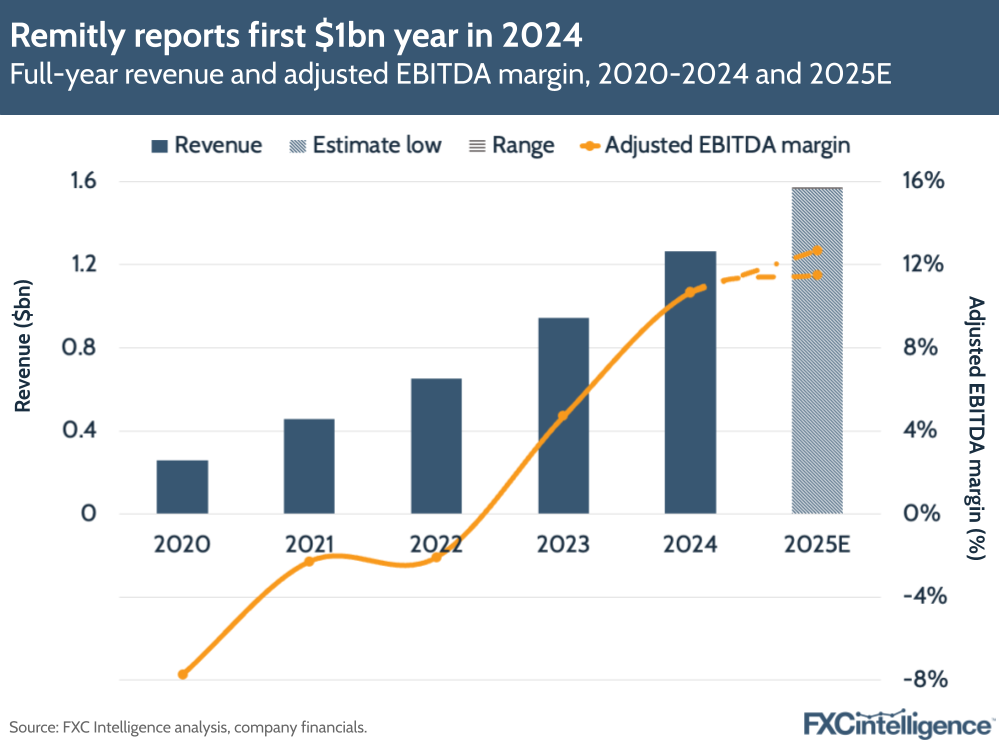

Remitly moved from strength to strength in 2024, comfortably beating its upper-range forecasts and surpassing $1bn in annual revenue for the first time. We speak to CEO Matt Oppenheimer about how the digital remittance player plans to unlock further growth in 2025.

