How has 2024 fared for ecommerce and retail-based cross-border payments? We review key trends and charts from across the year related to payments processors.

From developing technologies to changing consumer behaviour, 2024 has proved to be a strong year for payment processors. Despite a tougher consumer climate amid tightening consumption, the industry has moved on from its post-pandemic slump and is increasingly embracing innovation to help it grow and evolve.

We look back across our coverage this year to highlight some of the key trends for payment processors in 2024 – and provide an insight into what challenges may lie ahead.

2024 saw payment processors build a post-pandemic normal

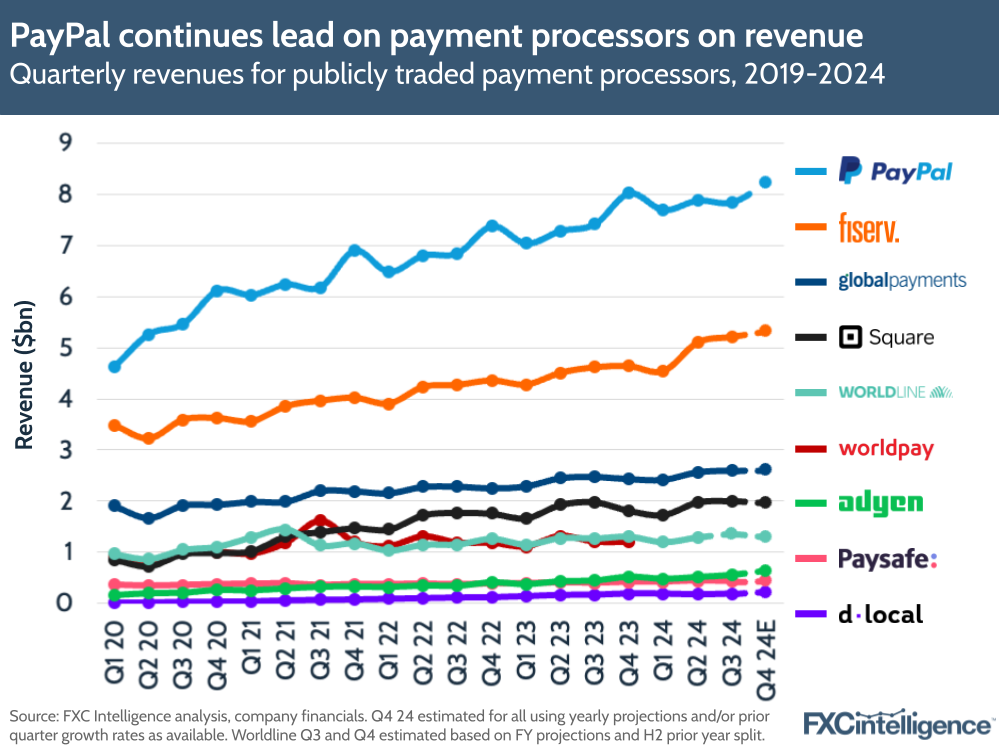

On earnings, 2024 was a solid year for many players. While lapping the pandemic-era jumps created a tough environment over the past few years, 2024 has proved to be a year with few unexpected surges, but also little in the way of severe underperformance.

Among the leading publicly traded companies in the space, PayPal continues to lead, and is focused on the medium term as it builds on its transformation project under recently appointed CEO Alex Chriss. The company has returned to growth in active accounts and saw strong transactions per active account in its most recent quarter, although its unbranded card processing growth through its Braintree brand remains muted.

Fiserv, Global Payments, Square and Worldline have all maintained their relative positions in terms of revenue, although over the past year Adyen has risen above Paysafe.

