Ripple has released key details of its global payments-focused, US dollar-pegged stablecoin Ripple USD only days after it received a long-awaited ruling in its SEC case. But can RLUSD help win back the industry?

After previously announcing that it was planning such a launch, crypto payments fintech Ripple has announced that it has begun testing its stablecoin Ripple USD (RLUSD), as well as laying out key details in a dedicated webpage and blog post.

Although not yet for sale or available to trade, RLUSD is in its beta phase, with the company saying it is being “rigorously tested” on the two blockchains it will initially be released on. Issued by Standard Custody & Trust Company, which Ripple completed the acquisition of in June, Ripple USD is set to enter an already fairly crowded USD dollar-pegged stablecoin market but is characterised as “purpose-built for payments”, augmenting Ripple’s wider offerings in the cross-border payments space.

“This is a pretty significant strategic move for us,” said David Schwartz, CTO of Ripple, in a discussion about the launch for the company’s podcast Block Stars.

“For a while we’ve used a combination of assets in things like on-demand liquidity, now Ripple Payments: XRP, fiat, stablecoins. We’ve built those into cross-border solutions to provide the best experience for our customers. And in emerging markets, we’ve seen a demand for stablecoin payouts in lieu of local fiat currency.”

It comes at a time when Ripple is looking to re-engage with parts of the cross-border payments industry, particularly in the US. The company was once heralded as a key player in the future development of the space, but saw a drop in industry support following the late 2020 filing of a lawsuit by the US Securities and Exchange Commission (SEC) over whether its cryptoasset XRP was an unregistered security. Last week, just two days before it announced it had started testing RLUSD, Ripple saw a partial win when the court returned a split decision, crucially ruling that XRP was not a security and ordering Ripple to pay $125m in fines related to early sales – much less than the $2bn the SEC had sought.

As it faces the prospect of a post-lawsuit future, Ripple has already begun to re-engage with the cross-border payments industry, particularly in the US where only 10% of its business is located at present. The company currently has a very small share of flows in the global cross-border payments market, which overall totaled $190.1tn in 2023, according to our Market Sizing Data.

In pursuit of this, earlier this year the company rebranded its cross-border solution RippleNet to Ripple Payments, refocusing it on the enterprise space. The rollout of its stablecoin looks set to develop this further, at a time when fully regulated, asset-backed stablecoins are being increasingly used by some players to serve as the underlying infrastructure for global payments.

In this report, we explore Ripple’s payments background, its place in the market and the potential of its stablecoin offering for cross-border payments.

From XCurrent to Ripple Payments: Ripple’s evolving payments offering

The move follows a tumultuous few years for Ripple and comes as it looks to be trying to re-engage traditional payments companies.

