Real-time payments has seen growing demand in many regions, but in the US The Clearing House’s RTP network has been a critical driver. We speak to The Clearing House CEO and President David Watson and ACI Worldwide CEO Tom Warsop to find out more.

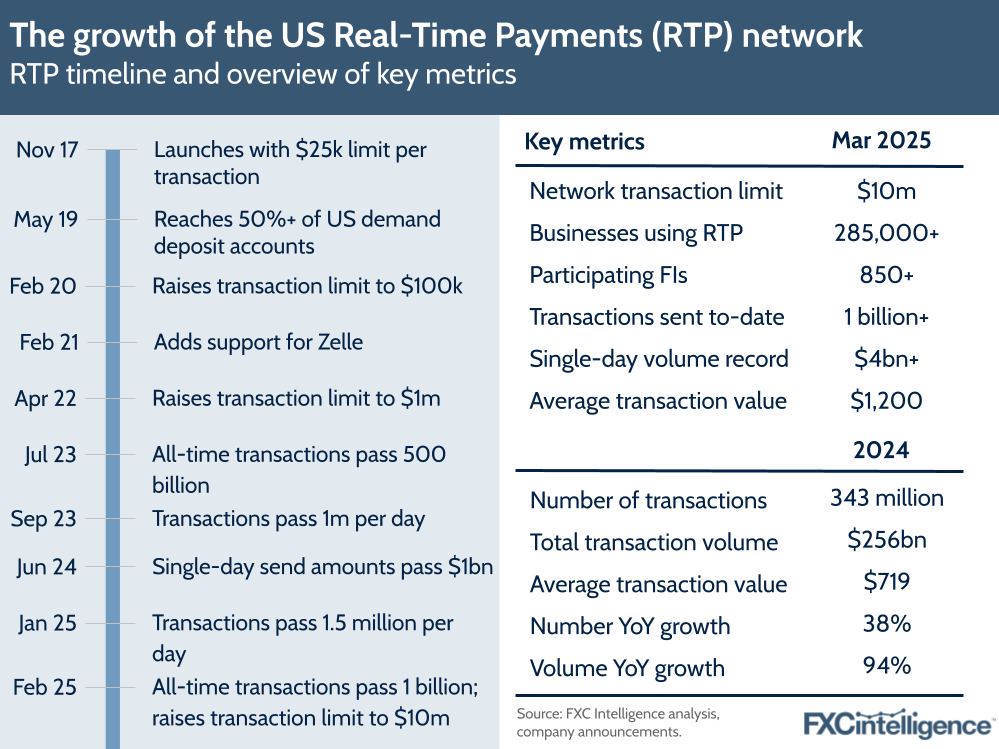

In 2017, The Clearing House, supported by key technology partners including ACI Worldwide, launched RTP, a 24/7 real-time payments platform in the US available to all deposit-holding financial institutions. And although it took some time to gain momentum, it has recently seen a significant upswing in adoption.

“The growth in account-to-account real-time payments here in the US has been quite phenomenal over the last year or two,” says David Watson, CEO and President of The Clearing House, a bank consortium-owned company that is also responsible for around half of the US’ commercial automated clearing house (ACH) volume.

