At its Capital Markets Day (or Owners Day) last week, money transfer provider Wise highlighted its latest growth figures, while discussing the next phase of its ambitious growth plans for investment. Here are the key findings from its presentation and preliminary FY 2025 results.

At its recent investor day, Wise remained clear on its ultimate mission – providing convenient, low-cost and fast transfers globally. However, the company is continuing its shift from enabling consumer payments to enhancing its business payments suite and providing its own infrastructure as a solution for banks and services.

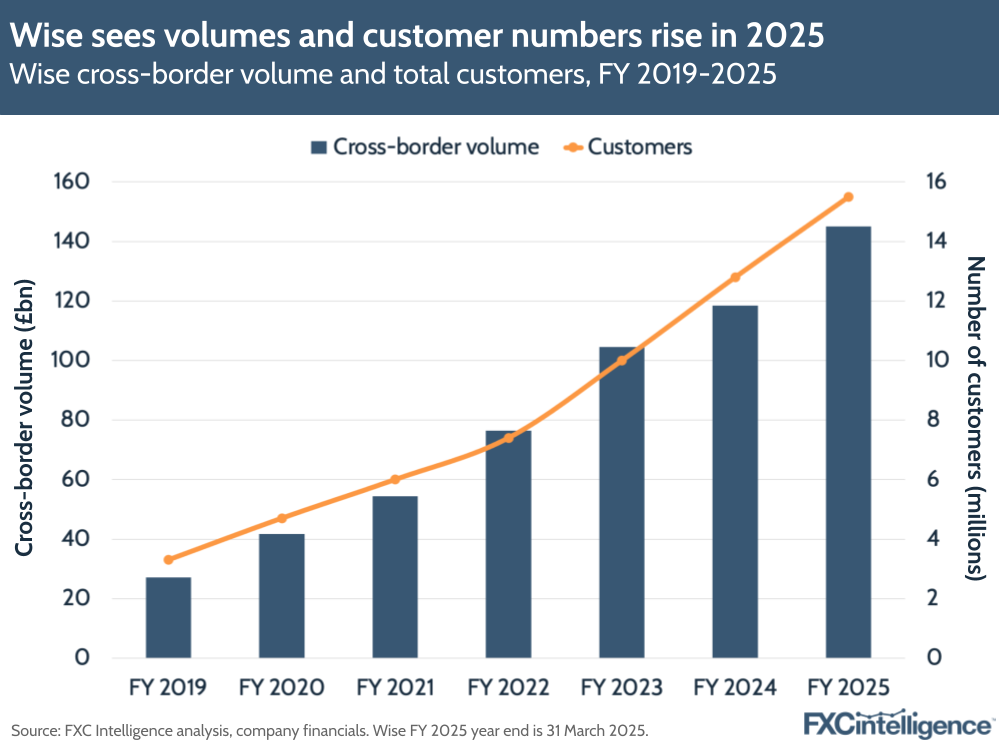

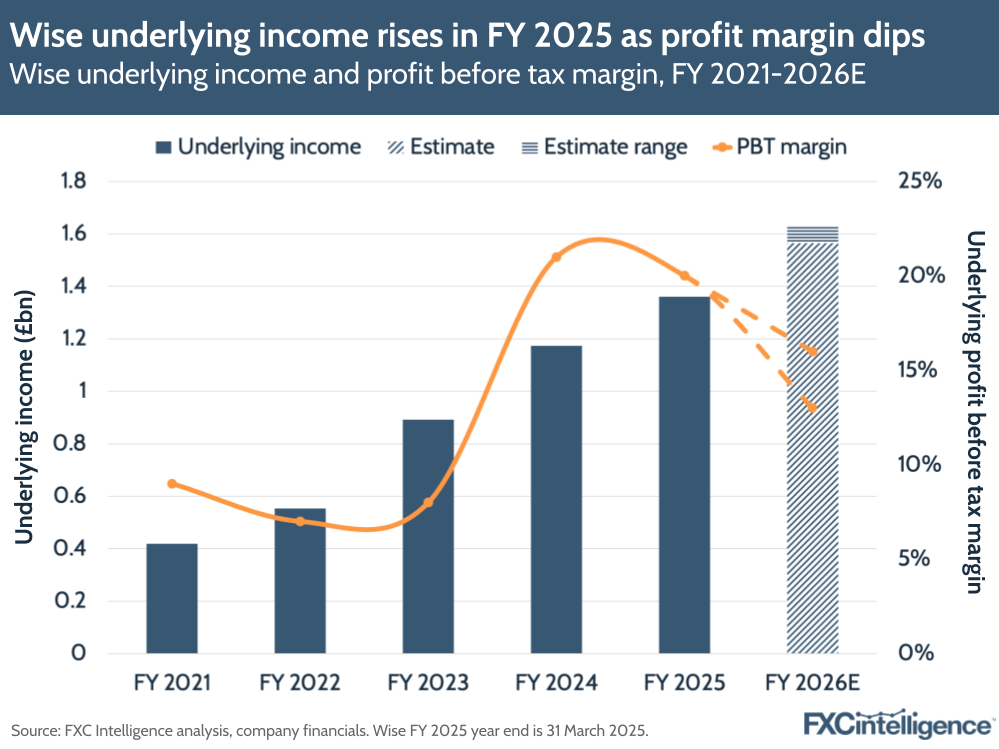

Since Wise listed in 2021, it has more than doubled its customer numbers and is moving three times as much cross-currency volume. Based on preliminary results for FY 2025, the company saw its underlying income rise 16% to £1.36bn on the back of volumes rising 22% to £145bn.

However, the company has set its sights on capturing a much greater share of the global cross-border market. In particular, Wise CEO Kristo Käärmann emphasised that a £170bn annual revenue pool (contained mostly within FX margins from banks) was the company’s immediate disruption target.

To grow its share of the space, the company has been continuing to build out its own proprietary cross-border infrastructure, growing its number of licences and local payout capabilities globally and continuing to deepen its products for businesses, specifically SMEs, which it already sees a high amount of business from.

Amid this, Wise is also heavily investing in Wise Platform, its B2B infrastructure that allows banks, fintechs and large enterprises to embed Wise’s cross-border capabilities via API. Similar to other B2B2X plays we’ve seen crop up in the industry (see Visa Direct or Euronet’s Dandelion solutions), the product would allow Wise to capture more cross-border volumes share from global banks without having to acquire customers directly.

