In their latest earnings (calendar Q4 24), Visa and Mastercard continued to highlight cross-border volumes and ecommerce as major drivers to growth. We explore the highlights from their latest earnings calls and explore how the companies are expanding their B2B2X solutions worldwide.

Visa and Mastercard have both released their latest earnings results – Q4 2024 for Mastercard, and Q1 2025 for Visa, spanning October to December 2024 – with cross-border volume growth seeing an upward trend for both payments companies. As part of this, both parties noted continued growth for their B2B2X platform solutions – Visa Direct and Mastercard Move.

In one of the more significant announcements last week, Visa partnered with X, formerly known as Twitter, for its new X Money Account service, which is expected to enable a digital wallet and P2P payments service via the X platform. The new money movement feature – adding to X’s quest to become an ‘everything app’ – will be powered by Visa Direct, Visa’s real-time payments platform.

Meanwhile, Mastercard Move has seen continued transaction growth, with the company launching a new commercial payments feature early in Q4 that enables 24/7 real-time cross-border payments for banks.

Below, we’ve explored some of the key cross-border trends from Visa and Mastercard’s most recent results, as well as how the growth of these two platforms is continuing to make an impact on their earnings.

Visa and Mastercard calendar Q4 2024 top-line results

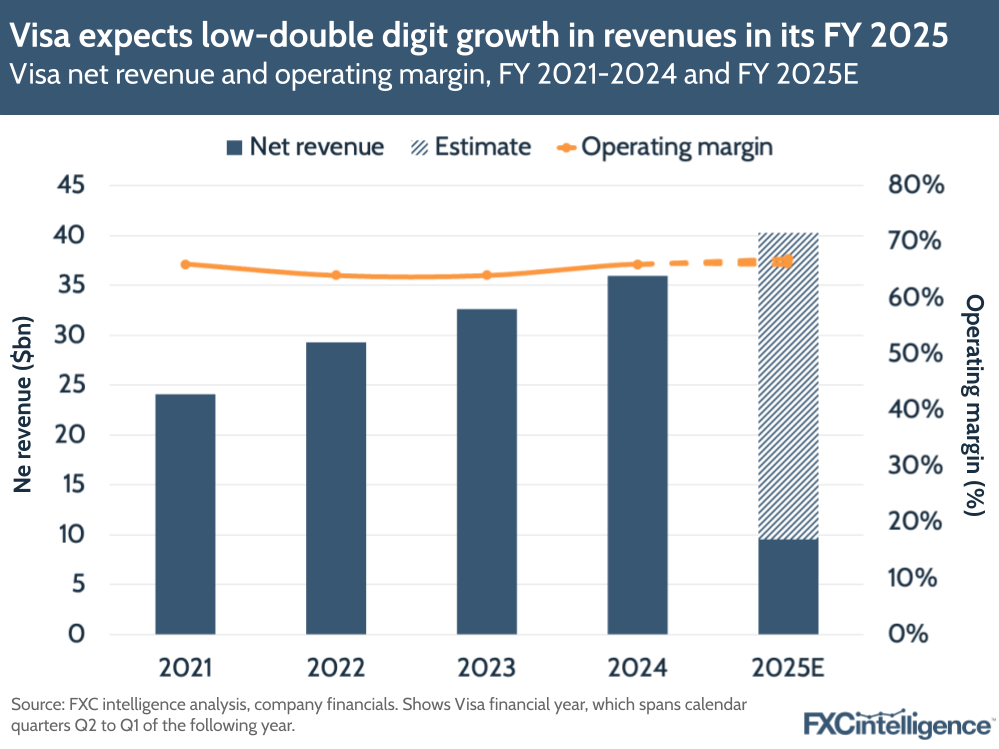

Visa Q4 2024 earnings

Visa’s net revenue rose 10% YoY to $9.5bn in Q1 2025, with the company citing cross-border volumes, strong holiday spending, improving trends in payment volumes and growth in processed transactions as key drivers.

Cross-border volumes grew by 16% both in total and excluding intra-Europe, while overall processed transactions grew 11% to reach 63.8 billion for the quarter. Visa will likely have more updates on its wider performance at its investor day, taking place on 20 February.

The company did see a notable rise in its operating expenses, which grew 22% to $3.3bn. This drove an operating margin of 66%, down three percentage points compared to the same period last year. The company attributed this to increases in personnel and general administrative expenses.