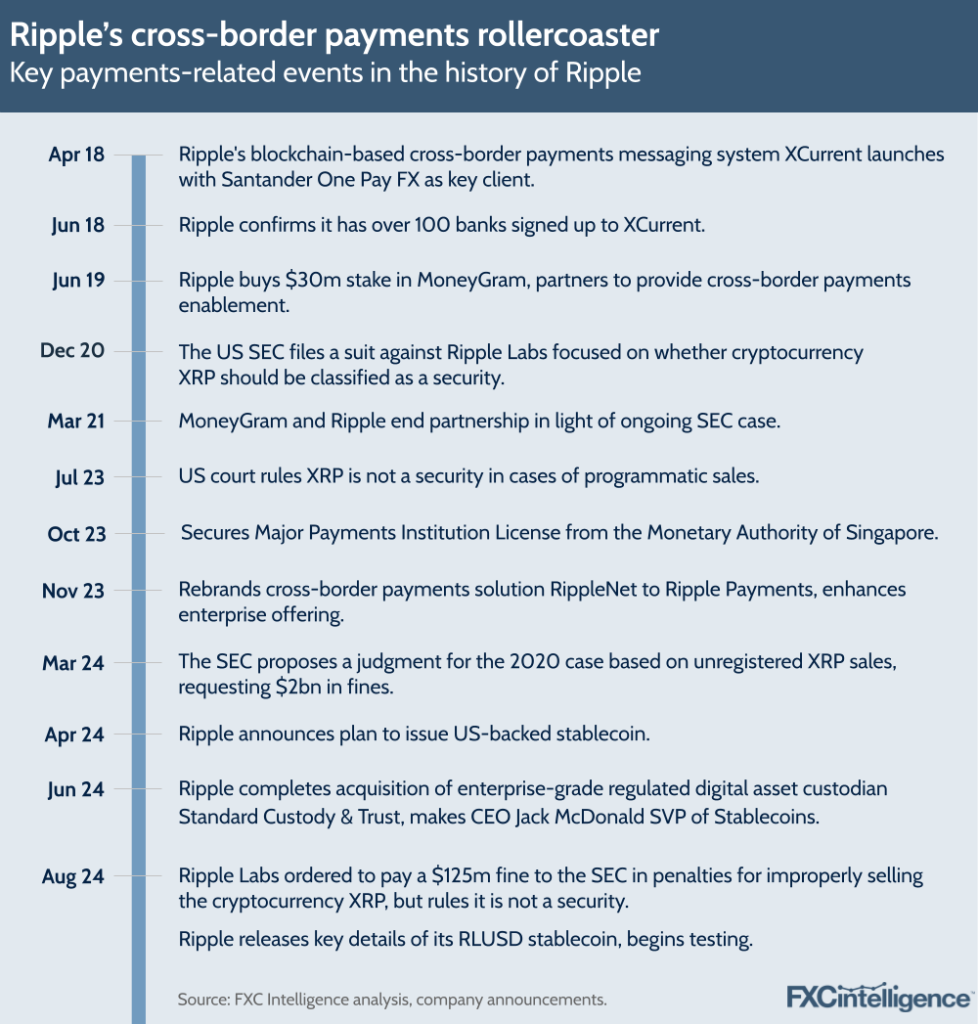

Back in 2018, the company had a very different reputation with such organisations. In April of that year, it made waves within the cross-border payments industry when Banco Santander announced the launch of its OnePay FX service, powered by Ripple’s blockchain-based cross-border payment messaging service XCurrent.

Ripple at that time already offered a full cross-border payments service using its XRP cryptocurrency, where XRP served as a token to move value across the company’s decentralised public blockchain XRP Ledger (XRPL). This had been developed from Ripple’s founding concept of “the decentralised exchange on XRP Ledger and the concept of IOUs”, according to Ripple President Monica Long (also speaking on the Block Stars podcast), which she described as “probably the first stablecoins in crypto”.

“The vision was to create issued assets onto the ledger, and built into the ledger was an order book that would be a really efficient liquidity mechanism for these different assets,” she added. “This is how the ledger would ultimately facilitate efficient transactions, and in particular payments.”

However, banks favoured the messaging-only XCurrent due to the lack of volatility involved, and within months Ripple had signed up over 100. The news garnered considerable industry attention, with many seeing Ripple as a major technological challenger in cross-border payments, and that same year the company was the focus of a Financial Times article that characterised it as being in a boxing match with Swift.

In 2019, Ripple cemented its place as a player in the payments industry when it took a 10% stake in traditional remittances player MoneyGram for $30m, alongside a partnership that saw it provide blockchain-based settlement services for the company through its XRP-based payments solution RippleNet. This was something that MoneyGram CEO Alex Holmes would retrospectively describe as “incredibly successful” at the time, despite bringing to light some previously unconsidered challenges, particularly around the use of XRP.

As it entered 2020, Ripple’s enterprise customers stood at around 300 and the company’s valuation climbed $10bn when it raised $200m in a Series C funding round. Notably, much of this valuation was drawn from its holdings of XRP currency: XRP had now hit a market cap of around $12bn and Ripple owned around 60% of XRP.

However, Ripple was about to hit a roadblock that would all but derail its fast-growing position within the mainstream cross-border payments space.

Ripple’s SEC case

In late December 2020, the SEC filed a lawsuit with Ripple concerning the early sale of XRP to public investors by two executives: Chris Larsen, Co-Founder and then CEO of Ripple Labs, and Brad Garlinghouse, CEO of Ripple. The SEC argued that the fact that XRP was at the time centrally controlled meant that XRP should be treated as a security and that it was therefore, crucially, an unregistered security. Ripple, meanwhile, countered that as a cryptocurrency, XRP was a commodity, not a security.

The market reaction was significant. XRP saw its value drop significantly on the news, and major payment players who had previously touted partnerships with Ripple began to distance themselves from the company. At its next earnings call, MoneyGram confirmed that it had ended its partnership with Ripple and would no longer be using RippleNet to facilitate its payments. Crypto companies also sought to protect themselves, with several exchanges, including Coinbase, suspending XRP trading in early 2021.

Over the next few years, Ripple conducted a lengthy legal battle with the SEC, gaining support from other key figures in the crypto industry, including Coinbase CEO Brian Armstrong, as the company sought to frame the lawsuit as a threat to the crypto industry as a whole.

Meanwhile, many payments companies, particularly those in North America and Europe, increasingly looked to sever ties with Ripple, seeing the lawsuit as too much of a reputational and operational risk. It also – along with several other later incidents, including most recently the collapse of FTX – led many Western payments companies to avoid any direct contact with cryptocurrencies that didn’t have a fiat peg.

As Ripple continued to fight the lawsuit, it focused its business development efforts on Asia and other non-Western markets, gaining several key payments customers in the region and ultimately gaining a Major Payments Institution Licence from the Monetary Authority of Singapore.

As 2023 progressed, the lawsuit began to see some momentum, and in July 2023, the judge on the case, Judge Analisa Torres, ruled that XRP is not a security in the context of programmatic sales, isolating the lawsuit to the early direct-to-investors sales – something that Ripple touted as a key win for the crypto industry and enabled it to relist the cryptocurrency on exchanges.

As the case began to enter its final months, in March 2024 the SEC – having already voluntarily dropped charges against Garlinghouse and Larsen directly – proposed a judgement on Ripple based on the premise that the early direct sales did treat XRP as a security and so were unregistered. On this basis, it proposed a fine of almost $2bn.

However, on 7 August Judge Torres issued a split decision, finding partially in favour of Ripple. While the court ruled that select early sales of XRP constituted securities offerings, it determined XRP was not a security and imposed a $125m civil penalty on the company – significantly lower than the SEC requested.

