A year after it launched, HSBC’s multicurrency and money transfers app Zing is closing. We review its positioning, performance and strategy and consider the challenges in competing against Wise and Revolut.

Just weeks after the one-year anniversary of its launch, news broke that HSBC was closing its UK-based standalone digital money transfers and multicurrency account product Zing.

Writing on its official website, in a notification that was replicated across its social media accounts and in emails to customers, Zing cited “changes in strategic business priorities” as the reason for the move. This was also echoed in a statement by HSBC, where the company confirmed that the decision formed part of a strategic review of the wider HSBC Group, announced in October, that has seen it streamlined into four key business areas.

“HSBC is focused on increasing leadership and market share in the areas where it has a clear competitive advantage, and where it has the greatest opportunities to grow and support our clients,” a company spokesperson said in the statement regarding Zing’s closure.

While the company has now stopped accepting new customers, existing Zing customers will be able to use all parts of the app, including its multicurrency wallets and money transfer services, until 2 April 2025. Customers who wish to convert non-GBP balances back into GBP are also able to do so without charge. After this point, no new funds will be allowed to be added, and customers will have until 22 May 2025 to transfer all remaining balances to alternative providers, at which point all Zing accounts will be closed.

The move highlights the challenge of launching new products in the digital-first consumer money transfers space, with Zing directly competing with major players Wise and Revolut. With this in mind, what were Zing’s main challenges and successes, and what lessons can the industry learn from its strategic approach?

Zing’s market positioning and offering versus competitors

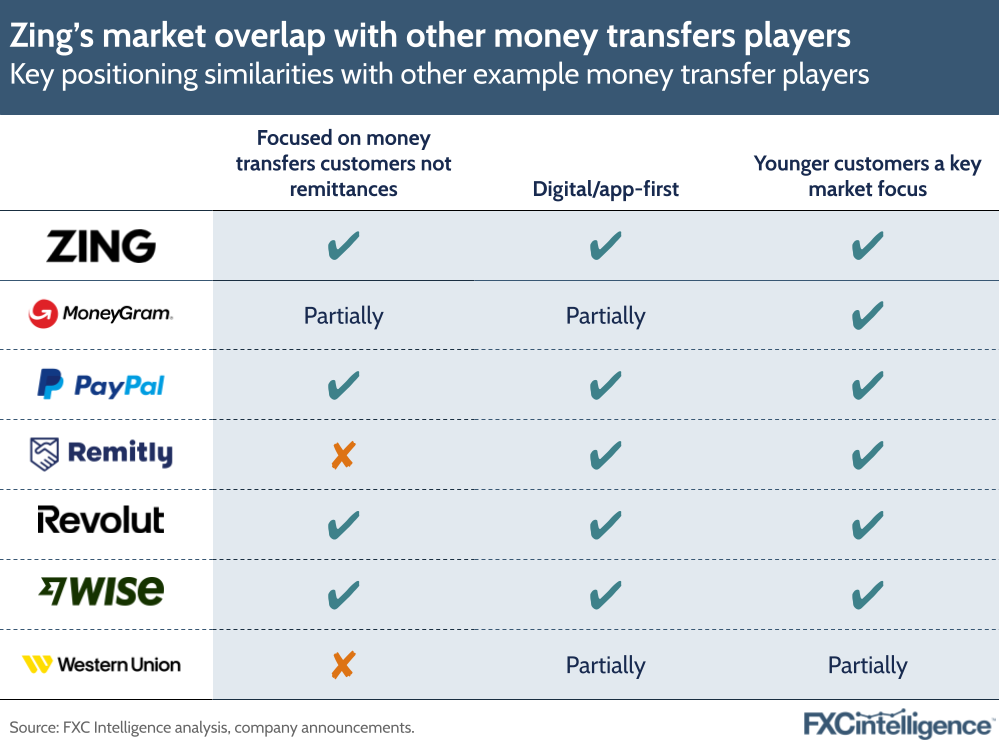

As we explored in a market analysis report published shortly after Zing’s launch in January last year, Zing came out in a market where there were already several major players offering similar services, although fewer that were combining both money transfers and multicurrency accounts into a single solution targeting younger customers.

