The strong digital performance of public money transfers players underscores the continued shift towards digital adoption in consumer money transfers and remittances. In this report, we explore what’s driving the shift, where cash still plays a role and key trends for the consumer money transfer space in the future.

The consumer money transfers industry presents a massive opportunity: a global TAM of $2tn in 2024 that will grow to $3.1tn by 2032, according to our market sizing data. A key growth driver for this industry has been a global push – led by digital disruptors in the space – to move consumer money transfers online.

Consumer money transfers, which covers both remittances sent by migrants and high-value consumer transfers, has seen major players emerge to service these needs with a focus on delivering faster, more convenient and less costly services via digital channels. However, in many places around the world, cash is still widely used and is still playing a major role in cross-border money movement.

This report evaluates the digital growth amongst key publicly traded transfer players in the consumer money transfers space, from historically retail-focused players Western Union and Intermex to Euronet’s global money transfer segment (containing Ria and Xe) and digital challengers such as Remitly and Wise – the latter of which has increasingly focused on larger-value consumer money transfers. It also explores the role cash continues to play in remittances and money transfers, as well as providing key insights about future trends in the space.

Digital drives growth across major money transfer platforms

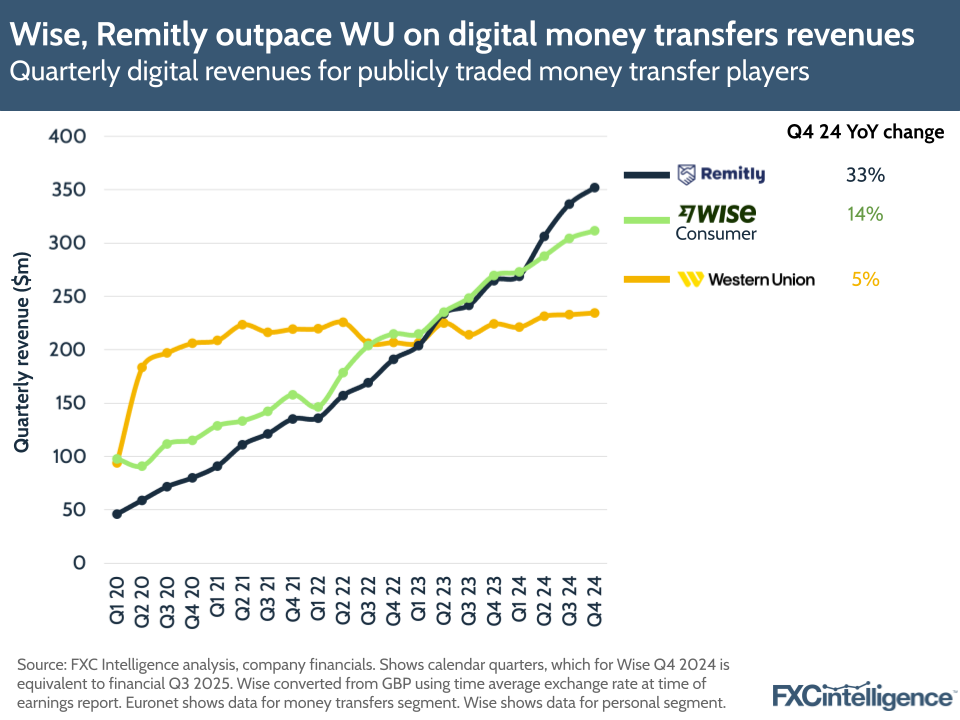

The growth of digital transfers across publicly traded providers continued to grow in 2024, and is likely to continue to be a key driver in upcoming Q1 results.

Across players that report this metric, fully digital Remitly saw the highest YoY growth in digital remittances revenues at 33% in Q4 2024 YoY, versus 14% growth for Wise’s Consumer segment. Meanwhile, Western Union, which has only more recently shifted its focus to digital, saw slower growth at 7%.