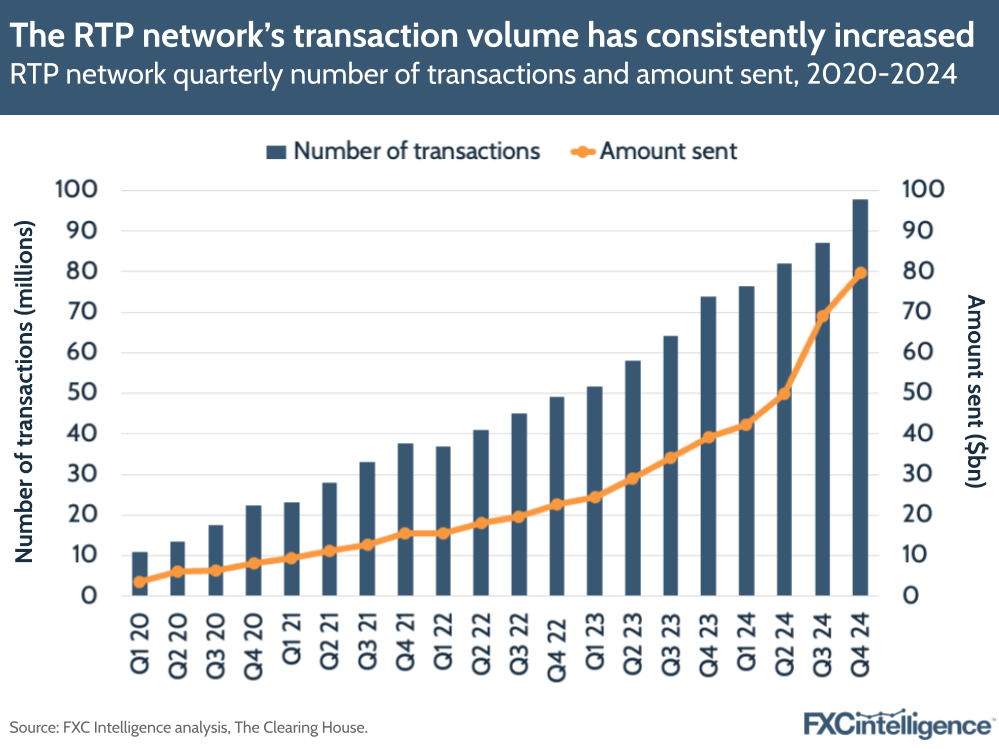

This has seen RTP grow the number of transactions it handles from around 172 million in 2022, with flows of $75.7bn, to 343 million transactions with flows of $256bn in 2024. This remains “a drop in the ocean” relative to other parts of the US payments network – CHIPS, for example, settles $1.8tn in domestic and international payments each day – but it represents a significant improvement on “a very low starting point”.

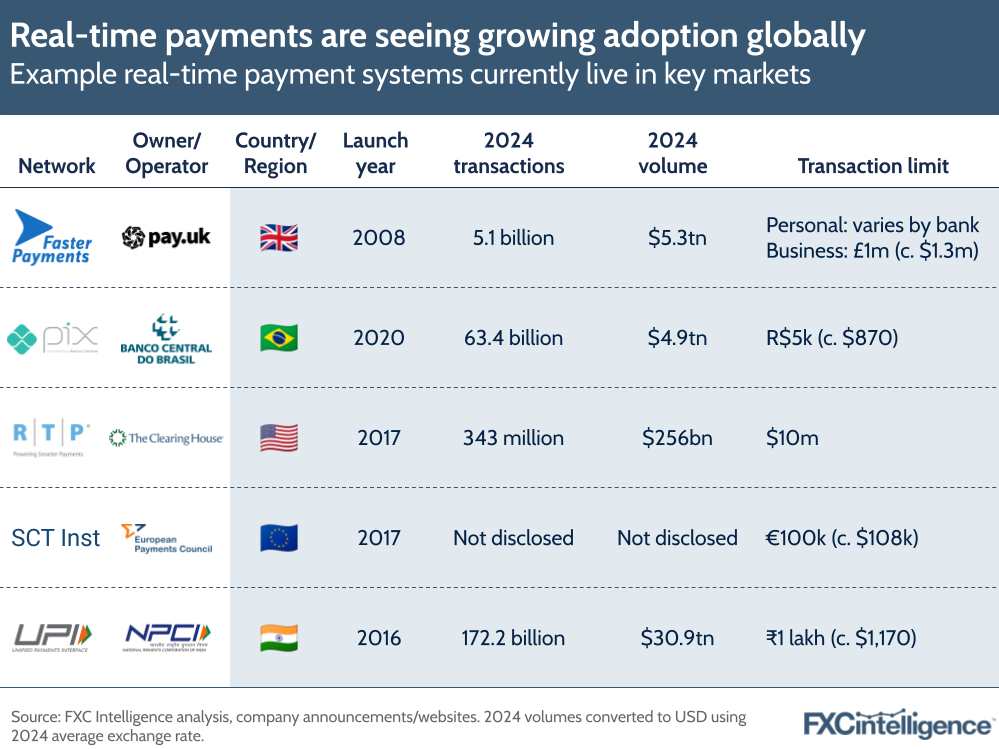

While the first of its kind in the US, RTP joined a growing number of domestic real-time payments systems being developed globally. At the time of its launch, the UK and Japan were among those with well-established networks, while India had launched its own system, UPI, the preceding year. Many more have also been added since, including Pix in Brazil.

