-driven reports and expert analysis on Latin America’s cross-border flows.

How digital connectivity is driving growth in Latin America

Latin America, on the whole, is still seeing a high amount of cash usage. Many people still lack full access to traditional financial services, which has created a significant gap that some fintechs have managed to fill. Some countries are increasingly adopting digital payment methods, which is in turn influencing cross-border payments as more people are able to pay and receive using digital methods.

A big factor with digital growth in regard to payments has been the presence of unbanked people in Latin America. On a regional level, this has seen a significant shift recently, with the World Bank noting that the share of adults with a bank account across the LAC region grew from 55% in 2017 to 74% in 2021.

This was largely driven by a mix of government-led initiatives (such as Brazil’s Pix) to increase connectivity and digital services, particularly with the advent of the Covid-19 pandemic. Looking closer, however, shows that there is still a great deal of variation across individual countries. For example, Chile tops the ranking with 87% of adults banked in 2021, followed by Brazil and Venezuela with 84% each, up from 74%, 73% and 70% respectively in 2017. However, on the other end of the spectrum, countries like Honduras (with a 38% share in 2021), El Salvador (36%) and Nicaragua (26%) still have highly unbanked populations.

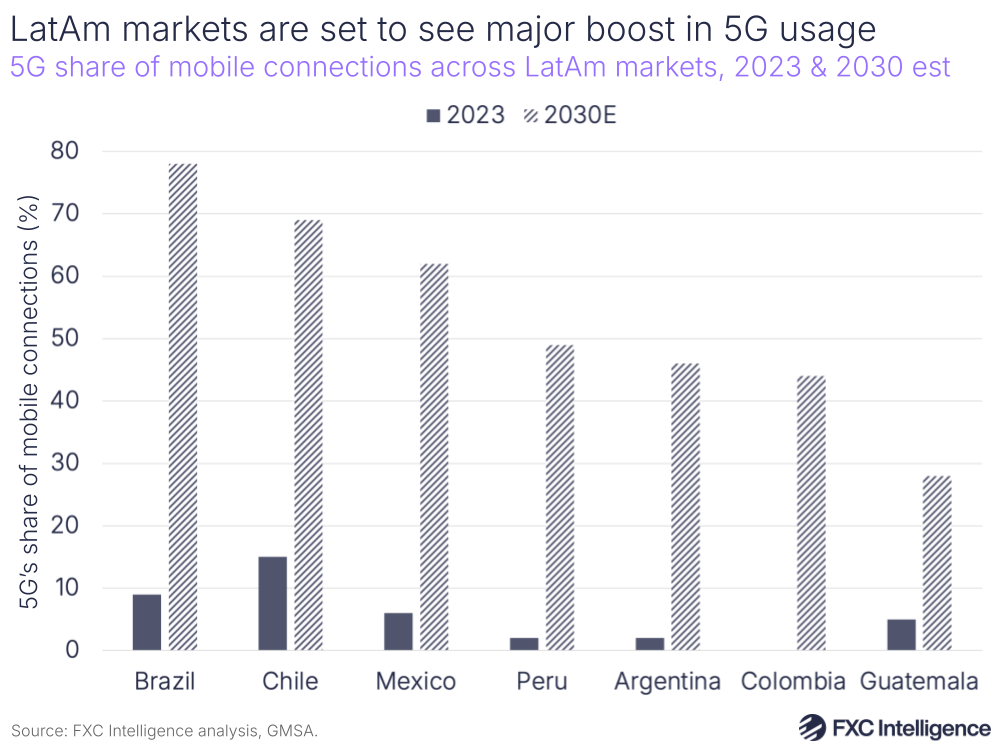

Similarly, figures from GMSA Intelligence show that the percentage of the Latin America population connected to mobile internet has risen substantially in some countries – such as Brazil and Mexico – but not so much in others, such as Guatemala. Overall, around 64% of the Latin American population was connected to mobile internet in 2024, up from 50% in 2017, while the percentage of smartphone connections across the region has risen from 62% in 2017 to 81% in 2024. The latter figure is expected to rise to 93% by 2030.

Digital initiatives across Latin America are expected to continue to help drive connectivity in the region. The GSMA figures show that Latin America as a whole is still seeing lower adoption of 5G than other regions globally, at 9%, but this is expected to grow to around 53% by 2030, making Latin America one of the fastest growing emerging 5G infrastructure markets.

As smartphones become more affordable, their adoption across emerging markets will continue to grow. This, combined with rising adoption of digital payments, is already creating fertile ground to enable cross-border ecommerce. Some of the major examples of digital wallets that have experienced rapid growth include MercadoPago, which is owned by MercadoLibre, and Brazilian app PicPay, alongside alternative payment methods.

Some digital wallets in the region are also partnering with companies in the cross-border payments space to enhance their offerings – for example, Mercado Pago’s partnership with Western Union and Xoom to enable transfers to Mexico and Argentina. Meanwhile, a number of digital players across B2B, consumer payments and remittances are helping spur these industries in the region.

The broader growth of digitalisation has also driven the demand for the benefits that digital can bestow on cross-border payments. Namely, faster and more efficient transactions at lower prices, particularly when it comes to remittances.