While the SEC may still appeal, the ruling is being seen as providing vital regulatory certainty to the crypto industry and begins to draw to a close the biggest event in Ripple’s history. Most importantly, it enables Ripple to begin to re-engage with parts of the payments industry who were unwilling to work with the company while the legal outcome was uncertain. And the company has already begun to lay the groundwork in anticipation.

Ripple Payments: Re-engaging the cross-border payments industry

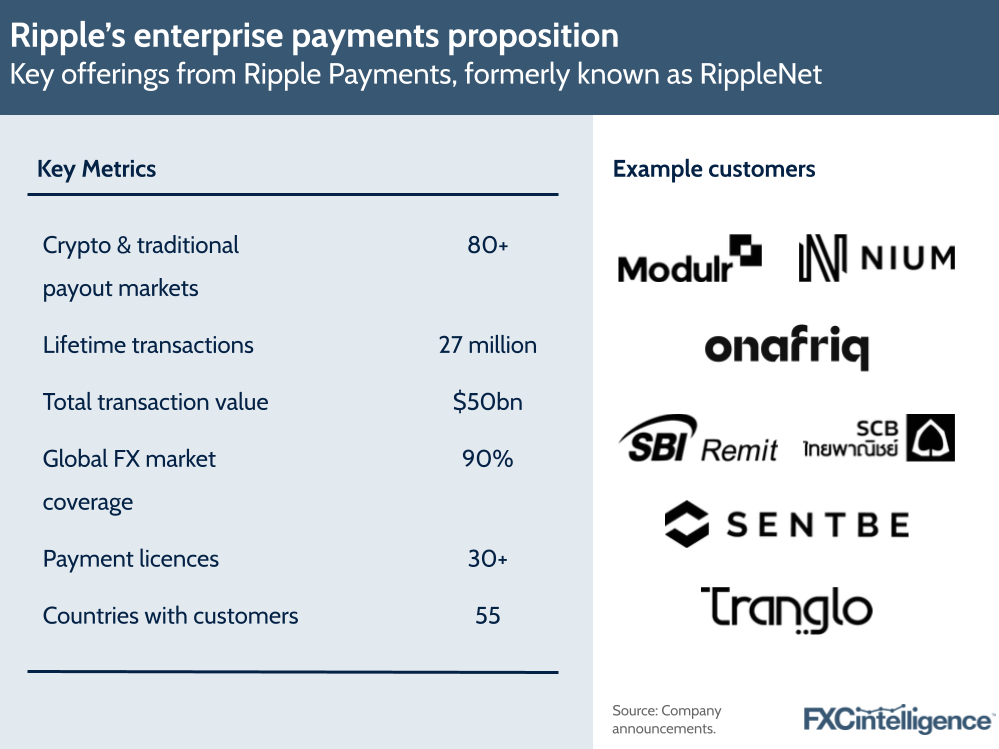

Ripple has already begun to make moves to re-engage enterprise players in the cross-border payments space, most notably with the November 2023 rebranding of its cross-border payments solution RippleNet to Ripple Payments.

From a marketing perspective, the name change frames the product in a less crypto-focused way that may be more appealing to mainstream payments companies, but it was also accompanied by several product enhancements designed to appeal to enterprise customers in particular.

Here, Ripple touted new integrations to its decentralised exchange, which it said would make it easier for companies to access global liquidity and therefore new markets, as well as improved onboarding and broader access to the 80+ crypto and fiat markets the company has access to. It also highlighted the service’s 24-7-365 operation across all markets – an implicit contrast to the time restrictions present in some fiat markets – as well as highlighting the 30+ licences the company has, including its recently acquired Singapore MAS licence and those it holds in the US.

“Since the start, Ripple focused on creating products that solve real problems for real customers,” said Long in a press release about the development at the time of the announcement.

“This evolution of Ripple Payments represents an extension of our long-running work to optimise the cross-border payments experience through transformative technology.”

Since then, there have been further signs of the company looking to re-focus on parts of the market that it lost the attention of during the SEC suit. In February of this year, W. Oliver Segovia, Ripple Senior Director and Head of Product Marketing – Payments, Custody, & Stablecoin, confirmed that 90% of the company’s business was outside the US, but said that Ripple was looking to change that, starting with a meetup at the company’s San Francisco headquarters.

Focused on the blockchain and payments outlook for 2024, the meeting was attended by companies including Adyen, Marqeta and Plaid, and is expected to be the first of several efforts to boost US and broader Western enterprise interest in the company’s payments offerings.

“After being relatively quiet for the past three years in the US for Ripple Payments, we’re geared up to announce new product updates, powered by our money transmitter licences that cover the majority of US states,” wrote Segovia ahead of the event.

Around a week later, the company reaffirmed these plans when it announced plans to acquire Standard Custody & Trust Company, a US-based enterprise-grade regulated custodian for digital assets. Completed in June, the acquisition bolstered Ripple’s US licences, meaning the company now holds almost 40 across the US as well as several internationally.

RLUSD: Ripple’s stablecoin offering

Ripple first announced that it would be launching a stablecoin in April 2024, citing projections that the $150bn stablecoin market would climb to $2.8tn by 2028. However, last week the company provided further information on the product with the launch of a stablecoin section on its website alongside a blogpost announcing that it had begun testing RLUSD.

