Visa and Mastercard’s calendar Q3 2024 earnings, reported as Q4 2024 by Visa, have seen both companies continue growth. But how are their consumer and B2B2X cross-border businesses performing?

Cross-border payments is a critical part of the businesses of both Visa and Mastercard. In both players’ card offerings, fees earned on cross-border transactions represent a major contribution to both companies’ top-line revenue. Meanwhile, both organisations also have significant and growing B2B2X offerings, which provide further contributions by selling the use of both companies’ network capabilities to payment service providers and other organisations with significant cross-border needs.

Both organisations are also seeing the growth of their services across the world, with strong top-line results reported by both organisations for calendar Q3 2024, reported as Q4 2024 by Visa.

In this report, we dig into some of the recent numbers to see how both organisations are performing in terms of cross-border payments and beyond, and where they differ in their strategies and successes.

Visa and Mastercard calendar Q3 2024 top-line results

While both companies saw low double-digit growth in Q3 2024, there were some differences between the two companies’ performances in the most recent quarter.

Mastercard Q3 2024 earnings

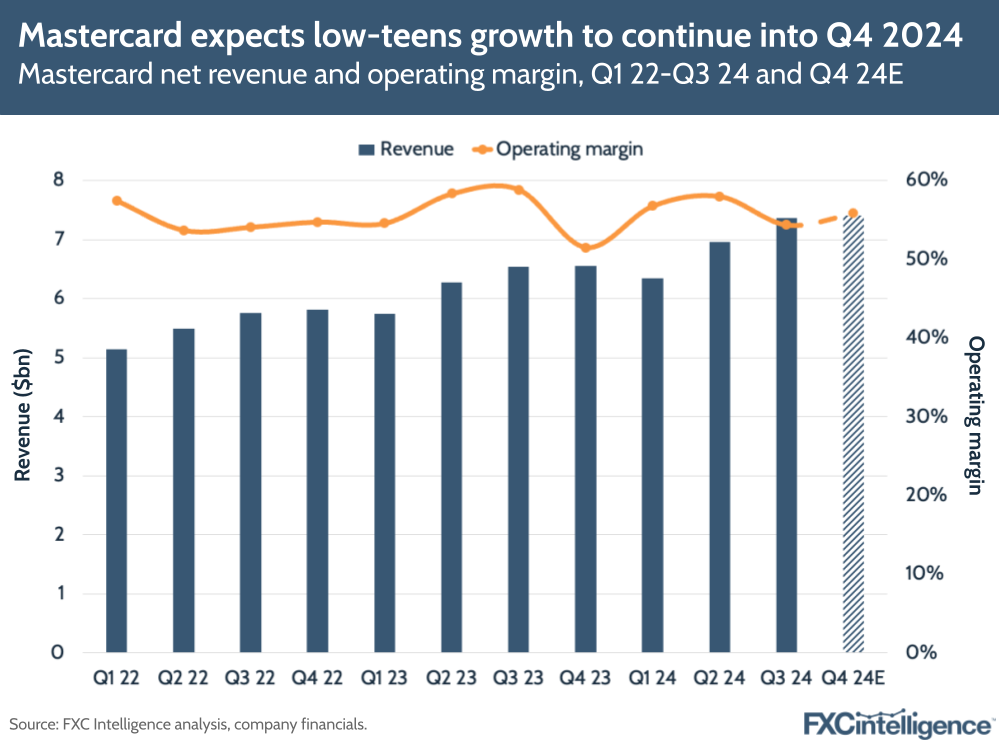

Mastercard reported 13% YoY growth in net revenue (14% on a currency neutral basis) to reach $7.4bn for the quarter, and is also projecting Q4 2024 net revenue growth in the “low teens”, which would translate to Q4 revenue of around $7.4bn-7.5bn.

This would see the company achieve full-year 2024 revenue of around $28bn – a 12% increase on the previous year.

However, Mastercard has seen a slightly more muted operating margin this quarter, as a result of increased operating expenses. The company saw expenses climb by 25% YoY to $3.4bn, the biggest increase it has seen since 2021, resulting in an operating margin of 54.3% – its second lowest in the last two years.

This has partly been attributed to general and administrative expenses, however more than half has been attributed to several short-term expenses, which the company declared as Special Items, without which expenses would have only increased 12% YoY.

One of these consists of one-off $190m costs associated with a company restructuring, which is ultimately designed to streamline the organisation. However, the company also reported around $400m in pre-tax charges for the nine months up to September 2024 associated with several litigation proceedings from merchants. These were largely merchants who opted out of a US class litigation over interchange fees that was settled earlier this year, although the company also reported costs associated with UK merchant settlements and a legal provision related to ATM surcharge complaints.

Mastercard expects some continued legal costs in Q4, although anticipated operating expenses to only see “low single-digit” growth, which is likely to result in a full-year operating margin of around 56% – roughly flat with 2023.