Below, we’ve highlighted some of the main pieces from Wise’s latest investor day, as well as analysing its financials to give a more in-depth picture of its place in the industry.

Wise’s earnings and key drivers for FY 2025

Alongside its investor day presentation, Wise offered up preliminary results for its financial year for 2025 (which spans April 2024 to March 2025), emphasising that these results were still yet to be confirmed “pending to its yen growth process”.

Wise has moved to using underlying income growth as a demonstration of its ability to eliminate the impact of growing interest income on its core results. Driving its predicted 22% cross-border volume growth in FY 2025 was a 21% rise in active customers to 15.5 million.

Wise CFO Emmanuel Thomassin said that customer growth had been driven by trust in Wise’s low-cost, fast and reliable products. Pricing has also been a significant investment for Wise, with the company claiming it now charges on average 56 basis points (i.e. 0.56%) across its transactions. Speed has also been a key driver, with the company now enabling more than 65% of its payments instantly, with 95% of payments completed within 24 hours. Other drivers included SMEs growing adoption of Wise features, Wise’s push to grow its number of payout countries and more partnerships on Wise platform.

Despite high investment, Wise continues to see a positive profit-before-tax (PBT) margin of 20% – down one percentage point compared to FY 2024, but still at the high end of its expected range for the year. Calculated against its underlying income, this gave the company a PBT of $272m in FY 2024.

Going forward, the company has reiterated its previous medium-term guidance, with underlying income expected to grow at 15-20%, which would bring it to between £1.56bn and £1.63bn in FY 2026, based on the preliminary FY 2025 results. Wise opted to maintain its medium-term PBT projection at 13-16%, a decline from this year, but the company stressed it expected this margin to be at the high end of the range in its FY 2026 results as the company continues to ramp up its investments.