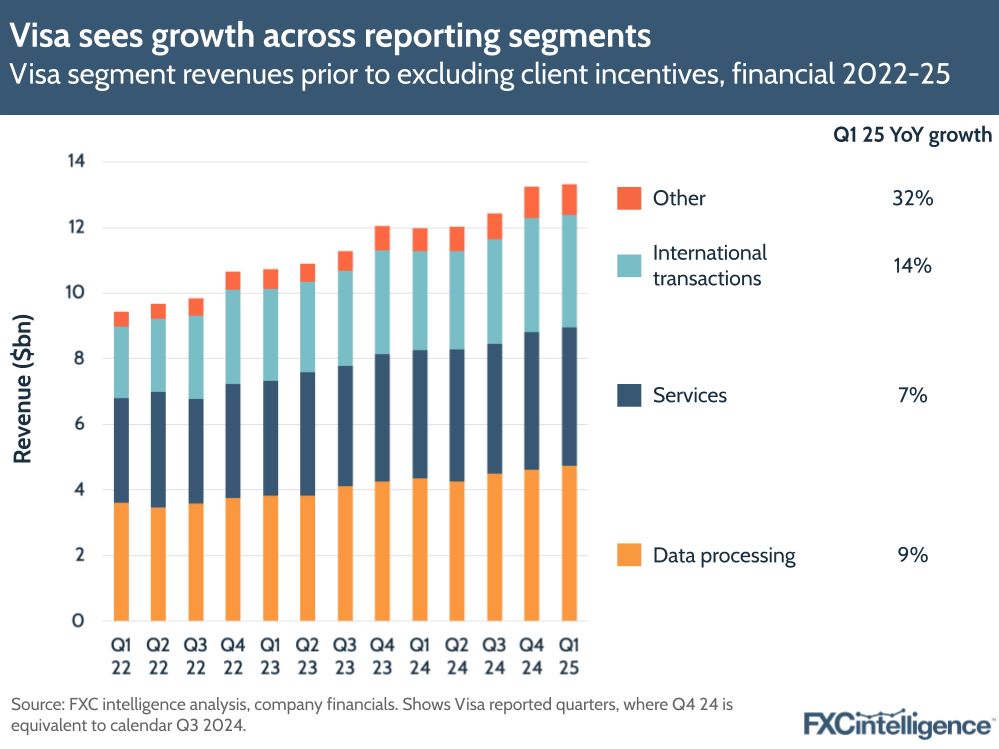

Breaking out Visa’s segments, the company’s international transactions revenue saw the second highest growth during the quarter, increasing 14% to $3.4bn. This represents 26% of the business’ revenues overall, excluding client incentives. Alongside the growth in volume, this was another demonstration that post-pandemic travel and global ecommerce continue to propel the company.

Having said this, Visa’s data processing and services revenues remain the biggest share of pre-client expense revenues, with 36% and 32% of share respectively. Data processing revenues – spanning authorisation, clearing, settlement and processing – grew 9%, while services revenues, which is driven by fees collected on payment volumes, increased by 8%. Meanwhile other revenue – which contains services such as consultancy services or licence fees – grew by 32% to $912m.