Set to be pegged 1:1 with the US dollar, Ripple USD will be “100% backed by US dollar deposits, short-term US government treasuries and other cash equivalents”, according to a LinkedIn post by Segovia.

RLUSD will initially be available both on Ripple’s own decentralised public blockchain XRPL as well as the Ethereum blockchain, with Ripple saying that “enterprise partners” were currently testing the stablecoin on both. The company also said in April that it ultimately planned to expand the stablecoin to further blockchains and decentralised finance protocols at a later date, something that it reaffirmed in the recent blogpost.

Ripple has not yet confirmed a final release date for Ripple USD, although the stablecoin is expected to go live for public use this year.

In the April press release announcing the stablecoin, CEO Brad Garlinghouse characterised the move as a “natural step for Ripple to continue bridging the gap between traditional finance and crypto”.

“Institutions entering this space are finding success by partnering with compliant, crypto-native players and Ripple’s track record and resiliency speaks for itself, as we launch new products and acquire companies through multiple market cycles,” he added.

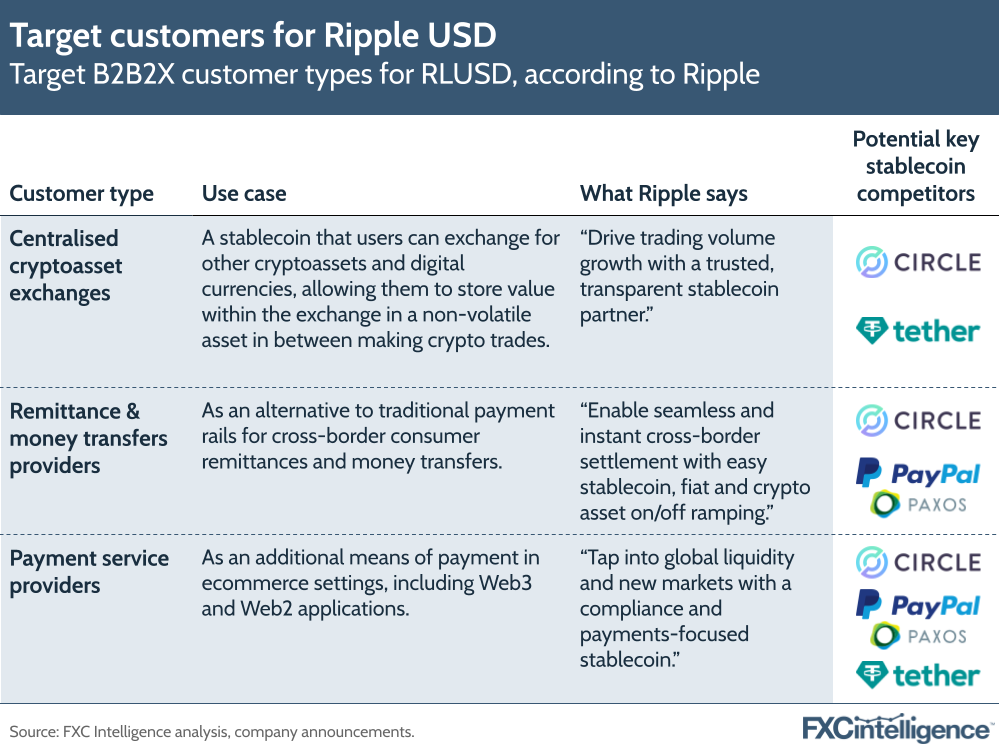

While the April press release highlighted the stablecoin’s role in driving more adoption and development on XPRL, the focus of the webpage is more on non-crypto benefits, with the three business use cases cited as remittances and money transfers, centralised exchanges and payment service providers.

Here the company highlights the benefits of instant settlement – a feature of all stablecoin-based money transfer solutions – alongside deep liquidity, which is vital to the success of any stablecoin used in the payments arena, particularly when serving enterprise-level clients.

Ripple USD’s cross-border payments potential

There are benefits in a stablecoin for crypto-native players, particularly those who are serving markets with volatile fiat currencies.

“A beneficiary might be in a market where they would prefer to receive payment in a US dollar stablecoin than in their local currency,” explained Long. “These are markets with very volatile domestic currencies, so that’s one example where we see more of a need for it.”

There is a similar potential for non-crypto players serving such emerging markets, but there is also growing potential for stablecoin’s broader use among non crypto-focused enterprise customers, many of whom are increasingly exploring the use of distributed ledger technologies for financial applications. Here, Ripple cites its own research that found that 80% of global finance leaders are “likely to begin using cryptocurrencies, CBDCs and/or stablecoins in their business in the next three years”.

