SMBs face additional challenges on cross-border payments. Looking back at FXC’s market sizing data and recent developments, we assess the unique challenges faced by SMBs, as well as how companies are currently serving this area.

Small and medium-sized businesses (SMBs) are crucial to global and developing economies, making up the majority of businesses worldwide. As digitalisation propels global growth, this is a market that payments companies – particularly money transfer providers – have continued to deliver and release services for over the past year.

Our recent report on market sizing showed that SMBs formed the second-largest TAM for retail cross-border payments. Though the SMB segment isn’t growing as fast as large enterprise, it is still developing significantly as digitalisation unlocks new opportunities and more software-as-a-service companies emerge.

While enterprises are sending larger amounts of money abroad, for SMBs, payments can be a barrier to going global in the first place. The cost and speed of these transactions are felt even more significantly, as are delays. If a transaction from a major client overseas arrives too late, it could damage a small business’ cash flow, affecting their ability to grow.

Many well-known cross-border payment specialists, such as Wise, have already built out their businesses to serve the needs of SMBs, though in some cases the goal has been to shift to businesses in order to serve the bigger large enterprise market. Having said this, many of the conversations we had with payments leaders last year – including OFX, Payoneer and Sunrate – involved discussions about the importance and opportunities of targeting smaller businesses.

This report looks more closely at the SMB payments market, asking how large the cross-border opportunity is versus other sectors and analysing the strategies of various companies targeting this audience.

Defining SMBs

Our definition of SMBs focuses on companies with fewer than 250 employees. There is some broad discussion, including at a governmental level, about the differences between SMBs and small and medium enterprises (SMEs), with some using the terms interchangeably and others saying that there are differences between their relative sizes, as well as the sectors that they cover.

In order to provide clarity in this report, we have encompassed products and solutions that are specified for SMEs as well as SMBs. From a cross-border payments perspective, we are referring to companies that have likely built a customer base and revenue stream that has enabled them to expand to other markets globally, but are smaller than large corporations.

Tracking an evolving SMB payments landscape

Having an established base is a given for companies that want to expand abroad, but a number of factors are helping drive more businesses towards taking this step. As digitalisation has become more prominent and accessible, we’ve seen more online marketplaces enable businesses to set up shop online and extend to new markets.

In a post-pandemic world, the way many people work has shifted to a more hybrid style, leading to SMBs being able to create more global workforces. A Mastercard study for 2023 found that around 50% of SMEs were conducting more business internationally than in 2021. Though the survey did not clarify if this was selling/buying more internationally, it did also note that 61% of SMEs were sourcing more suppliers internationally than they were 12 months ago.

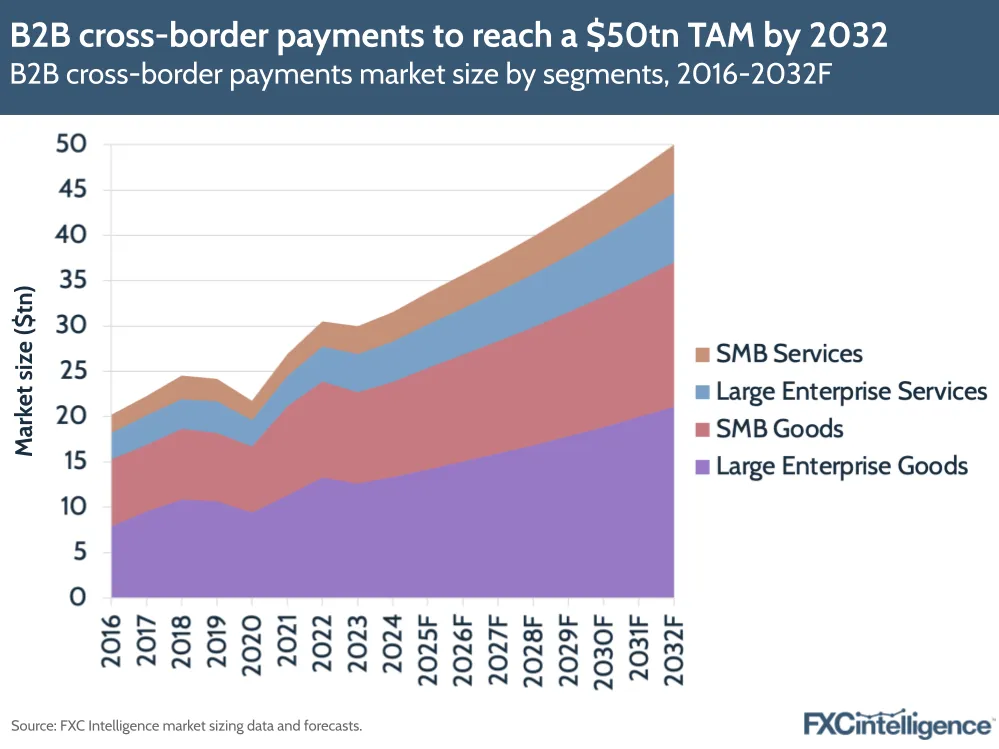

Our own market analysis found that SMBs overall had a TAM of $13.8tn in 2024, with $10.5tn of this being SMBs selling goods while $3.3tn of this was SMBs selling services. In total, we forecast the SMB market to rise by 54% to $21.2tn by 2032.