Mastercard Q4 2024 earnings

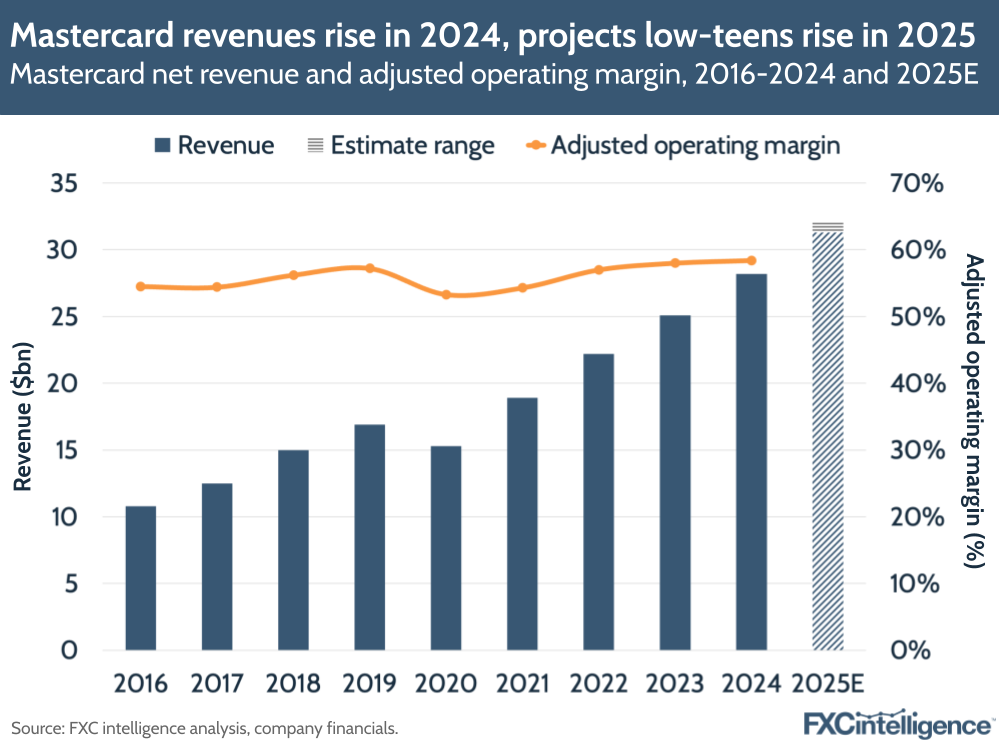

Mastercard’s net revenues rose 14% YoY (16% on a currency-neutral basis) to $7.5bn in Q4 2024, surpassing the company’s expectations. The company’s payment network net revenue rose 13% as part of this, with one of the biggest drivers being cross-border volume growth of 20% on a local currency basis. The company also saw gross dollar volume rise by 12% to $2.6tn.

Looking at profitability, the company’s operating margin in Q4 was 52.6% – higher than Q4 2023, but lower than previous quarters in the year, as the company continued to see higher-than-expected growth in operating expenses (up 12%).

Over the company’s full year, net revenues rose by 12% to $28.2bn, driven by its payment network as well as value-added services and solutions. Mastercard’s operating margin for the period was 55.3%, down from 55.8% the previous year as operating expenses rose 13% on the back of higher admin expenses, in addition to litigation costs. For the full year, cross-border volume grew 18%, while switched transactions and gross dollar volume both grew by 11%.

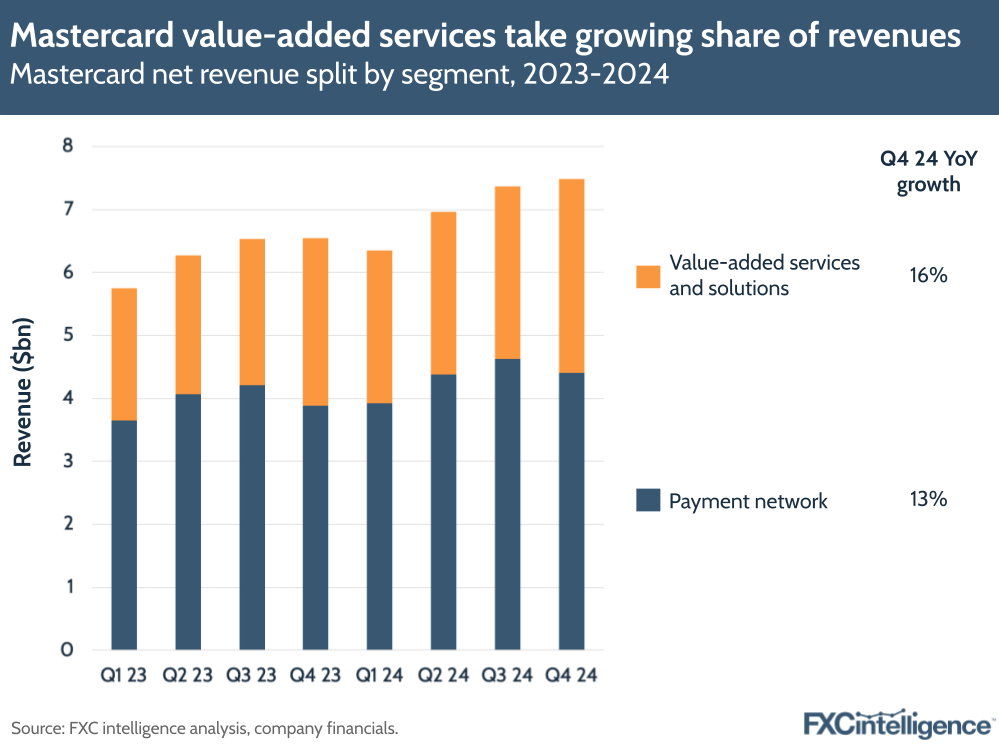

Notably, Mastercard’s revenue split continued its gradual shift to services, with value-added services continuing to grow faster than payment network revenue. The latter encompasses fees that Mastercard receives based on transactions, while value-added services includes additional services that Mastercard provides to financial institution clients and other businesses beyond transactions.