In terms of its money transfers offering, Zing had a similar proposition to PayPal, Wise and Revolut – both Wise and Revolut have similar multicurrency solutions that allow customers to hold balances in multiple currencies. Zing also had some overlap with Remitly and MoneyGram, although with a far greater focus on sending to developed markets. In this sense, Zing initially looked to be positioning itself to target the younger expatriate market.

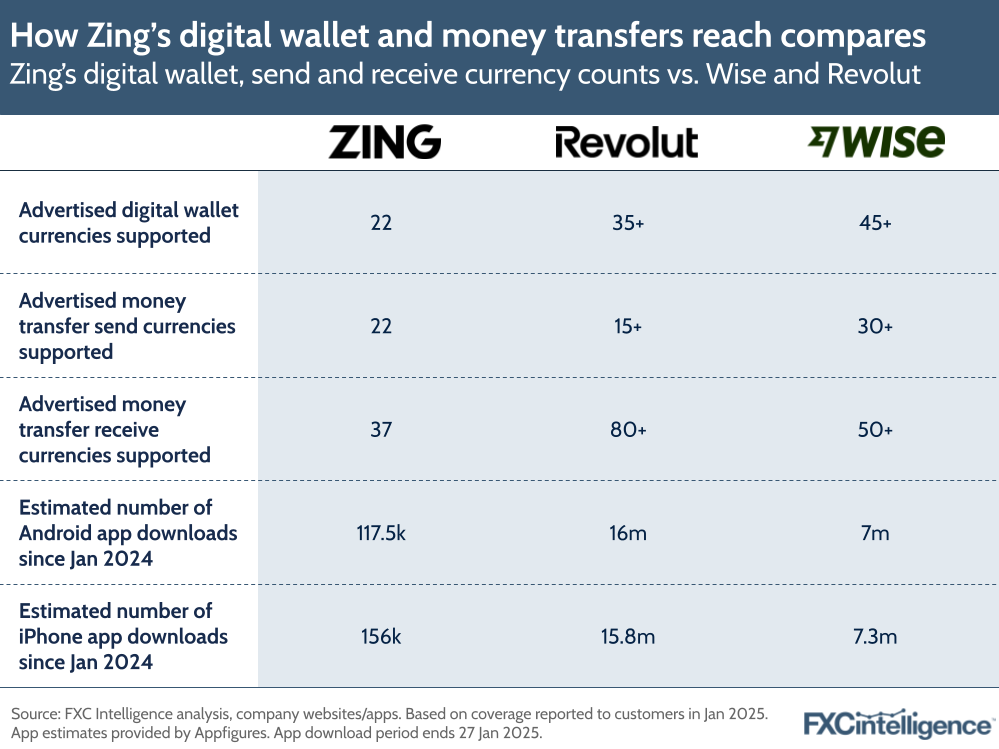

While at launch Zing enabled customers to hold balances in up to 10 currencies, by January 2025 this had grown to 22. This was lower than the 35+ and 45+ offered by Revolut and Wise respectively, but does cover the majority of the same markets. All of the currencies Zing offered digital wallets for are also available to Revolut customers, while all except one are available to Wise customers.

In terms of money transfers, Zing ultimately supported slightly more send currencies than those advertised by Revolut as of January 2025, although slightly less than Wise, but remained below both on the number of receive currencies it supported.