Elsewhere, Euronet reported that its money transfer segment saw 33% growth in direct-to-consumer digital transactions, with online-only money transfer provider Xe seeing 8% growth.

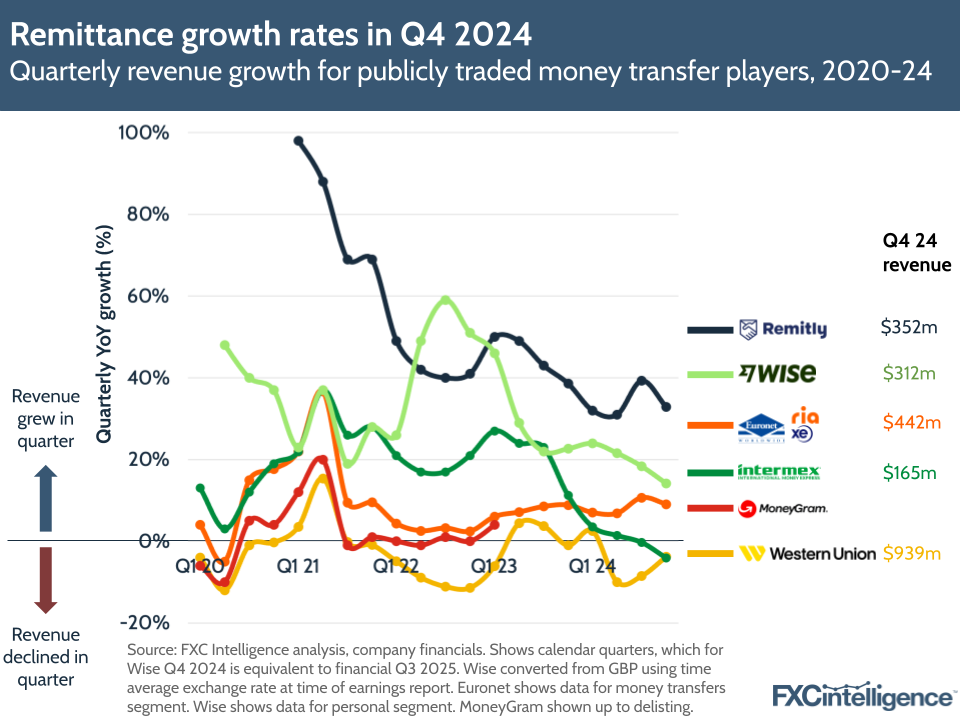

Within the wider context of these companies’ total revenues, Remitly and Wise’s growth over Western Union and Intermex speaks to the growing demand for digital disruptors in money transfers. Western Union remains the biggest player in the C2C space in terms of revenue, with $939m in Q4 24, but it also saw its revenue decline over the course of 2024, with all quarters except for Q1 being lower YoY. The company attributed numerous macro conditions to this drop, including the disruption of migration flows among LatAm countries.

Meanwhile, Intermex also saw a -4% decline in revenues in Q4 2024, driving flat growth for the full year.

