Stripe has reported its FY 2023 results for its EMEA and APAC-focused Stripe Payments International Holdings, including a significant increase in losses partly attributed to a one-off employee share payment. But what else has contributed?

As a company that has yet to IPO, payments processing giant Stripe does not release full accounts, making an accurate assessment of its ongoing performance challenging to assess. However, the closest it provides are accounts for Stripe Payments International Holdings, the Ireland-headquartered division that oversees the company’s European, Middle Eastern and Asia-Pacific operations.

Required to be published yearly under Irish law, these accounts provide a fairly in-depth look at the division’s performance and provide some implications for the business as a whole. While it is not clear exactly what revenue it contributes to the overall business, in 2022 – the most recent year numbers are available for overall company Stripe Inc – Stripe Payments International Holdings accounted for around 25% of the entire company’s employees.

However, while Stripe Payments International Holdings grew revenue in 2023, it also reported a very significant uptick in losses. Part of this was attributed to a one-off incremental share-based payment to existing and former employees, however this was by no means the only contributor to the company’s losses surge. Here, we dig into the details to unpack the various drivers of Stripe’s jump in its EMEA and APAC losses.

Stripe sees FY 2023 international revenue growth

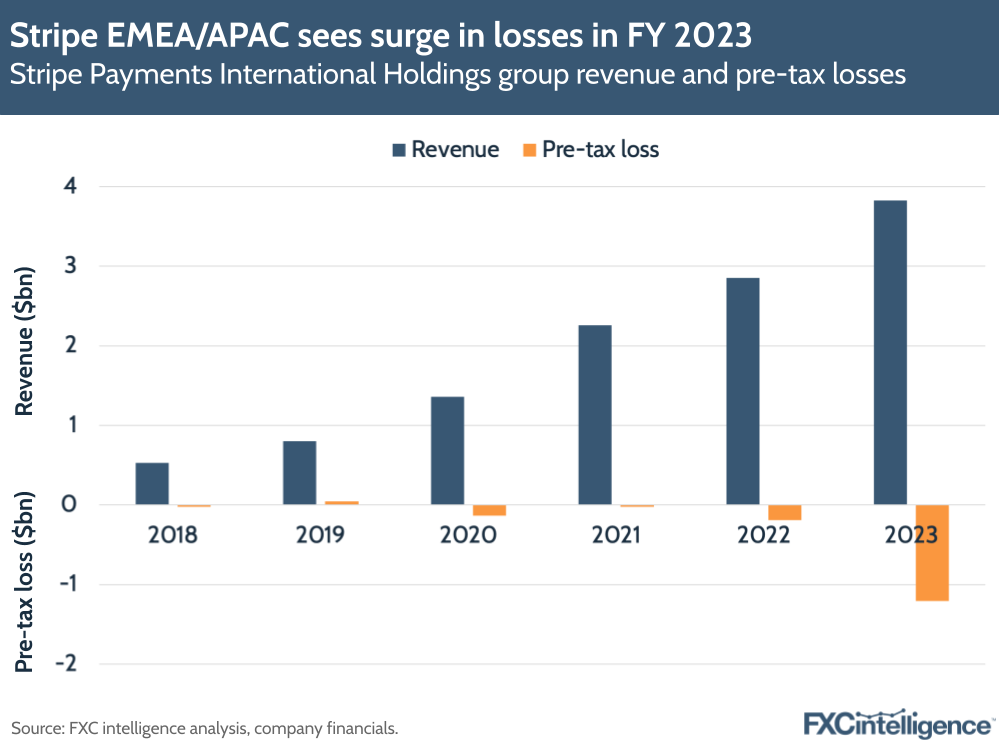

In full-year 2023, Stripe Payments International Holdings reported a 34% YoY increase in revenue to $3.8bn. This represents an almost $1bn increase on FY 2022’s $2.8bn, which itself was a 26% increase on FY 2021.

Stripe International also saw the combined net assets of the company and its subsidiaries, which are located across Europe, Asia-Pacific and the Middle East, increase by 50% YoY to $930m.

However, the company’s pre-tax losses also saw a very significant surge. Having already increased by 757% YoY in 2022 to -$190m, in 2023 they again climbed sharply by 537% to reach an all-time high of -$1.2bn.

This represents almost four times the combined losses of the five previous years combined, although Stripe has stressed that a significant part of the loss is a one-off cost.

Most of Stripe’s revenue is derived from user fees processed through the company’s network, part of which is fixed and part of which is variable depending on the volume processed. As a result, it directly correlates to the amount of volume Stripe processes each year. While Stripe Payments International Holdings does not publish volume, Stripe earlier this year reported that the entire company had seen its global volume reach $1tn in 2023. It also reported that Stripe Inc was cashflow positive, and expected to continue to be into 2024.