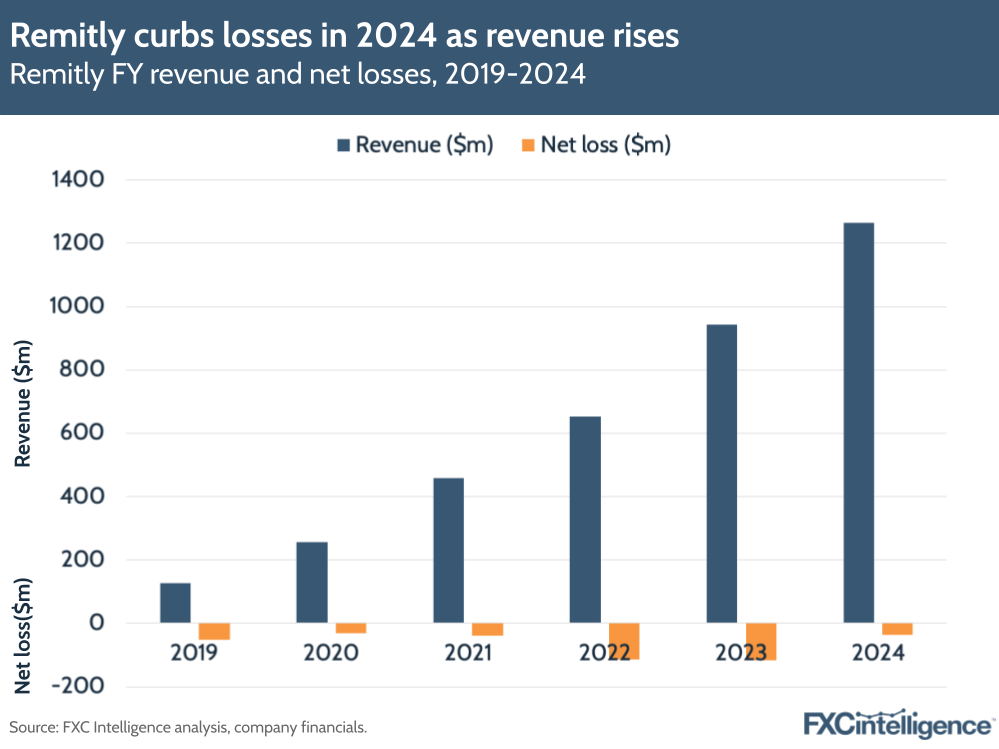

Remitly continued its growth streak in Q4 2024 with revenue rising 33% YoY to $352m, driving full year growth of 34% to $1.26bn. Perhaps more impressively, the remittances provider saw 203% YoY growth in its EBITDA to reach $135m in 2024 – its largest annual increase in this metric and a major milestone in its profitability journey.

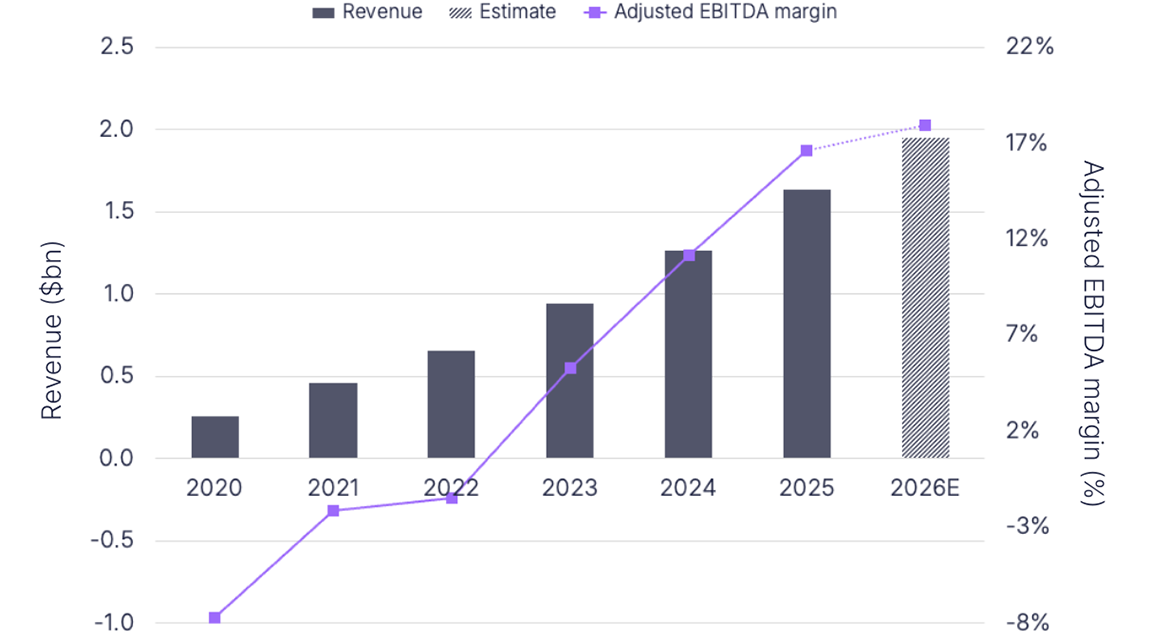

Remitly’s ongoing strength is built on consistent customer growth, secured via strong word-of-mouth marketing and its push to diversify in new and existing geographies. Though the company still saw high net losses in 2024 (-$37m), these are significantly down on the previous year (-$118m). Remitly now predicts 2025 could be its first year seeing positive GAAP net income, with revenue less transaction expenses (RLTE) also expected to surpass $1bn.