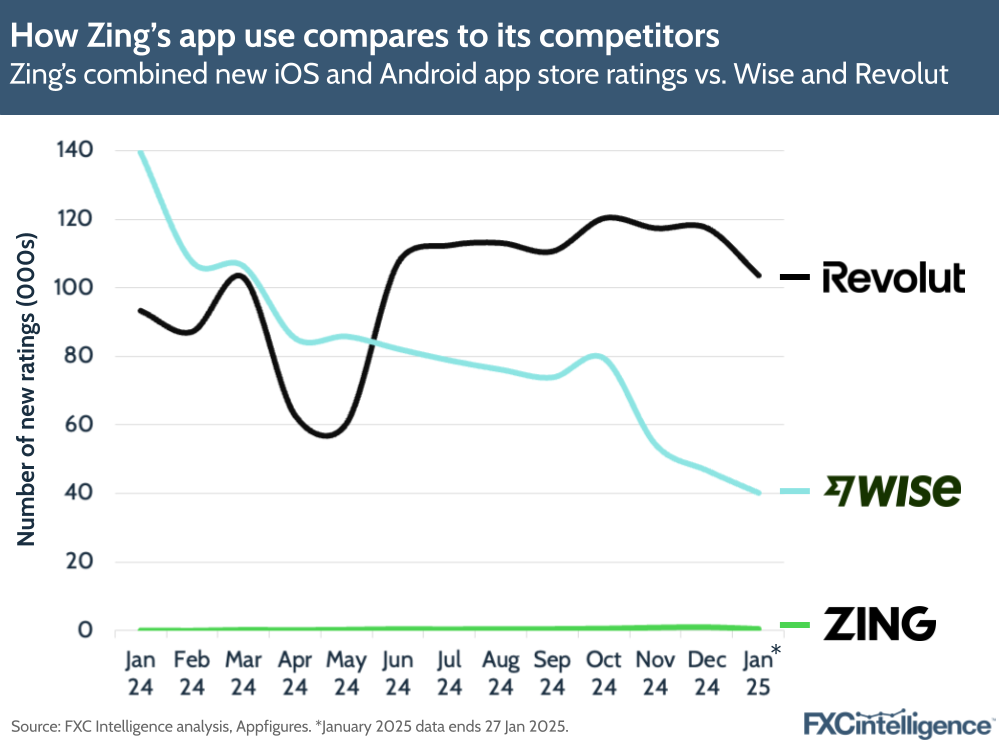

Inevitably, Zing also remained considerably below its competitors in terms of the number of downloads, having achieved an estimated 274,000 downloads across both its iOS and Android apps during the course of its operation, according to data provided by Appfigures. By contrast, Revolut is estimated to have seen around 32 million downloads over the same period, while Wise is thought to have reached around 14 million.

Crucially, however, not only are Revolut and Wise far more established products, which have had considerable venture capital to help support their growth, but they also accept customers from numerous locations globally, while Zing remained limited to the UK market.