Track the cost of cross-border transactions globally to enhance your ecommerce strategy

Latin America’s real-time payments boom

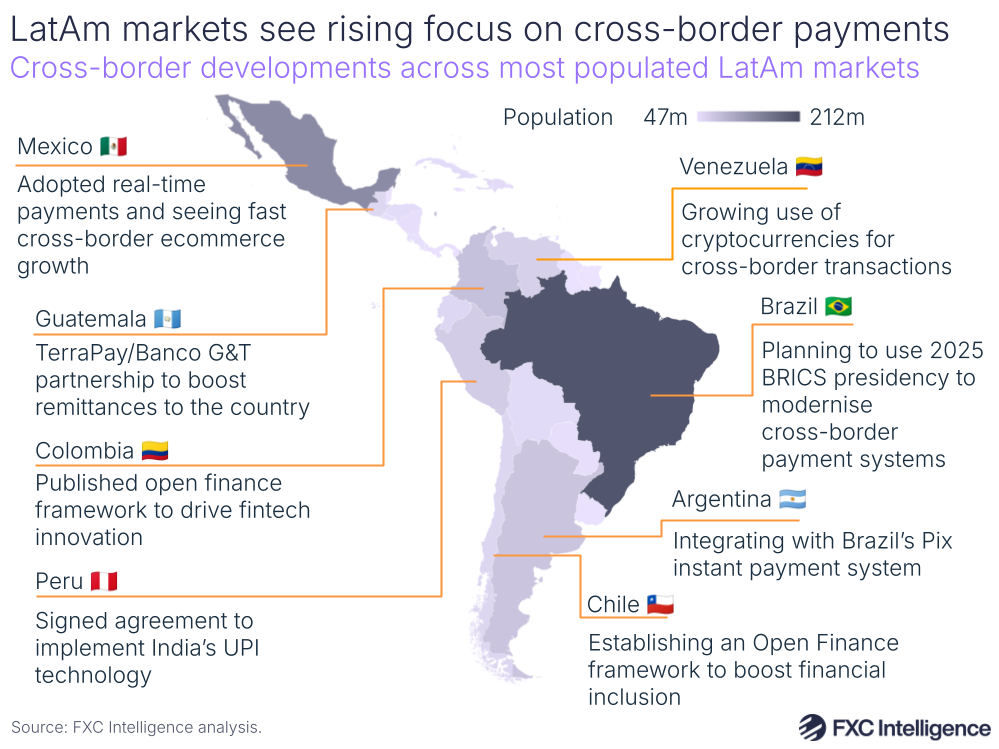

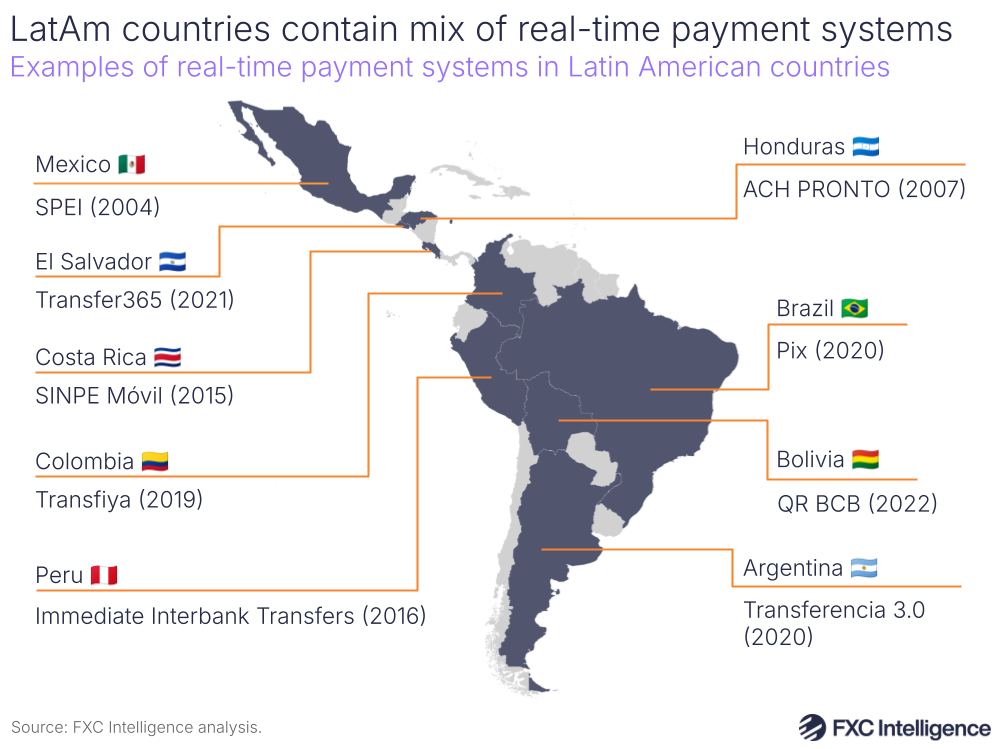

Over the last 20 years, but particularly over the last decade, countries across Latin America have been building out their real-time payments (RTP) infrastructure with the aim of speeding up domestic payments. These real-time payments systems enable individuals or businesses to transfer money or make payments across a network without any delays 24 hours, seven days a week, thereby bypassing lengthy delays.

RTPs are now widespread across the region, with key examples including Brazil’s Pix, Mexico’s SPEI and CoDi and Colombia’s Transfiya (the country is expecting to launch a new instant payment solution, Bre-B, this year). Other countries in the region are at various stages with their RTPs. Some have launched recently and are building traction (Bolivia, El Salvador, Argentina), while others are still in development.