Investors responded well to the company’s earnings, with the company’s share price rising after its results and continuing an upwards trend for the year so far. Since its IPO in 2021, the company has more than doubled its annual revenue. However, in 2025 the company is expecting more moderate annual revenue growth of 24-25%, to around $1.6bn, aligning with its comments in its Q3 earnings call.

We spoke to CEO Matt Oppenheimer to explore Remitly’s flywheel-led approach to growth and profitability, as well as its future plans to grow share in 2025.

How Remitly grew faster than the market in 2024

Daniel Webber:

Matt, the numbers are once again very strong, way above the market. What’s continuing to help you take share versus the market overall?

Matt Oppenheimer:

You look at the full year 2024 and we were up 34% year-on-year to $1.26bn in revenue, with similarly strong numbers for Q4. That’s because the flywheel for our business is really spinning, and we shared that flywheel for the first time in these earnings results.

You look at everything from the word of mouth and brand that we’re building – which is foundational and because of the reliable product that we’ve built – to the really excellent execution from the marketing team in terms of getting further word out about our excellent service. That consistent delivery of our product and of our marketing results is in the kind of growth that we saw in Q4, and we’re incredibly excited.

Inside’s Remitly’s 2024 growth and 2025 projections

Driving Remitly’s first $1bn+ year, the company saw revenue rise 33% in Q4 2024 to $352m, with EBITDA surging 434% YoY during the quarter to $43.7m. This meant the company saw an EBITDA margin of 12%, up from 3% in Q4 2023 and the second-highest margin the company has seen since its IPO.

Despite significantly outpacing its expectations for 2024, the company is projecting more moderate guidance next year, with revenue expected to rise 24-25% to $1.57bn-1.58bn. This guidance reflects Remitly’s “confidence in durable customer behaviour”, though it expects volume growth to outpace revenue growth both in Q1 and FY 2025.

Equally, Remitly expects its adjusted EBITDA to rise at a slower pace in 2025, between 34% and 38% to $180m-200m. This would drive a margin of 11.5-12.7%, up from 10.7% in 2024.

Remitly’s flywheel approach to growth

Daniel Webber:

Talk us through Remitly’s flywheel.

Matt Oppenheimer:

At the center of the flyheel is growth and profitability. That’s the output. We’re able to deliver that as a digital-first player with more scale, because by having those things, we can drive a lower cost structure around a variety of our variable costs. That enables us to offer better prices, which is part of what enables us to provide a better customer experience.

This is evidenced in the fact that 90%+ of transactions are delivered in less than an hour, and that number continues to go up. And that’s across 170 countries, 5,100 corridors, over four billion bank accounts and mobile wallets, and more than 400,000 cash pickup locations. So that customer experience and reliability drives more customer actions and that repeat behaviour. That enables customers to have a broader service selection.

As we think about our vision of financial services that transcend borders, that then improves the customer experience. And that flywheel at our scale and size is really exciting. I think we’re the only remittance company that’s over a billion in revenue and that is growing 30%+, and that flywheel is fueling a lot of it in addition to just brilliant, continued execution from the team.