Performance across 2024

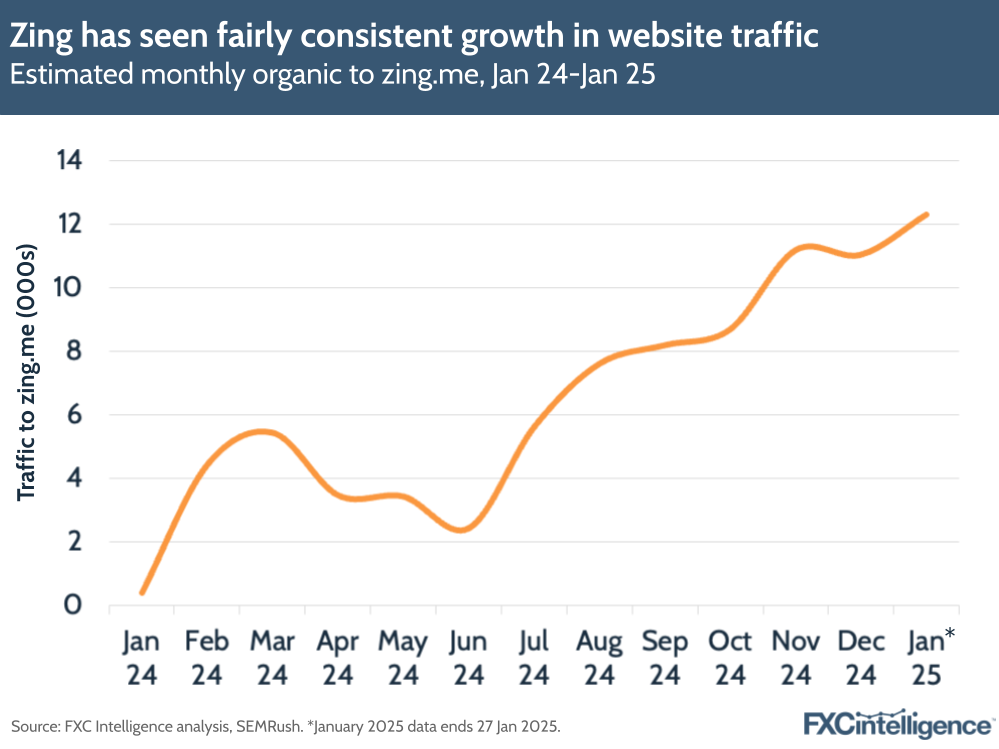

While HSBC has not shared customer numbers for Zing, there are a number of data sources that paint a picture of a brand that was growing over the course of the year. Estimated traffic data for the company’s website, zing.me, shows consistent month-on-month growth in almost every month from June onwards, with organic traffic in December being around twice that of March. Notably, the data suggests that while Zing did engage in some paid campaigns to acquire further traffic, these were largely in February and September, with no notable paid traffic identified in most months of the year.

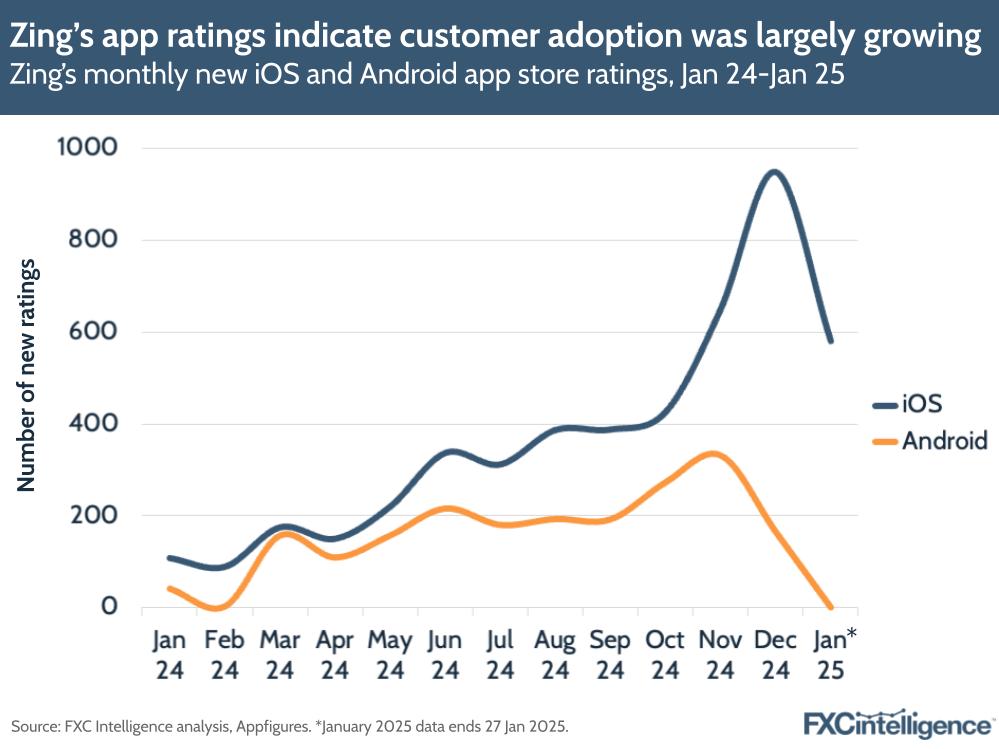

App ratings, which are something of a proxy for overall app downloads and usage, also saw fairly steady growth throughout the year. Data from Appfigures shows a consistent climb in the number of new ratings each month throughout 2024, although there was a notable drop off on Android from December and on iOS in January 2025.