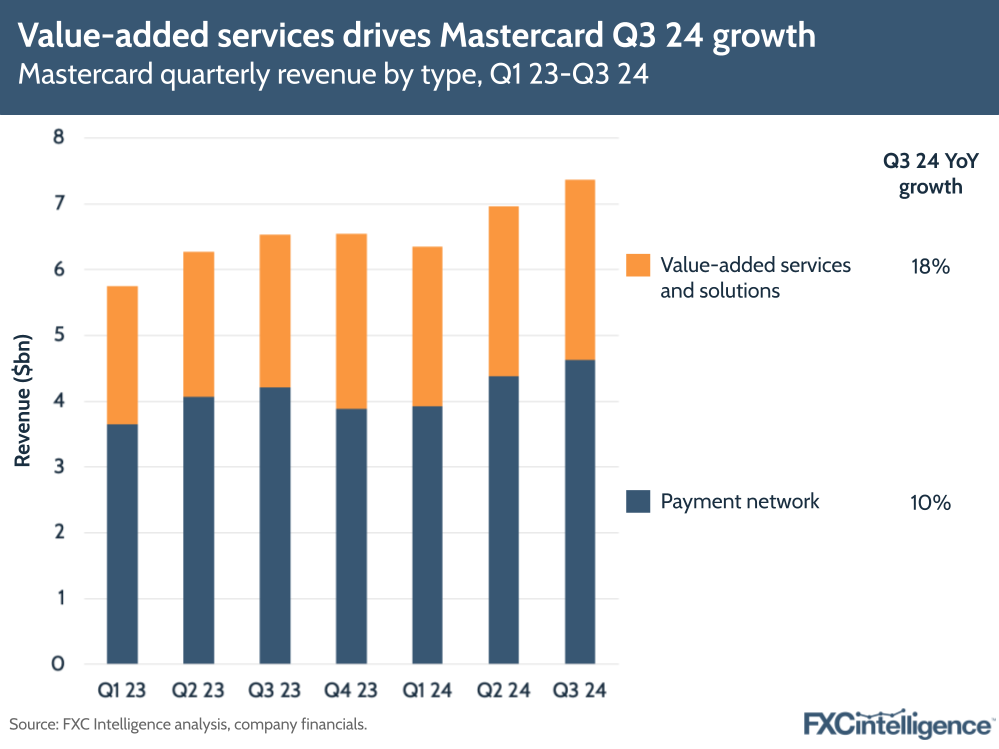

Mastercard cited a supportive macroeconomic environment and “healthy” consumer spending as key to its top-line performance in the quarter, which helped drive the company’s payments network revenue up by 10% YoY – 11% on a currency-neutral basis – to $4.6bn.

However, Mastercard’s biggest driver of top-line revenue in Q3 2024 was from its value-added services and solutions, which saw an 18% revenue increase – 19% on a currency-neutral basis – to $2.7bn. This was driven by demand for the company’s consulting and marketing services, as well as its fraud, security, identity and authentication solutions. Q3 2024 also saw Mastercard bolster its capabilities in this area, with the acquisition of global threat intelligence major Recorded Future for $2.65bn in September.

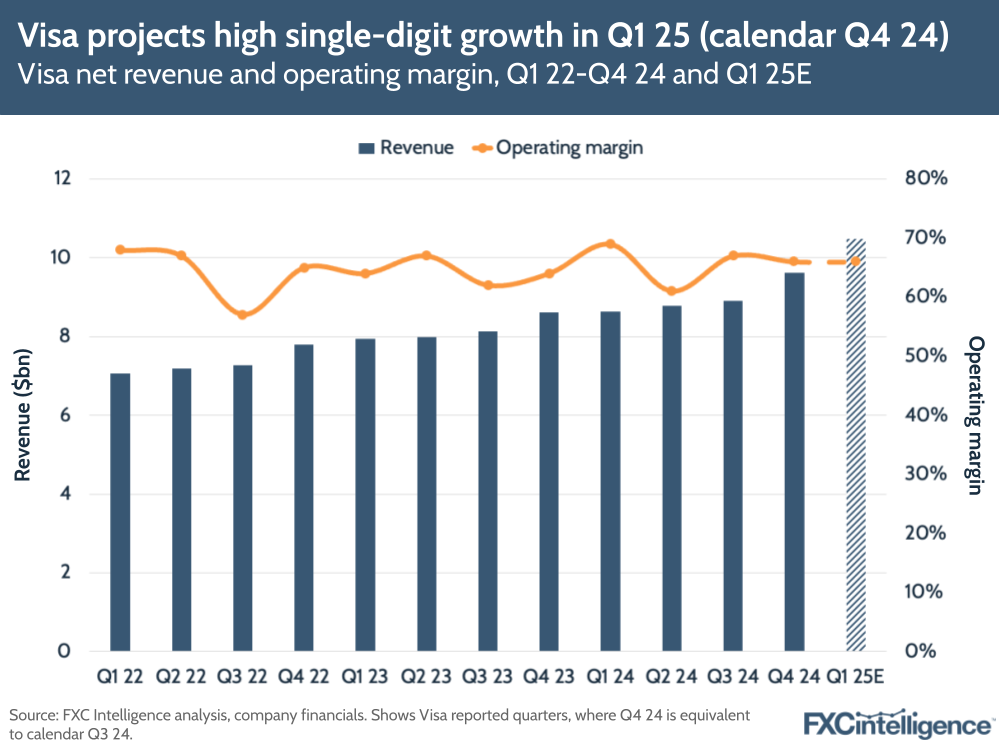

Visa Q4 2024 earnings

Meanwhile, Visa reported what CEO Ryan McInerney characterised as “very strong” results for its financial Q4 2024 (equivalent to calendar Q3 2024), with net revenue increasing 12% YoY for the quarter to reach $9.6bn. The company is also projecting “high single-digit” growth for Q1 2025, which is likely to translate into revenue of around $10.5bn for the quarter.

The company did see a slight increase in operating expenses, which grew by 7% YoY to produce an operating margin for Q4 2024 of 66%, driven by increases in expenses associated with marketing and personnel. This margin is set to continue in Q1 2025, driven by “high single-digit to low double-digit” growth in its operating margin for the quarter.