A major change that has been seen in the wider B2B space has been a shift toward the provision of digital services. In our breakdown of the cross-border payments market, we found that B2B cross-border services accounted for a total addressable market of $7.8tn in 2024. Around 50% ($3.9tn) of this market was digitally delivered, a nine percent increase from 2016, and this share is expected to grow even further up to 2032.

Our analysis found that in the B2B space, the share of the market from digitally delivered services is growing, while services are set to grow at a faster rate than goods. This reflects that digital services are being increasingly adopted in the B2B space, something that will likely continue with the advent of technologies such as AI, which boost productivity and enable the development of new solutions.

This is significant, as though SMBs make up the majority of businesses, they generally export significantly less than larger companies. Taking the UK as an example, SMEs (which the UK government defines as businesses with under 250 employees) accounted for 99% of the companies in the country but just 30% of export volumes in 2023, according to the latest figures available.

Continued investment from SMBs in digital – as well as the growing share of B2B services providers – is removing a barrier to global expansion, as digital services can be provided across borders much more easily and for lower costs than goods. Our figures project that the goods side of SMB will continue to take the biggest share of the SMB cross-border payments market in the next few years, but services will grow faster – SMB goods will rise 51% to $15.9tn in 2032, while SMB services will rise 61% to $5.3tn.

What are the cross-border payments challenges faced by SMBs?

However, while the globalisation of SMBs continues, they also face challenges when it comes to global payments, which can add an additional cost and complexity layer to an already difficult cash flow problem.

According to findings from a 2023 Small Business Credit Survey published by a number of Federal Reserve banks, roughly 70% of small employer firms in the US had an outstanding debt in 2023. The addition of rising interest rates has also added additional pressure to SMBs, which often need to source outside funding to keep going.

Challenges with financing mean that SMBs are more likely to feel the hit from fees, delays and transparency issues in payments than larger enterprises, even if they are not sending as much money overseas. This can exacerbate the pressure that SMBS are already under to ensure they are able to fund business operations and, crucially, expand into new markets to drive further growth.

One particular segment that faces these challenges is small ecommerce businesses that are selling internationally; for these businesses frequent cross-border transactions can lead them to swiftly rack up higher fees, which can dampen the positive impact of expanding into overseas markets.

Ecommerce companies on the rise

The number of new ecommerce businesses has grown significantly in recent years, driven by the advent of the Covid-19 pandemic, which saw a surge of consumers shopping online. Taking the UK as an example, internet sales as a percentage of total retail sales rose from 19.2% in 2019 to hit a peak of 30.7% in 2021, and this figure was hovering at around 27% in 2024, according to the Office for National Statistics.

Reflecting this change, the number of new ecommerce companies on Companies House (Britain’s register of listed companies) has risen swiftly in the wake of the pandemic, rising 58% in 2023 to over 67,000, based on figures collected by chartered accountants Your Ecommerce Accountant. Many new providers selling their wares online may eventually wish to spread across providers, which provides the additional opportunity for payments providers specialising in global ecommerce.

Amidst an ongoing move to digital, the payments industry is helping facilitate the expansion of SMBs globally, with a variety of payments companies making it easier for SMBs to build and develop an online presence as well as accept payments from overseas. Ecommerce companies like Shopify, for example, allow almost anyone to set up their own online shop and process payments through its checkout system. Meanwhile, payment processors such as Square, Stripe, PayPal and Adyen are helping SMBs to accept payment globally.

Supporting SMBs in emerging markets

Increasing digitalisation has not just boosted overseas ecommerce in developed markets like the UK, but in developing countries as well. India is a good example of this, with the country’s government reporting that internet users rose at a CAGR of 14% to 954 million in the period from March 2014 to March 2024. The growing number of internet users is spurring online shopping, with investment advisor Wright suggesting that India’s ecommerce sector could be set to grow at a 19% CAGR from $116bn in 2023 to reach $400bn by 2030.

From a payments perspective, the growth of instant payments, QR codes and mobile payment apps in emerging markets has reflected ongoing digitalisation, but for companies trying to sell their wares to developed markets overseas, cross-border payments can still be delayed or subject to high fees as a result of a lack of payment rails in place. What’s more, these markets can often face high currency volatility – see Nigeria, which recorded a 40.9% loss against the dollar in 2024.

Several payments companies have begun serving this need to facilitate flows from developed markets into emerging ones, including Payoneer. The company helps small businesses to reach new markets through its multicurrency payment processing platform and saw particular success with SMBs in its Q3 2024 results (the most recently published earnings for the company), which accounted for 73% of total volumes for the business. The vast majority of Payoneer’s revenues comes from SMBs on marketplaces, particularly looking to emerging markets.