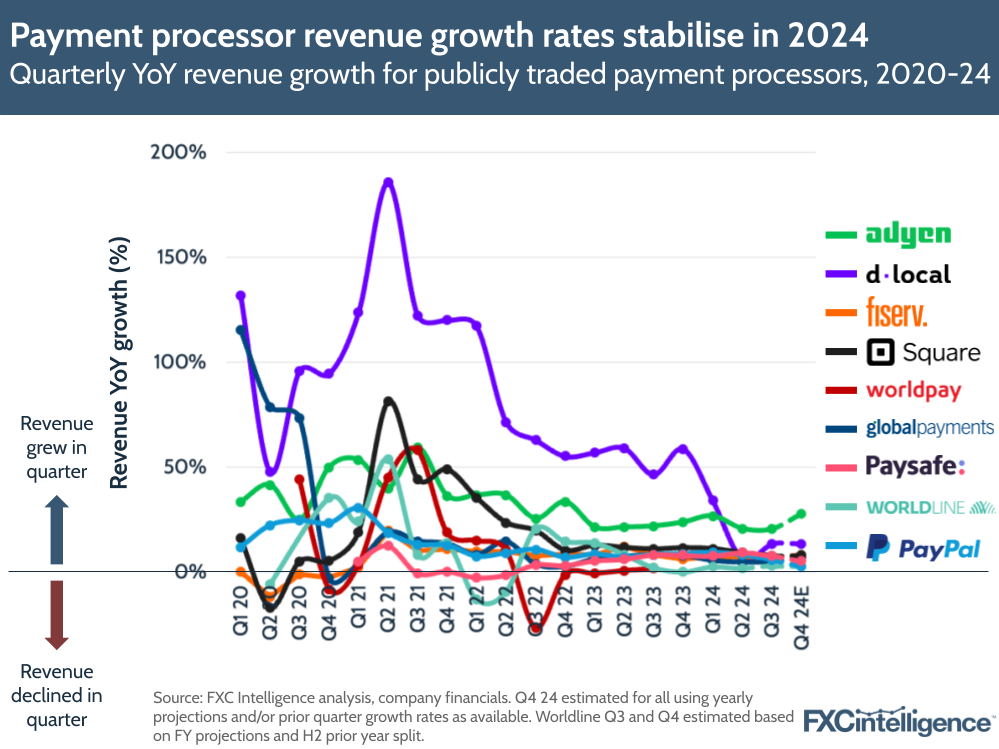

On growth, however, this year has been much more muted than some previous years. While emerging market-focused dLocal previously saw very high levels of revenue growth, the company faced a shift in product mix this year, compounded by serious macroeconomic headwinds in key markets that drove drops in performance earlier in the year, disappointing investors. The company has since worked to diversify its revenue base, which is translating into lower but more sustainable growth.

Adyen is now one of the strongest growing companies in the space, and continues to target annual net revenue percentage growth in the mid to low 20s through to 2026.

However, modest but sustainable growth is reflected across the majority of the companies that we tracked in the space this year. While most have seen solid rather than strong growth, all have consistently reported positive growth YoY and expect to continue to do so into Q4 and beyond. The results are strong foundations on which to build, creating opportunities to focus on innovation.

Cards and wallet growth helps drive volumes

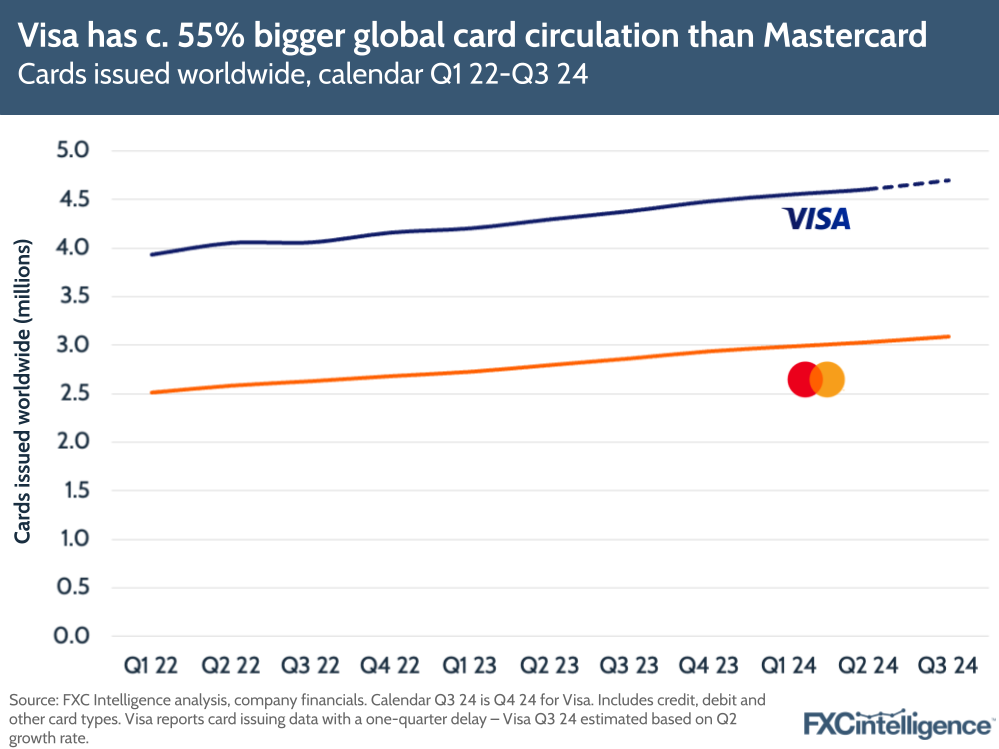

This year also continued to see the development of two trends: more people having access to payment instruments such as cards or e-wallets and more money being spent. The most reliable measure of global and country-level access to financial instruments, the World Bank’s Global Findex Database, has not been updated since 2021 (the next update is due within the year), however, there are clear indicators that global access to such instruments has grown, not least due to the numbers in circulation. As of September 2024, Visa and Mastercard together have more than 7.7 billion virtual and physical cards in circulation globally, up from around 7.2 billion a year previously.

Growth in wallets globally, and in particular the growth of region-specific wallets aided by the development of systems such as Alipay+, has also driven broader payment acceptance for some globally-focused players.