By contrast, while the overall scale of new ratings was far higher for Revolut and Wise, they did not see the same rate of growth. Revolut saw its app ratings remain flat for much of 2024, save for a dip in Q2, and Wise saw the number of new ratings it received each month fall throughout the year.

Marketing strategy and travel-led Gen Z customer focus

An analysis of Zing’s marketing strategy suggests that the company had quite a focused approach, built around a core audience profile.

While the company’s blog suggests it was engaging in some attempts to draw traffic via search engine optimisation techniques, there is little evidence that this had yet gained much success for the brand. There is also evidence that Zing was engaged in affiliate marketing, with referrals from travel, expat and consumer finance-related brands.

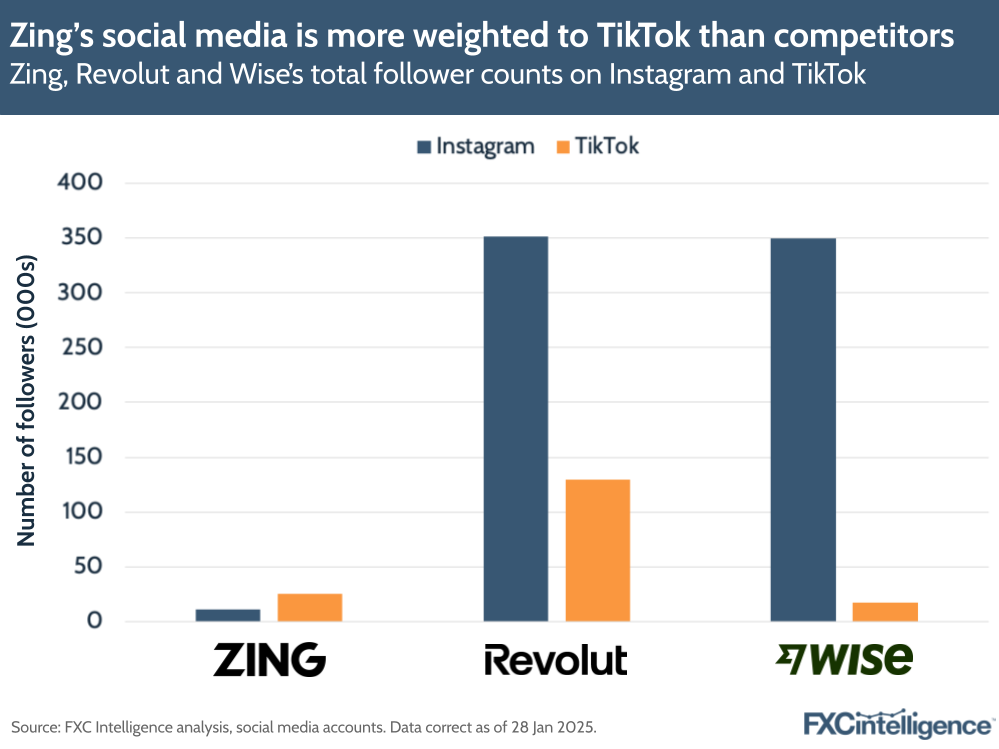

However, these tactics appear to have been peripheral to its core marketing focus: social media. Zing was highly active on both TikTok and Instagram, with the former dictating its focus on short video-based content replicated across both platforms.