Mastercard’s payment network still accounts for the majority of Mastercard’s revenue, at around 61%, but value-added services has steadily grown its share, from 35% in 2022 to 38% in 2024. This segment saw 17% growth in 2024 – faster than the 10% growth for Mastercard’s payment network.

This year, Mastercard is expecting its net revenues to grow at the high end of low double digits to teens on an adjusted basis, excluding acquisitions, while also expecting operating expenses to grow by low double digits.

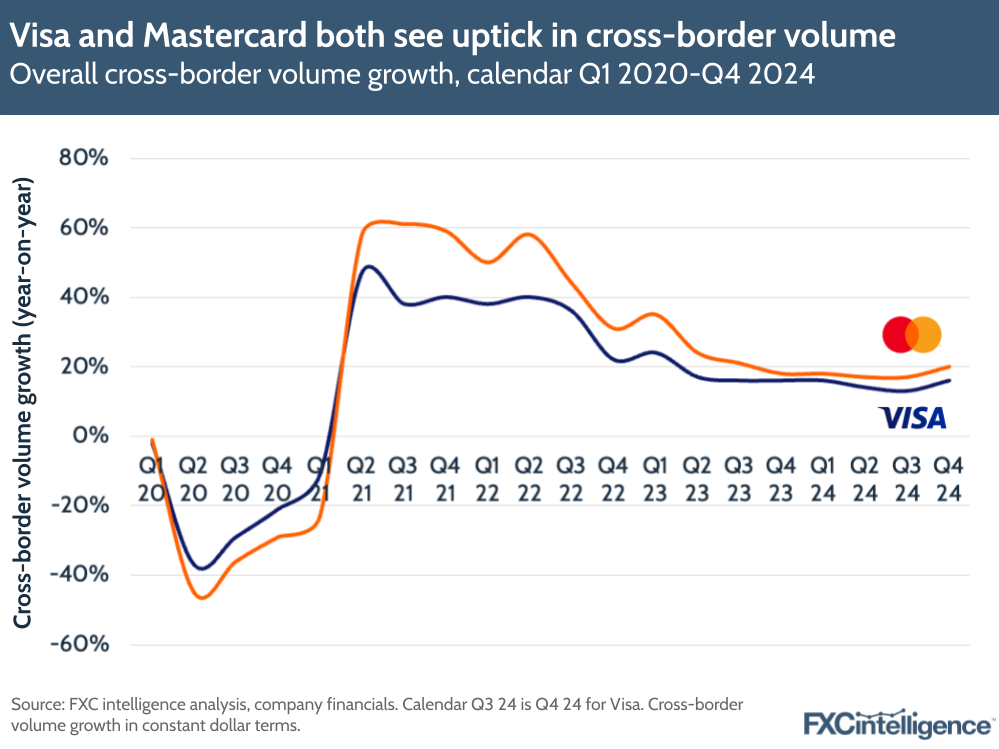

Tracking Visa and Mastercard’s cross-border volume growth

While Mastercard and Visa don’t explicitly share cross-border volumes, both highlight volume growth. Looking at cross-border volume growth over time shows that in constant dollar terms, both companies saw an uptick in cross-border volume YoY, with Mastercard seeing 20% cross-border volume growth while Visa saw 16% volume growth.