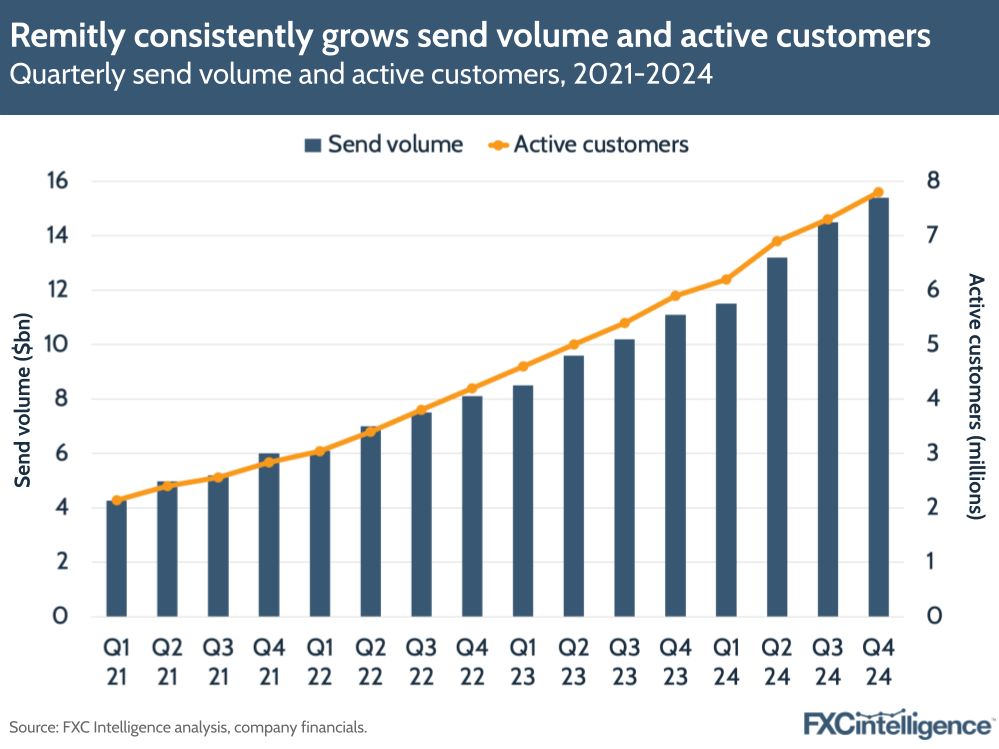

Active customers and send volumes

Remitly continued to grow its customer base in Q4, with active customers rising 32% to 7.8 million. This contributed to 39% growth in send volume over Q4 2023, while for the full year, send volumes rose 38% to $55bn.

Remitly is continuing to scale its operations to reach more customers. Product improvements and word-of-mouth marketing helping to drive higher numbers of transactions, in turn translating to more growth – this is Remitly’s flywheel in a nutshell.

Driving profitability as transaction expenses rise

Daniel Webber:

Aside from growth, people nowadays really care about profitability. You are focused on both. How are you continuing to approach driving profitability ?

Matt Oppenheimer:

That’s part of the flywheel. When you look at ’24, we saw $135m of adjusted EBITDA and 200%+ growth. In 2025, we are looking forward to our first $1bn in revenue less transaction expense (RLTE).

That’s important, because then you can decide how much you’re investing below that line. We’re being disciplined, so we are also excited about our first full year of not only the adjusted EBITDA numbers that I mentioned continuing to increase, but our first full year of GAAP net income profitability.

We have always been thoughtful, diligent stewards of capital, in terms of the investments that we make. And as a payments company at scale now, and with that flywheel spinning, it’s both showing a lot of growth on the top line, but also certainly on the bottom line, and that’s really exciting to us as well.