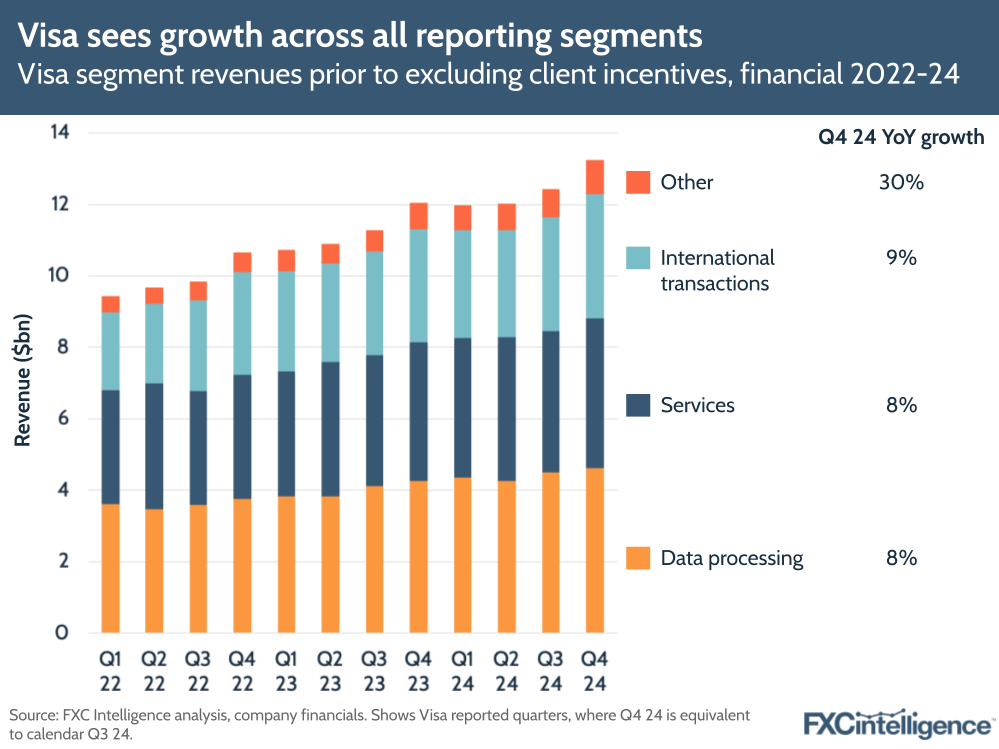

While overall revenue increased 12% in Q4 2024, Visa’s three largest segments saw slightly lower growth in terms of revenue. Data processing – the largest segment, which focuses on processing transaction data – grew 8% YoY to $4.6bn, while service revenues also grew 8% to $4.2bn. International transaction revenues, meanwhile, grew at 9% to $3.5bn.

In the case of both data processing and international transactions, this growth was lower than the equivalent volume or transaction metric, with the former being impacted by lower fees and penalties, while the latter was impacted by lapping increased currency volatility.

Services, meanwhile, saw stronger growth than its equivalent volume as a result of both mix and improved utilisation of card benefits.

However, the Other revenue segment saw the sharpest increase – of 30% to $0.97bn – largely as a result of revenue from Olympics-related marketing services, as well as Visa’s consulting offering.

To reach its net revenue value, Visa also reports deductions from client incentives against these revenue lines. This saw lower YoY growth of 5.5% to -$3.6bn, contributing to the improved overall revenue growth.

For its financial full-year 2024, Visa’s revenue increased by 10% YoY to $35.9bn, while its operating margin was 66%.

Looking to 2025, the company expects to see “high single-digit to low double-digit” growth for the year, driven by incentives, which would translate into revenue of around $39bn-40bn for the financial year. This would result in an operating margin of 64-67%.

McInerney also confirmed that the company will be holding an Investor Day in February 2025.

Trends in global credit and debit card use

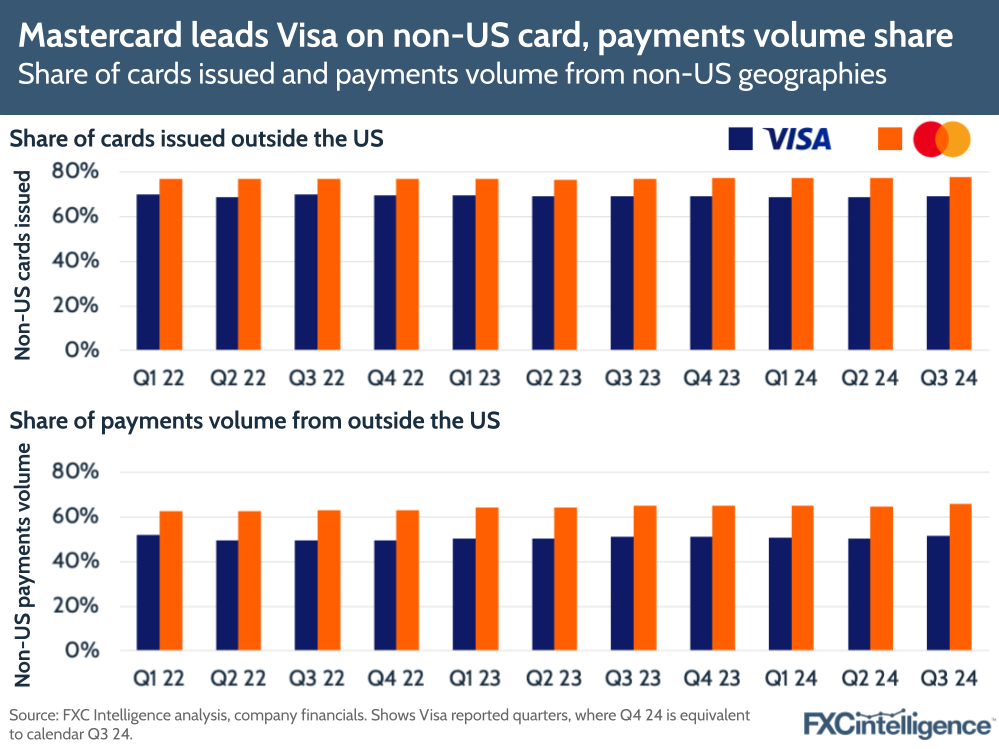

Both companies share extensive data around volume, transactions and cards issued, including breakdowns by regions, which provides a sense of the breadth of use beyond the US. This is significant for cross-border transactions, as these are more common in some parts of the world than others, particularly beyond the US.

