With new regional regulations inbound and a wave of open banking partnerships in the payments space recently, we examine the topic of open banking to find out more about the impact it is having on cross-border payments.

Open banking has been an influential topic in the European fintech space for several years, and is already powering account-to-account (A2A) payments across finance and retail applications. Now, other regions around the world are beginning to explore regulation to help push forward the concept to meet demand for faster, more convenient payments.

Advocates of open banking say that it is transforming the way consumers make payments and could help eliminate the challenges currently faced in the cross-border space – namely payments being too slow, costly and not transparent enough. More and more providers are offering ‘Pay by Bank’ services, while major payments players such as Visa and Mastercard are making acquisitions to introduce open banking into their offerings.

This report explores in closer detail how open banking is affecting the cross-border space, how countries around the world are responding to it and whether A2A open banking payments could become the norm in the future.

What is open banking?

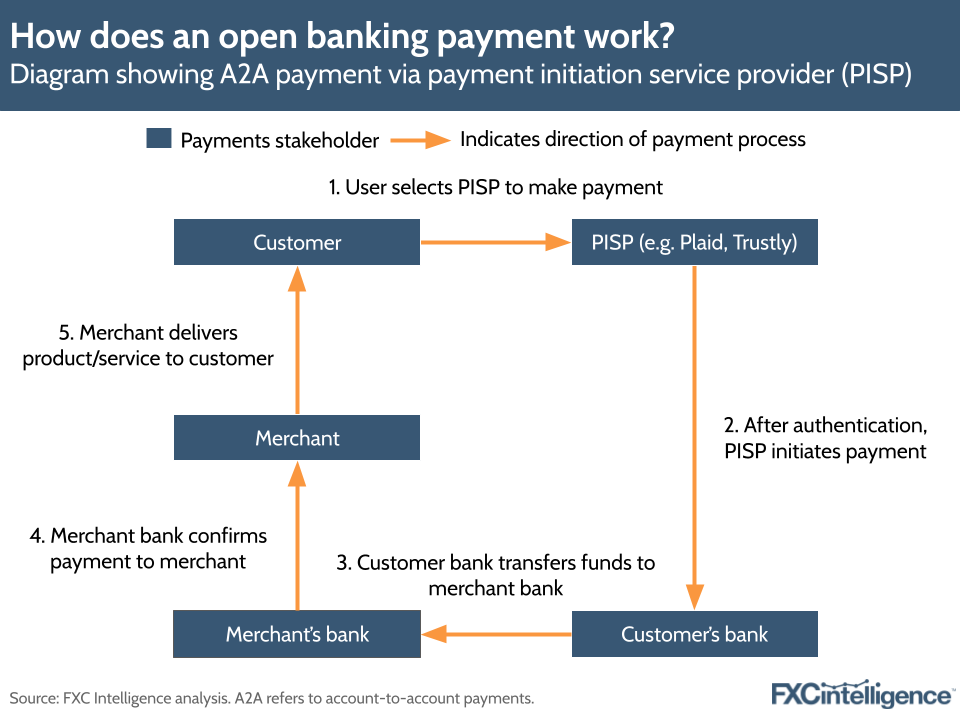

Open banking refers to the concept of banks and other financial institutions making their customers’ financial data open and available for other regulated third-party providers to use and, in some cases, facilitate payments. They do this using an application programming interface (API), which draws out the financial data that’s relevant to the task being performed (with the bank account holder’s permission).

The concept of open banking saw particularly strong development in the UK and Europe in the 2010s. For example, in 2017 the UK’s Competition and Markets Authority (CMA) ordered nine of the country’s largest banks (including HSBC UK, Lloyds, Santander, Barclays and NatWest) to open up access to their customer data using secure protocols.

This was followed by the EU’s Payment Services Directive 2 (PSD2) coming into effect in 2018 (having been passed by the Council of the EU in 2015). PSD2 required banks in the EU to make their data available to third parties (and is set to be updated with a new version, PSD3, by 2026).

Under Europe’s PSD2 framework, regulated third-party providers are split into account information services providers (AISPs) and payment initiation services providers (PISP). The former can access and present read-only financial information, but can’t actively initiate payments, while the latter is able to both present the information and move money from a user’s bank account.