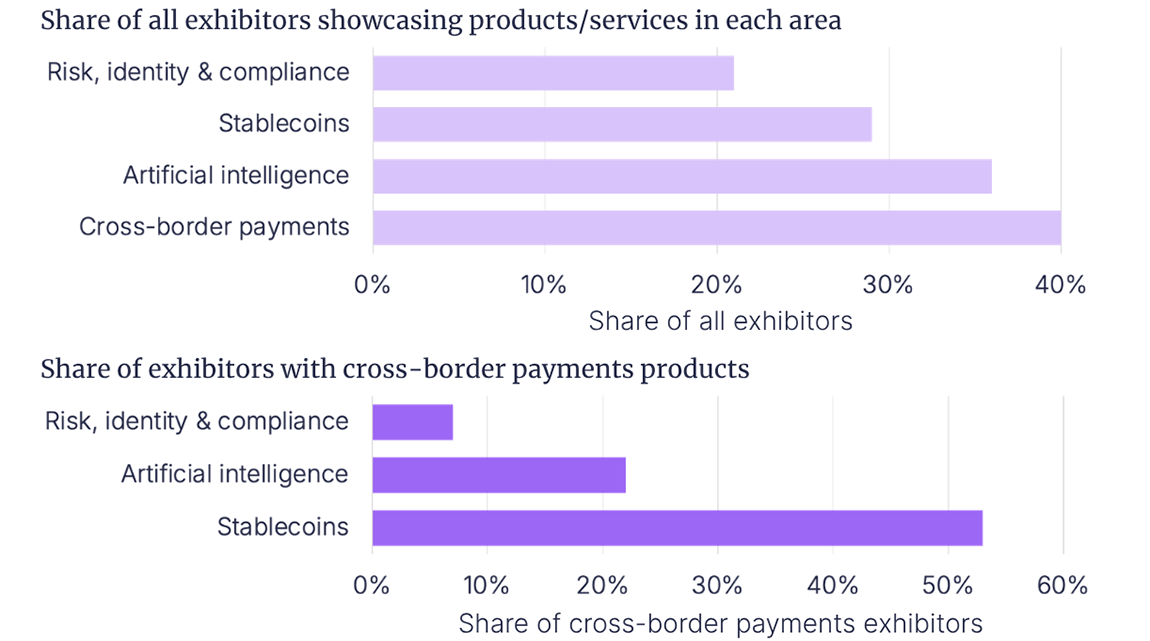

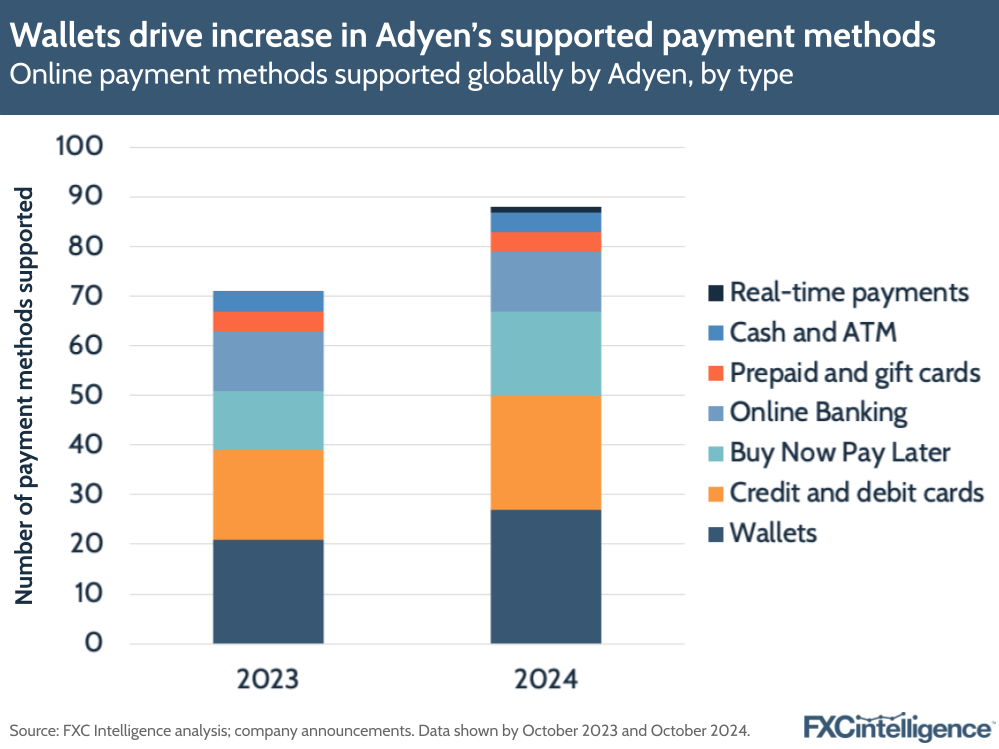

Analysis of Adyen’s supported payment methods in October 2024 versus October 2023 showed that while the number of different methods it supported on at least one corridor globally increased by 24% to 88, its largest category, wallets, grew by 29%, while its second biggest category, credit and debit cards, grew by 28% to 23. Buy now, pay later, its third biggest category, saw the biggest growth, climbing by 42% to 17.