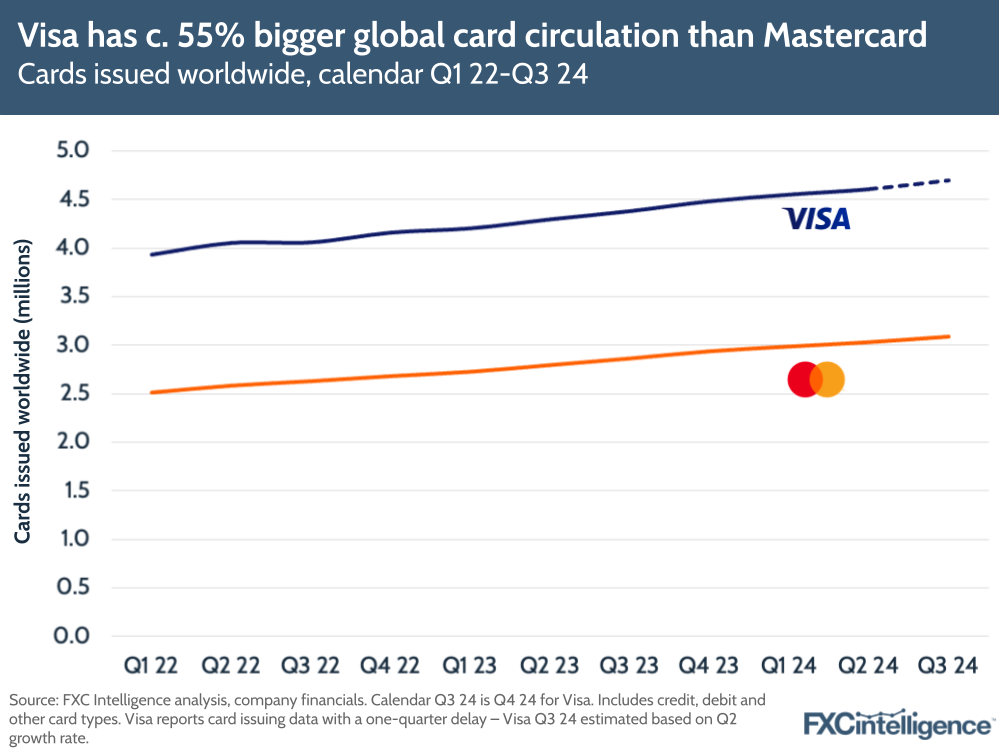

At the top level, however, Visa’s data on its credit, debit and other cards issued show it consistently has around 1.6 billion more issued globally than Mastercard. While Visa reports its card issued data on a one-quarter lag, its calendar Q2 2024 data puts this number at 4.6 billion, compared to Mastercard’s 3 billion, while in calendar Q3 2024 we project Visa will reach around 4.7 billion compared to Mastercard’s reported 3.1 billion.

Notably, Mastercard is seeing slightly higher growth in card issuance than its rival: at 9.5%, 8.4% and 7.9% in Q1, Q2 and Q3 2024 respectively. By contrast, Visa saw growth of 8.3% and 7.3% in calendar Q1 and Q2 2024 respectively.

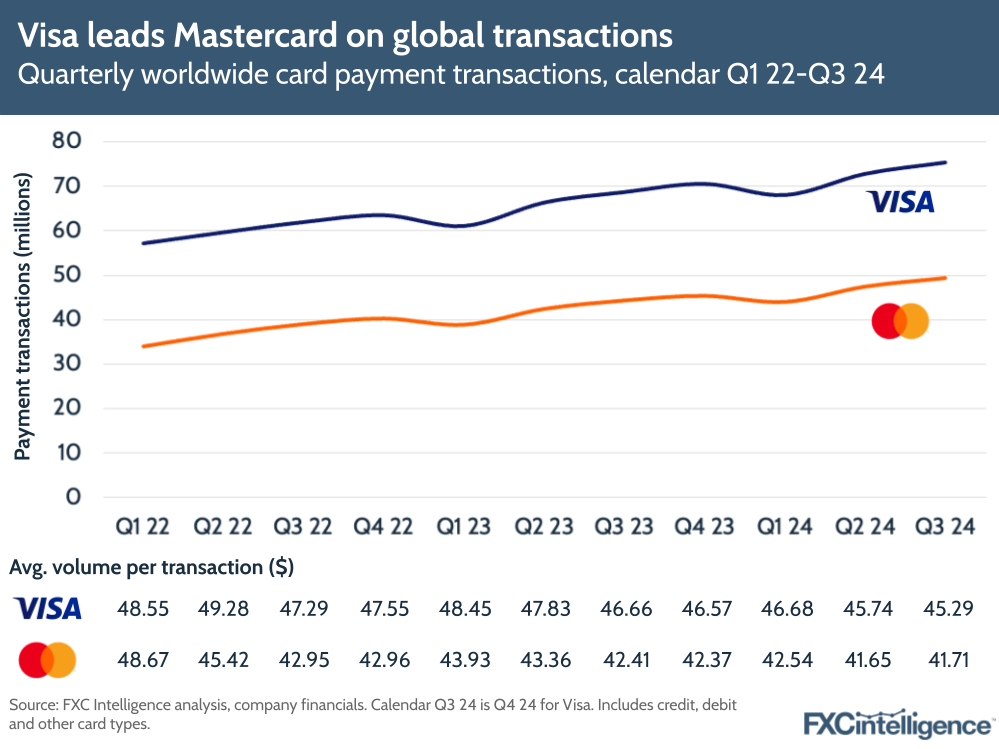

Mastercard also has lower payments transactions, which globally totalled 49.3 billion in Q3 2024, compared to Visa’s 75.3 billion. However, Mastercard has consistently seen slightly higher transaction growth rates than Visa, with 11% growth in Q3 2024 compared to Visa’s 10%.

Visa similarly reports higher overall payments volume than Mastercard, which translates into an average volume per transaction that is around $4 higher for Visa in most recent quarters.

However, Mastercard has a notably higher share of its usage outside the US. While in calendar Q3 2024 Visa saw 52% of its payments volume and 69% of its cards issued outside the US, Mastercard had 66% of its payments volume and 78% of its cards issued outside the country.

Within this, in Q3 2024 Asia Pacific, Middle East and Africa was Mastercard’s biggest reported regional segment in terms of cards issued (31%) and the third biggest segment in terms of volume (22%). Europe, meanwhile, is second on both volume (34%) and cards (28%), while the US comes in third on cards (22%) and first on volume (34%).

Meanwhile, for the most recently available quarters for Visa, the US had the biggest regional share in terms of cards issued (31%) and payments volume (48%). Asia Pacific came in second for cards (26%) and third for volume (15%), while Europe came in fourth for cards (15%) and second for volume (21%). Latin America and the Caribbean was the third largest region in terms of cards issued for Visa, at 18%, but accounted for just 7% of payments volume.

This difference in focus on non-US markets is also reflected in both company’s revenue reporting. In calendar Q2 2024, the most recent quarter this data is currently available for, Visa reported 41% of its revenue from the US, while 59% is from all other markets under International.

Mastercard, however, reports regional revenue in two segments: Americas – which includes the US, Canada and Latin America – and Asia Pacific, Europe, Middle East and Africa. In the most recent quarter, Mastercard reported 43% of its revenue from the Americas, while Asia Pacific, Europe, Middle East and Africa accounted for the remaining 57%.