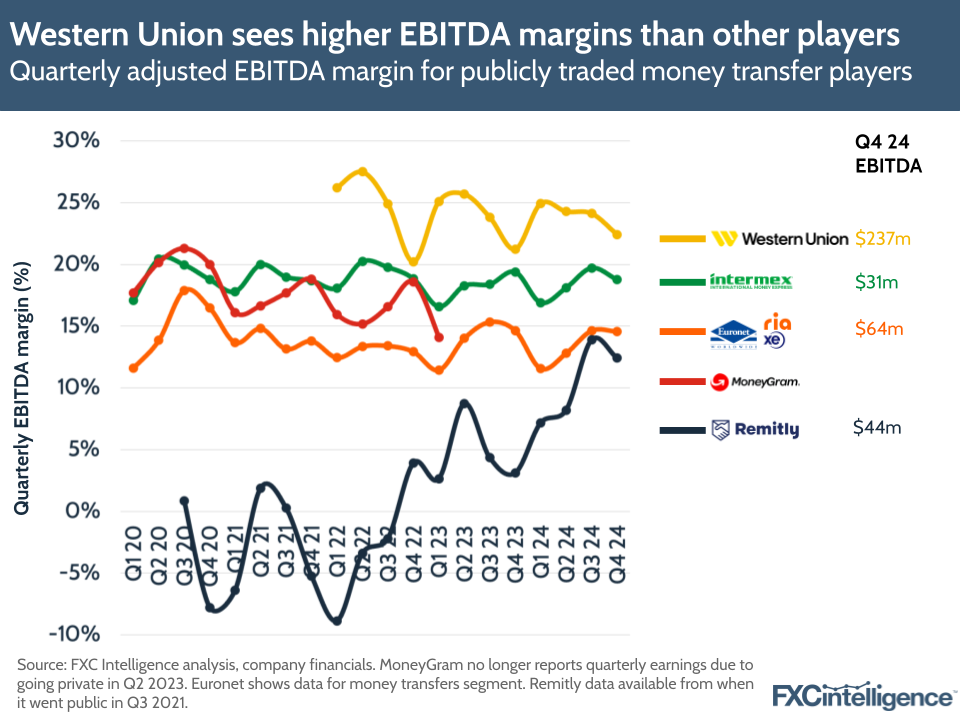

Despite both companies seeing a quarter-on-quarter dip in their EBITDA margins in Q4 2024, Western Union and Intermex continued to see higher EBITDA margins than Remitly during this quarter, indicating that despite macro conditions affecting growth, these companies are still managing to maintain operational efficiency. Having said this, Remitly has broken considerable ground in this metric over the past two years, having seen its first net profit in Q3 2024 and a 203% YoY rise in its EBITDA over FY 2024.

The crux of these results is that consumers are continuing to gravitate towards and reward the delivery of digital consumer money transfer services, which are seeing faster revenue growth than incumbents as a result.

Both Western Union and Intermex are directing more energy towards supporting digital growth, however. Western Union said it had seen the seventh consecutive quarter of double-digit transaction growth in its branded digital business in Q4 2024 and, during its Q4 earnings call, the company said it is continuing to expand its digital wallet to more locations and bolstering transactions through its acquisition of Singaporean mobile wallet Dash.

Meanwhile, Intermex, which has seen significant disruption to revenue growth due to a slowdown in its target market, is shifting its retail focus to drive more investment in digital. In its Q4 results, Intermex shared that digitally originated transactions had grown by 72%, versus a -3% decline in transactions for the business in the same period. However, this still only made up about 5% of the company’s transactions, and Intermex still sees retail as being its key driver for the time being.