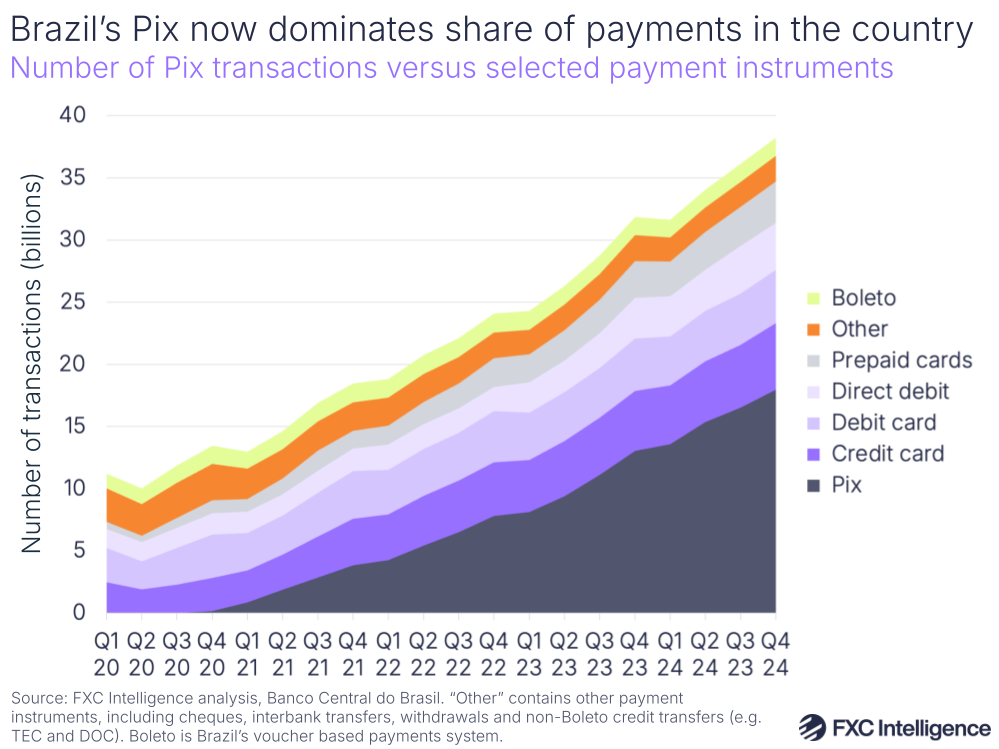

Brazil’s Pix is the standout example for RTP success in Latin America, driven by the central bank mandating the participation of major banks, the promise of low transaction fees and the Covid-19 pandemic spurring a nationwide move towards digital payments. Since its launch in 2020 Pix has grown significantly, with over 90% of Brazil’s adult population using the system, driving an estimated 63 billion transactions in 2024. Also in 2024, Pix accounted for 45% of all transactions across other payment instruments tracked by the country’s central bank (which include cards, direct debits, cheques and the country’s Boleto virtual voucher payment system).

“Pix has shown that if the central bank is able to enable a broad, wide-sweeping system it’s a tailwind because when people feel like they have authority over their money, they’re able to make better financial decisions,” says Imran Ahmad, General Manager at Mexican crypto exchange and payments infrastructure provider Bitso.

While some RTPs in the region have seen success, this is still only being seen with domestic transactions. One of the questions revolving around RTPs now is the extent to which they can be made interoperable with one another, with one potential benefit being making both intra-regional and global cross-border payments faster and less costly.

Once again, fintechs have been coming in to fill the gap. Brazil-based payment service provider PagBrasil, for example, has launched International Pix, a payment acceptance infrastructure solution allowing merchants across countries outside Brazil to accept payments overseas. Through partnerships, it has brought the system to a number of Latin American countries – including Argentina, Uruguay, Mexico, Paraguay, Peru and Chile – as well as countries outside the region such as Portugal, Spain, the US and China.

The company has also launched Pix Roaming, which allows international tourists to pay using Pix – which is increasingly important as more and more Brazilian merchants move away from credit card acceptance and towards Pix, which comes with lower acceptance costs attached. In February, the company said that the total volume of transactions made through Pix Roaming was expected to reach R$1bn ($174m based on March 2025 exchange rates) in 2025 and $2bn ($347m) in 2026.

“People tell us they would like to use the same thing to pay when they travel to Argentina or when they travel to Portugal or when they travel to the US,” says Ralf Germer, CEO of PagBrasil. “The future trend is this interconnection of these payment systems.”

Interoperability of RTPs has already been a key topic in Southeast Asia, with a series of partnerships allowing visitors to make cross-border payments using QR codes across countries like Singapore, Malaysia and Thailand. India, meanwhile, has now been expanding the reach of its Unified Payments Interface (UPI) system to enable consumer payments and remittances globally. Last year, Peru became the first country in South America to adopt UPI’s technology, enabling instant payments in the country.

However, a number of barriers still remain to driving interoperability of these payment systems, many of which need time to mature. Though Pix is the clearest example of an international export in the same vein as UPI, Germer says that the central bank is currently prioritising other features for Pix (such as enabling recurring payments) and so it is likely to be some time before international expansion becomes a focus.

He adds that geopolitical tensions could further spur the development of domestic payment systems, which bring the benefits of A2A payments. “If you look at India, [the country] developed UPI for that reason as well, because they didn’t want to depend on a foreign payment system,” he claims.

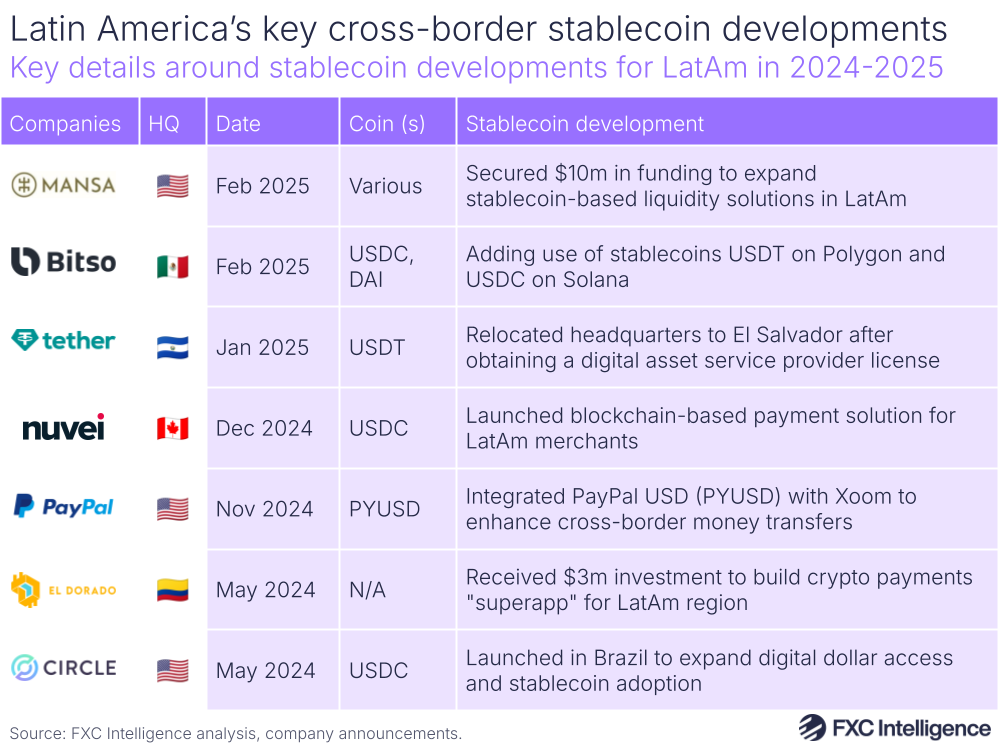

Stablecoin adoption surges in response to macro impacts

A side effect of digitalisation has been growing interest in cryptocurrencies, and in particular stablecoins. This is particularly true in countries such as Argentina and Venezuela, where inflation and currency devaluation have driven people to seek out different ways of storing the value of money and sending money abroad.