Paying remote workers globally

Another specific challenge case for SMBs is being able to pay not just suppliers operating abroad, but staff as well. The pandemic has precipitated a shift to hybrid working and digital nomads – defined as workers who no longer work in a conventional office but wherever they can get an internet connection, often in a different country to the company they work for.

Growth in the number of digital nomads has precipitated the need for more global payroll solutions that can enable SMBs to pay employees abroad securely and reliably, without FX fees adding additional costs.

It’s no surprise then that recent years have seen significant developments in businesses specifically serving global payroll needs, such as Deel and Papaya Global in the US. In addition to giving SMBs a platform to help them hire employees in other countries without having to set up entire legal entities, these companies enable businesses to quickly pay out salaries to their international employees through a single payments platform, instead of having to set up a different system of payment for each country.

While some global payroll companies, such as Rippling, have built their own in-house payment processing services, some of these companies have partnered with or acquired payments specialists in order to power their global payroll (such as Papaya Global, which bought remittances provider Azimo in 2022), reflecting this growing demand for solutions to paying workers in different countries.

Many of these companies have raised significant funding for their services, reflecting the growing demand for enabling payments to workers across borders.

Consumer-focused providers shift towards SMB payments

Elsewhere, traditional banks and payment providers have begun to serve the cross-border payments needs of the B2B space with more alacrity. These businesses present an opportunity not only in terms of scale versus serving consumers, but as they are able to increasingly expand and gravitate towards digital services, so the opportunity expands with them.

A number of cross-border payments providers have developed solutions that are having specific resonance with SMBs, including multicurrency accounts that allow SMBs to receive, store and pay out in multiple currencies; FX management services; virtual and prepaid business cards; and solutions for setting up online marketplaces.

A common trend has been companies starting out on the consumer side then shifting towards serving small businesses as a way to diversify into a new area before expanding the use case for their payments infrastructure.

Wise is a particular example of a company highlighting why a shift towards serving the SMB market can prove profitable. Initially serving consumer money transfers, the company has since launched its Wise Business solution, as well as several products targeting SMBs.

In its most recent trading update for calendar Q4 2024 (Q3 2025), Wise’s enterprise clients account for just 5% of its customers but 28% of its volumes and 22% of its revenue overall, showing that businesses are a significant contributor to its services – however, its average send per business customer is significantly lower than other players in the space that are focused more on big businesses, highlighting their historical SMB focus.

Wise has continued to launch new products focused on SMBs, but has signalled that it is looking to address a larger enterprise market through Wise Platform – its global payments infrastructure for banks and financial institutions. The company has also noted that it is working to raise transfer limits in some countries so that it can handle larger volume payments, signalling that it is increasingly shifting to the larger opportunity.

It’s a similar story for Revolut, which originally offered a prepaid debit card for travel payments when it first launched in July 2015. The company has since launched international bank accounts in Europe, as well as risk management and payment acceptance services. According to its latest results, the company was onboarding 20,000 SMEs each month by the end of 2023, however the company noted that its new business was “shifting towards larger and more complex businesses”.

OFX is another example of a company which started out handling consumer money transfers, but its strategy has since shifted towards B2B, not least through its recent acquisitions of Paytron and Firma. In our recent conversation with CEO Skander Malcolm, he discussed how the company was providing SMBs with workflow and spend management tools to access more transactions. In this way the company isn’t just handling the transfers for businesses, but extending its capability across multiple different pain points faced by SMBs to maximise its output from them.

Current and future SMB payments trends

While SMBs have historically been an underserved market in the payment space, recent product launches and partnerships reveal that both established players and newcomers in the space are increasingly stepping up to respond to SMBs’ payment challenges.

In particular, banks are increasingly joining the fray to launch solutions to simplify transactions for SMBs. In November, Santander – which already owns global-payments platform PagoNxt as well as SME-focused payments provider Ebury – announced it was launching a new global platform targeted specifically at SMEs, with a noted focus on helping these companies scale up in the process. One possible interpretation of this is that helping SMEs grow internationally becomes a flywheel for banks, as their growth internationally will lead to them eventually processing higher volumes.

Many of the developments here have been about making payments faster, with Adyen and Airwallex forming deals with other companies to power instant payouts worldwide. This reflects a move from payments infrastructure players in the space to integrate more with real-time payments networks, which have become a hot topic in B2B as they enable faster transactions and a higher level of transparency across the payments chain.

Going into the coming year, being able to simplify and speed up international transactions will prove important as various factors could contribute to a shifting landscape for SMBs. One of these is the potential for volatility, with the imposition of tariffs from or against the US having a possible impact on currency values, which could add additional pressures on SMBs in that country. Sourcing capital is harder during periods of economic uncertainty, which makes having cash flowing in from international sources reliably more important for growth.

On the other hand, the continued rise of technologies like generative AI is helping spur productivity for businesses, as well as the movement towards digitally delivered tools. The more demand there is to provide B2B services across borders, the more need there is for cross-border payments specialists to provide it.

While the SMB cross-border opportunity may not be as large in terms of total addressable market, the impact of removing global payment barriers to growth and the fact that banks and payment companies continue to target them make this segment of cross-border payments an exciting one to watch.