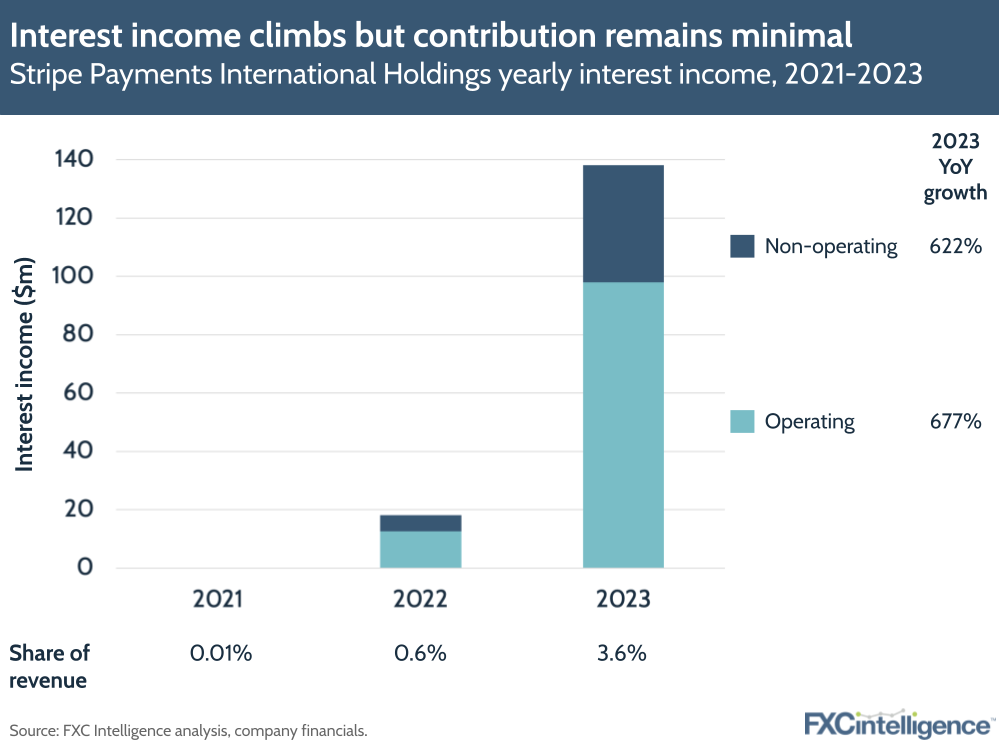

As with many players in the cross-border payments space, Stripe Payments International Holdings also saw a significant increase in the contribution of interest income to its revenue. While in 2021 the company saw interest income total $0.13m, in 2022 this had reached $18m and it had further grown to $138m in 2023. This means that it is now a small but growing revenue contributor, accounting for 3.6% of total revenue in 2023.

Much of this growth has been the result of operating interest income, which is interest income earned from activities related to Stripe’s core business operations. Of this, the majority was from bank interest income, which has likely been earned from customer reserves.

While the interest rate environment is changing, resulting in less interest income earned for a given amount, if Stripe’s reserve holdings continue to grow it is likely to see this become a regular contributor of revenue.