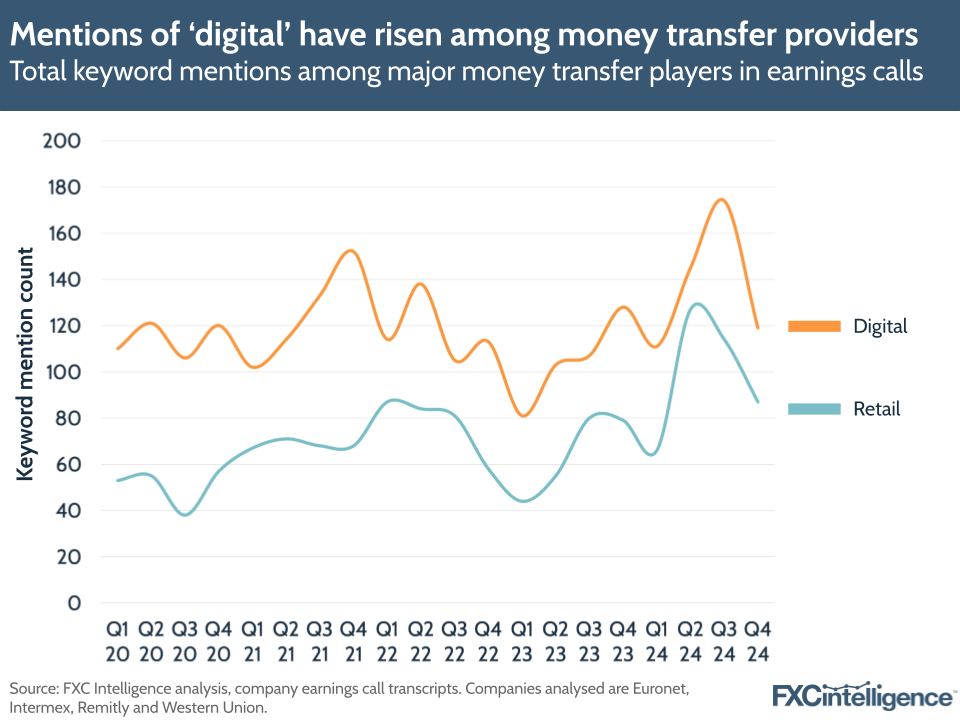

Reflecting this, we’re seeing more discussions around digital money transfers in earnings calls. The number of times the word “digital” was used during the earnings calls for Western Union, Remitly, Euronet and Intermex declined by -7% YoY to 119 for Q4 2024, but was up by 31% to 549 across 2024 in entirety. The vast majority of these mentions over the course of the year (73%) were made by Intermex and Western Union, highlighting the growing importance of digital to their strategy.

By comparison, mentions of “retail” (including the word “retailer”) across all the providers grew by 53% YoY in 2024, faster than digital, though with less overall frequency – at 394 times. This is unsurprising, as a significant portion of Western Union and Intermex’s business occurs through retail agents and will continue to form an important part of their business going forward.

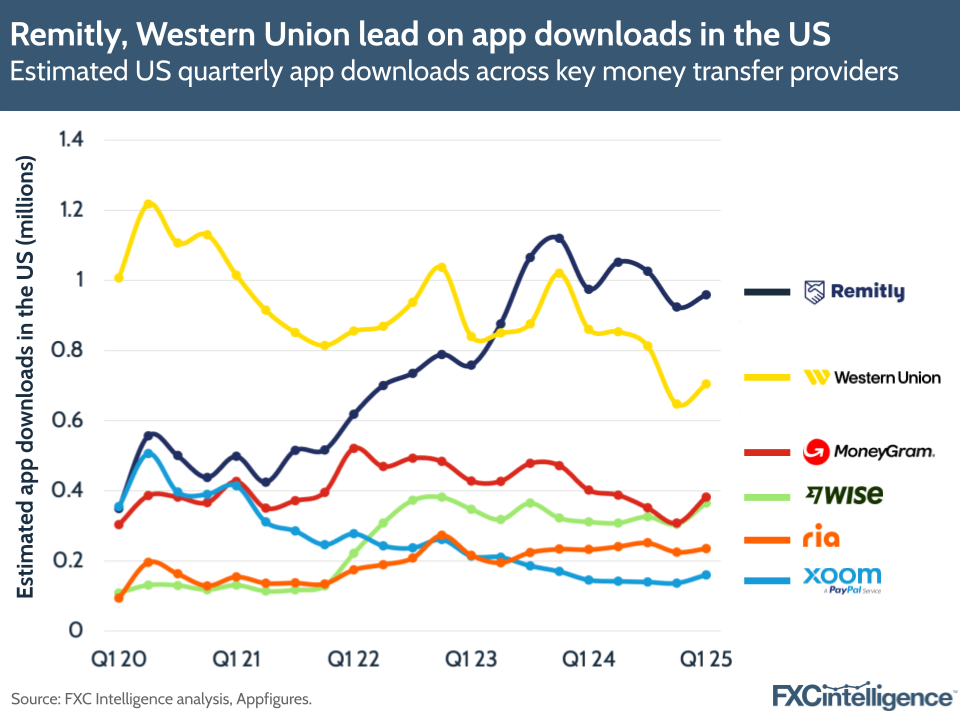

Remitly outpaces traditional players on app downloads

In remittances, users are increasingly moving from cash-based outlets to digital pay-in methods such as through mobile apps and websites, which is reflected in their use of such products.