As with TerraUSD’s collapse in 2022, the fact that stablecoins can be pegged to other currencies or otherwise ‘stabilised’ does not necessarily protect them from failing. Having said this, the specific use cases stablecoins tend to speak to – economic instability, high cross-border payments pricing, lack of transparency and unbanked populations – have particular relevance to Latin America.

“To the typical Argentinian, USDC is just a common language,” explains Ahmad. “Everyone knows what it is, you don’t have to explain it.”

In its 2024 results, Bitso said that it managed more than 10% of total remittances between the US and Mexico and is currently focusing its attention on Argentina, Venezuela and Brazil, where stablecoin adoption has been the strongest. The company has been one of several in Latin America to see new product launches and developments revolving around stablecoins and cross-border in the space. This includes moves into the region from cross-border crypto players such as Circle, Tether and Ripple.

The latter of these has been particularly active in the region, having partnered separately with crypto exchange Mercado Bitcoin and FX provider Unicâmbio to scale up its blockchain cross-border payments solution in Brazil and enable faster, less costly transactions for business customers. Startups are emerging too, such as El Dorado, which pitches itself as Latin America’s stablecoin-powered superapp, enabling cross-border payments between Latin America countries.

Ahmad says that stablecoins are seeing different levels of adoption amongst consumers and SMBs – under which he includes freelancers and gig economy workers that have moved to Latin America countries – and larger enterprise companies.

“The quickest adoption is on the consumer and the SMB side because it just makes such logical sense,” he adds. “The enterprise companies are a little slower to move down that path because they’re more entrenched in their ways of doing things.”

This analysis fits into a wider theme of legacy players typically taking longer to act than other fintechs, though as we noted in our 2024 state of banks report, global banks are taking steps to innovate – if not always transparently. Ximena Aleman, Co-CEO and Co-Founder of Uruguay-based infrastructure player Prometeo, says the company is remaining cautious about stablecoins currently as the company’s large financial institution clients tend to be “more conservative”. However, she says this could potentially change in the near future.

“I think that the industry will become more stablecoin-dependent,” she states. “What we might see, over the next couple of years, is large financial institutions jumping into the space with their own stablecoins or with partnerships that provide certainty regarding those stablecoins, making the stablecoin technology widely available with protocols and standards to reassure the user that that infrastructure will work properly.”

However, not everyone is convinced by the potential of stablecoins being the next big trend for cross-border payments in Latin America.

CBDCs ramp up in Latin America

Ralf Germer, CEO of Brazil-based payment service provider PagBrasil, says that although stablecoins have seen adoption in areas like Argentina with strict currency controls, he doesn’t currently see stablecoins as being more than a “niche thing”. Despite the rise of digital in Brazil, he points to the fact that large parts of the country can’t connect to the internet or support online payments.

He says this issue could eventually be solved by Pix or potentially by Drex – Brazil’s central bank digital currency (CBDC), which is currently in the second phase of its pilot program. Similar to other CBDCs globally, Drex is being developed to support offline payments, with Banco do Brasil enlisting Giesecke+Devrient to test it for this purpose specifically to support Brazilians with limited or no access to the internet. “With cryptocurrencies being regulated and Drex becoming operative, maybe again, Brazil will be the country that creates the role model,” he says.

Latin America on the whole has seen a surge in interest in CBDCs, with some of the motivations behind this including enhancing financial inclusion, reducing the cost of transactions and making payment systems more efficient. Central banks in the region are also responding to increasing demand for a less volatile digital currency in light of the rise of cryptocurrencies in some countries.

The wider LAC region is home to two countries that have already launched a CBDC – the Bahamas and Jamaica. Based on UN-defined LAC countries that are being tracked on the Atlantic Council’s CBDC tracker, around half of countries in LAC currently have a CBDC project that has either been launched, is at the pilot stage, is being developed or researched. It should be noted that this includes most of the countries in the Eastern Caribbean, which have together launched a blockchain version of this region’s shared currency known as DCash to enable P2P and merchant payments.

Regulation remains a key challenge to cross-border growth

Regulation – and spurring interoperability of payments with regulation – remains a key challenge for the cross-border payments market in Latin America. Alongside moves to support the growth of digital wallets, some countries in the area have launched schemes to help drive the development of fintechs in the region, such as Mexico through its Fintech Law and Brazil through its Regulatory Sandbox initiative.

However, when it comes to payments, a lack of centralised oversight in the region is making interoperability harder. Each country operates under distinct financial rules with no regional standard for cross-border payments, meaning companies need to navigate different licensing regimes in each country. This can mean increased costs and complexity for payments companies trying to scale regionally.

Germer says a lack of regulation in some countries continues to be a major challenge to payments innovation. “Countries need to regulate cross-border and payment transactions, and we, as a company, are involved with the authorities in several countries on this,” he says. “If there’s no regulation, then some companies stretch too much what they can do and what they maybe should not do.”

In particular, driving financial inclusion should continue to be a focus for the region, particularly for countries that are behind Brazil in terms of digital adoption. “Mexico is very cash-centric, and still in Argentina and some other Latin American countries, people want to use cash to avoid taxes,” he adds. “So, there are challenges, but Brazil is clearly a role model for these other countries and private institutions.”