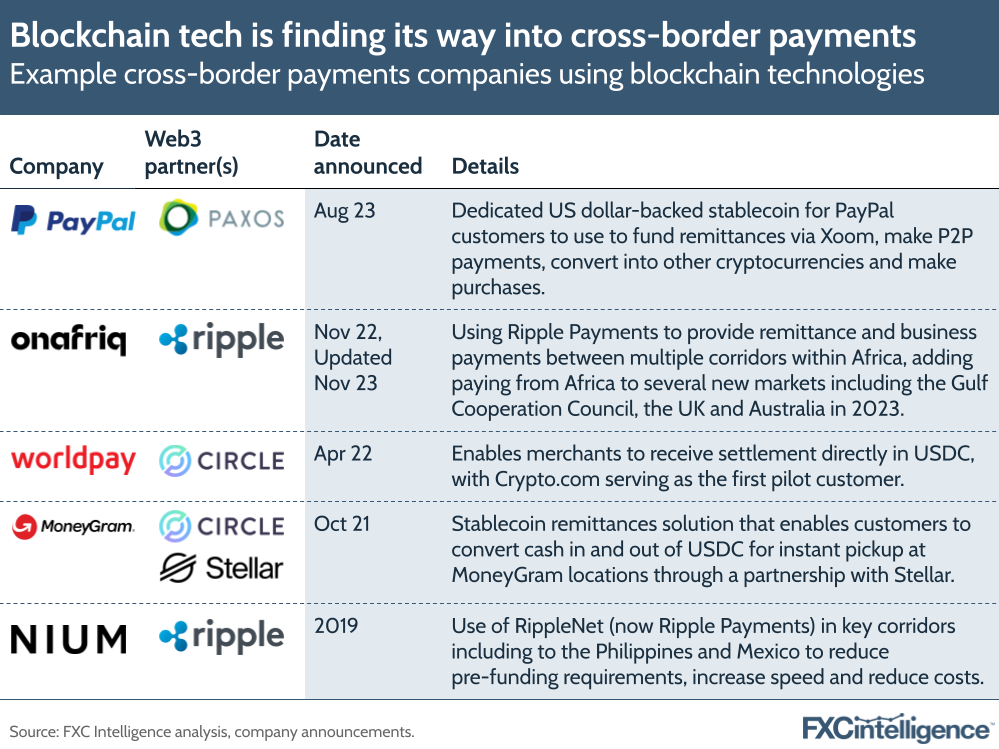

Even if this proves to be an optimistic projection, many in the payments space are looking at the technologies surrounding cryptocurrency – but not necessarily the currencies themselves – as a serious option. Growing numbers of companies are incorporating some forms of blockchain-based rails into select parts of their network, and there are a small but growing number of players actively offering stablecoin-based remittances as all or part of their service.

Having severed ties with Ripple as a provider, MoneyGram did return to crypto, with the launch of a stablecoin-based remittance service in 2022. Delivered using Circle’s USDC stablecoin on Stellar’s blockchain network, the service was built on the lessons learned from its prematurely ended partnership with Ripple, with Holmes touting blockchain-based real-time settlement as “much more effective” than traditional settlement solutions, which generally have a notable delay between the recipient receiving their money and it being fully settled locally for the provider.

“If you could actually match your settlement through the blockchain with every transaction you were doing, you would be actually buying and selling real-time and matching off your transactions,” said Holmes in a 2022 interview.

“You can do [this] on the blockchain and you can do [it] through crypto and you cannot do [it] in the fiat world today.”

Such settlement benefits have significant financial implications when operating at scale, and are one of the key reasons why blockchain-based solutions are seeing growing interest from non-crypto-based players. Other benefits include the ability to avoid market-specific challenges, such as the need to pre-fund and slow local infrastructure.

However, negative perceptions and regulatory uncertainty around non-fiat-backed cryptocurrencies have made any solution that makes use of them a challenge to sell in the West in recent years. A stablecoin may therefore be a critical component for Ripple to effectively capture this market – particularly in the US where it is focusing attention.

Long alluded to this, saying, “The other kind of broad use case [for Ripple USD] we see is that there’s more and more interest in the network on-off ramps that we’ve built over the years.

“We see a lot of utility for XRP Ledger in financial use cases; one of the use cases it has been best-in-class at since the beginning is payments.”

The Standard Custody acquisition and compliance implications

As Ripple looks to appeal to the mainstream financial industry in the US and beyond, its acquisition of Standard Custody is likely to prove critical. It is certainly vital to its ability to launch RLUSD: not only is Standard Custody the stablecoin’s formal issuer, but CEO Jack McDonald has also been appointed as Ripple’s Senior Vice President of Stablecoins in addition to his current role.

This speaks to Standard Custody’s place in Ripple’s stablecoin strategy, and also its view of the project. Not only does the company bring vital technological expertise in the space, but its highly enterprise-focused approach means it is well-positioned to address the parts of the market that cut ties with Ripple over the SEC case.

“Standard Custody provides financial institutions with the confidence and platform to safeguard their digital assets,” said McDonald in a press release announcing the acquisition.

“Ripple continues to lead the industry with its deep crypto expertise, relationships with financial institutions and strong product offerings, across both payments and custody. Together with Ripple, we will further innovate and extend our leadership position in providing crypto infrastructure.”

A Qualified Custodian under US federal law, Standard Custody has been granted charter status by the New York State Department of Financial Services (NYDFS), allowing it to offer custodial and escrow services.

“The NYDFS is widely regarded not just in the US but internationally as a very robust regulator,” said Long of the acquisition. “We’re holding the gold standard in mind in how we’re building and how we will be regulated.”