Share payments drive up Stripe staff costs

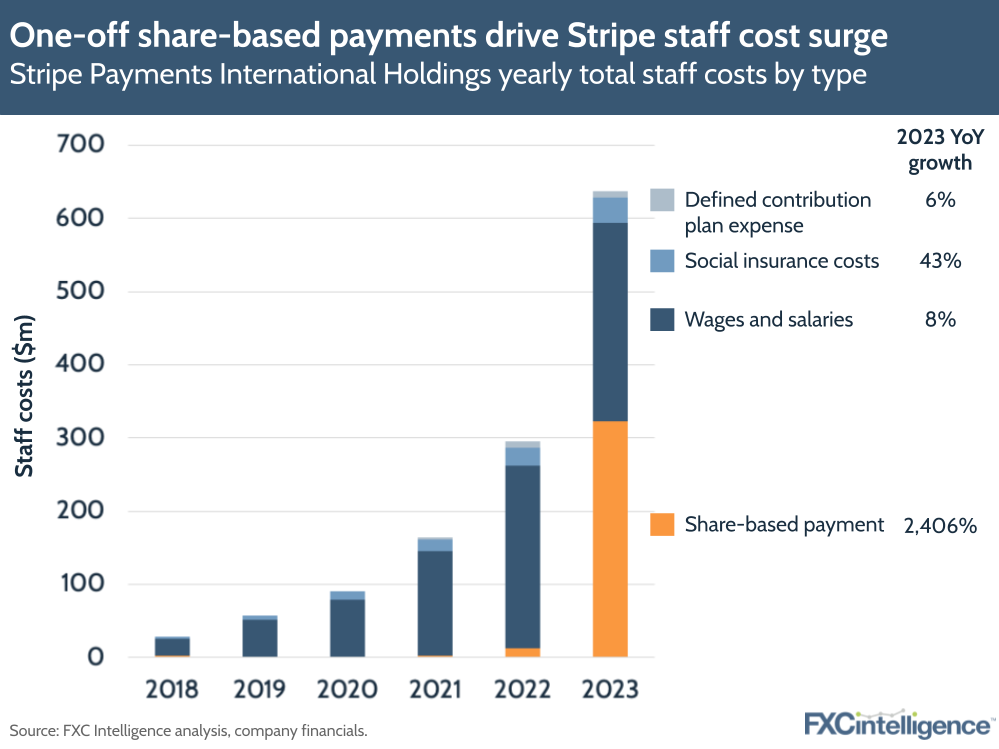

Share-based payments have been the headline driver of Stripe’s losses, and they have played a significant role. These are associated with a deal announced in February of this year, which saw Stripe raise $694m at a valuation of $65bn and in doing so enable current and former employees who held share options to cash out.

Globally, Stripe is reported to have enabled around $1bn of stock options to be vested under the deal, with those employed in Europe, the Middle East or Asia-Pacific seeing these costs recognised under Stripe Payments International Holdings’ 2023 results.

This was specifically recognised under share-based payments, a reporting line in the company’s staff costs, which in 2022 totalled around $13m. However, in 2023 this climbed 2,406% YoY to $323m, driving overall staff costs up by 116% to $637m.

By contrast, all other cost segments combined saw a YoY increase of only 11% to $314m, meaning these share-based payments accounted for almost half of Stripe International’s staff costs in 2023.

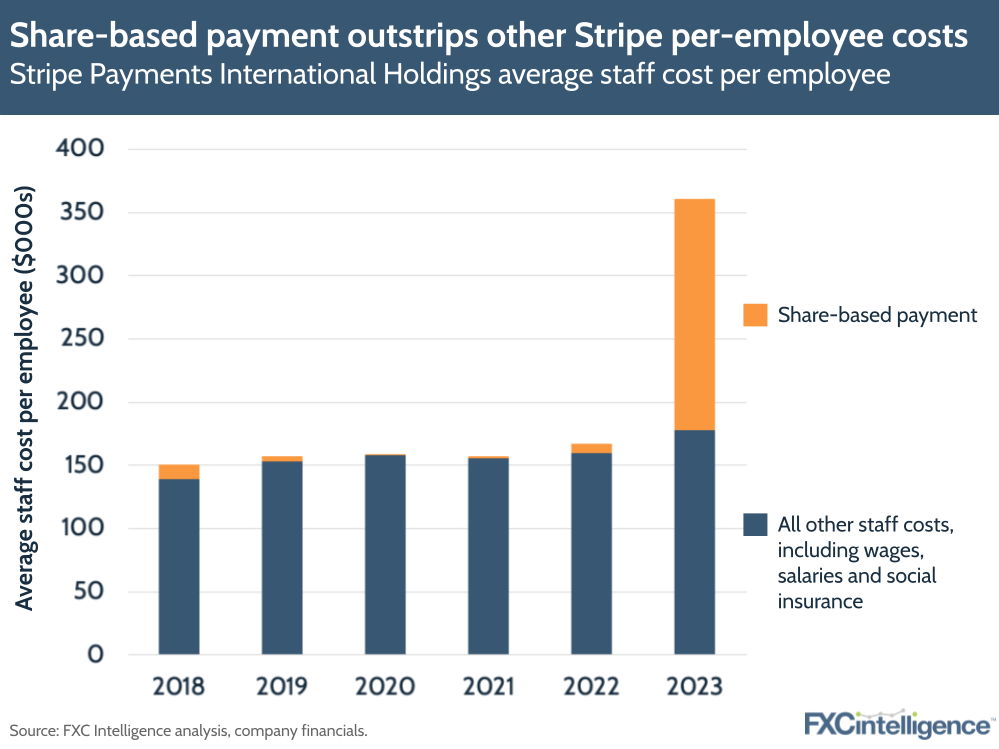

This is particularly clear when looking at average staff costs per employee for the company. In 2023, average total staff costs per employee were $360,980 – a 116% increase on 2022. However, without share-based payments they only saw an 11% increase to $177,708, $153,429 of which was wages and salaries.