For Aleman, Brazil’s growth has been linked to the fact that the government and central bank haven’t just sought to understand the market but actually helped drive it forward – which is unusual compared to other countries in Latin America, where regulators have just been trying to keep up. “It’s safe to say that the market – the private sector – is the one pushing regulation,” she adds.

As interest in stablecoins has grown in the region, so too has the need to have clear guidelines on crypto and stablecoin payments. Argentina has paved the way here, introducing in March 2025 new regulations for “virtual asset service providers”, which require them to comply with standards around registration, cybersecurity, money-landering and asset custody in order to promote transparency and protect consumers.

Ahmad says that Europe’s Markets in Crypto-Assets Regulation (MiCA) is already influencing not only how people view stablecoins in that region, but also incoming US regulations around crypto, which could provide a strong foundation for other countries to build off as well, especially in Latin America. He says Bitso is pushing “aggressively” to have regulation in place so that it can provide clear guidelines on behalf of its big clients.

“It just makes development life cycles and development processes a lot easier,” explains Ahmad. “Across Latin America, there seems to be this understanding that people want US dollars and that stablecoins offer a way to combat currency, but at the same time it poses a threat somewhat to the local currency.

“That push and pull has been very interesting to see, and the question is how these countries resolve that. Once you put regulation in place, these questions become far easier to address and then the ecosystem can continue to thrive.

LatAm retail payments still significantly above G20 cost targets

As we discussed in our report on the FSB’s KPIs regarding the G20 Roadmap (which contains FXC Intelligence data), there is still some way to go when it comes to reducing the cost of retail cross-border payments. Under G20 targets, global average retail cross-border payments costs should be no more than 1% by the end of 2027, with no corridor seeing average costs above 3%.

However, similar to other regions, the massive potential of Latin America continues to be hampered by inefficiencies in the traditional correspondent banking system, with multiple intermediaries leading to settlement delays, higher fees and less transparency of payments.

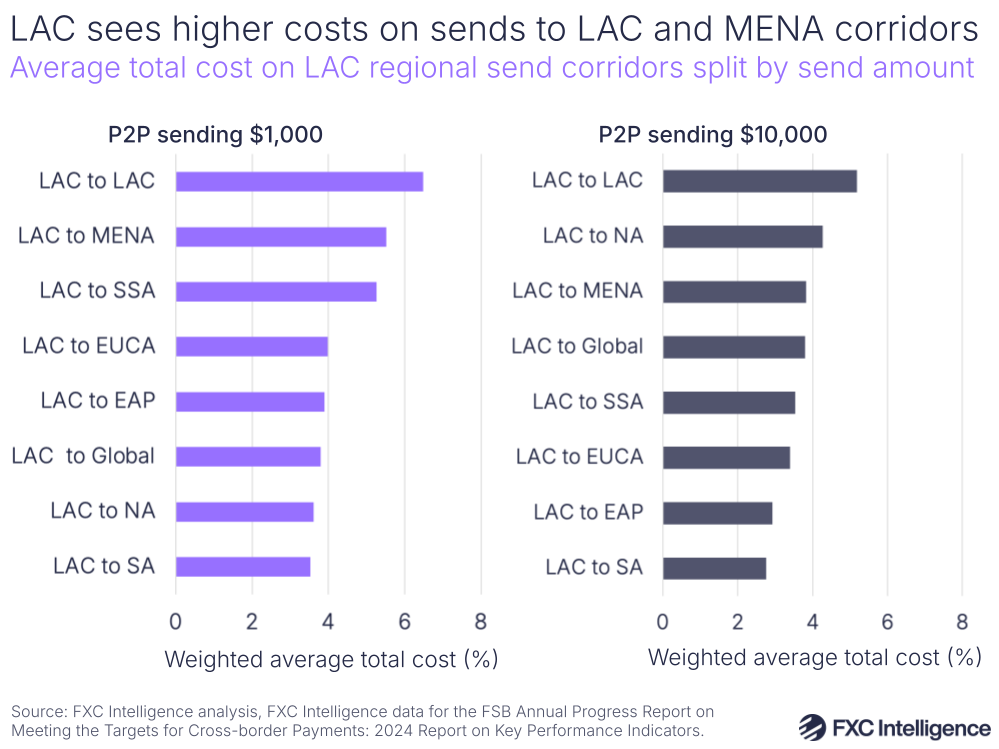

The FSB assessed sending and receiver fees across LAC, as well as Europe and Central Asia (EUCA), East Asia and the Pacific (EAP), Middle East and North Africa (MENA), North America (NA), South Asia (SA) and Sub-Saharan Africa (SSA). Within the dataset, LAC stood out as one region where cross-border corridor costs are still much higher than the assigned target, particularly across P2P payments (which under the FSB definition does not contain remittances).

Across regions globally, P2P payments sent from LAC were the furthest from the target in 2024, with costs overall amounting to 4%, while in the same category LAC also had the highest receiver-side fee (3%). Across every use case – including B2B , B2P, P2B and P2P payments – LAC had average costs above 3%.

LAC sees higher costs on sends to LAC and MENA corridors

The cost of sending P2P payments from LAC to LAC is higher than other corridors across both $1,000 and $10,000 transfers. This fits in with a wider trend that we discussed in our FSB analysis, in which we found that LAC is actually the most expensive region to send P2P cross-border payments from globally.

Across the other most expensive P2P transfer corridors for sending from LAC there is some variation on pricing, depending on the amount being sent. Across $1,000 transfers, the second-most expensive region to send to from LAC was MENA. By comparison, it is less costly to send payments from LAC to EUCA, NA and SA. Looking at higher-value P2P transfers (i.e. $10,000), NA was the most expensive region to send to outside of LAC.

