US President Donald Trump’s trade tariffs have introduced new charges for goods imported by the US from almost every country in the world. But how is the cross-border payments industry likely to be affected?

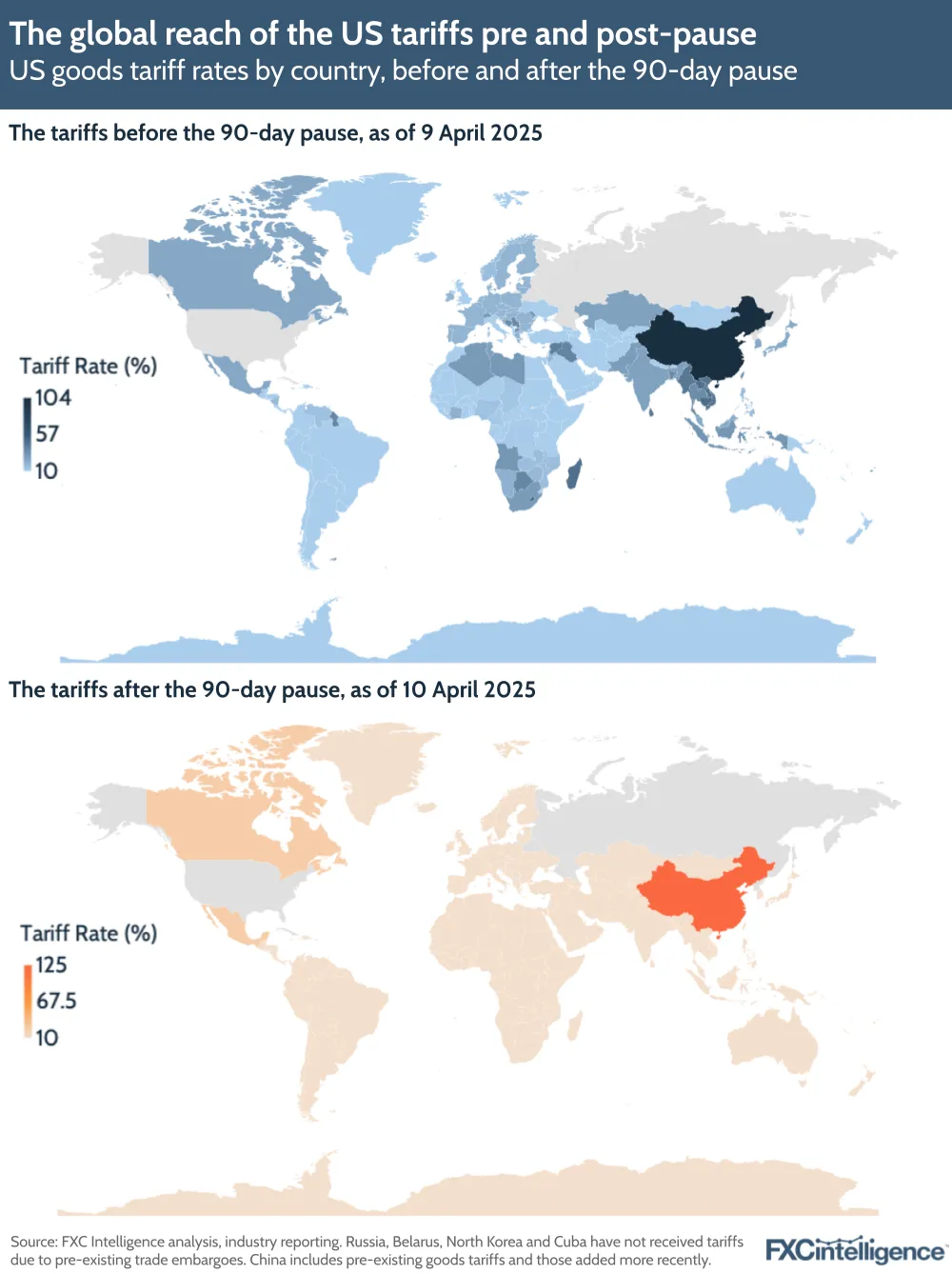

Last week’s so-called “Liberation Day” saw US President Donald Trump announce unprecedented, sweeping tariffs that could impact imports from almost every country on earth. From 5 April, all nations faced a 10% tariff, while from 9 April several dozen countries saw theirs rise further, with some passing 50%, before Trump announced a 90-day pause during which most countries will face a 10% tariff.