In the years since, open banking has been applied for all manner of purposes, but one of the big ones is A2A payments. For example, remittances player Wise enables users to transfer money to others or add money to their Wise account directly from their bank account, without requiring the user to login to their bank (though they may be required to carry out a 2-factor authentication), creating a more frictionless payment without the use of cards.

Now, countries across Europe, the Americas and the APAC region are introducing open banking regulation and initiatives to drive forward the concept.

What are the benefits of open banking for cross-border payments?

Advocates for the use of open banking say they could help make cross-border payments faster, more cost-effective and more efficient. The means by which it does so range from reducing the number of middlemen involved in a transaction to promoting greater competition between payments players.

Eliminating the need for intermediaries

Normally, payments made via card or direct debit require going through many intermediaries (for example payment processors, payment gateways), each of which has their own processes, take their own fees and have their own potential to create errors that can delay payments.

Because open banking enables money to be transferred directly between accounts, payments are faster but also less costly for merchants, as fewer companies along the way are taking a cut for their role in the payment.

“Traditional cross-border transactions often involve multiple intermediaries and fee-laden pay-in payment methods, leading to higher fees for consumers,” says Brian Dammeir, Head of Europe at Plaid. “Open APIs enable direct account-to-account transfers, bypassing these middlemen and offering consumers more competitive rates.”

Beyond standard payment rails, open banking enables real-time access to customer information for real-time settlement schemes, such as SEPA instant credit transfers. “This eliminates delays associated with traditional verification processes, leading to faster settlements for cross-border transactions,” adds Dammeir.

Making payments more traceable and secure

Transparency has been an important watchword in cross-border transactions. Payments that move through correspondent banking networks with multiple intermediaries can be hard to trace, making it difficult to work out when payments will arrive.

This is a challenge for consumers but also for businesses, particularly if they are relying on cash flow coming in on a certain date. Proponents of open banking say that it enables real-time payment monitoring to ensure transactions have occurred properly.

Open banking payments also integrate strong authentication methods, which Dammeir says helps “reduces operational burden” for cross-border payment providers. One example of this is Strong Customer Authentication (SCA), a set of regulatory requirements that was introduced by Europe’s PSD2 guidelines and requires two-factor authentication for customers when making purchases online, as opposed to previously where banks were only able to ask for a static password to confirm the identity of the payer.

Open banking payments are built to incorporate SCA verification, but because they don’t require intermediaries (i.e. cards) and enable payments directly between bank accounts through regulated third-party providers, the process can be faster and with fewer steps involved than with card-based payments, while still adhering to SCA rules.

Encouraging competition in the industry

Open banking payments, advocates say, create more secure, less costly and convenient customer payment experiences – this also creates a more competitive and innovative environment in the payments market.

In particular, because open banking acts as a potential competitor to card networks, this in turn can spur more competitive exchange rates and fees amongst payment providers.

This has been a key part of the EU’s introduction of new regulations to support the development of open banking – driving greater competition amongst both incumbent and new payments players, as well as making payment infrastructure more accessible to new challengers.

How do open banking providers enable cross-border payments?