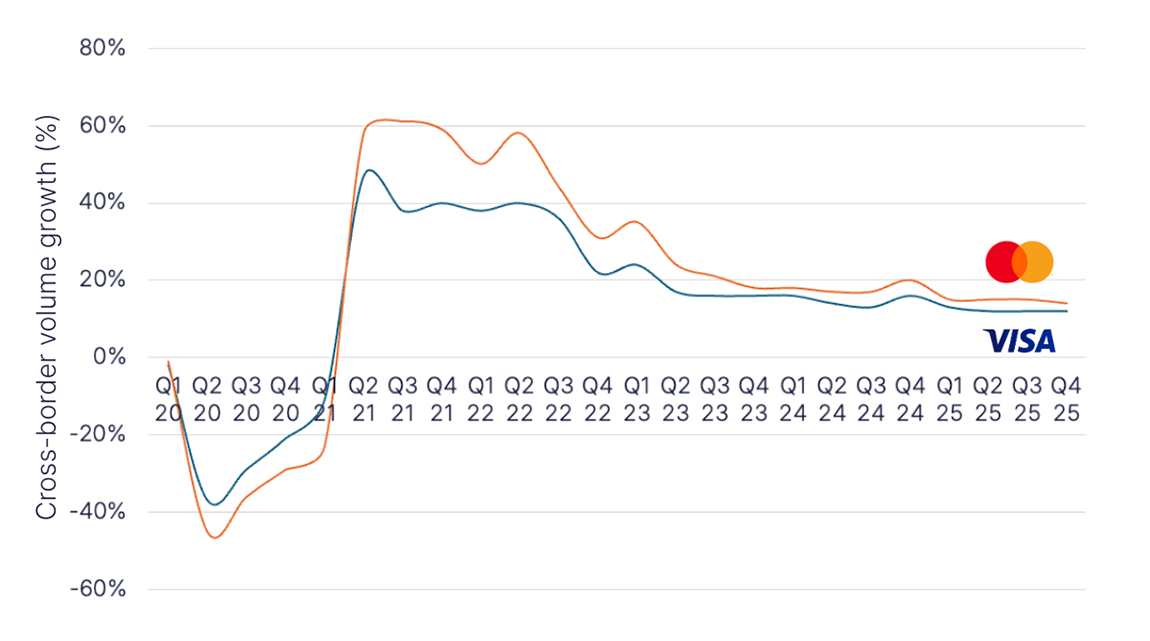

Visa and Mastercard’s cross-border card payments growth

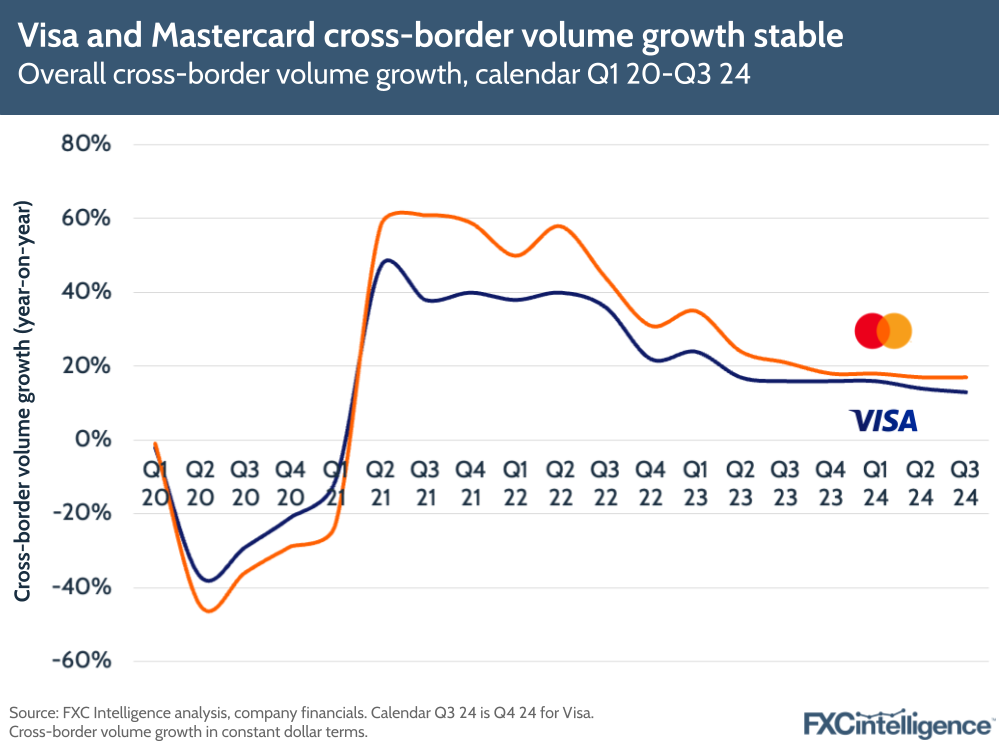

While neither company explicitly breaks out volume for cross-border payments, they both provide YoY growth rate metrics that provide key insights into how the segment is performing, and for both this quarter saw growth.

On overall cross-border volume, both companies reported fairly similar metrics, with Mastercard slightly ahead. Visa saw 13% YoY growth, having slowed from 14% in the previous quarter after a three-quarter run of 16%. Visa also saw cross-border volume growth for the 12 months ending 30 September reach 15% on a constant-currency basis.

Mastercard, meanwhile, reported 17% YoY growth in cross-border volume, the same as the previous quarter, which followed a two-quarter run of 18%.