Today, the number of countries globally with active real-time domestic payments systems sits at around 80, with the majority of major markets across Europe, the Americas and Asia-Pacific now having active networks.

A key driver of this growth is the financial benefits that real-time payments bring. Analysis of the economies of 40 countries by ACI Worldwide found that such payments had increased their 2023 GDPs by a combined total of $164bn, with the company projecting real-time payments to contribute $286bn to their GDPs by 2028.

“Real-time payments is a key driver of incremental economic growth,” explains Tom Warsop, CEO of ACI Worldwide, adding that it acts as a multiplier for the velocity of money, particularly in cash-intensive economies.

“If you turn those transactions into digital payments of any kind, the multiplier goes up, but with real-time payments, clearing happens immediately, freeing up the capital that’s tied up with that transaction in seconds or microseconds. So you can use that money many times in the time that one cash transaction would take.”

With such potential, which areas are real-time payments finding particular success in and what lessons can be learned from RTP in the US in particular? Watson and Warsop share their insights.

Growing global demand for real-time payments

While more than two-thirds of countries globally now have some form of real-time payment system in place, when the UK’s Faster Payments system launched in 2008, such solutions were rare.

“The UK was one of the first economies to explore real-time payments,” says Warsop, pointing to ACI Worldwide’s early involvement in Faster Payments.

“We were one of the original innovators in real-time payments. Now we’ve gotten to the point where 27 real-time payment schemes around the world use our software to handle all the payments in that scheme.”

However, use cases and adoption are by no means consistent. India has the largest real-time payments market globally through UPI, which Warsop says “has grown incredibly fast” since its 2016 launch. Meanwhile, Brazil’s Pix, while smaller, has seen similarly strong growth since its launch in 2020.

In both countries, but especially in India, a population where a high share was unbanked or underbanked, as well as a relatively immature financial services market, meant the economy was highly cash-dependent, creating an environment where an accessible real-time payments system could prove to be a step-change.

“Those factors created this real urgency, a need for something new to make the payments ecosystem in India work better, reduce friction, speed up and lower costs,” says Warsop.

“That’s where UPI came in, just at the right time, and adoption went crazy.”

However, in more developed countries such as the US where real-time payments are an incremental improvement on an already well-developed financial system, the situation is quite different, resulting in slower adoption.

“It’s the opposite of the India story,” explains Warsop. “You have a very mature, well-functioning financial services market and a relatively low unbanked or underbanked population, so there wasn’t this sort of urgent need that real-time payments were stepping in to fulfil.”

Finding use cases for RTP in the US

While the US has not seen the urgent step-change impact from RTP that UPI has brought to India and Pix to Brazil, it still has immense potential, as its recent surge in adoption suggests. The difference, however, is in specific use cases.

According to Watson, when RTP launched it was pitched to “every payment, any payment anywhere”.

“There were a lot of use cases that just didn’t make sense or weren’t needed,” he says. “Monthly payroll, for example, doesn’t need to go over an instant payment system; there are certain things that work incredibly well over delayed ACH settlement and should stay there.”

However, RTP has since refined the use cases it is being pitched for, with Watson identifying four use cases in particular that he says have provided traction for the system.

These include person-to-person payments, particularly those that use domestic bank-based digital payments network Zelle, which RTP has supported since early 2021. There are also what Watson describes as “me-to-me payments”, when an individual is transferring money between different accounts they own.

“If I’m moving money to my brokerage account, I’m doing it because I want to buy or sell something or trade, and therefore I want that money there instantly so I don’t miss that market opportunity,” he adds.

Beyond this, he also highlights B2C disbursements, such as pass payouts from an insurance company, as well as what is known as “earned-wage access”, which covers ad-hoc earnings sent to gig economy workers or others in the service economy.

Warsop, meanwhile, sees some of the strongest potential in B2B payments, giving the example of a public company needing to pay a cloud server bill – an expense that can run into millions of dollars a month.

“Today they usually send a wire, which costs a lot of money – the average is around $42. They can do exactly the same – get immediacy of payment, traceability, proof of receipt – with a real-time payment at the cost of a few cents,” he explains, adding that while this use case is beginning to be seen, he anticipates the cost difference driving “a lot more interest” in the future.