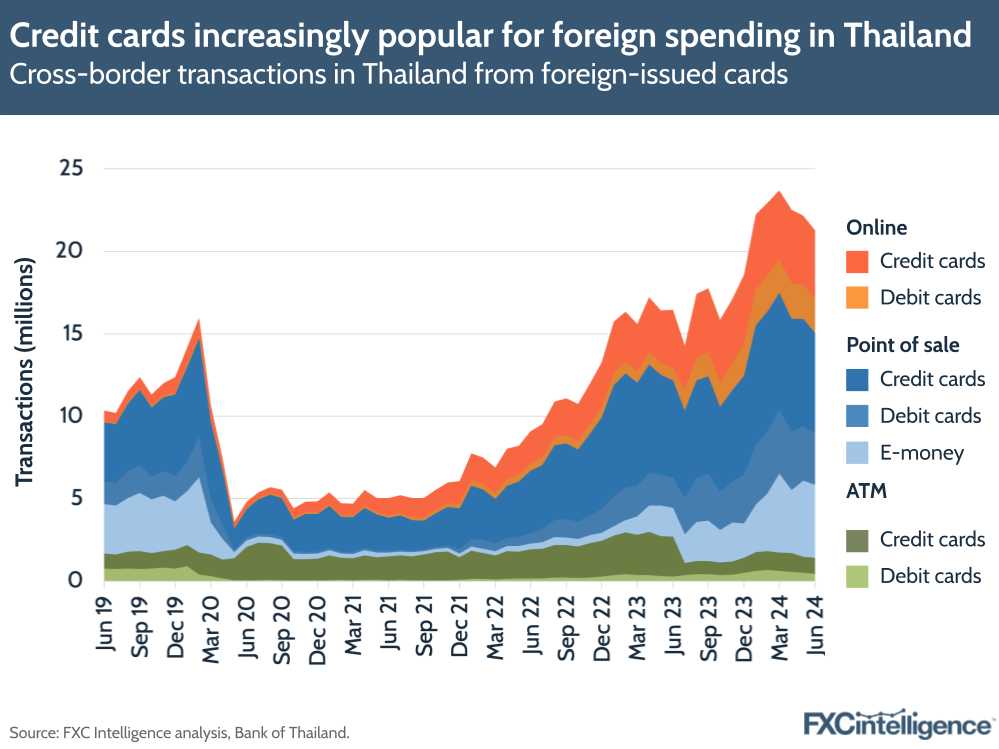

Shifts in ownership and use of payment instruments was also reflected in several central bank datasets we reviewed this year. India has a greater share of digital wallets than cards, although credit cards have seen greater year-on-year growth and have led cross-border flows. In Thailand, cross-border card usage also showed how much of an impact the pandemic had made on the country’s economy – particularly in terms of inbound cross-border card usage – and how the country has only seen pre-pandemic norms return in the past year or so.

While full-year volumes data has yet to be published, data from Black Friday indicates year-on-year gains for many players, with Stripe reporting a 67% increase in total transaction volumes during the four-day period covering Black Friday and Cyber Monday versus 2023.