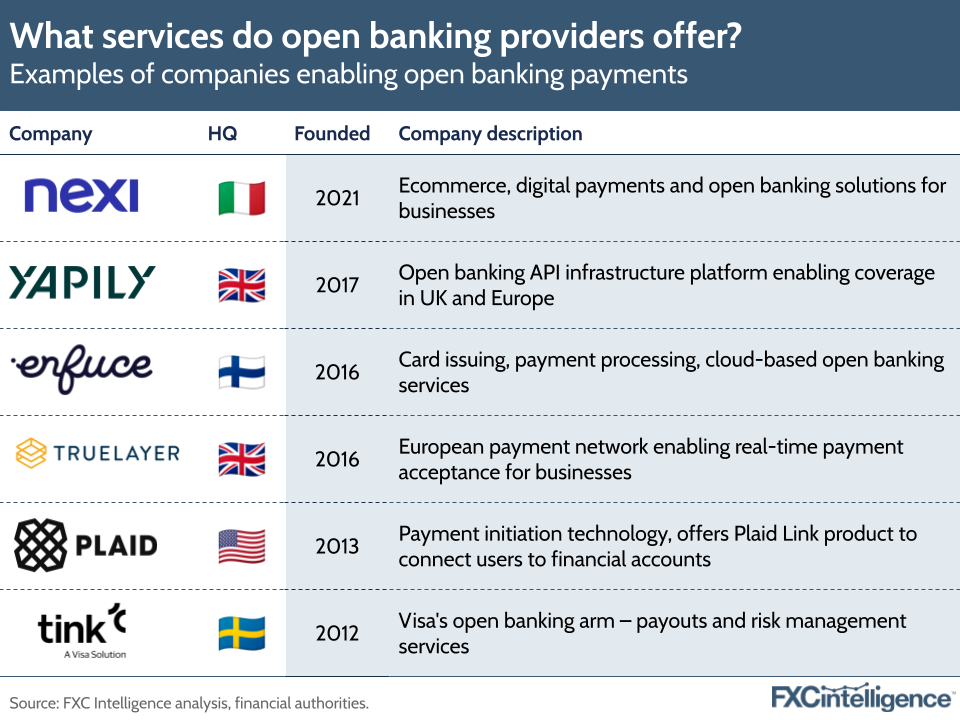

Key players in the market deliver open APIs that enable payments using open banking. For example, as part of its offering, Plaid provides an API to merchants that allows users to authenticate payments directly through their bank via another app – for merchants, this reduces the costs that would usually be incurred for receiving payments from networks and acquirers.

As we found with our analysis of Swift’s migration to ISO 20022, legacy infrastructure remains a problem for many financial institutions, particularly due to the risks and costs that may come with moving to a new system and integrating with open APIs.

Third-party companies such as Tink (now owned by Visa) have emerged to help solve this issue by providing their own technology to enable data sharing. By partnering with fintechs, banks are able to overcome many of the challenges from outdated systems and infrastructure.

There have already been several open banking developments that are relevant for cross-border payments this year, with some of these being acquisition-related. For example, Visa launched its new Open Banking product in April, which it has been developing since it completed its €1.8bn acquisition of Tink in 2022, and is now allowing users in the US to connect accounts and provide parties with access to financial data.

This comes after Tink signed deals with companies including Adyen and Revolut to enable European open banking payments, as well as several merchant-facing banks and fintechs such as Capital One and Fiserv.

Meanwhile, Mastercard’s open banking solution is built on Aiia, a company that the business acquired in 2021 and which now enables companies to connect their apps to financial data provided by more than 3,000 European banks to enable payments. In March, Italian bank Nexi partnered with Mastercard to use its open banking platform to enable ecommerce payments for Europe-based merchants in Nexi’s network.

Open banking solutions have also enabled money transfer partnerships. For example, Wise’s Open API product allows other companies (such as N26 or Monzo) to provide low-cost international transfers through its network.

Radha Suvarna, Chief Product Officer, Payments at Finastra, explains how Finastra is helping drive financial inclusion by onboarding cross-border payments providers onto its platform and pre-integrating them with its payment solutions through open APIs.

“Our partnerships with Visa, Mastercard and Thunes, for example, are making cross-border payments more cost-effective than the incumbent solutions,” says Suvarna. “This enables our customers to offer new, faster, more affordable solutions to their clients.”

The shift to provide more seamless open banking payments is, in some cases, being driven by banks themselves. UK-based Standard Chartered recently launched an Open Banking Marketplace, through which it allows companies (for example, fintechs or ecommerce players) to experiment with different open banking APIs, including those that are designed to allow cross-border payment companies to provide FX quotes and enable overseas payments.

For some time now, fintechs have been disrupting traditional cross-border payments operations by providing more agile, responsive and customer-friendly payments experiences at lower costs, Suvarna explains. However, an “open partner ecosystem” could help make cross-border payments more accessible, transparent and cost-effective, enabling banks and credit unions to remain competitive.

“While Swift will continue to be very important and relevant for many use cases around high-value transactions, there are a number of alternate cross-border capabilities that are emerging that provide an alternative, particularly for low-value transactions,” he adds. “We believe these solutions will continue to scale through direct-to-client as well as bank distribution channels.