Wise Account’s growing impact

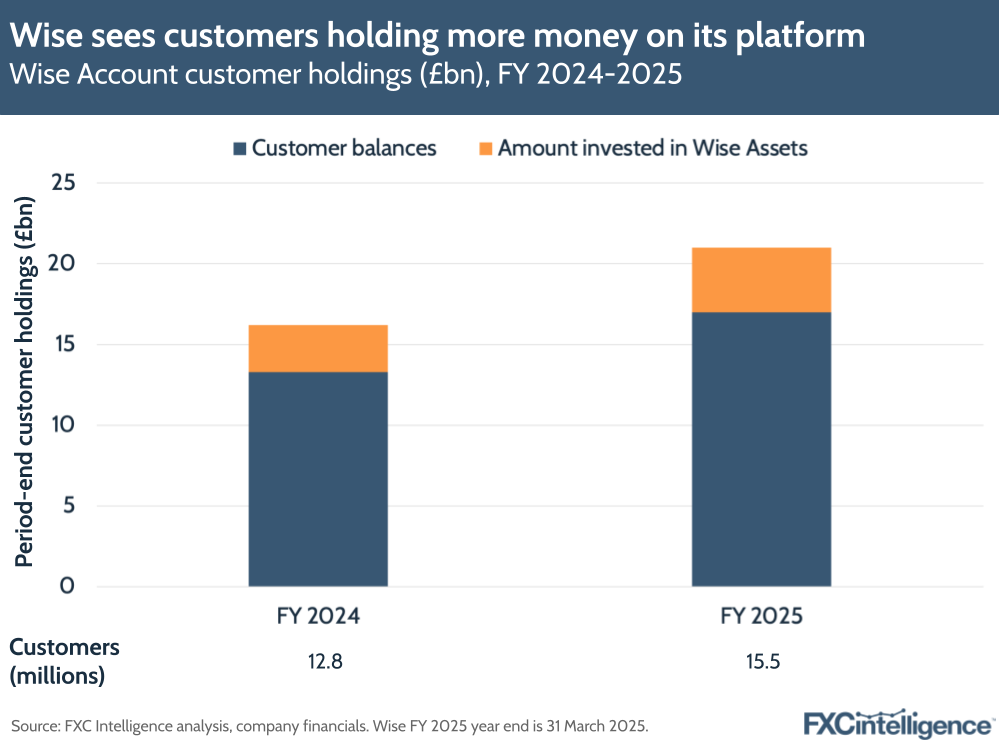

Wise has seen a significant rise in customer balances held across both its personal and business accounts, with c. 50% of the company’s active personal customers and 60% of Business customers having adopted the Account product.

Overall, customer holdings rose to more than £17bn with the company, while investing an additional £4bn in Wise’s assets product. This brought total customer holdings with Wise to £21bn at the end of FY 2025, up 30% from FY 2024.

More than just a transactional service, Wise is increasingly seeing customers looking to hold money on its platform ready to pay or convert to other currencies, which is deepening their engagement with the company.