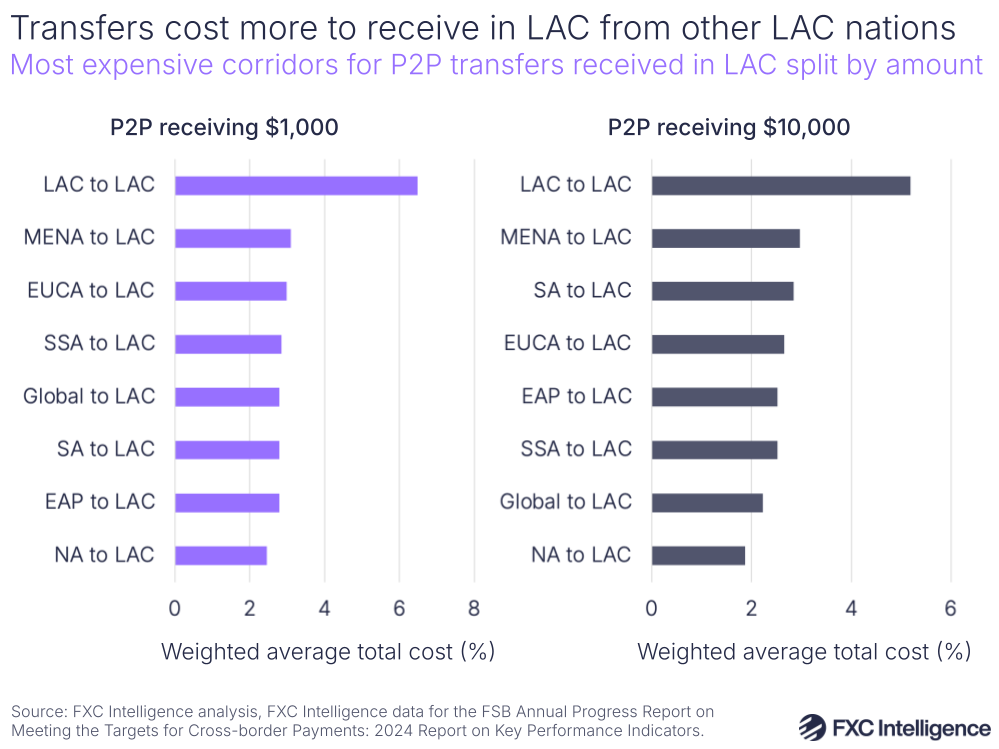

Transfers cost more to receive in LAC from other LAC nations

When it comes to the receive side, it also cost more to receive P2P transfers from other LAC corridors across both lower and higher value P2P transfers in 2024. MENA and EUCA both ranked in the upper group when it came to receiving amounts across both low-value and high-value transfers.

On the other hand, P2P transfers from NA to LAC have the lowest average weighted total cost out of all the regions, which may reflect competition across providers in the region given the proximity and significance of the US to transfers.

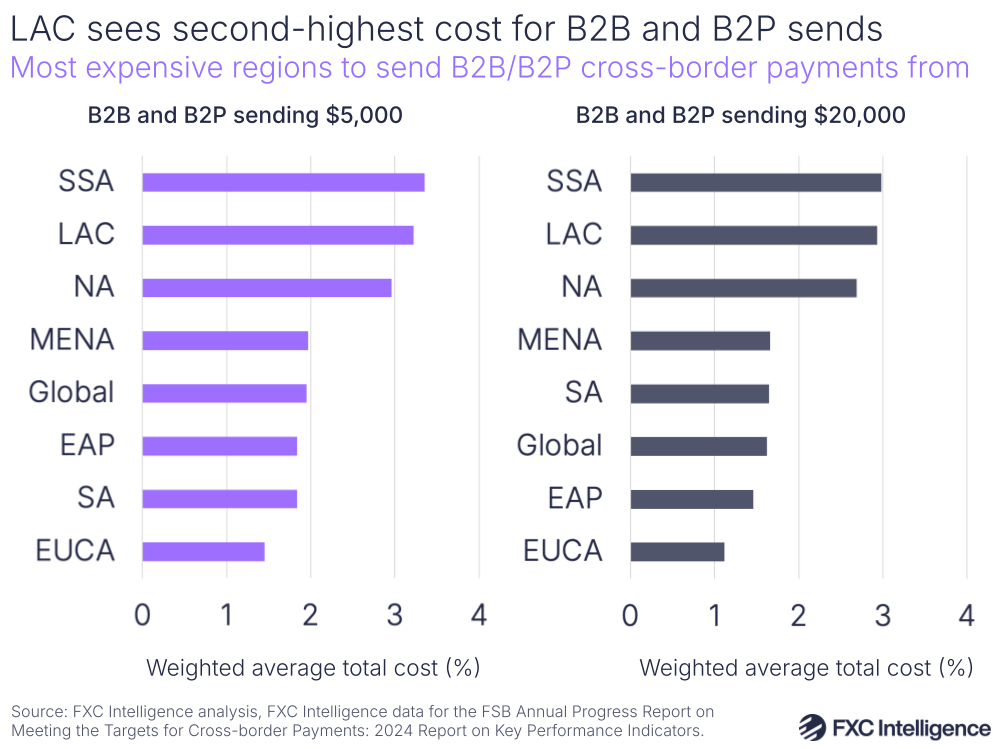

LAC sees high costs for B2B and B2P sends globally

LAC is also one of the most expensive regions to send B2B and B2P transfers from globally across both $5,000 and $20,000 transfers, behind Sub-Saharan Africa and ahead of North America. This highlights that there is still an opportunity to try and reduce the costs of transfers as growing businesses in the region look to make payments for imported goods or services from abroad.

On a corridor level, B2B and B2P transfers from LAC to other LAC countries see the highest costs globally across both of these send values, followed by transfers to EAP, EUCA, NA, MENA and finally SA (with the same ranking across both values).