Targeting goods, with services currently unaffected, the tariffs have sent shockwaves through global markets in the US and beyond, creating a great deal of uncertainty in the process. Some initially assumed the move was a short-term ploy as part of wider negotiations, and many countries are now moving to respond to the tariffs. However, while Trump has confirmed a three-month pause, other comments from the US President and others in the US government have led some to fear that the tariffs will be in place in some form for some time to come, with significant implications for the global economy.

If this is the case, there will inevitably be an impact on the cross-border payments market, but how severe could this impact be and how is it likely to be felt? We explore some of the possibilities in this report.

US goods imports impacted by the tariffs

The tariffs are the most sweeping of their kind implemented by the US since President Herbert Hoover signed into law the Smoot-Hawley Tariff Act in 1930, which prompted a global trade war widely considered to have played a key role in the Great Depression.

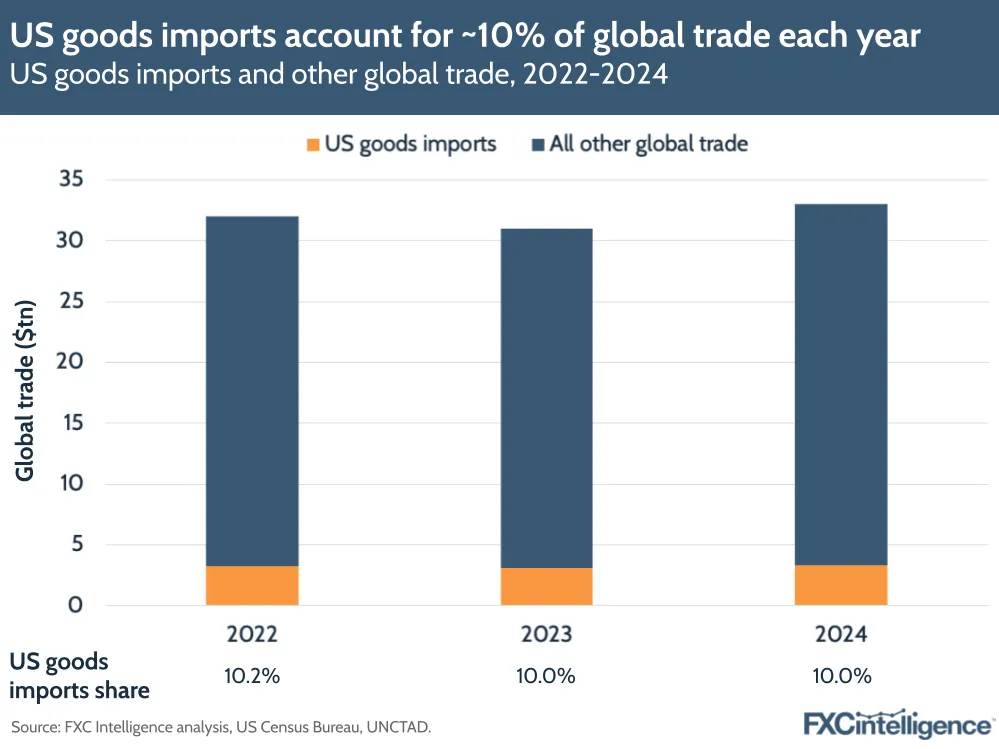

Although they only apply to goods, creating a disproportionate impact on some economies versus others, they effectively mean that 10% of the world’s trade is subject to at least a 10% charge.

While many countries are faced with just the baseline 10% tax on goods imported to the US, there are a wide range of exceptions, some of which remain in place despite the 90-day reprieve. For example, Canada and Mexico have not seen additional tariffs, but had already been subject to a 25% tariff on goods beyond the remit of the preexisting US-Mexico-Canada Agreement since February, which will remain in place despite the pause.

Meanwhile, China saw a 34% charge that is in addition to a previously imposed tariff of 20%, bringing its initial total to 54%. However, when it responded with retaliatory tariffs, the Trump administration added a further 50%, to reach 104%, and then added an additional 21% when the broader pause was announced, bringing its current total to 125%.

Other countries in Southeast Asia that had benefited from international manufacturing relocations in response to the previous hike on China have also seen very significant jumps, including Thailand (36%), Vietnam (46%) and Cambodia (49%), although during the 90-day pause will be subject to 10%.