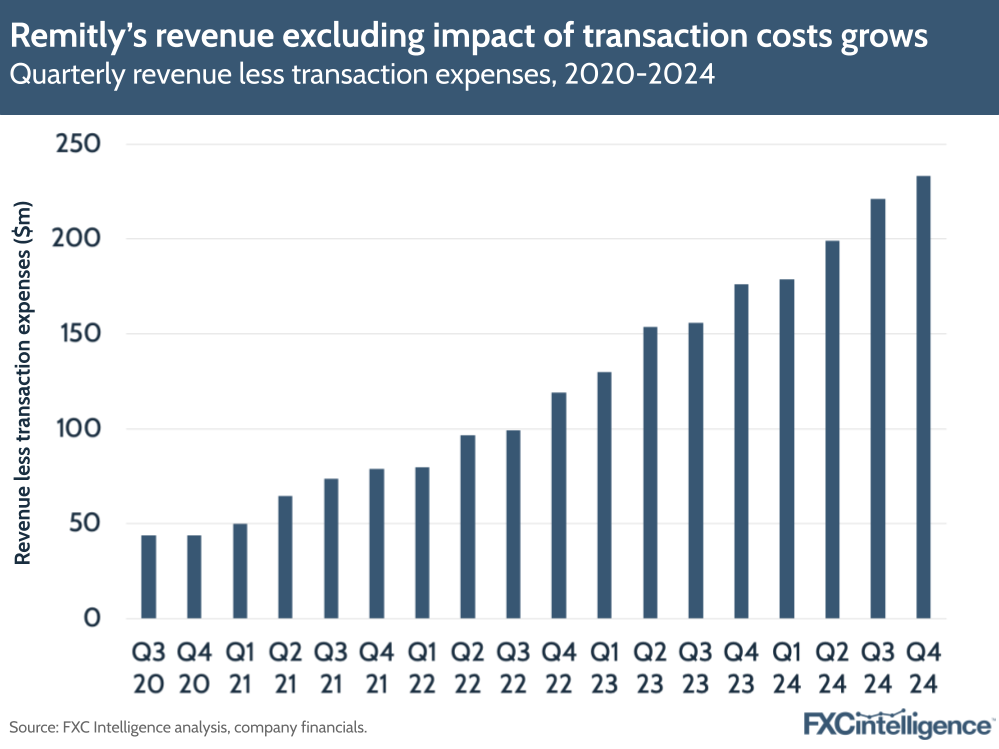

Remitly’s revenue less transaction expenses

To showcase the long-term profitability of its business model, Remitly has been increasingly frontloading revenue less transaction expenses, which grew by 33% in Q4 2024 to $233.5m. The majority of RLTE came from repeat customers, highlighting the ongoing trust in the company’s services.

As a percentage of revenue, transaction expenses still accounted for 33.6% in Q4 2024 (consistent with the previous year). However, Remitly said that it expects to see continued economies of scale as it grows its volumes. In particular, this allows it to secure better terms with pay-in and payout partners.

How Remitly is driving marketing ROI

Daniel Webber:

You spend money on marketing, but you’re also driving more efficiencies from it. How are you continuing to improve there?

Matt Oppenheimer:

I would say two things there. One that is foundational is word of mouth, and that goes back to what I said earlier. But we are seeing increased organic traffic. If you put it into context, we have 7.8 million quarterly active users.

We have about three million iOS App Store ratings at a 4.9 rating, and we have about a million Google Play ratings at 4.8 rating. You add that up, it’s four million of 7.8 million quarterly active users that have proactively gone and given us a strong review.

Quarterly actives is smaller than annual actives, so put that in context. A lot of customers are practically saying, “I love this product, you’ve got to try it out”. And that’s also happening organically within the communities they live in. By having that, we naturally get more leverage on the marketing line item, because we’re growing via organic traffic that is founded in having a great product.

Overlap that with a marketing team that is executing. I mentioned a campaign we did in the Philippines for Christmas, just as one example. When we talk about an integrated campaign in the Philippines for Christmas, it’s incredibly creative, strong, customer-centric marketing – from upper funnel on things like the Filipino channel, to middle funnel (Facebook etc) to bottom funnel in terms of paid search. That integrated approach just improves the return on the marketing dollars we’re spending and just continues to get better.

Inside Remitly’s growing efficiency

Remitly’s strong 2024 was reflected by the company’s growing efficiency. Net losses fell from -$35m in Q4 2023 to -$5.7m in Q4 2024, with net losses falling 69% for the full year to -$37m. The company now expects to see its first ever positive GAAP net income in 2025 – driven by positive quarterly net income from Q3 2025 – as it balances growth investments with operating efficiencies.