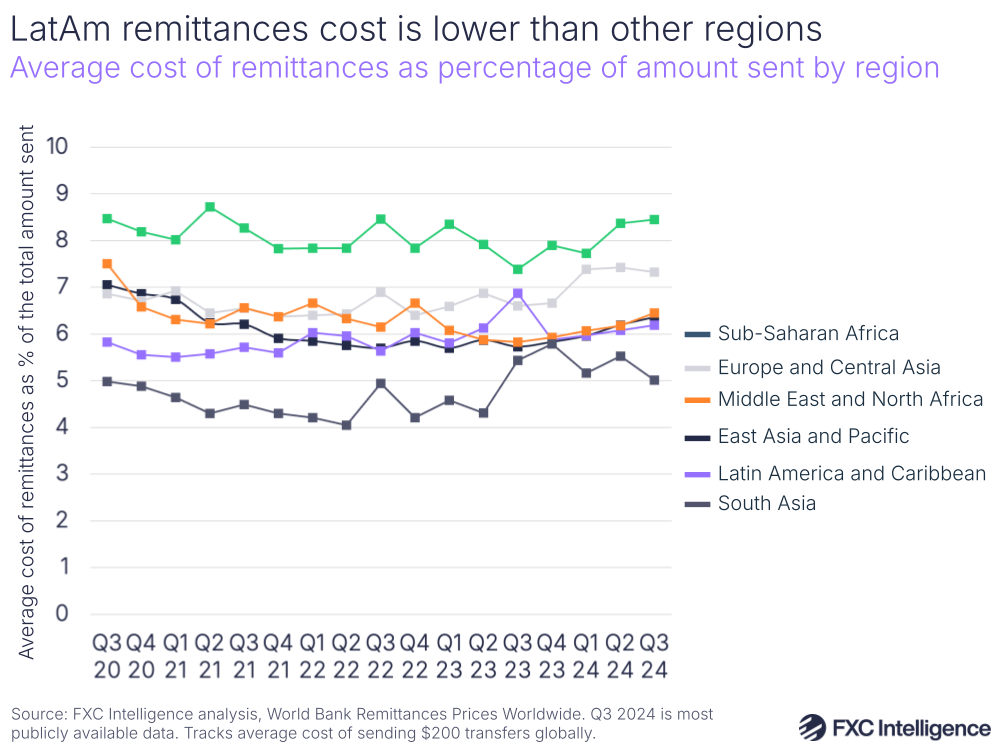

LAC remittance pricing is still well above UN goals

Separately, the FSB report also used the World Bank’s Remittances Prices Worldwide (RPW) dataset (which is powered by FXC Intelligence data) to assess the cost of remittances globally. On the pricing side, the most recent publicly available figures from the RPW data (up to Q3 2024) show that the average cost of sending $200 to the LAC region has declined from a peak of 6.87% in Q3 2023 to 6.19% in Q3 24, though this was a slight increase from Q2 24, as was Q2 from Q1 and Q1 from Q4 23.

Having said this, the cost of sending remittances to LAC in Q3 2024 was lower than other regions, particularly Sub-Saharan Africa (8.45%), Europe and Central Asia excluding Russia (7.33%), the Middle East and North Africa (6.45%) and East Asia and Pacific (6.36%). The cost of sending to LAC was also lower than the global average cost of 6.4%, though the cost across all regions is still higher than the UN’s 3% target.

Within LAC there is of course variation in cost depending on the country being sent to. For example, across the US-Mexico corridor, the average price of sending $200 in Q3 2024 was 4.94%, while the least costly corridors for transfers from the US were Ecuador, Honduras and El Salvador. The fact that pricing along these corridors is lower than elsewhere in the region is significant, particularly for countries like El Salvador and Honduras, whose GDP relies heavily on remittances.

A significant factor for pricing has also been the method used to make payments. According to the RPW, the average cost of sending $200 via cash gives a total cost of 6.45%, versus a total cost of 4.96% for digital services, reflecting a global trend of digitally funded transfers being cheaper than cash-funded. As more and more digital means of sending transfers to Latin America are being implemented, new startups launch and incumbent providers to the region transition to focusing more on digital, this could help bring the cost of remittances down.

Compare FX pricing across competitors in the space

Imports highlight Latin America’s payments potential

The growth of imports in Latin America (i.e. the value of all goods and other market services received from the rest of the world) has highlighted significant trends across key economies. The most recent World Bank data shows that between 2019 and 2023, LAC countries as a whole saw 28% growth in imports of goods and services to $1.8tn.

Imports in the region dipped in 2020 amidst the Covid-19 pandemic, but saw a sharp rebound in 2021 and 2022, while 2023 showed a slight decline or stabilisation, potentially due to macroeconomic impacts such as inflation and interest rate hikes.

Looking solely at the countries with the highest import values in 2023, Mexico (+31% since 2019), Argentina (+36%) and Brazil (+24%) had the most substantial growth, with Peru, Panama and the Dominican Republic also experiencing steady increases. Out of LAC total imports, Mexico held by far the highest share, with around 37% of total import values in 2023, with the next biggest countries being Brazil (19%), Chile (6%), Argentina and Colombia (5% apiece).

The impact of recent US tariffs on Mexico is forecast to affect exports from the country, particularly within its steel and auto parts industry. Having said that, a wider trend of imports growth in the LatAm region also means a higher number of global B2B payments, which in turn suggests importers are seeking out more efficient, low-cost and transparent cross-border payments solutions.

Prometeo’s Aleman says that one of the biggest pain points for her corporate customers is having visibility on cross-border payments. The company is trying to solve this with its recently launched Borderless Banking solution, which allows companies to access local accounts in countries across Latin America and the US and send and receive international payments.

“If we cannot perform the reconciliation, that’s not scalable for the customers because you cannot turn that payment rail into a payment method,” she says. “Perhaps you can use it if you have 200 payments received in a day, but if you have 6,000, it becomes unscalable. We provide the tools to make the payment flow, but at the same time we provide the tools to understand how the payment flows work and have visibility on the data point that those flows created.”

Migration drives remittances amid tough economic conditions

Migratory movements in Latin America have a significant impact on remittances, and this has shifted over time as a result of macroeconomic impacts and the Covid-19 pandemic. In particular, migration to destinations such as the US, Spain and other Latin American nations has historically driven higher remittance inflows, particularly to Mexico, Guatemala, Honduras and El Salvador.

Organisations such as the World Bank track net migration, which shows the difference between the number of people entering and leaving each country. A positive net migration rate suggests a population increase due to migration, while a negative migration rate indicates a decrease in population.