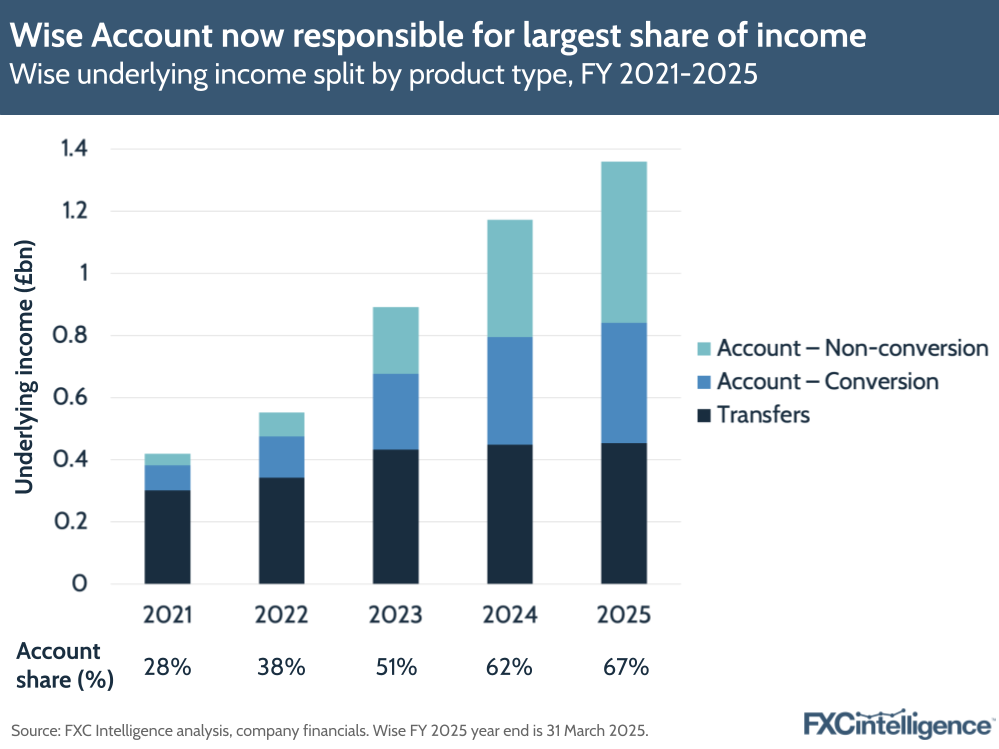

Income for Wise Account – its multicurrency account offering that allows customers to hold money in 40+ currencies as well as spend it using a debit card – has grown substantially faster than transfers income over time, with a 66% CAGR between FY 2021 and 2025. This is also faster than Wise’s overall rate of income growth during the same period (34%), signalling the company’s significant shift away from being transfer-led to account-led.

In FY 21 and FY 22, the key driver for Wise Account was conversion income, which Wise receives from FX fees when customers convert money between currencies within their account. However, in the years since this has been overtaken by non-conversion income, which saw a 93% CAGR from FY 2021 to FY 2025, and now accounts for 38% of the company’s overall underlying income. Of this non-conversion income in FY 2025, 42.5% was made up of card fees, 29% from interest income and 28.5% from other fees.

As customers hold and spend more with Wise, they are contributing an ever increasing proportion of the company’s growing income, highlighting the importance of this product to Wise’s strategy. One of the company’s many noted investment cases was in Wise Interest, its instant access savings product, which is helping drive returns through customers holding and spending more through the business, driving interest income and interchange revenue.