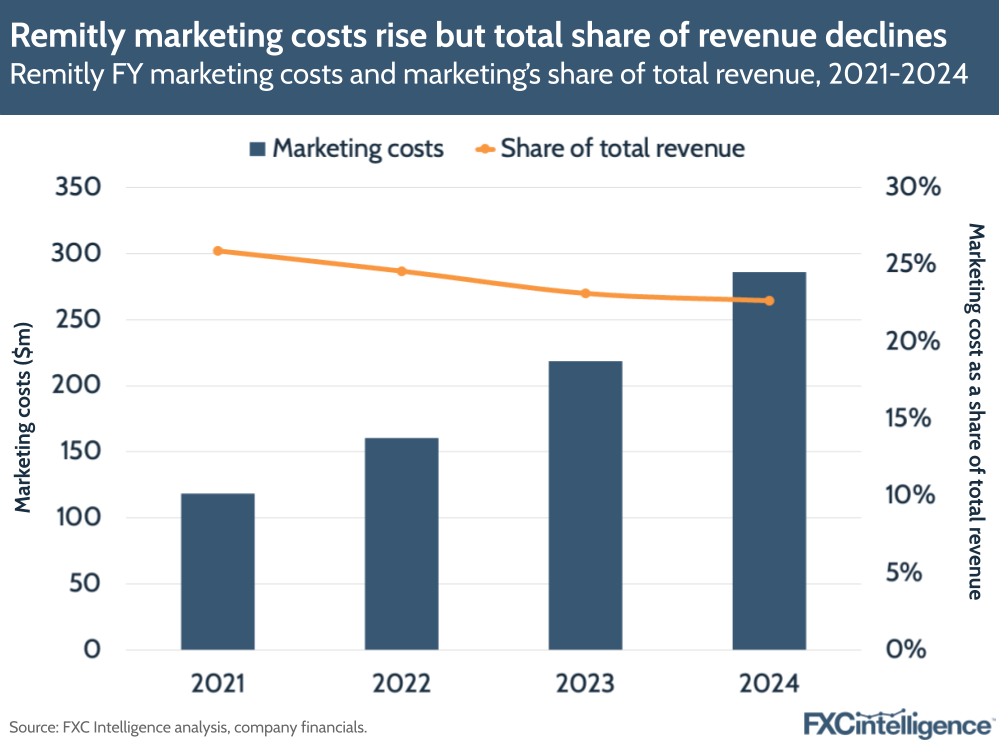

Remitly has taken a “disciplined hiring” approach and given cash in lieu of equity to new hires, which has helped drive its net burn rate down from 5.6% in 2023 to 4.9% in 2024. Elsewhere, customer support and operations and technology and development expenses improved as a percentage of revenue, as did marketing spending.

Though overall marketing spending rose in 2024, as a share of revenue it has continued to decline each year, from 26% in 2021 to 23% in 2024. Marketing expenses per quarterly active customer also decreased nearly 16% YoY in Q4 2024, and Remitly reported its lifetime value to customer acquisition ratio was driven to approximately six times.

Growing Remitly’s share of a multi-trillion-dollar market

Daniel Webber:

You’re still under 3% of a $2tn market that’s continuing to grow, while the US accounts for about two-thirds of the business. Talk us through how you’re thinking about growing into the next part of the market.

Matt Oppenheimer:

One thing I love about our business is obviously we’re a growth company, but we also have no shortage of growth opportunities. So, there’s lots of opportunity to continue to grow in markets we’ve been in for a long time. There’s new markets that we’ve recently launched and new regions where we just have a lot of room to grow. I’ll look at Africa receive as an example.

Then you layer on adding additional services to our existing customers, which is part of our vision and we’re excited about, as well as adding completely new customer segments, whether it’s seafarers, high-dollar senders or microbusinesses that I talked a little bit about on the call. There’s lots of opportunity to grow.

One of the things that we have been disciplined about over the last 14 years is investing in the right portfolio of horizons in terms of growth. What you see this year is investments that’ll return good growth and profitability in ’25, but we’re already thinking about ’26, ’27, ’28 and some of the investments there to be able to continue to drive growth in the long term.