“These will enable the financial institutions to provide optionality and better value to their clients depending on the use case, without taking on the complexity and cost of correspondent banking, and while protecting their client relationships and driving cross-border payments as a significant profit and growth centre.”

Access our FX pricing data to compare cross-border payments providers

How are cross-border payments companies talking about open banking?

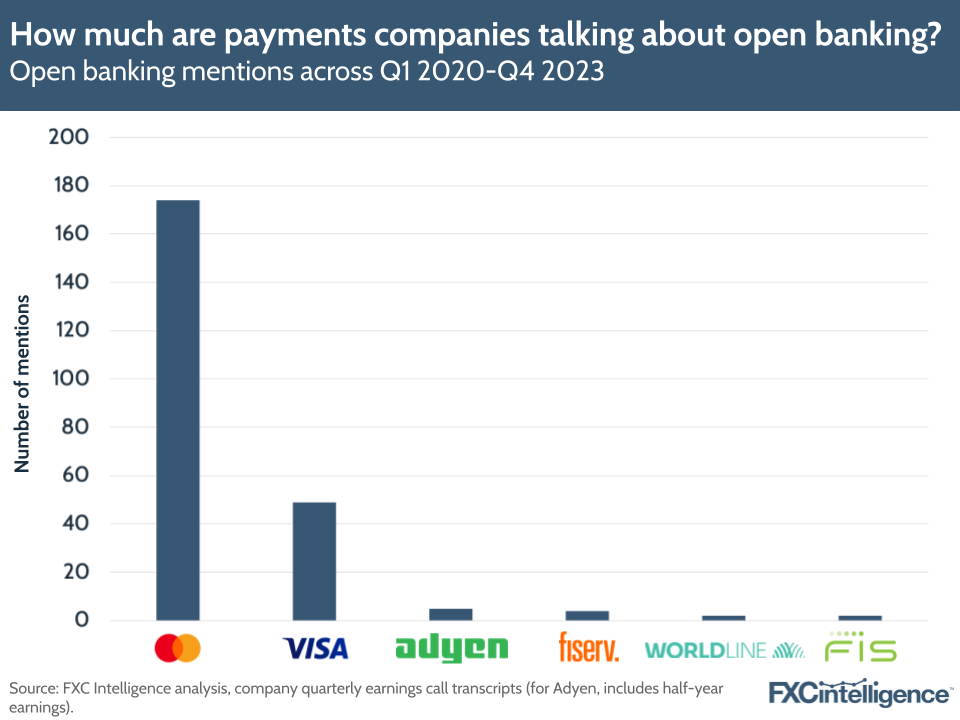

Looking at how public companies in the cross-border payments space are talking about open banking in earnings calls, the concept has only been actively mentioned a handful of times by some companies over the last few years.

Among the companies we track, the term “open banking” has appeared most frequently in calls led by Visa and Mastercard, with the latter seeing the term mentioned over 170 times in calls since the start of 2020.

In one of its most recent calls, Mastercard talked about the potential of its open banking solutions to tie in with real-time payment systems such as FedNow, Pix and UPI. The company has also launched an open-banking subscriptions management tool that banks can plug into their apps and earlier this year launched a programme that uses open banking to streamline account opening for some of its US products.

Visa and Mastercard’s interest in open banking has led to speculation about whether the companies may see open banking payments as an eventual threat to their card payment businesses. With open banking potentially eliminating intermediaries in the payment process, this also has an impact on card processing fees.

For a similar reason, some financial institutions – particularly in the US – have been resistant to open banking, which is making the financial space more competitive but also drawing consumers to alternative digital challengers that, in turn, affect the amount of money from fees that incumbent institutions may accrue as a result.

James Booth, Head of Partnerships at digital payments platform PPRO, says that open banking is not yet a major driving force for cross-border traffic. However, it does provide new user-friendly payment schemes that meet consumers’ requirements, impacting conversion success rates and cross-border customer loyalty.

“I believe that open banking is still in its infancy and as it matures, it will eventually be a part of our everyday lives,” says Booth. “It will become an invisible utility behind most of the applications and services that we use today.”