While Standard Custody’s more institutional focus will likely prove a benefit, its compliance experience is likely to be essential. Ripple has been very keen to highlight its regulatory compliance in the launch of its stablecoin as it seeks to shift its market image away from the SEC case.

“Compliance is something that is going to be paramount, especially if we see more enterprise users of stablecoins and of blockchains for financial use cases,” said Long.

“It’s something you can’t compromise on and it has to be rock solid, air tight.”

The wider stablecoin market: Key competitors

While RLUSD will be the only major US dollar-pegged stablecoin available on XRPL, it is not the only stablecoin in circulation, and faces some tough competition along a number of lines from other key players in the industry.

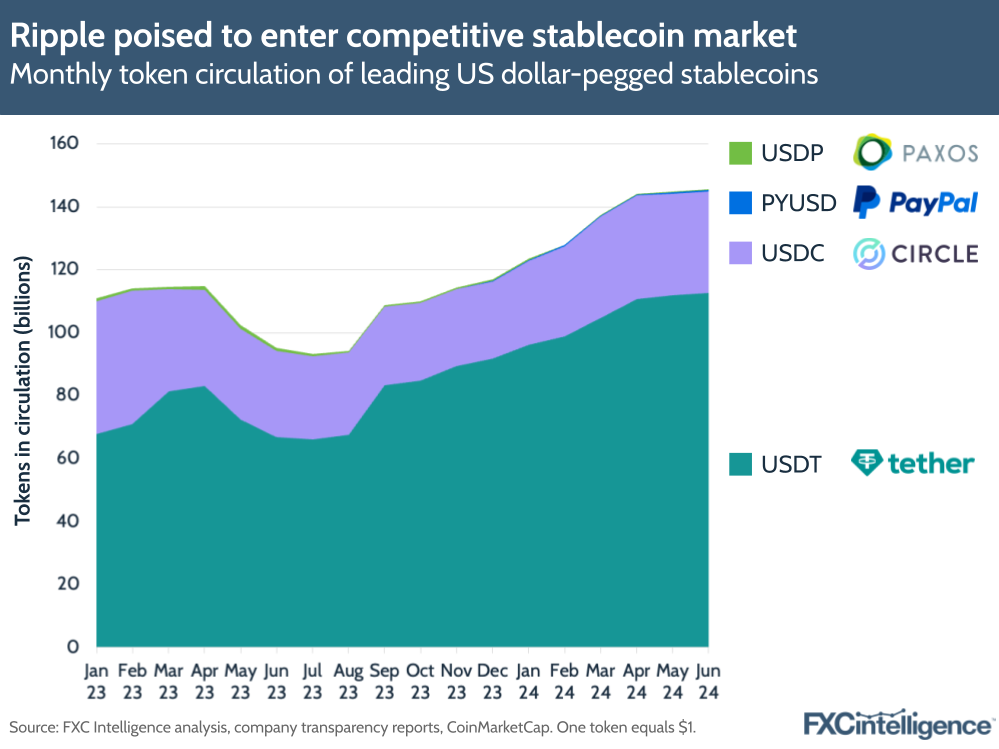

In terms of circulation, the two largest US dollar-pegged stablecoins currently available are Tether’s USDT and Circle’s USDC. At the time of writing, Tether had an estimated market cap of around $116bn, slightly up from the c. 112 billion tokens pegged 1:1 with the US dollar that the company reported being in circulation at the end of June.

By contrast, Circle reported having around $32bn worth of the USDC stablecoin in circulation at the end of June.

The most recent entrant to the market, PayPal’s Paxos-issued PYUSD, has already grown to third place, having climbed from a circulation value of $44m in its first reported month in August 2023 to $499m in June 2024. Meanwhile, Paxos’s own stablecoin USDP had a circulation value of $122m, having seen a decline in circulation over the past year.

The Binance USD (BUSD) stablecoin remains relatively close behind, despite its issuer Paxos halting minting of new tokens in February 2023 at the instruction of the NYDFS, with a circulation of around $71m that has been unchanged since April 2024.

The significant combined market cap is aided by the fact that stablecoins in general have already proved their value in the decentralised finance (DeFi) space, which has driven much of the overall market growth.

“Right now DeFi does need on-ramps and off-ramps that are reliable and efficient, so that’s mostly been in the form of stablecoins,” said Long.

“We also see the need for the world of crypto to have reliable, compliant stablecoin offerings. The two that have been most prominent, USDC and USDT, they’ve been around for a while, but we do think that there’s space and opportunity and that the market needs to see more high-quality offerings, so that’s where we come in.”

Which stablecoins are suitable for cross-border payments?

However, while all of the current offerings are US dollar-pegged stablecoins, their nature and therefore utility varies quite substantially, with only some being suitable for use by companies within the cross-border payments space.

Despite being the largest, and highly popular with both crypto traders and some in the DeFi space, USDT is unsuited to many applications within the cross-border payments industry because of the way its value is maintained.