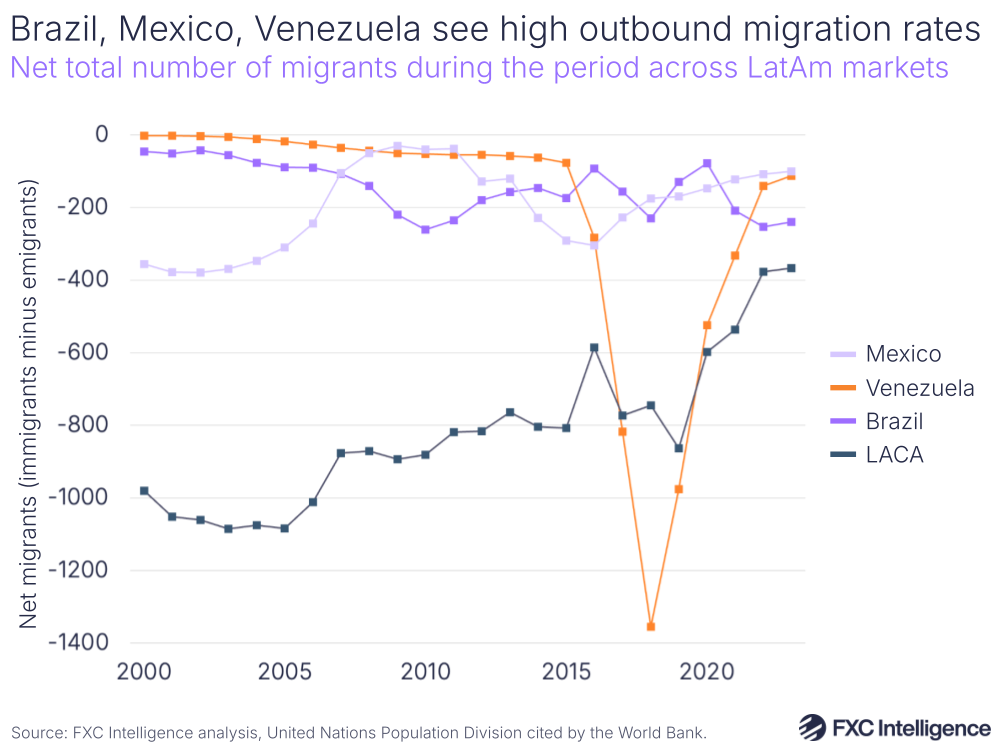

Across the LAC region in general, net migration to the region has varied, with some countries such as Venezuela and Haiti exhibiting significantly lower net migration rates. However, a number of countries saw positive net migration rates in 2023 (the most recent figure provided by the World Bank), such as Colombia, Chile, Peru, Puerto Rico and Panama. In addition to south-to-north migration, the region has also seen significant growth in intra-regional migration as the Venezuelan diaspora has migrated to other countries in the region, including Colombia, Peru, Chile, Ecuador and Brazil.

Venezuela is still in the midst of a political and economic crisis that has led to historically high migration levels. According to the International Organization for Migration, the number of Venezuelan migrants and refugees has risen from 700,000 in 2015 to 7.9 million as of December 2024. The departure of millions has led to significant rises in remittances to the country. In 2023, according to most recently reported data from Chainalysis and the Inter-American Dialogue, as cited by Bloomberg, Venezuelans received more than $5.4bn in remittances, up from $4.2bn in 2022.

For many countries in the region, remittances still form a substantial part of their GDP. Across LAC countries (not including Venezuela, which is not included in World Bank’s most recent figures), personal remittances took up the highest share of GDP for Nicaragua, Honduras, El Salvador, Guatemala and Haiti. Although these countries are not the biggest recipients of remittances in the region, they present a strong opportunity for money transfer providers.

Having said this, recent policy moves in the US could have an impact on immigrants, and therefore their contributions to cross-border money transfer flows in Latin America. For remittance providers operating in the region, this could signal a need to prepare for more volatility in the future, including through diversifying into different regions entirely.

Schedule a session with our team to discuss cross-border flows in Latin America.

What’s next for cross-border payments in Latin America?

Looking forward, there is still some work to be done from regulators and the market to maximise the potential of the cross-border payments market forward in Latin America.

As connectivity continues to grow in the region and digital payments spur the availability of ecommerce, it will continue to provide a major opportunity for global payments players. Having said this, the fragmented nature of Latin America’s payment ecosystem makes interoperability and a global goal of making cross-border payments better in the region more difficult.

For Prometeo’s Aleman, the continued focus on establishing strong payments infrastructure in the region that other companies can plug into is paramount. “It’s just the first layer,” she says. “On top of that, you will see a lot of progress. What we are seeing in the cross-border space is exactly this. We need cost-efficient rails. We need visibility. We need automation. But definitely on top of these rails, new things will come.”

Germer sees Latin America countries moving more towards the Brazil model, particularly when it comes to a move towards A2A payments across real-time rails. In this sense, open finance and Pix are applications that banks can build applications on top of. “In Brazil, because of Pix, banks are the main players of payments because the money goes directly out of a bank account to another bank account,” he says.

Within the stablecoin space, Ahmad believes the liquidity benefits of stablecoins will continue to drive businesses in the region towards using them for payments. He also says that USD stablecoins will maintain their dominance in the Latin America region, but the growth of local startups and companies will mean that local stablecoins such as BRL 1 (pegged to the Brazilian real) could eventually grow in importance.

“We’re seeing other geos develop their own local stablecoins,” he explains. “That will become a more and more dominant part of the stablecoin landscape, especially when it comes to things such as enabling people who don’t have a Mexico presence and cannot hold MXN otherwise to be able to participate in the Mexican economy through a Mexican stablecoin.”

Whether it’s in real-time payments or the development of new stablecoin rails, as the Latin America market continues to shift and cross-border payments providers seek out opportunities, the importance of understanding each country and market as its own individual landscape cannot be overstated. Within this space, providers will need to prioritise expanding their knowledge of each country through a mix of the right data and partnerships.