However, one area he sees particular potential in is government payments, which he argues were a critical driver of ACH in the 1980s and 1990s, when the US government moved the “vast majority” of its payments to the system. And in time he expects a similar shift from ACH to real-time payments in the country.

“It costs less. Not that ACH is super expensive but it’s [RTP’s] still a fraction, so a few pennies for each transaction and that will drive tremendous volume into the system,” says Warsop, contrasting this with the consumer side of the market where he sees an “addiction to credit card rewards points” being a major barrier to broader RTP adoption. Nevertheless, he sees the system ultimately becoming a major part of the US payments landscape.

“Over time, real-time payments will play an important role in the United States because there are really powerful use cases and there are really good benefits.”

Growing send amounts for real-time payments

Part of finding the right use cases for RTP has been growing send amounts to match, a process that has seen caps on individual transactions steadily lifted over time. Initially, payments were limited at $25,000, before being raised to $100,000 in 2020 and then $1m in 2022. In February this year, however, RTP’s limit was raised again, to $10m, with BNY Mellon becoming the first to take advantage of the change, with a $10m inter-company liquidity management payment a day after the cap was lifted.

In the long term, Watson says the plan is for RTP to have a cap similar to ACH where it is either non-existent or “so huge you don’t think about it”, although banks are free to set their own caps and some vary this depending on the client type and risk levels involved.

However, the steady progression up to higher caps has ultimately been a matter of caution.

“When something is new, you want to do the growth of that network in a safe, secure manner – we do not want to launch something that potentially has billion-dollar payments running over it until we’re comfortable with everything that is there around safety and security,” he says, adding that the “incredibly low” levels of fraud mean he is “already there”.

“I could quite happily raise that limit to a hundred million, to a billion.”

While such caps may still take some time to actualise, however, the recent raise to $10m has already made an impact, with Watson adding that The Clearing House has seen “an explosion in value” on RTP, above what the organisation expected.

“We always expected to see more payments between $1m and $10m by increasing that limit, but the average size of payment over the network has gone from $800 two months ago to $1,200,” he says.

“We have three days in the last two weeks where we’ve settled over $4bn on that day, whereas our previous record was one and a half billion dollars last year.”

Making real-time payments cross-border

While RTP’s volume has grown considerably, it remains limited to domestic payments. However, The Clearing House has begun to explore ways to add a cross-border component.

“We spent a lot of time last year analysing whether we could, would or should connect RTP in the US to Europe, to other countries,” says Watson, adding that he believes that is “where we’ll get to as an industry”.

This has seen The Clearing House explore bilateral connections with other real-time payments systems in other markets, something that other real-time payments systems have begun to explore, such as using India’s UPI in Singapore.

This is something that Warsop sees significant potential in, giving the example of Indian expats based in the US, who want to send money to India for family members or to cover a mortgage payment. This is typically currently handled by traditional remittances players or via bank wires, the former of which “looks like a real-time transaction” but does not include immediate settlement, while the latter is expensive and not real-time.

“If you overlay cross-border with real-time, let’s say, and it’ll start out as bilateral agreements between, say, the Indian central bank and the Fed, they’ll be able to send instantaneously, with very low cost, very low friction.”

Building interoperability between RTP systems

From a technology perspective, establishing bilateral connections between real-time payment systems remains relatively straightforward, however ensuring alignment from an operational perspective is another challenge, although both Watson and Warsop see compliance with ISO 20022 standards as key.

“RTP is ISO 20022 native: it was built on ISO, it continues to be on ISO. Our government competitor is ISO; it’s ISO in Europe; ISO will be the basis for Canada’s rails; and there are some countries like the UK who are designing a journey to get to ISO for their Faster Payment system,” says Watson.

“You end up with that international standards organisation really defining the format, which is richer data in a structured manner that makes it much easier to align because there’s a framework.”

However, while ISO 20022 is key, there are potential issues too, with Warsop highlighting that “the agreement between the various schemes, the rules, aren’t quite the same”. This creates challenges that need to be resolved for such bilateral agreements to fully be embraced, such as commercial concerns including the question of liability if a payment goes wrong.

“That has to be worked out, otherwise no one’s going to send $10m or £20m or whatever the number is, until they understand where the liability sits and how they’re going to mitigate that risk.”

Towards an interconnected real-time payments future

However, The Clearing House’s ultimate focus is in developing a one leg out (OLO) based solution, a term often used to refer to cross-border payments where one half of the transaction is regulated under European Union payments laws, although in this case used slightly differently.