Crucially, unlike Revolut and Wise, Zing took a TikTok-first approach. Revolut and Wise both have more followers on millennial-focused Instagram, with Revolut’s Instagram account having almost three times the followers of its TikTok account, while Wise’s Instagram account has more than 20 times the followers of its TikTok account.

By contrast, Zing has more than twice the number of followers on Gen Z-focused TikTok than it does on Instagram, and also has more followers overall on TikTok than Wise, despite being considerably younger.

The social media content Zing produced also appears to focus on a Gen Z audience, and references several trends that originated on TikTok, including videos filmed in popular shopping areas where Gen Z passersby are challenged to answer currency-related questions.

Data from Appfigures also indicates that users aged 18-24 represented its biggest customer base, while data for Wise and Revolut indicates their biggest groups are users aged 25-34. In all cases the audiences skew slightly male.

Within this focus on Gen Z, Zing made considerable use of competitions to both engage its customer base and broaden its reach to potential users. This saw it run 12 major competitions over the course of its existence, two of which were based on partnerships, one with its card and open banking partner Visa and the other with the football team Brentford FC.

Zing became the official international payments and remittance partner for English Premier League club Brentford in August 2024 and has since featured players in several social media videos, as well as offering tickets for a key match as a competition prize.

Visa, meanwhile, partnered with Zing to offer a high-end trip to attend the 2024 Olympic Games in Paris, including tickets for the athletics and closing ceremony.

Zing’s social media largely pushed the app as a solution for travel, which is reflected in the competitions it ran. These largely focused on high-end luxury travel experiences, typically including eye-catching activities such as winery tours, helicopter rides and hot air balloon experiences.

This travel-first strategy aligns most effectively with its multicurrency wallet capabilities rather than its money transfer capabilities, with the vast majority of its social media content focused around Zing’s multicurrency solutions.

However, there were some limited exceptions, including its competition to win a “nomad travel bundle” that included a £500 travel voucher and a variety of travel gadgets themed around working abroad.

Initially presented alongside the hashtag #ZingSurprizingRewards, Zing’s competitions for the most part required applicants to be members of Zing, although in some cases competitions appear to have primarily been used to grow reach and follower counts. This customer-first approach was clearly intended to incentivise sign-ups but also centre rewards within the wider Zing user experience.

This was also echoed in the company’s other rewards, which included a choice of 20 fee-free international ATM withdrawals or converting up to £1,000 into other currencies and paying no FX conversion fees for “founding members”, as well as 10% off Booking.com stays for a limited period.

Zing also added fee-free conversions on the first £500 of FX transactions every month in June – a reward that was originally meant to run up to December 2024, but which the company extended to April 2025 earlier this month.

The challenge for bank spin-outs

Zing’s 2024 metrics speak to a company that showed potential for future growth with the right investment, however it is likely that HSBC felt that the ongoing levels of investment required were not compatible with its wider strategy. Initial reporting on the closure by Financial News also suggests that increased resourcing requirements associated with a project to increase Zing’s fraud controls and support its AML compliance may have contributed to this.

Wise and Revolut, meanwhile, were given the opportunity to grow under very different circumstances. Both have raised $1.7bn in funding each since their launches in 2011 (Wise) and (2015), allowing them considerable runway to grow before they needed to generate a profit. By contrast, Zing ultimately forms part of a publicly traded company, meaning it is likely to have faced far more restrictive resourcing than either fintech rival enjoyed during their early years of growth.