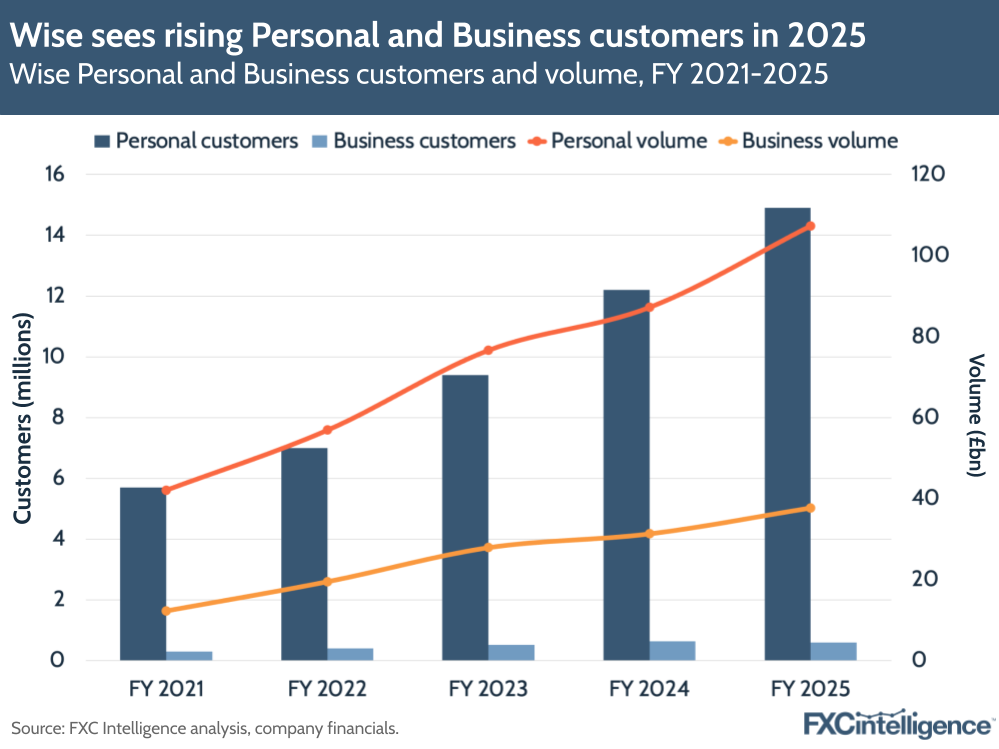

Wise sees growth across Personal and Business segments

Breaking down customers and volumes, Wise is still largely consumer-led, with the company’s Personal customers accounting for 74% of cross-border volume and growing 23% in FY 2025. Having said that, a large portion of the presentation revolved around how Wise is aiming to grow its business segments, spanning business debit cards, payroll and B2B payments abroad.

The company currently has over 600,000 active business customers. Taking this into account with its 15.5 million overall active customers for FY 2025, this would put its number of personal customers at around 14.9 million for the year. However, despite being a fraction of the company’s overall customer numbers, Wise business is still contributing around 23% of the company’s revenue, with volumes growing 20% in FY 2025.

During the presentation, Wise said that the company’s strategy is to continue to invest in features that help businesses move more transaction volumes and holdings to the company to generate income. Though the majority of its business has been focused on micro, small and medium-sized businesses including SMEs, the company is looking to make more investments to see a greater proportion in SMEs and larger businesses over time.

These will focus on improving services and making them more secure; building out its networks to enable more local payment methods; and introducing new features and adapting existing ones to add more features. For example, allowing businesses to pay hundreds of thousands of invoices through a Wise bill payment solution, as well as introducing a more enhanced version of card acceptance the company referred to as “Checkout by Wise”.

Wise’s drive to boost its business segment reflects similar moves by other players in the money transfer space as it moves to make use of its growing infrastructure and develop new products. As our market sizing data shows, a fragmented B2B payments market continues to hold the strongest TAM for non-wholesale cross-border payments, showing that there is still a lot of room for Wise to manouevre in this market.