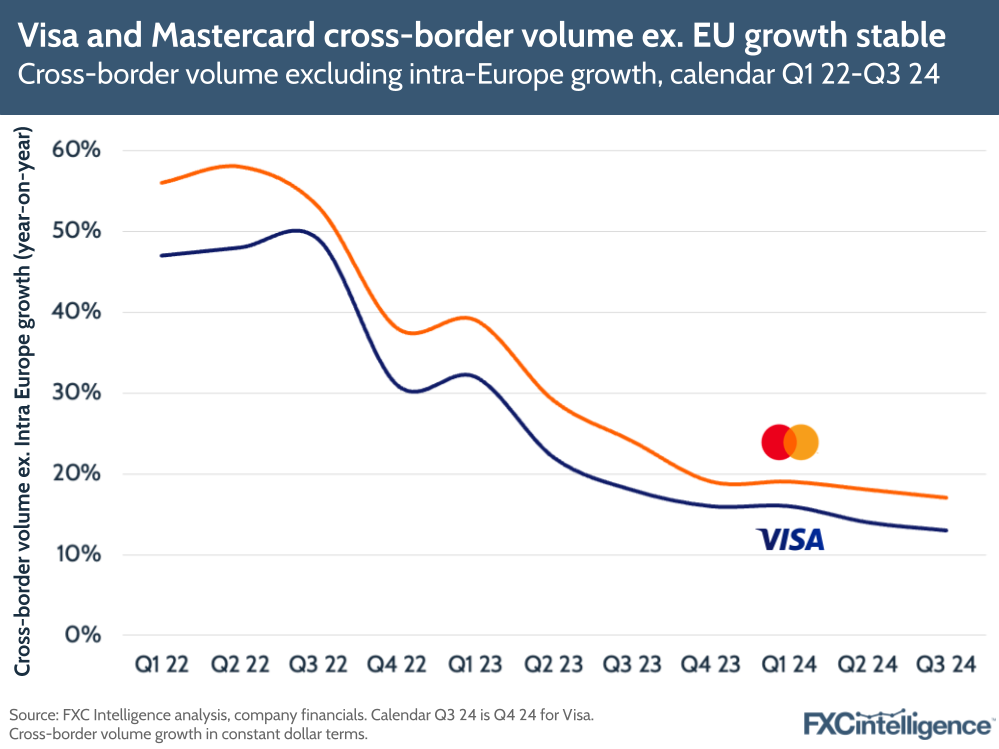

Both companies also track cross-border volume growth excluding Europe, which is key as this drives much of the cross-border revenue. While cross-border transactions in Europe typically use the euro, requiring no currency conversion, outside of Europe cross-border transactions provide greater opportunities for revenue generation.

While in past quarters there has been divergence between the excluding and including Europe metrics, in calendar Q3 2024 these were essentially the same in each company – Visa reported 13% growth across both metrics while Mastercard reported 17% for both.

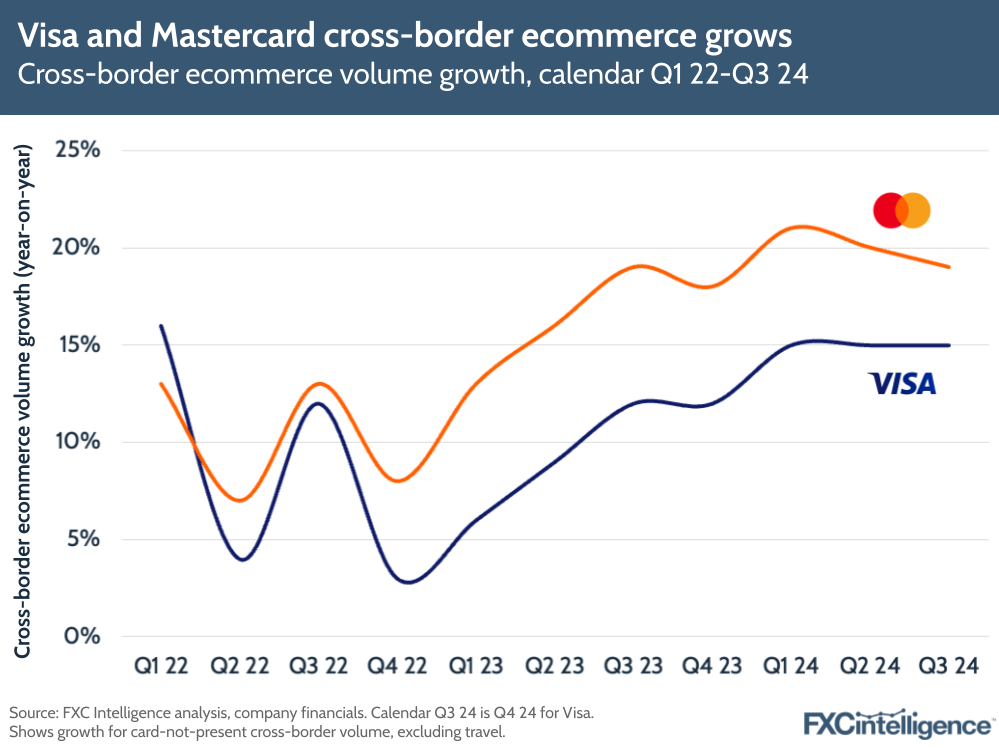

However, there was considerably more variation in cross-border volume for different purposes. Cross-border ecommerce, which is shown by card-not-present transactions, excluding those related to travel, saw a period of slowing growth following the pandemic but over the past year has seen growth rates rise again. This continued into the latest quarter, with Mastercard reporting cross-border ecommerce growth of 19%, while Visa reported 15% growth.

This represented faster growth than for payments volume overall, with Visa reporting an 8% rise for the quarter globally. This was slower in its core US market, where payments volume overall grew 5% YoY for Visa, while card-not-present volume increased 6%.

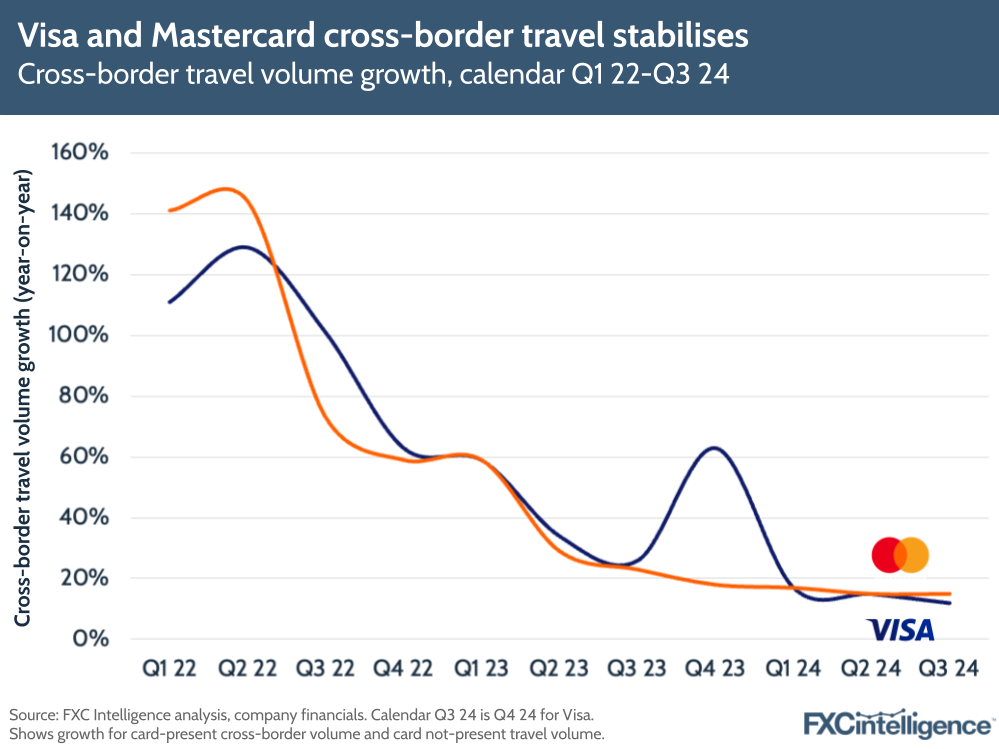

Meanwhile, cross-border travel volumes, defined as card-present cross-border volume and card-not-present travel cross-border volume, also performed well in the quarter. This was a metric that inevitably struggled during the pandemic, and then saw significant year-on-year growth in the quarters that followed. This period of surging growth is now over, with the travel sector now comfortably above pre-pandemic levels, however recent growth has been more modest but still positive.