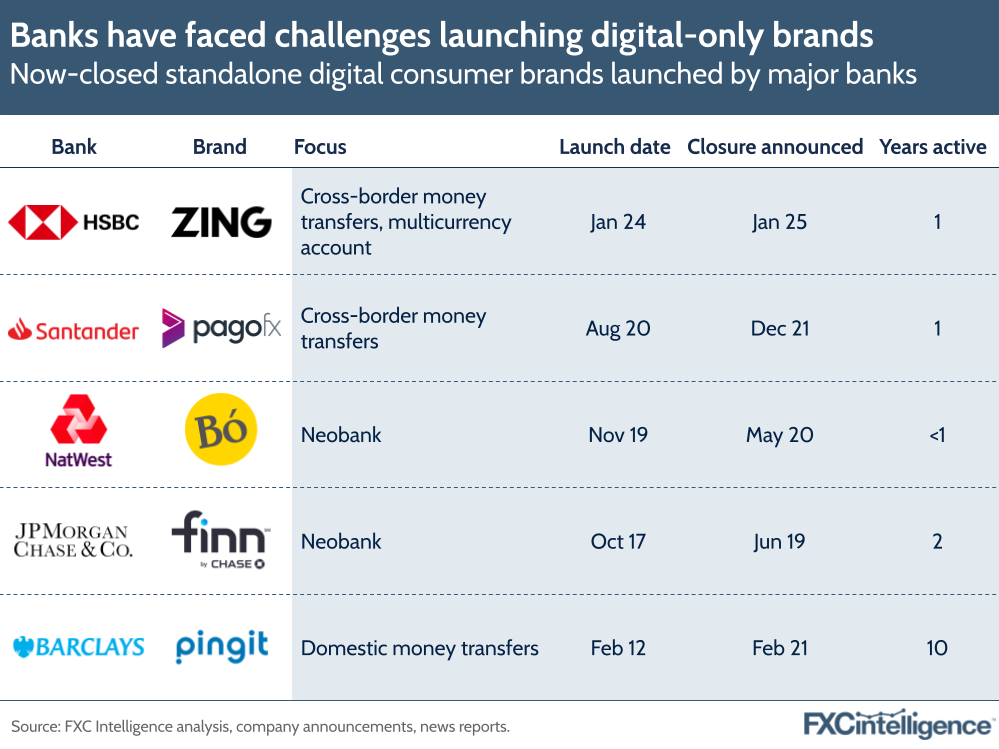

This challenge is a common issue for consumer-facing fintech challenger brands launched by banks, and may explain why there are multiple examples from other banks that are no longer operational. Within the money transfer space, Santander’s PagoFX was closed after a similar period of operation to Zing in 2021, while other examples include neobank launches Bó and Finn, from NatWest and JPMorgan Chase respectively.

Was 2024 the right time to launch Zing?

Regardless of funding levels, if HSBC had launched Zing in the early to mid-2010s, it may have had a much easier path to success. At the time Wise and Revolut launched, the offerings available to consumers were much less sophisticated, and typically not geared towards the digital-first expectations of a younger audience.

There were also no major entrenched digital-first brands to compete with in this space, meaning that an earlier launch would have given Zing a chance to grow without the headwinds of two major, well-established competitors.

However, while there is a clear case for Zing to be a case of a good product launched too late, there is also an argument that Zing is a product that has been launched too early.

Zing’s positioning and marketing strategy showcase it as a brand that recognised that Gen Z has different expectations and behaviours to millennials, and tailored itself to effectively fit these in a way that more established brands have not prioritised.

However, this represents a divide in Zing’s offering. While it offered both international money transfers and digital wallet capabilities, the majority of the Gen Z audience it was targeting in its marketing were travelling for holidays, but had no need or requirement to send money internationally. This need is also catered to by other brands outside of the money transfers space, such as UK neobank Monzo, which includes transaction fee-free cross-border spending among its features.

Where customers were looking to send money, Zing prioritised corridors with higher send values but, due to the age of its customer base and therefore their average career levels, the typical send amounts are also likely to have been lower than those of a company targeting slightly older customers.

As Gen Z ages, it will retain a buyer persona that is unique to its group, but it will also increase its need for high-value money transfers as it sees a greater percentage of its cohort work and live internationally. A brand such as Zing may therefore have greater success once Gen Z is a slightly older, slightly more mature demographic, when its needs in the money transfer and multicurrency space specifically are more clearly differentiated.