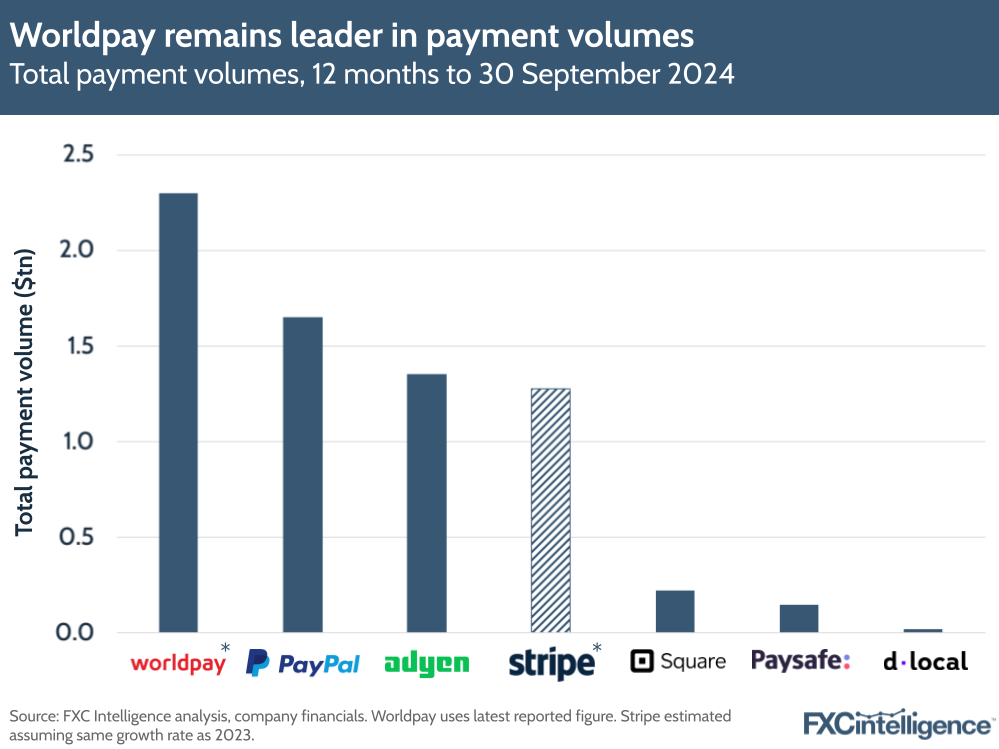

While there has been growth in payment volumes globally, volume remains split between multiple processors, although Worldpay remains the leader in this metric. Having been a subsidiary of FIS for four years, in 2023 the company announced that it was spinning off as a standalone player in a private equity deal.

The deal was completed in Q1 2024, however the full impact of the move is yet to be felt, and it is likely that Worldpay will make further moves to capitalise on its position as volume leader.

AI sees growing ecommerce presence

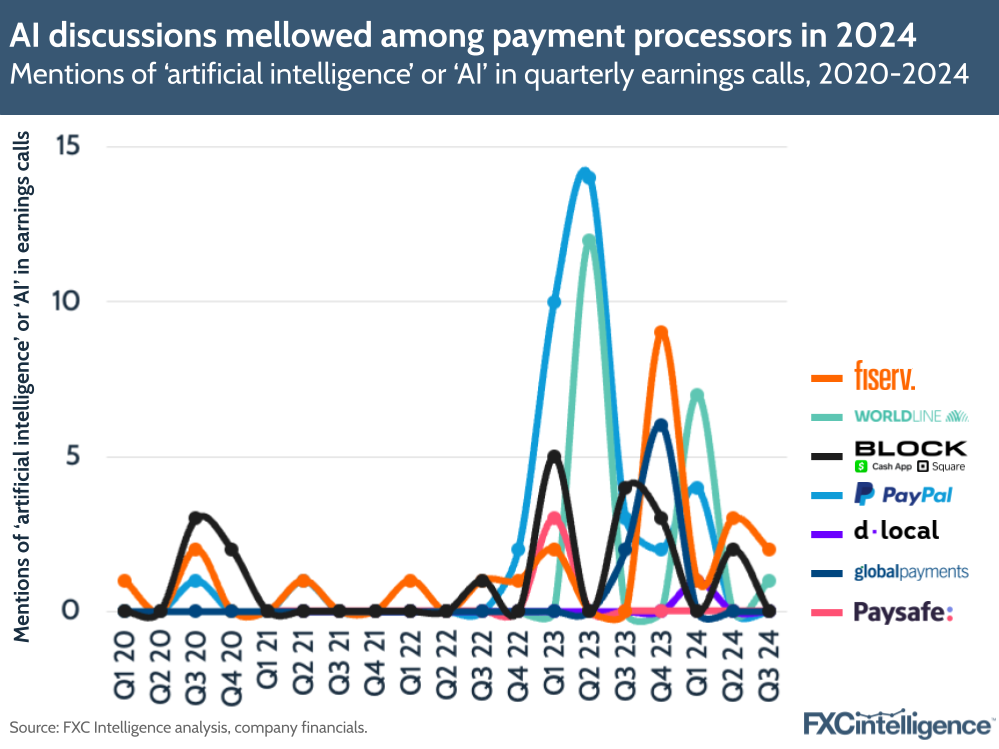

While the industry has been fairly financially stable in 2024, many players have been looking to technology to combat inefficiencies and drive further growth, not least when it comes to artificial intelligence (AI) and, in particular, generative AI. While in 2023 much of the focus was on signalling to investors that the fast-emerging AI space was something companies were thinking about, in 2024 the focus has shifted to tangible outcomes and real projects. As a result, while many companies are still mentioning the technology in earnings calls, the rate of mentions has now passed its peak.

However, that isn’t to say that AI hasn’t played a role this year. Many players have embedded the technology in a variety of their products or otherwise integrated it into their processes.

PayPal, for example, has integrated the technology into a host of the merchant and checkout tools it launched this year, which form part of its ongoing project to overhaul its ecommerce processes. This includes Smart Receipts, which encourage further shopping through personalised recommendations and an Advanced Offers Platform to improve merchant reach.