Jonathan Vaux, Head of Proposition and Partnerships at processor Thredd, agrees that the cross-border payments space in the UK hasn’t been as heavily impacted by open banking payments, but in Europe there may have been more of an impact. “While within one region, the Eurozone still has very fragmented domestic payment systems, so there may be more of an opportunity for open banking to help relieve some of the challenges,” he says.

How are countries around the world supporting open banking?

Open banking is facing a number of challenges – in particular, a lack of standardisation across APIs can make projects to implement them more costly and difficult, which somewhat negates the benefits of open banking (i.e. reducing cost). As with all data sharing – but particularly with sensitive financial data – there is also a need for consumer data to be shared by banks with third-party providers in a safe and responsible way.

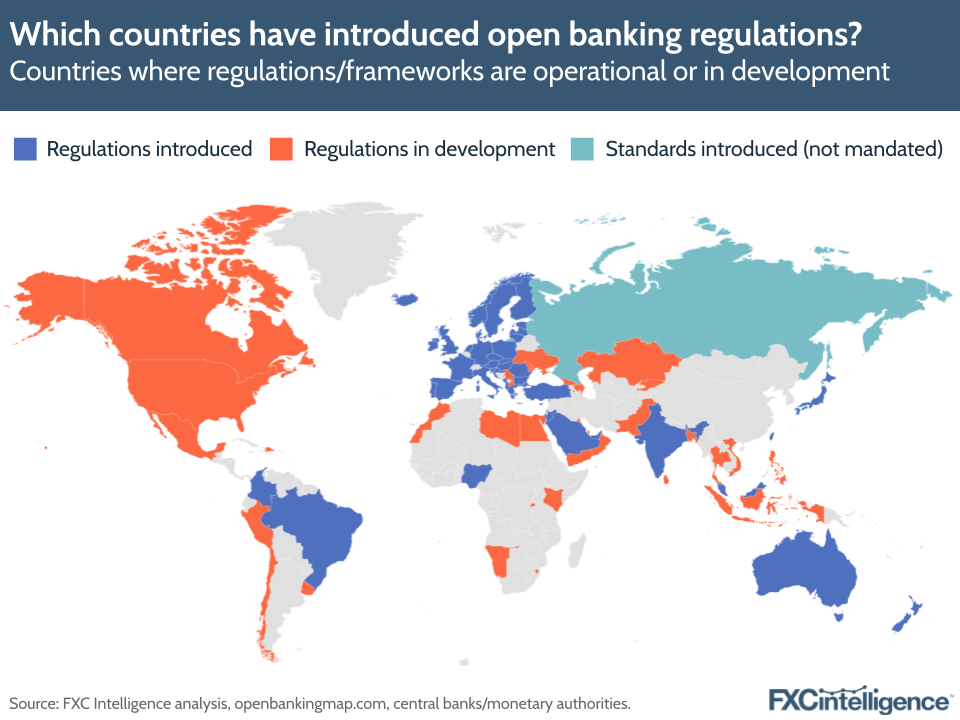

For these reasons, a number of countries worldwide are adopting regulatory standards in order to support the development of open banking, as well as make the payments space more accessible for fintechs.

Our analysis found that countries fit into a number of categories when it came to implementing rules around open banking – the concept of banks sharing customer’s financial data (with their consent) to third parties. In some cases, such as the EU, banks have already been mandated to share their data, while other markets – like the US – are still developing regulations.

There are more than 80 countries worldwide that clearly state they have either implemented regulations or a specific framework for open banking, or are currently in the process of developing regulations or a framework. Having said this, in many countries open banking is still very much driven by the market – i.e. banks in those countries are introducing their own API-based collaborations with payment providers in the absence of directives.