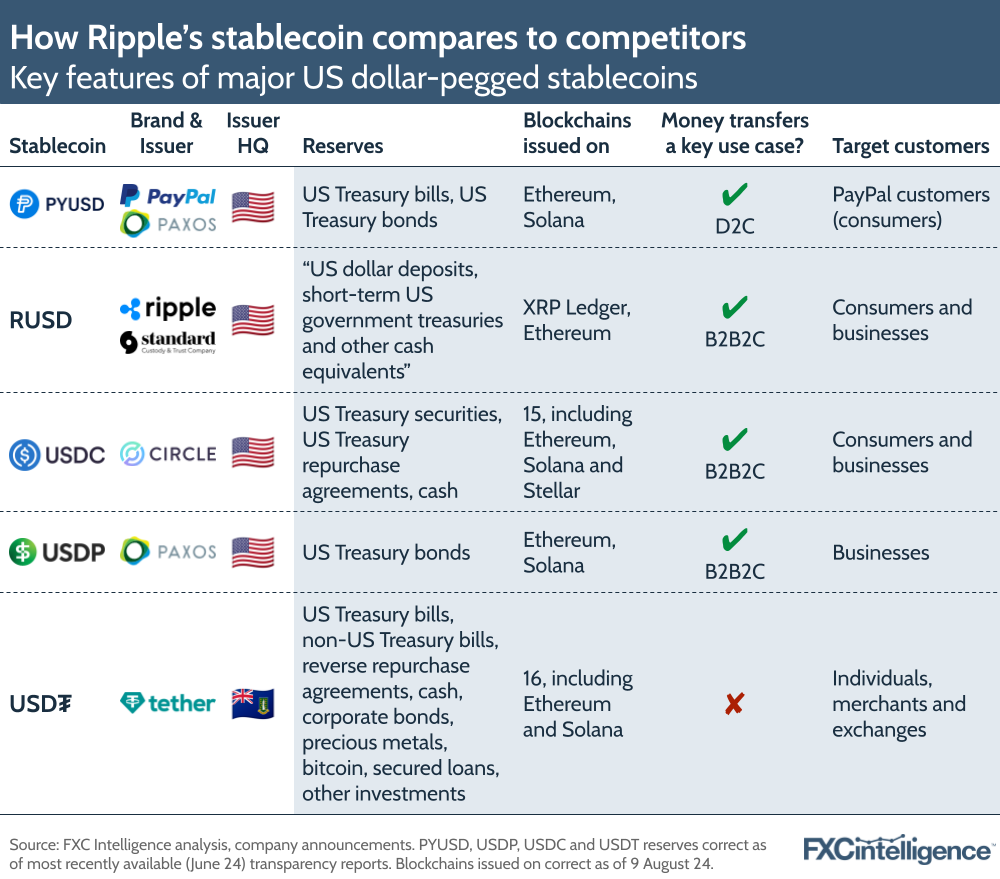

PYUSD, USDP and USDC all maintain their value through reserves held in a mixture of cash, US Treasury bonds, US Treasury bills and other related US Treasury securities. Which of these are used and in what ratios varies slightly by stablecoin, but in all cases the reserves are selected because they are a good direct representation of US dollar value and can be quickly converted in cases where there is a sudden surge in demand. In support of this, current numbers of tokens issued and the reserves supporting them are audited on a monthly basis, with transparency reports published on the respective companies’ websites in compliance with US law.

RUSD is expected to be backed in much the same manner, with the same types of transparency reports made available at the same cadence.

By contrast, while USDT is backed by reserves detailed in transparency reports, these are only published once every three months, and the assets that form the stablecoin’s reserves are far broader. In addition to US Treasury bills, they also include other currency Treasury bills; corporate bonds; precious metals; and Bitcoin, among others.

This means that while many organisations globally, particularly those in the Web3 space, are happy to use USDT, Western organisations and traditional financial institutions will generally be unable to make use of this particular stablecoin as it does not fully meet certain regulatory and operational minimums.

Organisations have become especially cautious about the particulars of stablecoins since mid-2022 when then popular stablecoin TerraUSD (UST), which used an unconventional algorithmic backing, experienced a sudden and dramatic collapse where it lost its peg, dropping each token’s value from $1 to less than 10 cents. In the following days, as the market reeled, USDT also briefly lost its peg, dropping to $0.95, before recovering.

Beyond robust backing, not all stablecoins are suitable for being used as part of payments infrastructure. PayPal USD is already in use for consumer payments, but is largely designed for this within the company’s own walled garden of infrastructure and is not intended to form part of the payments rails for other organisations, some of whom may be the company’s direct competitors.

USDC and USDP are better suited to serve as financial infrastructure, with the former already being used for this purpose by a number of players. Here USDC’s higher circulation provides greater liquidity, which can be key, and its broader range of blockchains are also a benefit.

Not all blockchains are well placed for payments, and different types may be better suited to payments of different sales. Ethereum, a blockchain used by all of those above as well as RLUSD when it launches, is well liked for its high liquidity – measured by a metric known as total value locked (TVL) – as well as its stability and decentralisation. However, it has lower speeds and scalability than some other blockchains, as well as having comparatively high network fees.

By contrast, Solana has lower TVL than Ethereum and is more centralised, with poorer reported stability. However, it has a higher network speed due to its more advanced consensus algorithm, allowing it to process a much greater number of transactions: 2,600 per second, compared to just 15 on Ethereum. It also has considerably lower transaction costs. While RLUSD will not be initially available on the Solana blockchain, all other major stablecoins are available on it and Ripple may see Solana as a key choice when it comes to rolling out the stablecoin further.