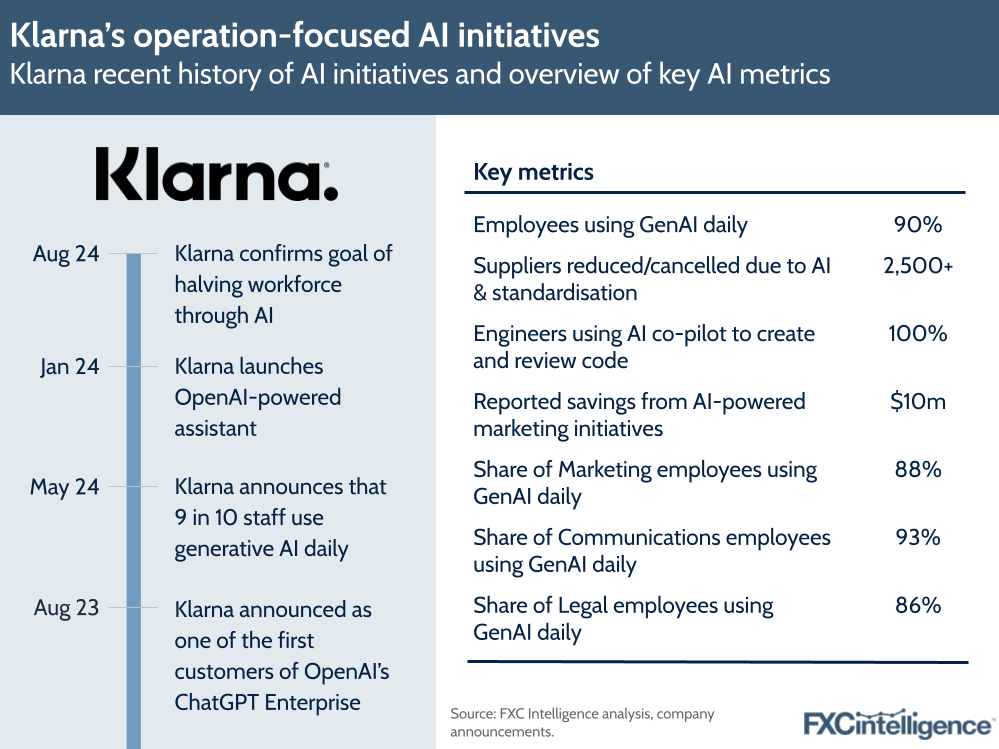

Several companies are also using the technology to reduce costs associated with their customer service. Stripe, for example, is one of several organisations using virtual assistants and chatbots, while BNPL player Klarna’s AI assistant reportedly took on the work of 700 human agents when it was launched at the start of the year.

Klarna has taken one of the most aggressive approaches to adopting AI in the industry, using the technology across the business, along with a hiring freeze, to reduce its headcount by thousands in the runup to its 2025 IPO.

While no other players have taken such an extreme approach, the use of AI is becoming increasingly normalised across the industry and is likely to continue to play a critical role as we move into 2025.

Stablecoins become key asset for future innovation

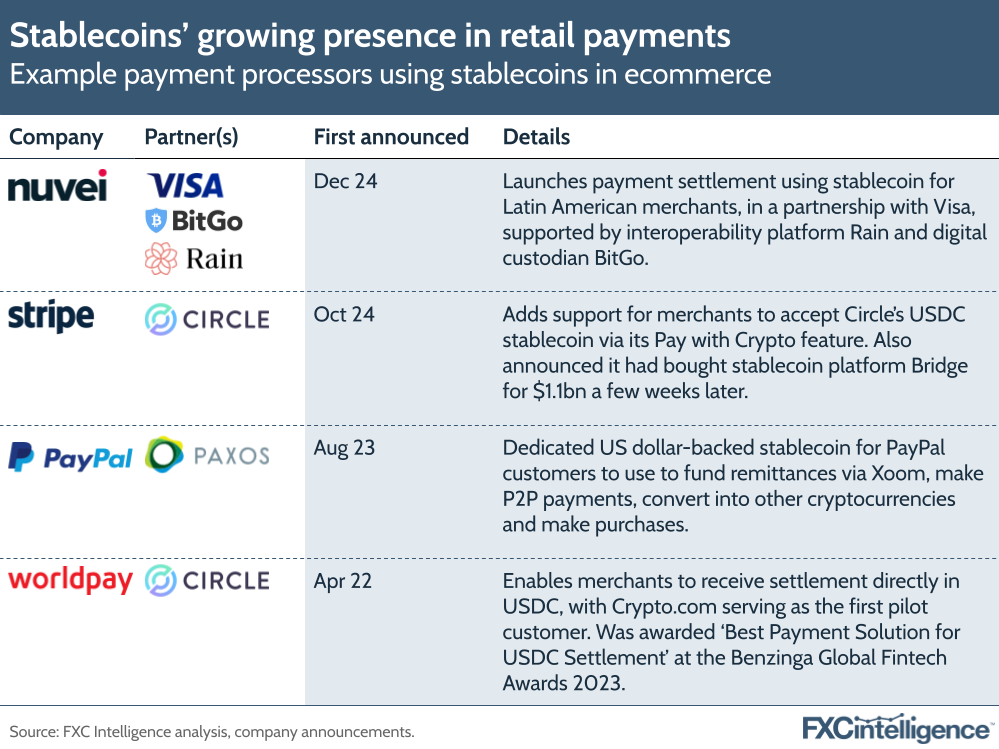

Across cross-border payments, stablecoins have emerged as a hot topic this year, and many payment processors have been a key example. For some players, the opportunity for instant settlement has made the technology an increasingly popular cross-border option and a key focus of partnering this year.