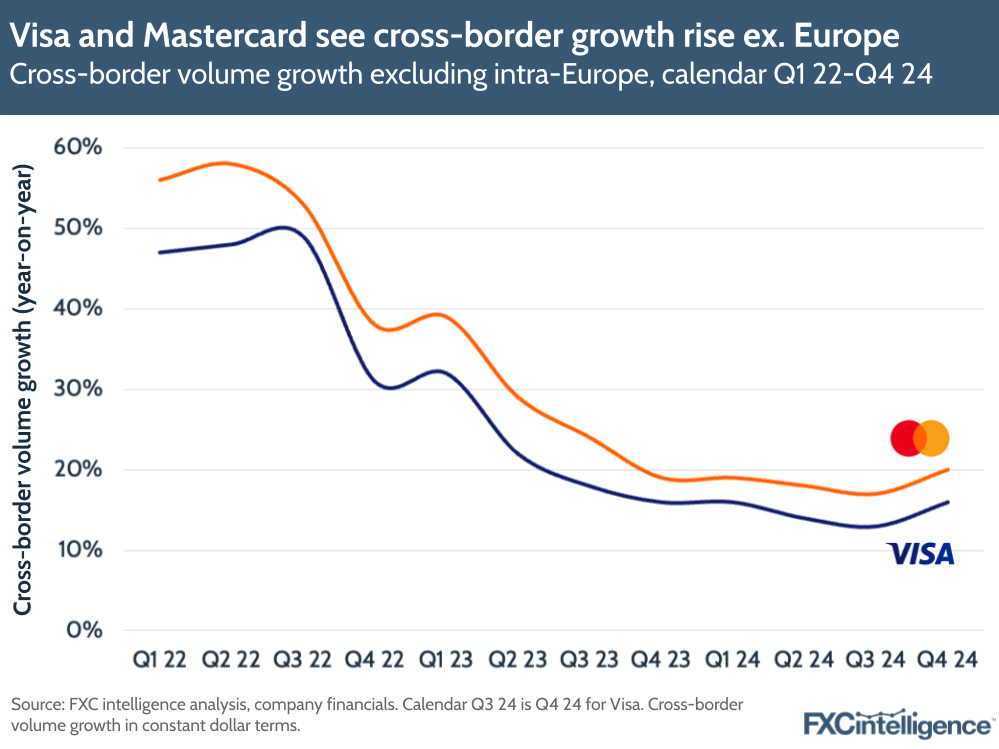

For both companies, cross-border volumes continue to be key drivers to growth, and this extends to their performance excluding Europe, where euro-to-euro sends require no currency conversion and therefore provide lower opportunities for revenue generation. Visa’s cross-border volumes excluding Europe matched its total volume growth for the quarter at 16%, while Mastercard reported 20% cross-border volume growth across the board.

The continued alignment between the two companies showcases that both are continuing to benefit from cross-border ecommerce and volumes, though Mastercard’s growth on a quarterly basis has consistently outpaced Visa’s growth over time.

Mastercard noted that it had continued to see strong consumer and commercial spending, with cross-border volumes benefitting particularly from a “pulling forward” of travel spending. The company also noted that its cross-border card-not-present volumes excluding travel (i.e. ecommerce volumes) rose 21%, driven largely by crypto purchases in Q4 2024.

Meanwhile, for Visa, card-not-present volume excluding travel and cross-border travel volumes both rose 16% YoY. Both were driven by strong consumer spending over the holiday period, but the company also noted that it had seen “solid performance of client portfolios” that benefitted Visa’s outbound Europe and APAC travel volumes. In the US, the company also noted the strong dollar aiding outbound ecommerce and travel volume growth.

Visa and Mastercard’s B2B2X expansion in Q4 2024

Visa and Mastercard are still only breaking out performance figures for Visa Direct and Mastercard Cross-Border Services in limited detail. However, both of these B2B2X services have seen continued progress in Q1 2025.