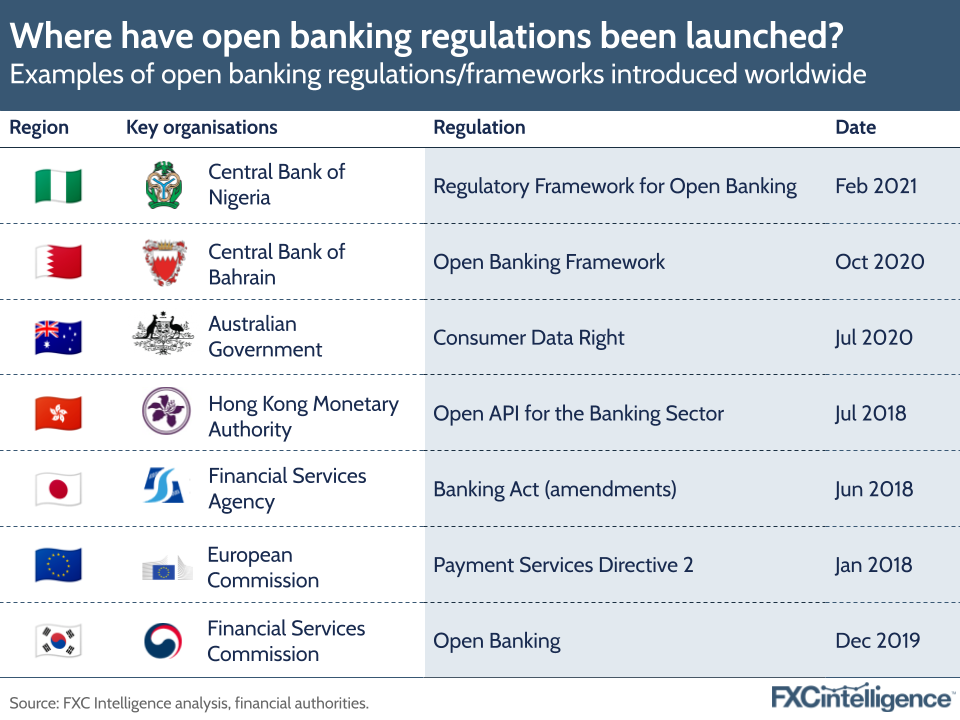

Some countries have already seen legislation introduced to provide a framework for open banking, and in some cases compel banks to open up access of financial data for third parties through open APIs, such as in Europe through PSD2.

Meanwhile, Australia has required banks in the country to participate in the Consumer Data Right, a legislative framework for how consumer data may be used, with this being rolled out in phases (beginning with the banking sector in 2020).

On the other hand, in some cases open banking is still being driven by companies within the financial market, often with the support of central banks. The central bank of South Africa, for example, has been exploring the potential impact of open banking, but it is still led by banks bringing out their own solutions – examples of this can be further seen in South Africa’s instant payment service PayShap and India’s UPI, which is regulated by the Reserve Bank of India but run by a non-profit company, NPCI.

Tracking the growth of open banking payments

All this raises the question of how well open banking payments are currently growing, particularly when compared to existing card methods.

Looking specifically at the UK – one of the earlier adopters of open banking regulation – demand for open banking payments has been rising recently. Open Banking Limited – an organisation set up by the CMA to create technology and set data standards for open banking in the UK – has been tracking open API usage across nine open banking providers and 20 brands since November 2022.

According to the organisation’s most recent figures, the total number of successful open banking payments in March 2024 for these providers rose about 70% YoY to 16.3 million, with 14.8 million (over 91% of the total) being single domestic payments and the remainder being variable recurring payments. In addition, the number of user connections to PISPs specifically (i.e. including users who may use multiple banks) rose by more than 151% YoY in March 2024.

These figures show how open banking use has increased across many providers in the UK, but it’s important to note that they don’t give a complete sense of how open banking currently competes with the cards in the country.

For example, according to the most recent figures from trade association UK Finance, there were 1.93 billion debit and credit card transactions made in the UK in January 2024 (an increase of 2.6%) while Open Banking Limited’s figures show that 13.3 million successful single domestic payments occurred during the same period across its selected dataset. Meanwhile, UK Finance claims that their data covers over 97% of the total credit card market, which is therefore a more complete picture of payments across the country.

While open banking data is more readily available in the UK, where regulation is driving and tracking open banking, it is harder to find reliable sources to demonstrate the progress of open banking in countries like the US and China, where the concept hasn’t seen the same level of regulatory control so far.