Visa has seen several stablecoin-focused partnerships this year, most recently with Nuvei to support stablecoin settlement in key Latin American markets. Meanwhile, Stripe this year added support for merchants to accept Circle’s USDC stablecoin – the most common stablecoin for this use case.

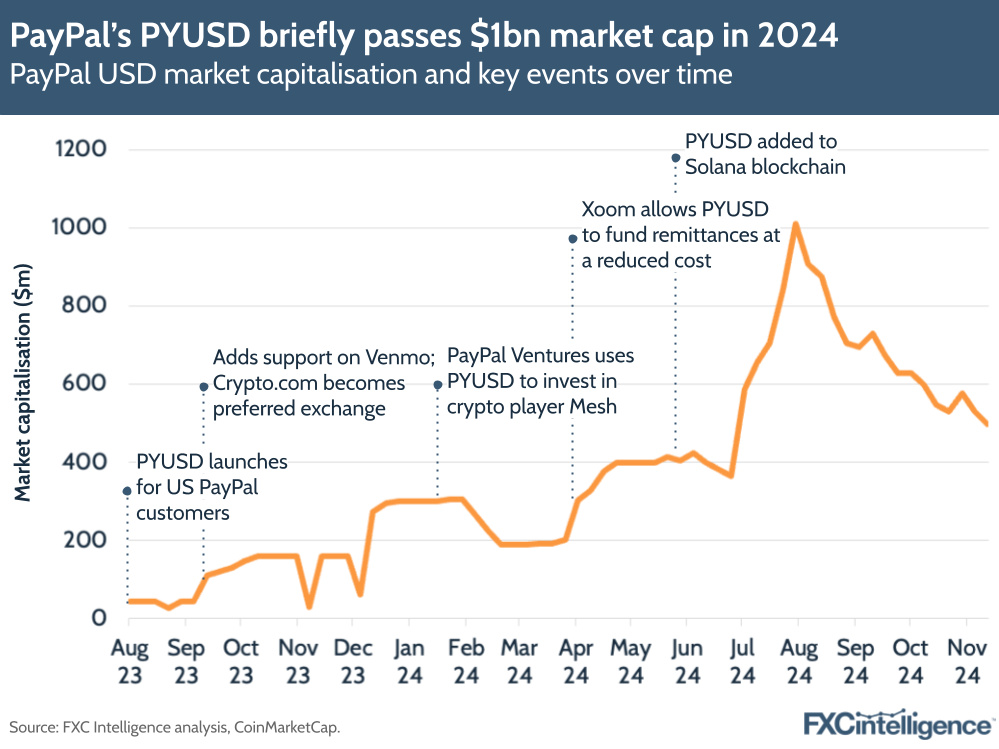

Notably, however, there are also some moves to create stablecoins. After launching its own stablecoin (PYUSD) in 2023 in a partnership with Paxos, PayPal has developed PYUSD significantly in 2024, broadening its use across retail and remittance settings.

Stripe’s October purchase of stablecoin player Bridge for $1.1bn has led many to speculate that it is also planning to launch a stablecoin, suggesting that this may be an area we hear far more from into 2025.