Visa reported 12% growth for the quarter, which is now more than 150% up on calendar Q3 2019, but saw ongoing headwinds from Asia-Pacific inbound and outbound. In this region, flight bookings still remain below pre-pandemic levels, while macroeconomic conditions and currency weaknesses also remain a challenge. Central Europe, Middle East and Africa also saw a reduction on the previous year, although this was attributed to the timing of Ramadan, with the region seeing stable growth when this factor was normalised.

Mastercard, meanwhile, cited an increase in the penetration of contactless payments as a key contributor to its cross-border travel volume, which increased 15% YoY.

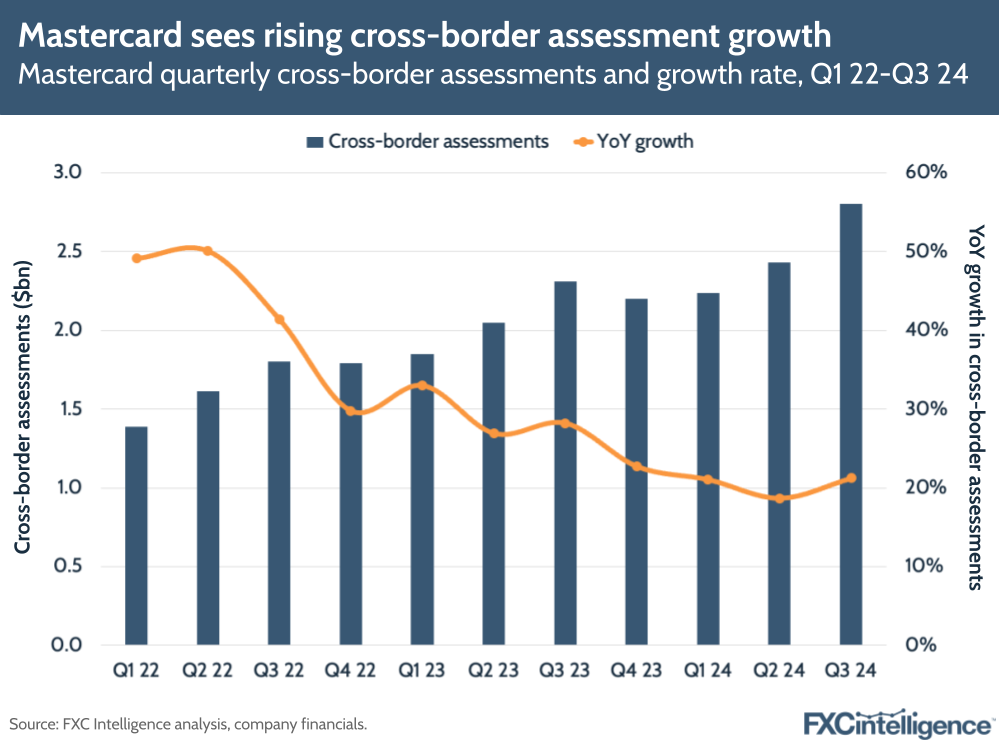

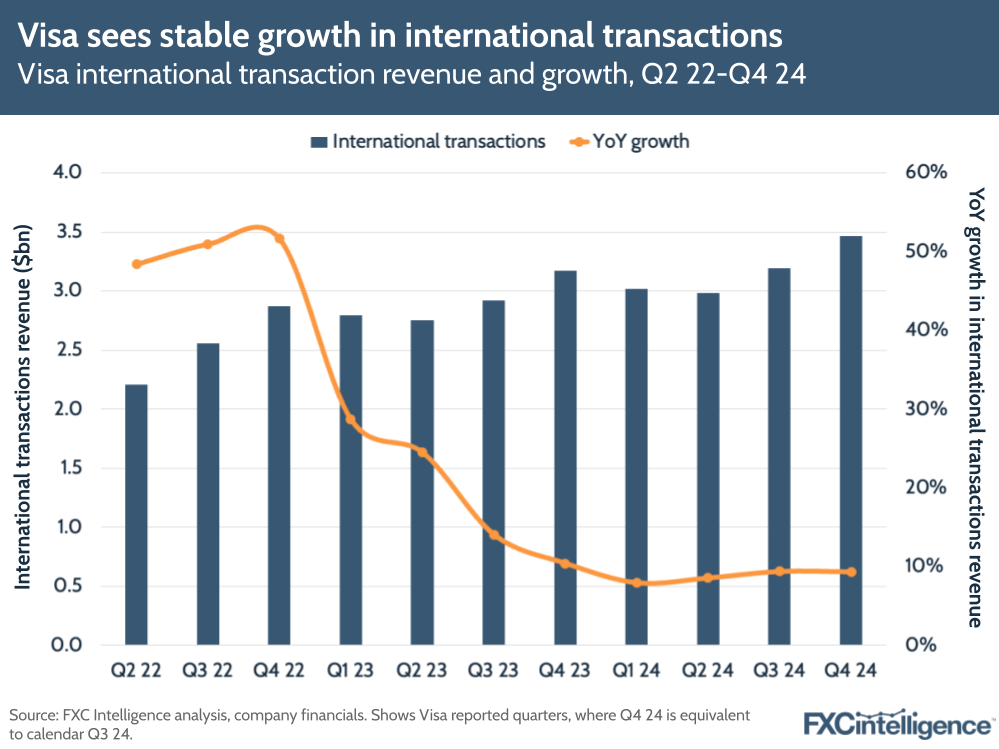

While neither company publishes direct numbers for cross-border volume, both do publish some figures related to revenue that give a sense of how cross-border transactions are contributing to their respective bottom lines. For Mastercard, this takes the form of its key metrics related to the payment network, an internal metric to monitor performance.