Diversifying Remitly’s revenue mix

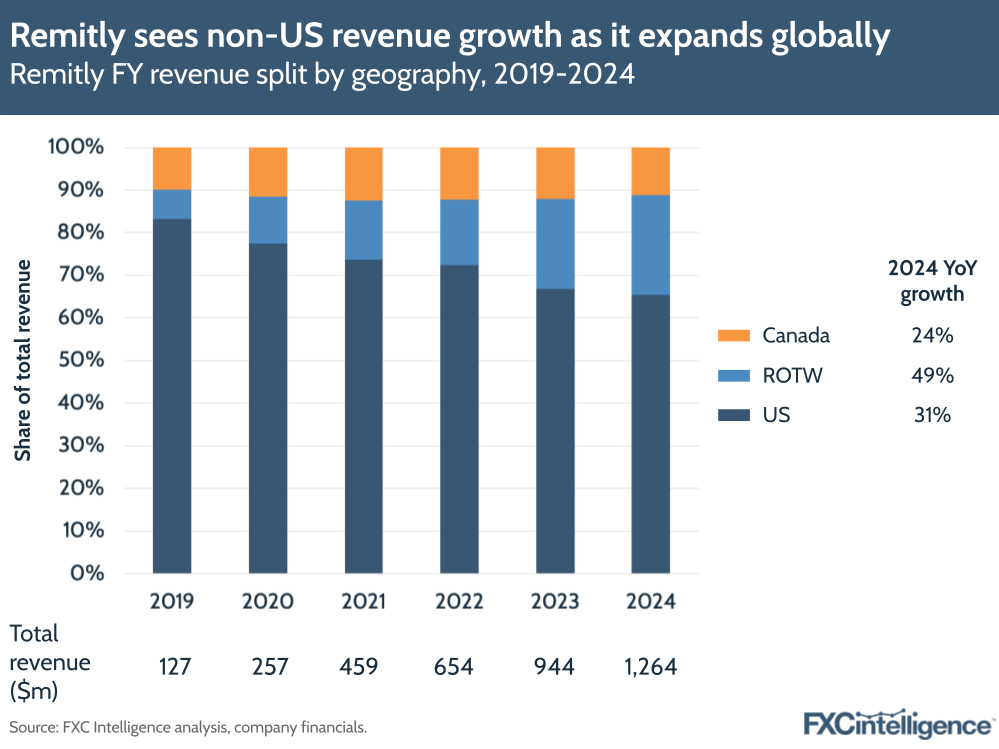

Remitly’s geographic revenue mix has significantly shifted over time as the company has diversified its product offering, added new partners and grown its customer base globally.

In 2024, revenue from US-based customers grew 31% in 2024 and accounted for 65% of total revenues, down from 83% in 2019. By comparison, rest of world revenues grew 49% and accounted for 24% of revenues in 2024, compared to just 7% in 2019.

The change in mix reflects Remitly’s growth in existing markets while entering new ones, with the company seeing a wave of new partnerships in Q4 2024 (e.g. Wave in Senegal and TMoney in Togo). According to Remitly, it still only has a 3% share of a $2tn remittances market, signalling significant room for expansion.

Expanding services for existing and new customers

Daniel Webber:

You said you were remaining “thoughtful” about expanding your services for existing and new customer types. What goes into the thoughtful process for you?

Matt Oppenheimer:

One thing is looking at where we uniquely have the right to serve customers better, and that’s in financial services that transcend borders, so we’re squarely focused on that area of our vision. And then, it’s also leveraging the platform we’ve built to be able to make adjustments to our product so that microbusinesses can use it.

Microbusinesses actually share a lot of similarities (in terms of the customer experience) to a consumer that needs adjustments to the product to do things, like know your business (KYB), as opposed to know your customer (KYC).

When we say thoughtful, we’re also steering clear of areas like small and medium business or larger-scale businesses that are served well by other companies. That’s at the heart of what good strategy and good focus is. The great news is that with that focus, there’s no shortage of growth opportunities. We’re just prioritising the ones that we believe we have the best ability to serve customers in.

How AI is driving productivity at Remitly

Daniel Webber:

You mentioned AI 27 times in 2024 earnings calls, which is more than in 2023. How are you using AI and how are you adapting to the change that’s happening in the AI market at the moment?

Matt Oppenheimer:

I love that you counted! It’s actually really indicative of who we are as a company, which is that we’re going to talk about things when they are real and when they matter to customers. We’re not going to talk about it before or be a speculator – but if you look at some of the things we’re doing in AI now and it’s really exciting.