Estimated data supplied by Appfigures for app downloads in the US across Western Union, MoneyGram, Wise, Ria and Xoom provides some key insights into digital engagement across key players.

Remitly has seen significant growth in the number of downloads for its mobile app across iOS and Android compared to others over time, with almost a million downloads in Q1 2025. The company overtook Western Union on the number of quarterly combined app downloads in Q2 2023 and saw the highest number of app downloads in 2024 overall at 4 million, followed by Western Union (3.2 million), MoneyGram (1.4 million), Wise (1.3 million), Ria (951,000) and Xoom (566,000).

In particular, the difference between Remitly and Western Union in terms of quarterly app downloads and how these have grown over time speaks more to how the former is positioning itself in the market. Though Western Union is a far more established brand, Remitly is a digital-first player that has seen solid customer reviews for its app, driving strong word-of-mouth marketing that is complementing its targeted campaigns.

Though some providers have seen significant growth in the number of app downloads in 2024 compared to 2020 – most significantly Wise, Remitly and Ria – several have seen this figure decline since then, including Xoom and Western Union. However, all six of these providers saw an uptick in downloads in Q2 2020, which is likely to have been prompted by a wider move to digital payments methods as a result of the Covid-19 pandemic.

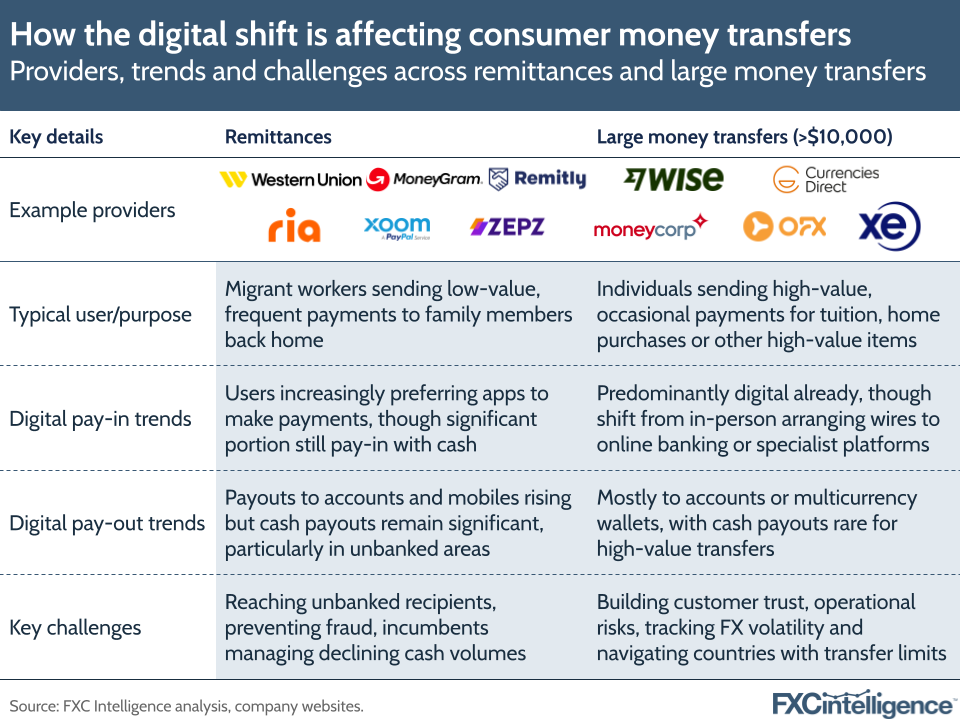

How the digital shift affects remittances versus larger transfers

A number of factors have been driving a shift for consumers to move transfers to online over the last five years. For example, new digital platforms and services building traction, particularly in regions where access to banks is harder; the convenience, speed and safety of digital for consumer money transfers; and digitalisation receiving a boost due to the Covid-19 pandemic, which made it more necessary for consumers to make payments digitally/remotely.