While the company stresses that these do not represent net revenue, they do include cross-border assessments, which cover cross-border charges from cards. These saw a 21% YoY increase in Q3 2024, significantly above domestic assessments’ 7% YoY increase and above the rate of growth for cross-border volumes. This difference was attributed to mix and pricing in international markets by Mastercard.

Visa, meanwhile, reports international transaction revenue, a metric largely driven by cross-border volume excluding Europe. This saw a 9% YoY increase, which the company noted was several percentage points below cross-border volume ex. Europe’s 13% growth. Visa attributed this to its lapping of higher currency volatility in calendar Q3 2023, despite the most recent quarter seeing increased currency volatility versus calendar Q2 2024.

B2B2X offerings: Visa Direct, Mastercard Move and beyond

While both Mastercard and Visa provide fairly significant information on growth and performance in their cross-border cards performance, there is significantly less information available about their respective B2B2X services, which include a significant amount of cross-border business.

These see both companies use their networks to underpin payment capabilities for other players across B2B, P2P and beyond. This is achieved through partnerships, with clients including banks, money services providers, other financial services providers and major organisations beyond financial services with a payments need.

Visa Direct’s 2024 growth

For Visa, this takes the form of Visa Direct, which in October rebranded to incorporate all of Visa’s B2B2X offerings for the first time, including Visa B2B Connect and Currencycloud. It typically reports Visa Direct as part of new flows, which also includes its B2B-focused commercial payment solutions.

While Visa does not break out precise revenue metrics for new flows, it did report revenue growth of 22% YoY for the most recent quarter. The company also reminded investors of a target set at its 2020 Investor Day, to be achieved by the end of financial year 2024, for new flows and value-added services (which includes issuing and acceptance solutions, risk and identity solutions and advisory services). Together, the company planned for these two segments to account for more than 30% of net revenue by the end of 2024, a target that McInerney says the company has now passed.

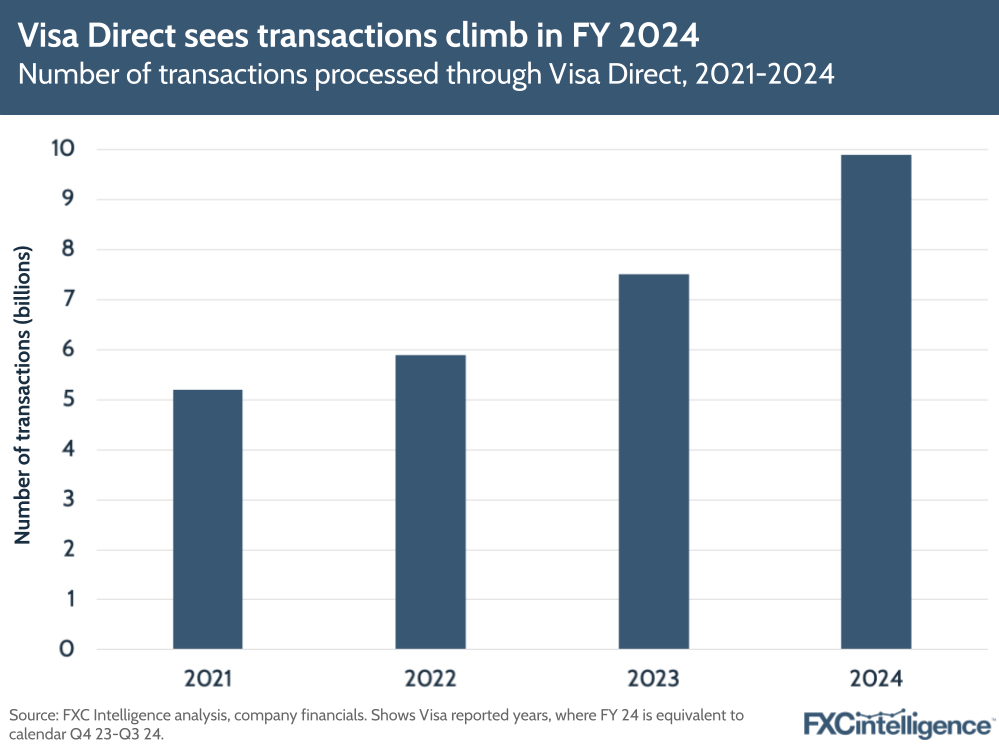

Visa does also break out some direct transaction metrics for Visa Direct, reporting that transactions grew 38% YoY for financial Q4 2024 to reach 2.8 billion in the quarter. For financial year 2024, meanwhile, transactions had climbed more than 30% to 9.9 billion.

This was aided by both new and expanded client relationships, with Visa citing several examples during the earnings call. This included an expansion of its partnership with Revolut that sees it support real-time card transfers for business customers in more than 78 countries and 50+ currencies, as well as an expansion of a partnership with US-based DailyPay to send earnings as international remittances. Visa also highlighted a new partnership with Brazil’s Travelex Banco de Cambio for both remittances and import and export payments.

Mastercard Move’s growth

Mastercard, meanwhile, provides B2B2X services to a variety of organisations through Mastercard Move, which also includes P2P-focused platform Mastercard Send alongside B2B-focused Mastercard Cross-Border Services. It also recently expanded Mastercard Move to increase its focus on the B2B side of the B2B2X space with the October launch of Mastercard Move Commercial Payments.

Mastercard does not break out any explicit metrics for Mastercard Move, although did highlight that its offering covers 95% of the world’s banked population across 180 countries and 150 currencies. CEO Michael Miebach also stated that Mastercard Move saw more than 40% transaction growth in the latest quarter.

However, CFO Sachin Mehra did highlight that cross-border volume within Mastercard Move flows on non-card rails, meaning that it is attributed to the company’s value-added services and solutions revenue.

The company also highlighted several partnerships with Mastercard Move, including the integration with Citi’s cross-border payments network that will see it enable near real-time cross-border payment transfers to Mastercard debit cards. Supported for Citi customers in 65 countries, this will initially serve 14 receiving markets, with more to be added in 2025.

Meanwhile, the company also highlighted several key regional partnerships announced in the recent quarter, which included partnerships with US processor Astra and Latin America’s Paysend, Leap Financial and Felix Pago.