Others have seen higher rates in response to their own pre-existing tariffs on imports from the US, including the EU (20%), India (27%) and Switzerland (31%). However, these will also see the 10% rate during the pause period.

In all cases, tariffs on cars, steel and aluminium, which had a separate tax of 25% applied in March regardless of the import country, remain unchanged.

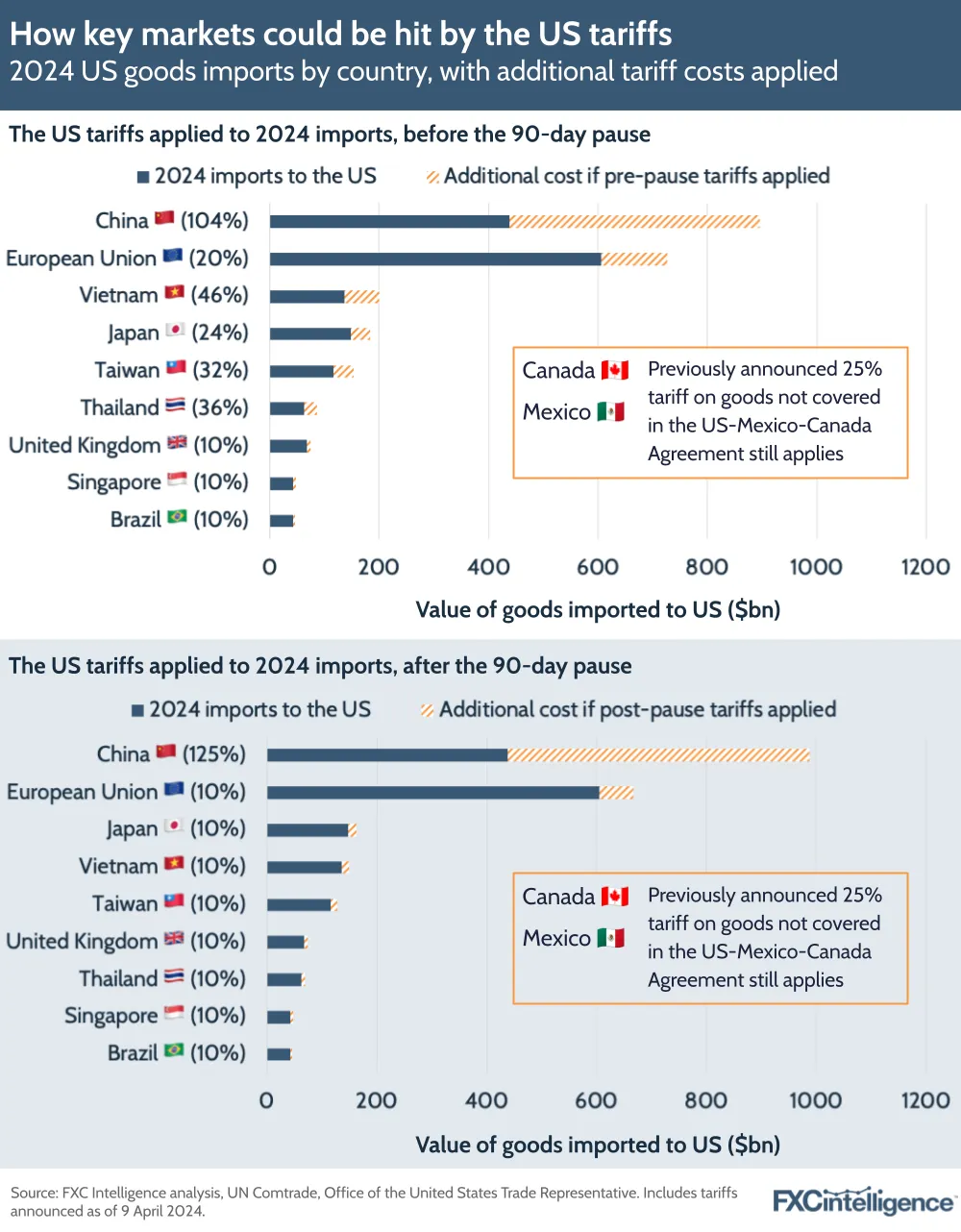

If the pre-pause tariffs were applied to all goods imported to the US in 2024, they would have seen $120bn in taxes paid on imports from the European Union and $457bn paid on imports from China. Worldwide, this would have totalled more than $1.2tn for all goods imported to the US in 2024.