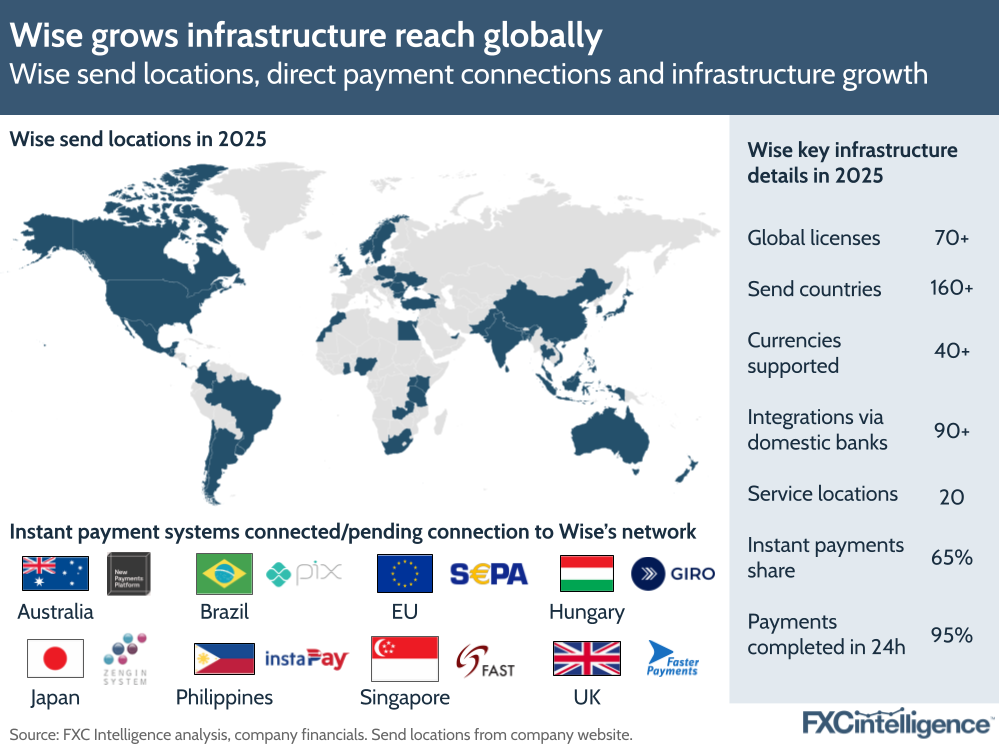

How Wise is growing its reach globally

Crucial to Wise’s growth has been its pursuit of expanding to new markets. The company now has more than 70 global licences and over 90 connections with local banks, with money transfers supported to more than 160 countries, as a result of 14 years and £3bn of investment.

As part of its expansion, a recent focus for Wise has been growing the number of real-time domestic payment schemes that it has forged connections with to speed up payments. Wise already has six connections live across Europe, Hungary, Singapore, Australia, UK and the Philippines.

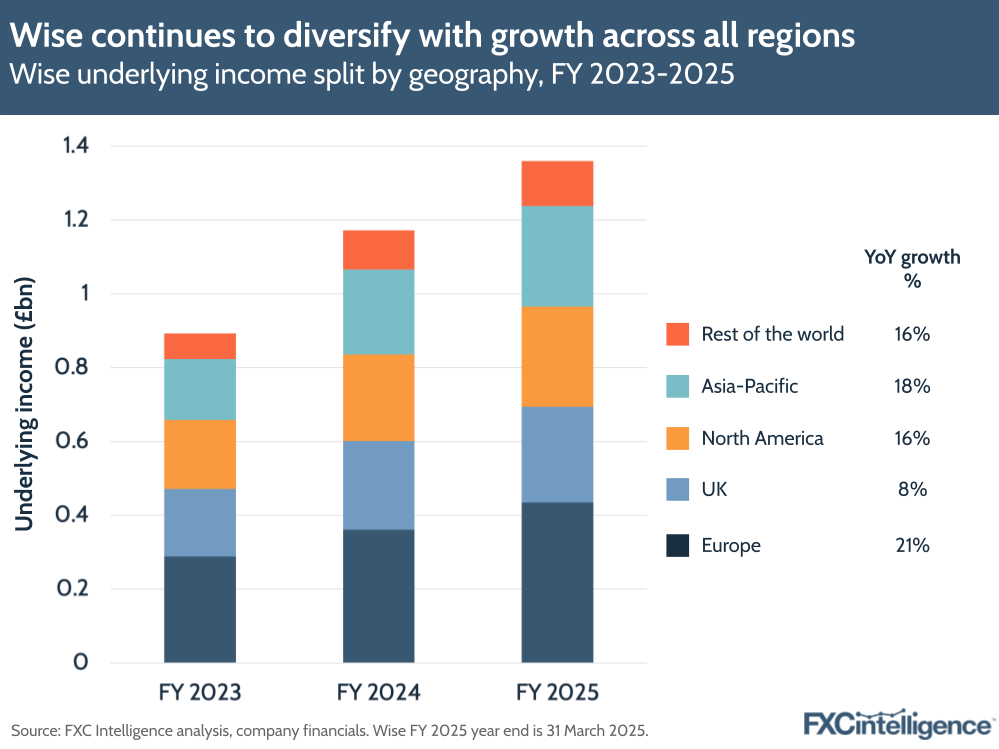

Reflecting the growth of its platform, Wise continues to diversify its underlying income across geographies over time, spanning the UK, Europe, APAC, North America and the rest of the world. The company grew across all regions, but continues to see its strongest growth in Europe (where it also sees the majority of its income), followed by APAC and its Rest of the World segment, while showing lower growth in the UK.

Over the next two years, Wise is planning to invest an additional £2bn into its infrastructure, according to Wise CTO Harsh Sinha. “Fundamentally, we believe whoever has the best infrastructure in this space will win in the longer run,” he said.