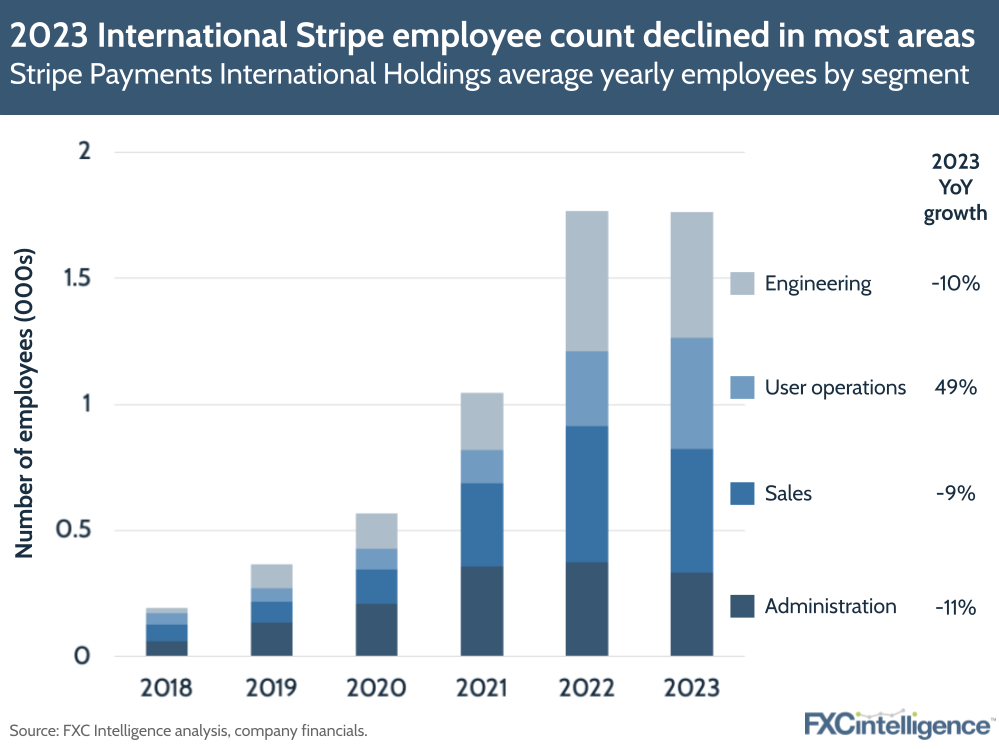

The year-on-year growth rates for staff costs and average staff costs per employee were almost identical in 2023 because the overall number of employees remained essentially flat between 2022 and 2023, with two fewer employees being added to the total number.

This saw an overall -0.1% reduction to 1,765 employees across Europe, the Middle East and Asia-Pacific. However, within this, almost all segments saw declines in employees.

Administration, which saw 4% growth the previous year, dropped by -11%, while Engineering, which in 2022 had seen employee numbers grow by 144%, dropped by -10% in 2023. Meanwhile Sales, which had grown by 64% in 2022, reduced by -9%.

Only User Operations, which in 2022 had increased by 123%, grew in 2023, increasing by 49%. This segment now accounts for 25% of all employees, up from 17% in 2022.

Such reductions are likely the result of layoffs announced by Stripe CEO Patrick Collison, who in November 2022 told employees that Stripe Inc would be reducing its overall headcount by 15%.

Cost of sales was a key loss driver for Stripe in 2023

While the circa $320m in share-based payments were a contributor to Stripe’s mounting losses in 2023, they were by no means the only element at play, accounting for just 6% of the total costs the company reported in 2023.

Combined, these totalled $5.2bn, with administrative expenses, of which share-based payments was a part, accounting for 23%, while cost of sales accounted for 77%. A negligible amount was also accounted for by interest payable and similar expenses.

While the share-based payments helped drive administrative expenses up 63% YoY in 2023, they still saw an increase of around $118m excluding share-based payments and retained around the same share of total costs as they had done in 2022. Other factors that contributed to administrative costs included foreign exchange losses, depreciation, amortisation and fees for services provided by partners.

However, growth in total cost of sales was a bigger driver of overall costs, seeing a 71% YoY increase to $3.99bn – around $164m more than the company’s reported revenue.