Cross-border pricing remains an industry challenge

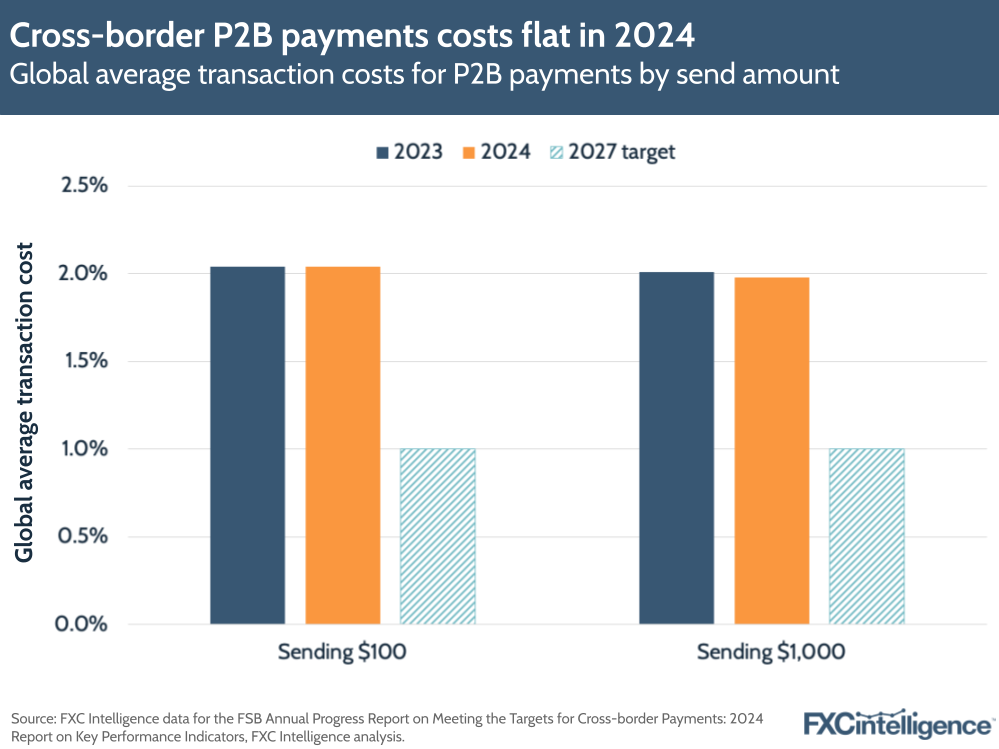

While there have been key developments in 2024, there are still challenges facing the industry, not least when it comes to pricing. This year saw the publication of the second set of KPI data on the Financial Stability Board’s G20 Roadmap for Enhancing Cross-Border Payments, for the first time providing a sense of the direction the industry is moving on its 2027 targets.

This includes significant data supplied by FXC Intelligence, which supplied all data for the retail section of the report. This includes P2B payments – payments sent cross-border from consumers to businesses, much of which is retail-related card payments.

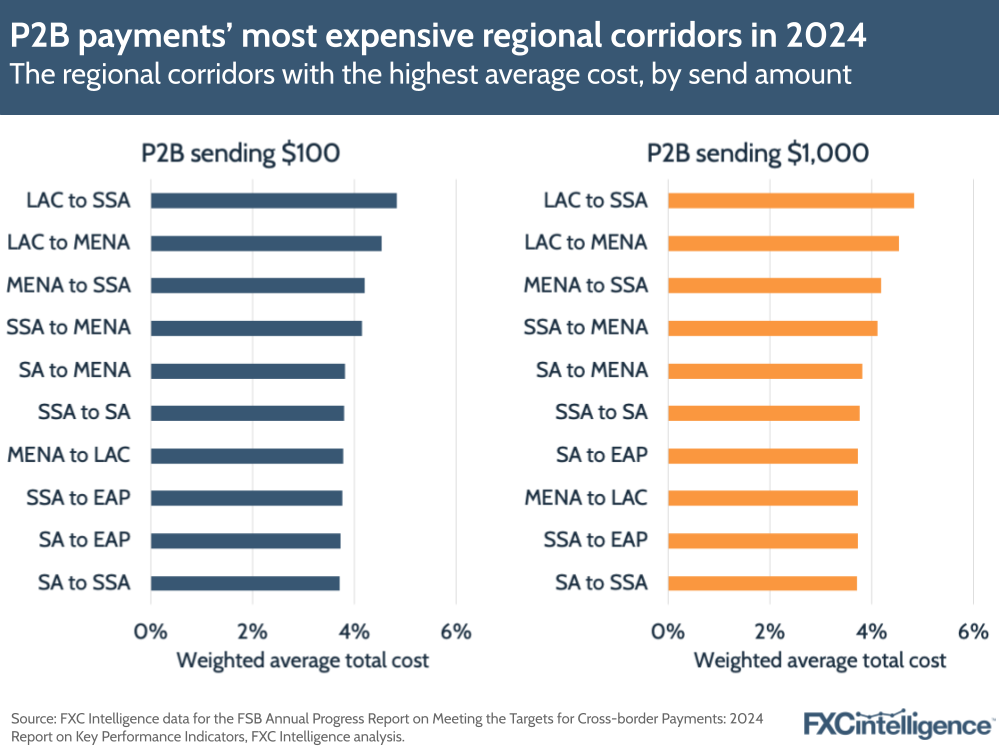

Here the target is for cross-border costs to be reduced to an average of 1%, with no corridors above 3%. However, the latest data shows P2B payments are still around twice the 2027 target, with minimal change from 2023.

2024 data saw no change for global averages for $100 payments versus 2023, although there was a 0.4% improvement for $1,000 payments. This remains better than many other use cases, with several others, including P2P payments, seeing average costs rising year-on-year, rather than falling.

There are also still more than 1,000 corridors where costs are over the 3% cap, with many of the most expensive seeing the payer located in Latin America and the Caribbean (LAC), Sub-Saharan Africa (SSA), the Middle East and North Africa (MENA) or South Asia (SA).

For the industry, this is a challenge. While payments processors are often not solely responsible for the cost of a cross-border payment to a consumer, there are opportunities to provide localised currency solutions that can help combat additional costs and improve the buyer experience.

Beyond this, continuing to develop infrastructure in emerging markets, where there are already clear opportunities, is likely to help drive down costs and improve the global commerce potential for the industry.