Overall, Wise sees the infrastructure it has created as moving the company through three phases: from its historical transfer offering (still contributing a significant chunk to the business today); to its current combination of Wise Account and Wise Business; to a future in which Wise Platform – its white-label product enabling banks, fintechs and enterprises to piggyback off its global payments infrastructure – could help it capture a significant portion of global payments flows.

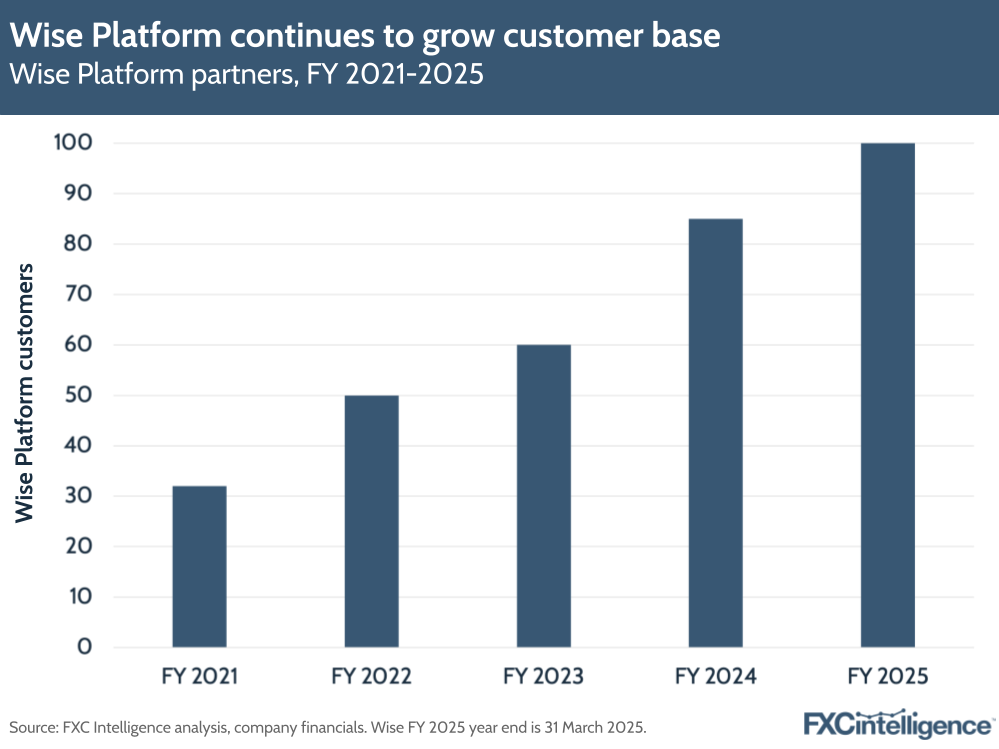

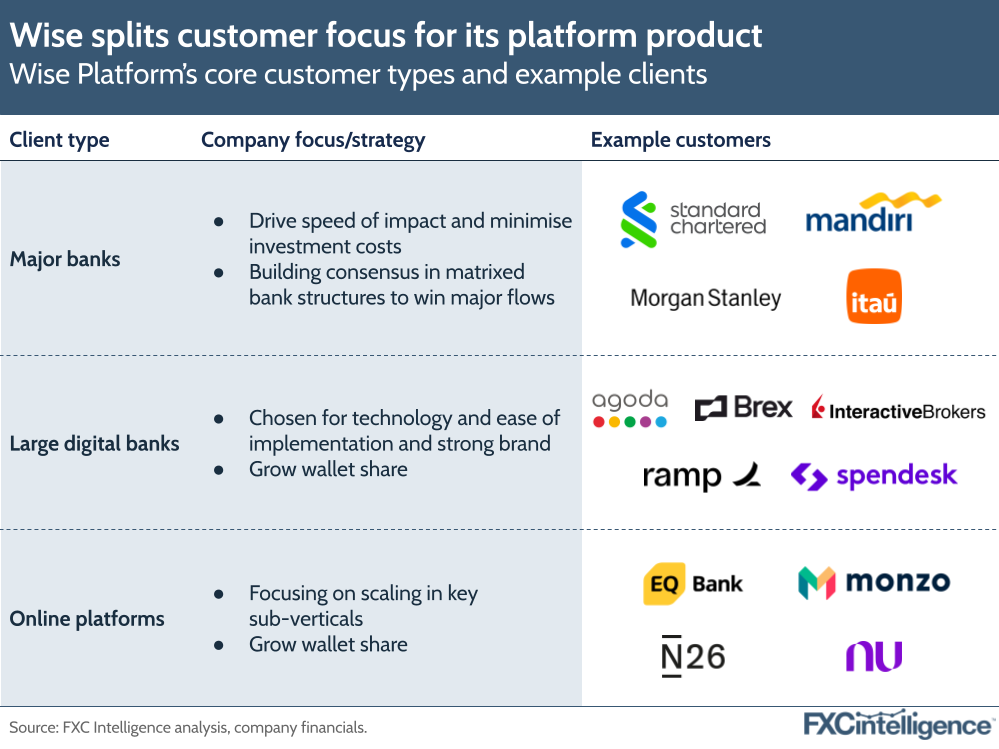

Wise Platform: Scaling Wise’s B2B2X offering for banks

In previous earnings calls, Wise has held back on the contribution of Wise Platform to Wise’s overall mix. However, this is starting to change as the company places more significance on the product as a major driver of future growth.

More than 100 financial institutions are now integrated with Wise Platform, spanning a mix of major banks, large digital banks and online platforms. Recent new additions include Brazilian digital bank Nubank to provide multi-currency accounts and international debit cards; Standard Chartered to power remittances out of Asia and the Middle East; and Morgan Stanley to enable fast and low-cost cross-border payments for businesses.

Wise expects in the medium term that Wise Platform will grow to reach approximately 10% of the company’s FX volumes, up from 4% today (which would be around £5.8bn, based on preliminary FY 2025 results). However, Wise Platform’s MD Steve Naudé said that ultimately the company expects it will account for the majority of volumes as it seeks to integrate Wise’s infrastructure with tools that customers are already using at Tier 1 and Tier 2 banks.

Naudé asserted that recent partnerships with Wise Platform show that more banks are willing to invest in cross-border. While this hasn’t always been a priority, it has started to shift as low-cost, faster and more efficient infrastructures emerge and prove a more attractive alternative than banks for consumers and businesses looking to send money abroad. As banks invest in cross-border (i.e. through a partnership with Wise), this then will encourage other banks to invest, creating a network effect that Naudé said would help boost the platform.