Stripe did not go into extensive detail here, but did report that the increased cost of sales had been due to growth both in business from existing users as well as increased user adoption in the company’s existing markets. Both these factors were also attributed to the increase in revenue, however the company also pointed to an increase in research and development as a key driver of cost of sales.

Stripe sees climbing R&D costs

Stripe does not break out the detailed financials of its research and development costs, however they are likely to have been a key driver of Stripe Payments International Holdings’ jump in pre-tax losses in 2023.

Stripe Inc’s yearly business update, which it published in March, went into extensive detail on some of the overall company’s R&D efforts in 2023, with highlights including efforts to tackle cart abandonment and localisation improvements, as well as the near-doubling of the number of payment methods it supports globally, including Swish in Sweden.

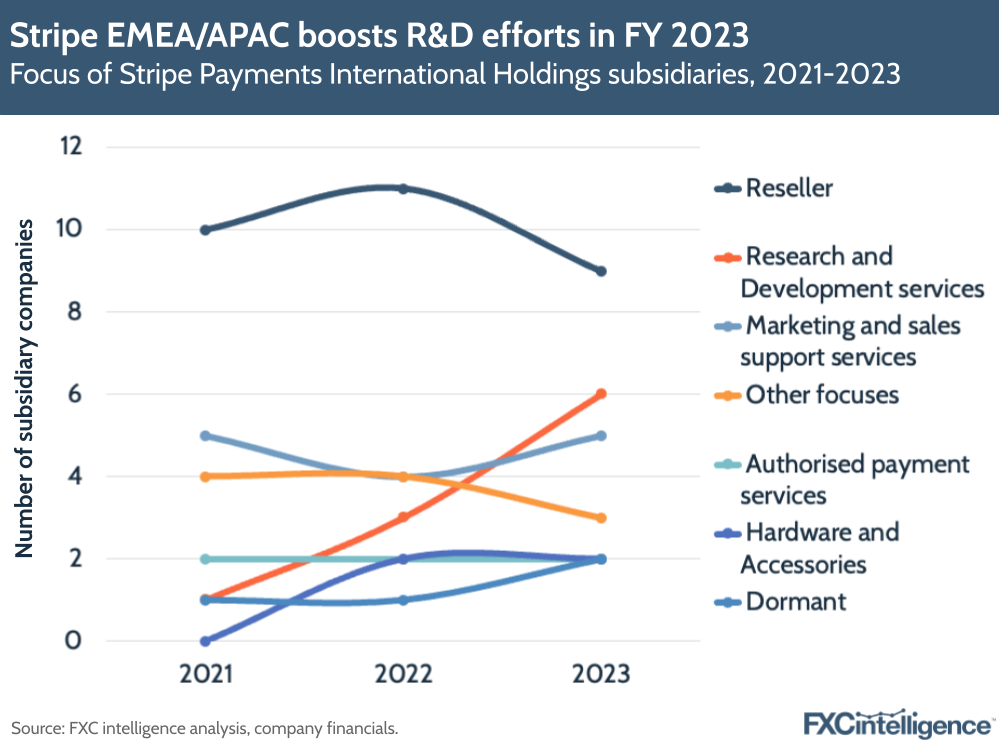

Analysis of the subsidiary companies reported under Stripe Payments International Holdings also shows an increase in those focused on R&D. While the total companies climbed from 22 in 2021 to 27 in 2023, the share conducting research and development as a primary activity grew more sharply. While in 2021 just one subsidiary (5%) focused on R&D, by 2023 six (22%) were focused on it across a broad range of geographies: China, Hong Kong, Switzerland, Romania, India and Taiwan.

Implications for the wider company and potential IPO

It is not clear how representative Stripe Payments International Holdings is of Stripe Inc overall, but there are some potential implications of these latest results for the wider company and in particular its IPO plans.

While Stripe International’s losses may well be lower in 2024 due to the lack of share-based payments, most of the increases in losses this year came from other factors, the majority of which are less likely to be one-off expenses.

The mounting costs, many of which appear to be associated with research and development, speak to a company that is not urgently shifting into pre-IPO mode – unlike a company such as Klarna – but which instead is making investments for long-term growth.

This aligns well with previous statements from the company, which frames itself as over time aiming “to increase the gross domestic product of the internet”. Earlier this year, Collison told the Financial Times that Stripe was “not in a rush” to IPO, and these financials reflect that.

However, Stripe Inc’s overall statement of reaching cashflow positive status in 2023 suggest that the international unit is taking a greater share of the financial burden and may be behind its parent on this metric.

The performance of 2024 will ultimately provide a significant insight into how quickly Stripe is developing, but as of now a 2025 IPO may be optimistic.