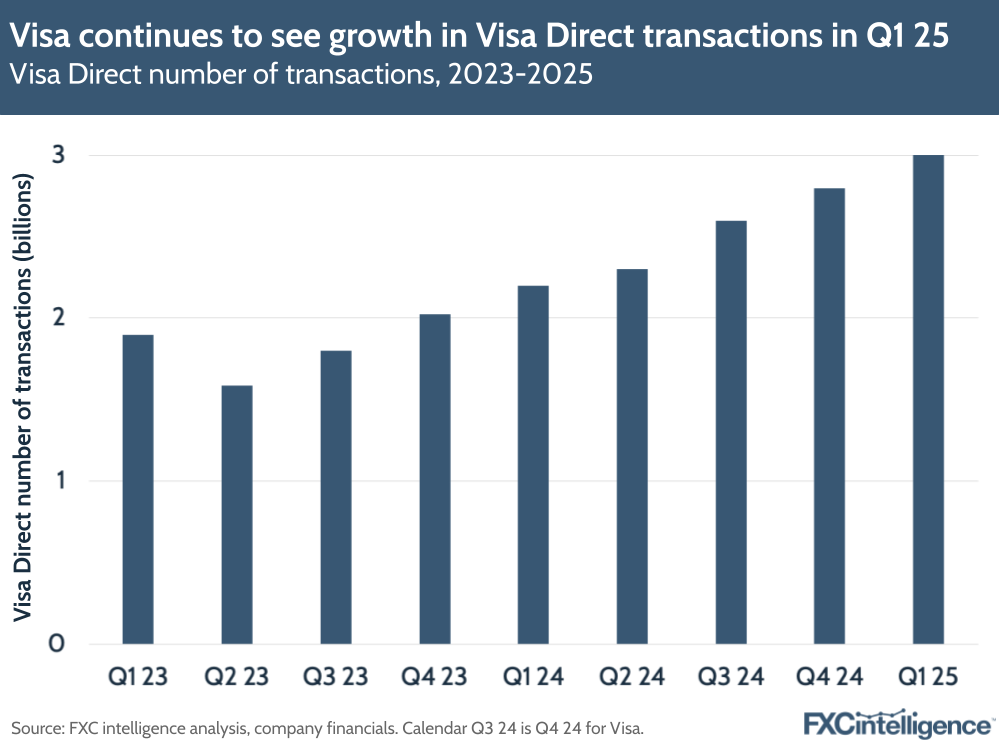

Visa Direct sees continued transaction growth

Visa Direct saw nearly three billion transactions during the quarter and processed more than 10 billion transactions over the last 12 months. The number of transactions grew by 34% YoY in Q1 2025, which the company attributed to growth in Latin America for interoperability among P2P apps.

Back in October, we spoke to Visa more about Visa Direct’s overhaul, in which it brought its four Money Movement brands – Visa Direct, Visa B2B Connect, Currencycloud and YellowPepper – together under the single moniker of Visa Direct, with the goal of creating a single solution suite connecting 8.5 billion endpoints globally.

Visa Direct growth, which is being supported through expanded partnerships with issuers and fintechs, is helping to drive Visa’s “new flows” revenue, which grew 19% YoY in constant dollar terms in Q1 2025. New flows essentially refers to the part of Visa’s business outside its traditional C2B card payments processing business, spanning B2B, peer-to-peer transfers and cross-border remittances.

CEO Ryan McInerney mentioned that Visa Direct remains a “very small” portion of the company’s cross-border transactions and payment volumes. A small portion for Visa transactions (3 billion is around 5% of Visa’s 64 billion transactions) is still large compared to other global money transfer players.

In addition, Visa Direct transactions are still growing at a significantly faster rate than processed transactions overall (34% versus 11%), and the impact of the system on the company’s revenue could continue to grow.

Mastercard Move forges new partnerships

Meanwhile, Mastercard also provides a number of B2B2X offerings through its Mastercard Move portfolio of money movements solutions, which includes peer-to-peer platform Mastercard Send and B2B-focused Mastercard Cross-Border Services.

While Mastercard didn’t break out revenue impacts for Move, transactions for this product set rose by more than 40% in Q4 2024, and it is contributing to growth in the company’s value-added services segment.

There was no specific mention on the performance of the recently launched Mastercard Move Commercial Payments – Mastercard’s solution for banks that allow them to handle 24/7 real-time payments for businesses. However, Mastercard did note a number of cross-border initiatives, including a recent tie-up with J.P. Morgan to integrate its tokenisation solution into J.P. Morgan’s Kinexys Digital Payments network, enabling J.P. Morgan’s clients to quickly send payments overseas via a blockchain. J.P. Morgan’s system is one of several forays into blockchain we’ve seen banks make lately.

Mastercard Move – which supports the transfer of funds to endpoints in over 150 currencies and across more than 180 countries – is also being used to support initiatives to emerging markets. In November, Mastercard partnered with the BCP Group to use Mastercard Move to support cross-border payments to multiple markets in Africa.

The movement of Mastercard Move (and Visa Direct) to supporting these markets – and particularly supporting wider policymakers on real-time payment initiatives globally, as we discussed with Mastercard last year – reflects the growing movement to tap into a burgeoning remittances and B2B payments market in new areas.

Though Mastercard Move and Visa Direct may currently be a smaller part of these companies’ transactions globally, this could change as banks and financial institutions increasingly seek to tap into new cross-border opportunities abroad.