The growth of Wise Platform will lead to some near-term wins, but it will likely take some time to truly take centre stage of the company’s strategy, given a typically longer sales process to connect with banks. Naudé said that the platform is expecting faster growth in the short and medium-term from some businesses, but banks such as Standard Chartered may see their contribution to grow over a medium-term timeframe.

Over the medium term, the company is looking to continue onboarding new partners while also ramping up business across its existing clients. As it continues to see demand, the company is growing its teams in APAC, Europe and the US to serve clients in these regions.

One question during the presentation was on how Wise is looking to differentiate itself from other similar B2B2X plays on the global market, particularly Visa Direct. Sinha responded that the early investment in forming direct connections to enhance Wise’s infrastructure – as well as the fact that it has built a consumer network first and taken learnings about the pain points from this infrastructure – puts the company ahead of its competitors.

Why Wise needs to diversify

Wise’s recent investor day underscored its evolution from a consumer-facing money transfer player into a global infrastructure provider for cross-border money movement. With growing enterprise partnerships, increasing customer balances and strength across different regions, the company has diversified to become a resilient, profitable company.

Strategic investments in proprietary infrastructure, embedded B2B services and business-focused products are positioning the company to scale well beyond its current footprint. In addition, Wise’s focus on transparency and efficiency continues to challenge legacy banks, and ultimately it is targeting the B2B volume of many of those same banks through its Platform offering.

The continued growth of Wise’s offerings beyond transfers will prove important, particularly (as we’ve previously reported) the company’s investments in lower pricing also mean it is decreasing its take rate per transaction. This is where continued investments in its Wise account product, as well as diversifying to offer new business services, will prove fruitful in additional revenue streams in the future.