“We’re looking to open up the real-time payments network to one leg in and one leg out transactions, so this idea of a leg starts in another country, it moves cross-border and then it settles domestically,” he says. “Or a payment settles domestically and then there’s an out-bound foreign exchange and international payment.

“Today that’s not allowed over RTP and traditionally it hasn’t been allowed in Europe or other countries.”

In the long run, however, Watson sees the goal not just to be bilateral connections with other single payment systems, but to develop a lightweight, interconnected system that would allow multiple real-time payments systems to work together across borders using this OLO-based approach.

“If all of the domestic networks start allowing this, you can actually start working together on rules and schemes across the world,” he says, adding that this could remove the need for a “big giant lump of technology in the middle”.

His examples of such technology include Immediate Cross-Border Payments (IXB), which was piloted by EBA Clearing, The Clearing House and Swift in 2022 to convert real-time messaging between real-time payments systems in the US and Europe, and Project Nexus, a BIS initiative to interlink domestic payments systems via a single connection to a central hub.

“We call it OLO squared. It’s not just one leg out from one side, but do it with the other party, and then align on rules,” he says, adding that would allow real-time payment systems to agree on which types of payments they would accept.

“You end up getting that scheme-type feeling – potentially you can align on pricing as long as it’s done appropriately – and actually get the same benefits of an international real-time payment system by connecting the networks through rules and schemes and allowing that one leg in, one leg out.”

Crucially, this is not just an idea. The Clearing House is already taking considerable steps to make this project a reality, and we are likely to see considerable movement within the next 12 months.

“We’re looking to go live with that towards the end of this year, early next year and are working between now and then, not just to offer it in the US, but also having conversations with other jurisdictions around what that alignment, OLO squared, would look like eventually.”

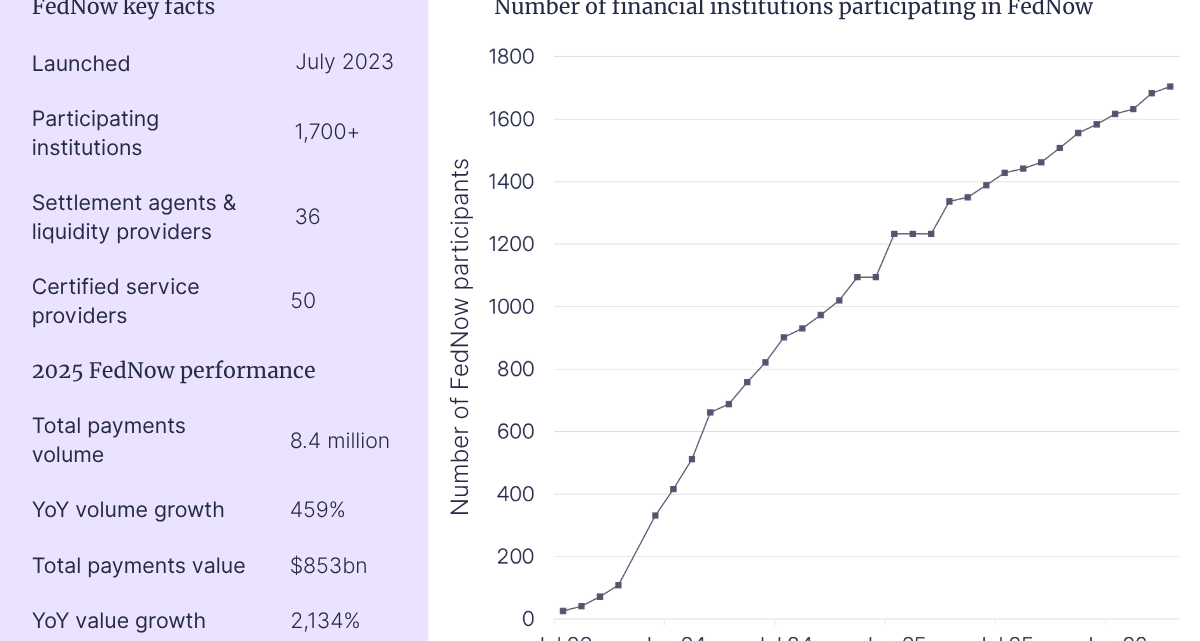

Is FedNow a rival to RTP?