Despite there being multiple stablecoins in the market, USDC is likely to serve as RLUSD’s clearest and most direct competitor for most payments-related applications due to its combination of high levels of regulatory compliance; prominence in the market; liquidity; and established use cases. However, USDC does differ in one crucial aspect from RLUSD, in that Circle does not also offer its own blockchain.

By being able to offer both the rails (its XRPL blockchain) and the token that can move along those rails (RLUSD) for cross-border payments companies, Ripple is positioned to be able to provide a complete solution, rather than needing to partner with other providers, such as Circle’s Ripple partnership to supply MoneyGram.

Implications for Ripple’s XRP

While RLUSD can serve as an alternative to XRP when it comes to moving value on Ripple’s XRP Ledger and beyond, the company was keen to stress that the stablecoin is not a replacement for the cryptocurrency – but an alternative.

“For our payments customers, we’ve supported various tokens in the payment flow. Of course, XRP is a bridge asset, and that position for XRP doesn’t change in our view,” said Long.

She sees XRP continuing to be key here, particularly as growing numbers of different types of assets become tokenised on blockchains. As this happens, liquidity will be needed across “a longer and longer tail of different types of assets” – a challenge that Long says XRP is well-placed to support.

“Even amongst the currencies, there’ll be different issuers of different currencies and the more that transactions happen, especially right on ledger with the decentralised exchange, there’ll be more and more demand for XRP as a bridge asset. That will continue.”

Potential for DeFi

While the stablecoin has potential for cross-border payments, it also has potential implications for the wider DeFi landscape.

“A view now is that if DeFi is going to work, it can’t be all digital assets and it also can’t all be one stablecoin, because if we’re going to build these decentralised, permissionless public blockchains and the assets on them that are controlled, that kind of defeats the point of them being permissionless,” said Schwartz, speaking on the company’s podcast.

While he acknowledged that some people were “surprised by the timing” of RLUSD’s launch, he argued that it follows the rollout of other key DeFi products that the stablecoin will provide benefits to.

In particular, he pointed to the company’s Automated Market Makers feature, as well as its On-Chain Lending Protocol, both of which were launched on Ripple’s XRP Ledger in H1 2024.

The former provides crucial liquidity in the XRP Ledger’s decentralised exchange, and benefits from the launch of a stablecoin because unlike some crypto, it is a viable counter asset to every other asset on the exchange, creating the opportunity for between-asset markets to be created. Meanwhile, the latter allows the creation and issuance of fixed-term loans on XRPL, with the use of stablecoins ensuring that lenders aren’t negatively impacted by volatility in the assets they are loaning.

More broadly significant, however, is the fact that stablecoins are already widely used in DeFi applications – and having its own allows Ripple to more effectively play in this space.

“If you look at DeFi as a whole category, a lot of the total value locked is in USD stablecoins, so it’s a really critical piece of infrastructure for on and off ramps to make any ledger more useful,” said Long.

Here, Ripple sees potential for Web3 players looking to serve financial institutions, particularly around applications such as tokenising equities, bonds and similar.

Can a stablecoin help Ripple rebuild?

As it faces the prospect of a post-SEC case world, Ripple now has both the opportunity and the challenge of re-engaging with an industry that has in many ways moved on from where it was when Ripple was forced to part ways with it three and a half years ago. While many of the same challenges remain, the network solutions on offer are considerably richer and broader than they were in 2020 and Ripple will need to work hard to make a case for its solutions, particularly given the residual concerns that the legal case will have left.

The use of a stablecoin is potentially a strong solution. When effectively regulated, US dollar-backed stablecoins have proved to have utility within cross-border payments and the wider financial space, and offering companies solutions built around RLUSD rather than XRP will do a lot to assuage concerns for many.

However, Long acknowledged that there are challenges ahead for the company, reflecting on its tumultuous past decade.

“If you think about the aspiration of Ripple and the industry overall to create the next age of the internet, the next stage of finance, what we and probably everyone else in the industry underestimated was the hard work of connecting blockchains to traditional financial rails,” she said, adding that both Ripple and the wider industry also did not expect how challenging the regulation piece would ultimately prove to be.

“It’s felt like a lot of thrash over the years of how different governments receive this technology, understandably wanting to really protect consumer interests – which we do too – but to find that way forward of sensible policy and regulation where we can reinvent finance in a way that’s helpful to people, brings down costs and makes things a lot more efficient.”

With this in mind, she highlighted that launching the Ripple USD stablecoin would come with its own challenges.

“It’s a big effort, not just from the technology side: the operation of it; making sure that we’re holding a tight line on compliance; that we’re giving a good experience to our customers with onboarding; and always laser-focused on maintaining the peg,” she said.

“We’ll be really focused on that and also connecting it with our demand side, the use cases like our payments flows.”

She accepted that there “will be demand in use cases for other types of stablecoins in the future”, namely those pegged to other currencies such as the euro, and indicated that the company was watching this area closely, but said that the priority for now was on the launch of RLUSD.

“More than ever, I’m more bullish about what the next one to two years holds for Ripple because of the payoff from all the work we put in.”