However, the move to digital is split depending on the actual purpose and size of the money being transmitted. On the one hand, there are remittances, which tend to be primarily driven by migrant workers sending lower value, frequent payments to family and friends back home. According to the UN, on average migrant workers send between $200 and $300 every one or two months. On the other hand, there are larger consumer money transfers, which tend to be higher value, more occasional payments, typically amounting to tens of thousands of dollars and occurring as a one-off or yearly payment.

These different payout types are seeing a different kind of shift over time. On the remittances side, digital pay-ins have seen a rapid shift to digital, with senders increasingly preferring to use apps and online payment methods to make pay-ins as these have become a less costly way to send money. Many providers also enable money to be sent directly into recipients’ bank or mobile wallets or to prepaid debit cards, allowing recipients to access money electronically.

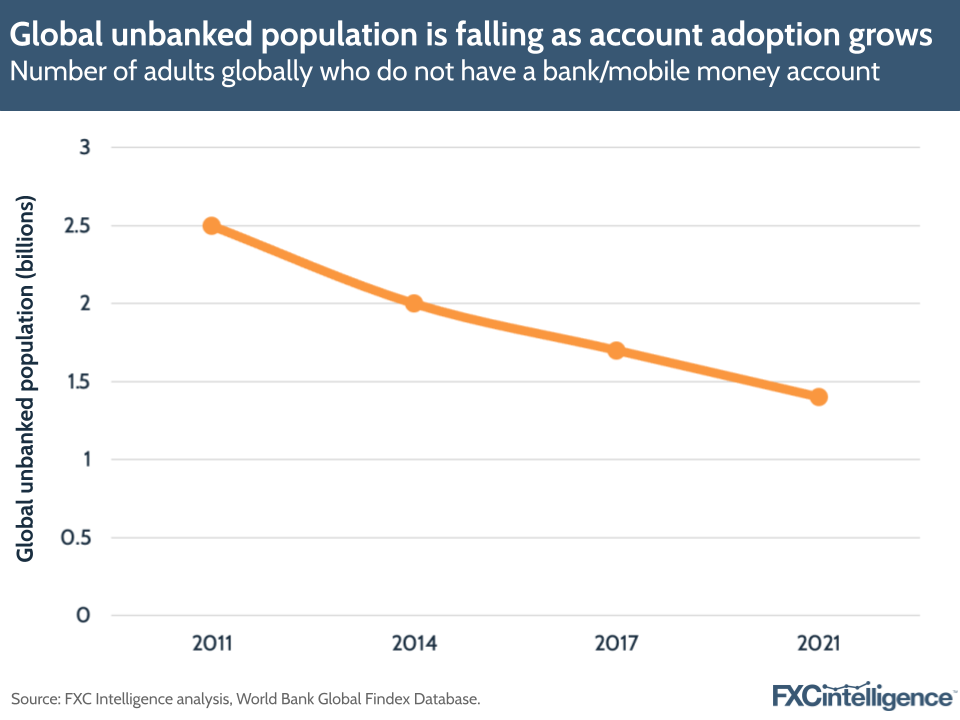

Having said this, remittance transfers still often involve cash at one or both ends, with this being prompted in some countries by a lack of financial inclusion. According to the World Bank’s Global Findex, most recently published study in 2021, global financial account ownership rose from 51% of adults in 2011 to 76% in 2021, though this still left 1.4 billion unbanked adults. This is why it has been necessary for major remittance providers to continue to service cash payouts across a network of retail agents globally.