This could change soon in the US, which had seen intent to regulate open banking as early as 2010, when US Congress included a provision in its Consumer Financial Protection Act requiring the Consumer Financial Protection Bureau (CFPB) to prepare rules around financial data sharing. However, since then, there has been no clear regulatory framework for open banking and it was only in June 2023 the CFPB unveiled plans for open banking regulations in a bid to encourage competition. At the time, CFPB estimated that at least 100 million consumers share their banking data with third parties, as a number of banks and fintech partners have already begun forming data sharing partnerships.

In some countries open banking applications are contributing to a shift in the way payments are made. For example, India’s UPI – through which users can use QR codes or a pin to transfer money and make payments – was used to make more than 117.6 billion transactions in 2023, and has significantly eaten into the use of debit card payments in the country. However, as discussed in our QR code report earlier this year, in other countries NFC technology (which enables contactless payments through digital wallets such as Apple Pay) has been more popular.

By comparison, Visa and Mastercard’s massive global networks both process trillions of dollars worth of payments annually across billions of transactions, many of which are card payments made across borders. However, both companies acknowledge the importance of open banking for payments. For example, in a 2023 report, Visa discussed that its own consumer survey found that 87% of US consumers use open banking.

Both companies’ interest in the open banking space shows that the concept is on their radar, and it will be interesting to see whether they make further acquisitions and inroads into the space in the future.

How do Visa and Mastercard compare on cross-border pricing?

How will open banking change in the future?

Open banking is set to see more regulation going forward as countries seek to encourage competition within their markets, with benefits trickling down to consumers.

“We continue to see regulations and standards around open banking evolve in a positive way,” says Dammeir. “For example, the introduction of variable recurring payments in the UK opens up a world of ‘card on file’-like capabilities to Pay by Bank, increasing the use cases and – by extension – consumer adoption of this technology.”

In particular, recent years have seen the emergence of open finance – a concept that is being linked to open banking. While open banking refers to the exchange of data between banks and financial services, open finance is set to take things further by enabling the sharing of even more financial data – namely, data related to pensions, investments, mortgages and loans.

While open finance as a concept hasn’t seen as much regulation as open banking, this is beginning to change as open banking continues to evolve. One example is the European Commission’s proposal for a Regulation on a Framework for Financial Data Access, which it put forward in July 2023.

“Security and data protection remain at the forefront of regulatory concerns and the outlook suggests a more comprehensive and inclusive framework that will shape the financial services industry for years to come,” says Suvarna.

Integrating new technologies within an open finance framework will be instrumental, says Suvarna, with one of these being artificial intelligence. In a recent report, we found that AI was more frequently discussed by cross-border companies in earnings calls in 2023 than in 2022, largely driven by the trend towards generative AI.

AI has several use cases for cross-border payments, in particular helping financial institutions combat financial crime, including through AI-driven real-time sanctions screening, as well as AI-powered anti-money laundering and transaction monitoring to support instant payments services. Driving these features is AI’s potential to analyse large amounts of device data and behavioural patterns to identify potential fraud.

“Generative AI is increasingly being explored to improve the accuracy of fraud detection and prevention, including through the generation of synthetic data,” Suvarna explains. “Harnessing such cutting edge identity verification technologies and simplifying system integrations will enable secure and seamless onboarding and access to financial services.”

Advocates of open banking and regulators such as the EU commission ultimately want to improve financial services, including cross-border payments. However, moving to new systems comes with a number of challenges and although digital payment methods are growing in popularity in some markets, cards will still be king in many countries for years to come.

In fact, Vaux notes that if open banking isn’t fixing a problem for the customer, this could act as a barrier to the future potential and uptake of open banking.

“One area of open banking that has failed is not having a good understanding of the different payments’ journeys and requirements,” says Vaux. “For example, I don’t think open banking in the face-to-face payment environment is going to work, because Apple Pay/contactless cards work really well, whereas recurring payments and subscriptions are more of an issue.

“Users expect more tailored services for specific channels, so it’s important to understand what market you are going after, and then develop the solution to fit.”

FXC will continue to track the impact of open banking – and the payment methods enabled by it – on cross-border payments moving forward.