Following the pause, this would be equivalent to $60bn in taxes on the US’ 2024 imports from the EU and $549bn from China, with the worldwide import taxes to the US reaching over $0.9tn.

Market reaction from the cross-border payments industry

Around the world, stock markets have seen sharp declines in response to the tariffs, with growing fears of a recession in several markets. In the UK, the FTSE 100 saw its steepest fall in five years on the Friday following the announcement, before opening more than -5% lower the following Monday. As markets closed on Wednesday, the FTSE 100 remained around 10% lower than prior to the announcements.

Asian stocks, meanwhile, have seen some of their worst falls in decades, with Japan’s Nikkei 225 closing down by -7.8% on Monday, while Hong Kong’s Hang Seng Index fell by over -13% on the same day, with the former continuing to slump through Wednesday, while the latter rallied slightly.

In the US meanwhile, the Dow Jones Industrial Average saw four-day losses pass 4,500 points on Tuesday, while the S&P 500 fell more than 12% over the four days to Tuesday, However, both began to rally on Wednesday, before rising sharply on news of the pause.

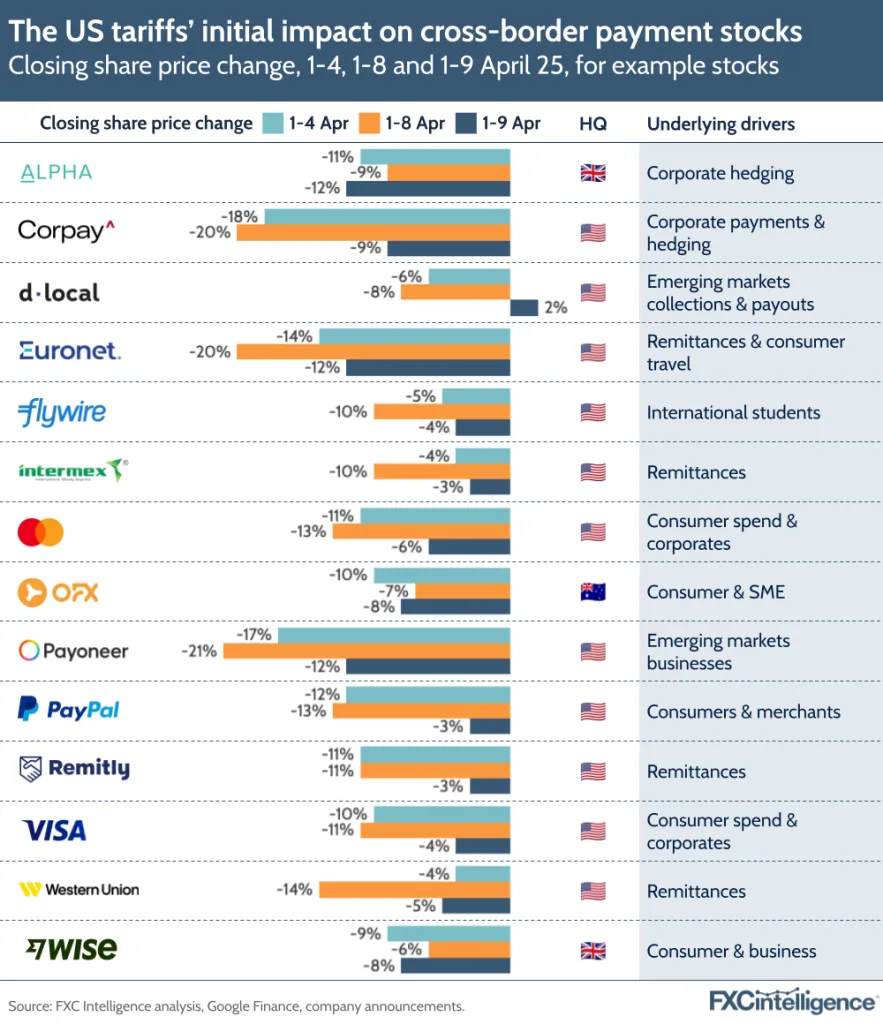

For publicly traded cross-border payments companies, there have been widespread share price declines, although there is some variation depending on the customer types and markets they focus on.