Our virtual AI assistant, which is live serving customers and continues to roll out to more use cases, is incredible. When you look at both the efficiency and the customer satisfaction scores, and look at how our team is using it, whether that’s our CS agents, our engineers or myself, it’s just improving productivity across the board.

The reason we’re talking about it more is because I’m genuinely excited about the early reaction that we’re seeing, in terms of the return and the experience, and there’s a lot more to come.

AI helps decrease customer support costs

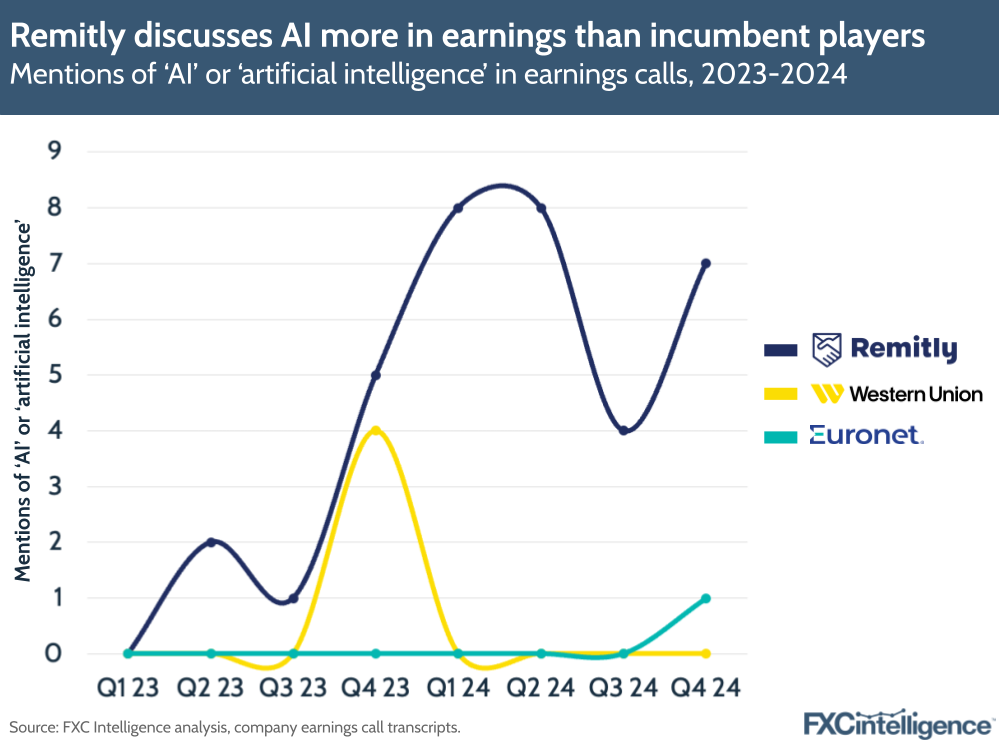

AI is being discussed significantly more in Remitly’s earnings calls than other incumbent publicly traded players in the remittances space – specifically Western Union and Euronet. This trend continued this quarter, bringing the total number of mentions of AI to 27 for Remitly in 2024 earnings, versus 8 the year before.

Remitly said in Q4 that its AI-based virtual assistant is helping the company lower agent contact rates and improve customer satisfaction, contributing to a reduction in customer support and operations costs as a share of revenue from over 10% in 2022 to 6.5% in 2024.

Daniel Webber:

Anything else you’d like to add?

Matt Oppenheimer:

I would say two things. One, as we reflect on ’24, I’d like to express huge gratitude to the team. Our growth rate, scale and size relative to the rest of the industry is because of their hard work every day serving our customers. It’s a tough, complex business and they’re very good at what they do and they work incredibly hard.

One of the unique things about our culture is that we’re a mission-driven company and we focus a lot on our customers. Our mission is to transform lives with trusted financial services that transcend borders.

Millions of customers are using our platform, which is [becoming] increasingly diverse in terms of the type of customers we serve, and they’re incredible. We’re here to serve them, we’re here to continue to grow and we’re here to continue to transform this industry.

Daniel Webber:

Matt, a pleasure as always. Thank you

Matt Oppenheimer:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.