Closer to home, however, is the question of competition in the US market. While RTP has been steadily growing over the past few years, in 2023 it gained a challenger in the form of FedNow. Launched by the US Federal Reserve, this also provides domestic real-time payments in the US, and while some have positioned it as a direct rival poised to take flows from RTP, the reality has been somewhat different.

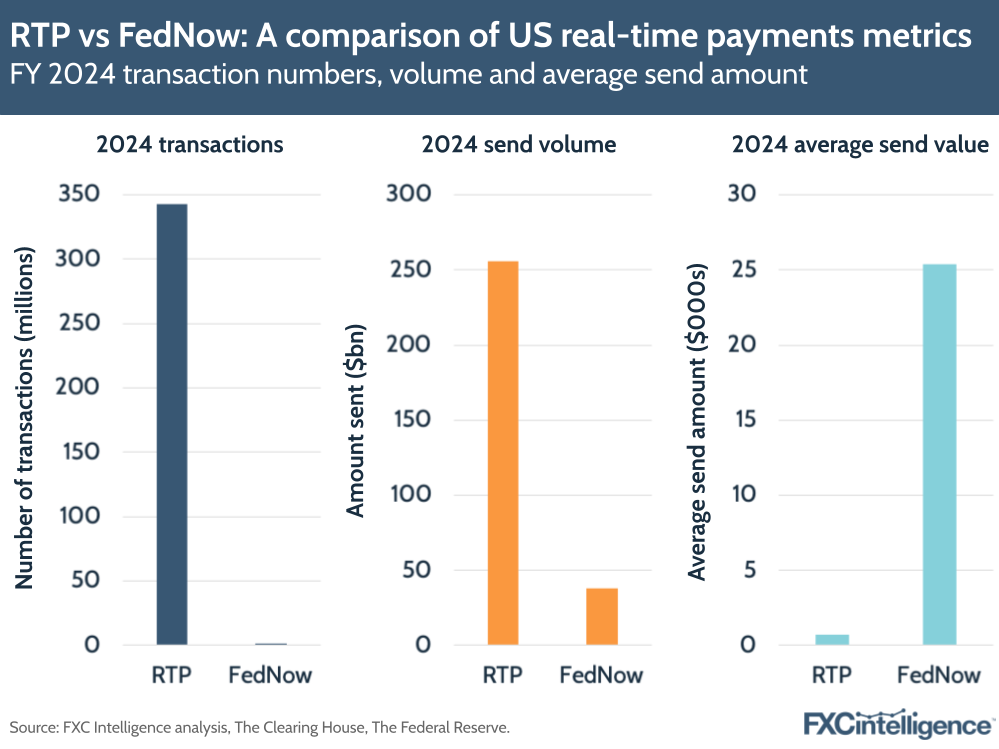

Watson sees FedNow as having been a “huge accelerant” to RTP, pointing to the “exploding” growth rates it has seen since the former’s launch. In 2024, RTP saw transactions grow by 38%, with their value climbing by 94%, while the number of businesses using the network has almost doubled over the same period.

“A lot of people were holding back on RTP to wait for this announced second system,” he says, adding that when FedNow launched such organisations went live on both systems simultaneously but found that due to its relative maturity, they were seeing more immediate impact from RTP.

“When they go live on FedNow, they don’t see any volume or value for their clients of any real scale. Whereas when they go live on RTP, because we have large B2C distributors, literally a bank turns on their routing number on RTP, they start receiving payments for their consumers that day.”

This is aided by the fact that, at less than two years old, FedNow is still building its coverage and use. While it has more banks connected than RTP, its account coverage is significantly lower and FedNow’s send volumes are a small fraction of RTP’s.

“Their average payment size is interestingly a lot higher, which implies they’re seeing a lot more wholesale volume on FedNow than necessarily the retail side,” adds Watson.

While this indicates that FedNow is ultimately catering to a different use case, he ultimately sees the network having considerable success, with the two systems eventually becoming interconnected.

“It will grow, it will have scale, it will likely have a great effect in getting us both to ubiquity,” he says.

“When they’re ready – and we’re ready now – we would like to talk interoperability. I understand that they have something that’s in its infancy and needs to get a bit more to maturity before they’re able to start discussing that strategically with me. I just hope they do it sooner rather than later.”