Traditional remittance-focused players Intermex and Western Union saw some of the slightest initial declines, with both dropping by -4% between 1 and 4 April – likely a reflection of the fact that neither they nor their customers are directly affected by the tariffs beyond the risk of general price rises and tougher economic conditions. However, both saw these falls widen as the following week began, with Intermex dropping -10% and Western Union -14% between 1 and 8 April. News of the pause did cause both to rally on 9 April, although they remained below their price at the start of the month.

Interestingly the same was not the case for digital-focused remittances player Remitly, which dropped -11% between both 1 – 4 and 1 – 8 April, although also rallied on the news of the pause. Meanwhile Wise, which focuses more on high-value consumer transfers, SME B2B payments and B2B2X through its Wise Platform offering, reduced by -9% between 1 – 4 but saw its reductions narrow to -6% between 1 – 8 April.

Corpay, which has a significant focus on the cross-border fleet industry and so is going to be more directly impacted by the tariffs, saw the sharpest initial drop among the players we reviewed, at -18% between 1 – 4 and -20% between 1 – 8. It also jumped on news of the 90-day pause but remains below its pre-tariff price.

Similarly, Payoneer, which has a strong focus on cross-border marketplace sellers, many of them in Asia, was close behind at -17% between 1 – 4 but saw its drop widen to -21% – likely in response to the additional Chinese tariffs. However, the additional Chinese tariffs added when Trump paused the majority of the others did not cause further damage, with the company rallying with the rest of its peers.

There have also been impacts for players poised to make their public market debut. Klarna and eToro are among those to officially halt plans for an IPO while the markets are still so uncertain, and Circle is rumoured to be considering the same.

The potential impact for global payments players

While cross-border payments is a service-based industry, and so will not have to deal with the tariffs directly, they will inevitably impact the flow of money globally and so have knock-on impacts for many providers in the space.

It is likely that cross-border payments made for goods moving from other countries to the US will initially reduce as many companies pause imports while the situation is unfolding. This is something we have already seen from organisations such as the UK’s Jaguar Land Rover, which has paused shipments to the US.

If the tariffs continue into the medium term, however, we are likely to see some form of reduction of flows to the US, as well as a reallocation of much of that volume to other corridors, as companies look for alternative markets for the products they are selling.

The tougher macroeconomic climate may also bring other financial challenges, with Fitch Ratings warning that the tariffs are likely to intensify corporate credit risk.

“The tariffs will cut revenue growth and profitability for most corporate sectors globally, limiting issuers’ ability to restore their leverage headroom and increasing pressure on ratings,” the ratings agency said in a report released on Tuesday.

The impact for B2B cross-border payments providers

Any reduction in flows to the US is likely to have a far greater impact on flows for large enterprises and corporates than for small and medium-sized enterprises (SMEs). As a result, companies whose primary cross-border payments offering is B2B payments for larger companies are likely to see greater exposure to the tariffs, particularly if the US is a major inbound market for them.