On the larger consumer money transfer side, the digital shift in recent years has been less about moving from cash to digital methods and more about a shift in the types of platforms being used. Previously, such payments would be handled through bank wires but they are now being increasingly initiated through online banking or specialised fintech providers such as Wise, with payouts more often going to bank accounts or alternatively to multicurrency accounts.

In this sense, the disruption of digital payments players is having an impact both on the remittances space and on larger consumer money transfers, and banks and traditionally retail-led incumbents are therefore pushing to respond to remain competitive in the market (banks have seen varying levels of success with this, as we saw in our report on Zing’s closure earlier this year).

Where is cash continuing to play a role in remittances?

Though it is starting to shift in some developing countries, access to banking services or online financial services or digital payments infrastructure can be more limited. This means that in these countries, many consumers are continuing to provide or receive cash at physical locations, or using informal remittances networks.

Growing digital connectivity in regions is expected to help empower mobile banking services. This a key topic for our recent report on cross-border payments in Latin America, which sees vastly differing use of digital payment services in some countries.

Some countries in Asia have seen a major shift in the way they handle remittances due to the rapid growth of digital wallets, with this having a direct impact on livelihoods. For example, the World Bank’s Global Findex report for 2021 found that in Bangladesh, poor rural households with family members who migrated to the city received higher remittance payments when they had a mobile money account, allowing them to spend more on food and other items.

However, the same study found that globally, 12% of unbanked adults – about 165 million people – receive private sector wage payments in cash, highlighting that it continues to be an important payment instrument in countries worldwide.

Moreover, in 2021, the share of adults making or receiving digital payments in developing economies was 57%, compared to 95% in high-income economies. The developing economies figure had risen from 35% of adults in 2014 and could increase further in updated Global Findex results from the World Bank, expected later this year.

Having said this, the propensity of a significant proportion of the world’s population to make non-digital payments, combined with the fact that many are still unbanked, highlights that cash will continue to play an important role in how consumers tend to make payments over time.

The future of money transfers

Despite the continued presence of cash, the consumer money transfers market has undergone significant change as new digital platforms have emerged to compete with banks and provide faster, less costly and more convenient payments.

In the future, it is likely that this trend will continue as more and more consumers adopt mobile payments solutions and digital connectivity and payments infrastructure solutions improve globally. The latter of these takes time, and in the meantime mobile money solutions such as Kenya’s M-Pesa or GCash in the Philippines could continue to help drive financial inclusion in their respective countries.

Governments worldwide are continuing to introduce initiatives to regulate fees and make prices more transparent. The G20 has been working towards its goal of reducing remittance fees to below 3% of total transaction amounts – however across both remittances as well as larger consumer money transfers (the latter was discussed in our analysis of the FSB’s KPIs for the G20’s roadmap last year), there is still some way to go for countries to reduce the price of money transfers.

Various countries are employing a mix of solutions to do this, including investing in central bank digital currency (CBDC) projects; launching initiatives to boost the attractiveness of digital transfers; launching bilateral networks to sync up international payment networks (as seen across numerous countries in Southeast Asia); or even partnering directly with banks and fintechs to launch their own cross-border payments solutions.

Another macro development has been the impact of market turmoil, spotlighted by recent events in the US. As discussed in our wider piece on the recent tariffs’ cross-border impact, remittances and high-value consumer money transfers could see a minimal impact from this as tariffs aren’t being placed directly on consumers or service providers (i.e. money transfer companies). However, there could be knock-on effects – i.e. consumers having less money to send overseas, or currency volatility across some corridors leading to lower flows.

Amid this environment, the continued growth of digital players in the space – as well as the continued growth of digital within traditional providers – is likely to be a major narrative for 2025.