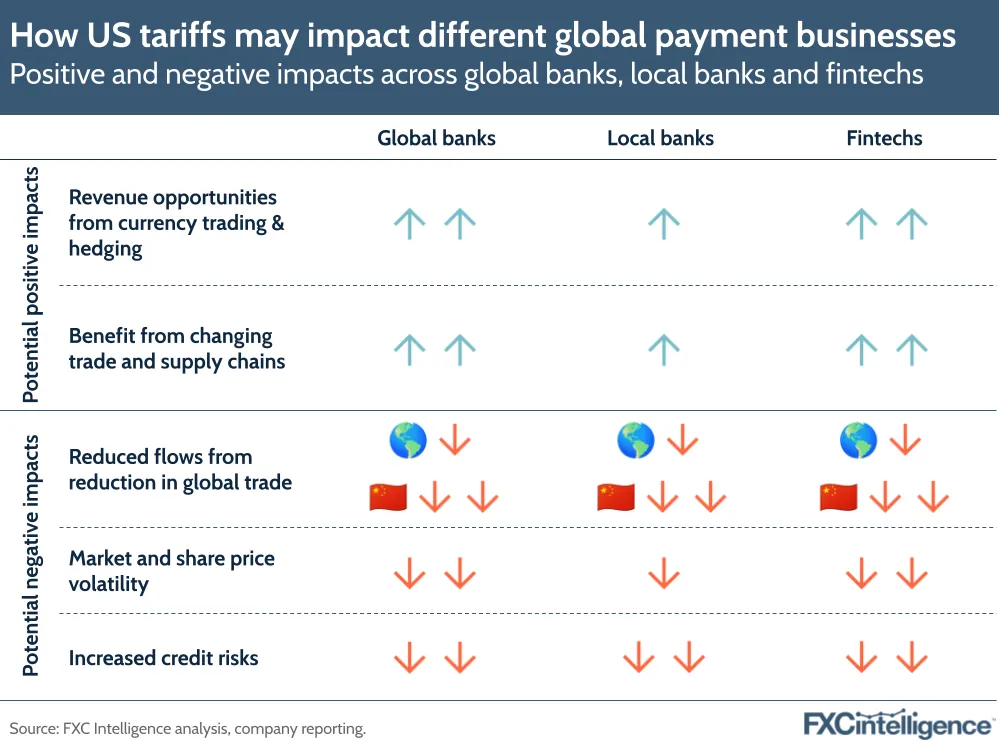

Given that banks still account for more than 90% of such flows, this will therefore create a greater risk for the bank side of the cross-border payments industry, although the small number of non-bank players catering to this space are also likely to see challenges.

However, the same clients’ needs also create additional revenue opportunities. Increased currency volatility will create increased demand for value-added services, in particular hedging solutions that can protect companies against further hits from sudden FX price changes.

Meanwhile, changing flows may see formerly exotic currency pairs becoming more commonplace, creating opportunities not only for providers to generate revenue to support this, but for B2B2X providers to help B2B payments providers broaden their market reach in response to changing client needs.

Challenges for ecommerce-focused players

For companies catering to the ecommerce market, meanwhile, there are also potential challenges. Many online marketplaces with strong cross-border purchases from US shoppers have sellers located in some of the hardest-hit markets, including several of those in Asia, and if the tariffs are maintained it is likely that US consumers will largely opt to purchase from domestic sellers instead.

This may impact some payment processors, payment services providers and merchant acquirers focused on this space, particularly those for whom cross-border payments are a particularly key source of revenue.

However, such sellers will ultimately look to cover lost revenue from other markets internationally, meaning that such ecommerce-related providers may ultimately see the source of their business move geographically rather than simply decline. In the case of payment service providers who offer additional localised services to sellers, there may also be revenue opportunities to support sellers entering markets they have previously not focused on.

Consumer money transfers: Mostly unaffected?

Consumer remittances and high-value money transfers are, for the most part, likely to see relatively minimal impact from the tariffs, given that the consumers themselves are not being taxed directly and that, as service providers, their businesses are also not being directly impacted. However, there may still be some impacts felt. The wider market uncertainty and potential harm to key economies may see consumers having less income to send abroad, resulting in lower flows.

On the remittance side, the pandemic showed us that this type of payment is highly resilient to shock, with many customers prioritising sending money home to friends and family over other expenditures. However, high-value payments, which are often to cover luxury expenses, may see some declines if the tariffs result in broader economic declines.

Increased credit risk may also create challenges around liquidity for settlements, although some companies may opt to shift network technologies to instant settlement solutions such as stablecoins to minimise this issue.

Currency volatility as an industry-wide challenge

Regardless of what part of the industry a company is in, however, the current currency volatility is a challenge that may evolve over time. At present, many players are reporting a significant upswing in trading activity in response to surges in the values of major currencies, although there is the risk of the situation changing as time goes on.

At present, the US dollar has weakened in response to the tariffs, however some have warned that if global trade reduces, this will impact the amount of the dollar in circulation and so cause it to rise against other major currencies.

In time, other markets may emerge as key players, having knock-on impacts on currency pairs beyond the dollar itself.

Who will benefit from this will ultimately depend on the headquarters of each company, and whether they are earning in the stronger or weaker currency. In 2022 when the global economic downturn hit, Payoneer, Remitly and Western Union were among those to see benefits from earning in weaker non-USD currencies but reporting revenues in USD. However, Euronet and PayPal both saw headwinds from the strength of the US dollar and wider FX volatility.

The currency volatility will also create challenges for those whose infrastructure does not support as rapid a response to pricing changes, as well as those with slower settlement times.

Ultimately, the precise impact of the tariffs is not yet clear, and how deeply it is felt is likely to depend on the length of time they are in place for. If they only prove to be short-term, this could be a minor headwind for a quarter or two, but if they persist for longer this could ultimately become a significant ongoing challenge for the industry, requiring innovative solutions and a global mindset.