The launch of the FedNow instant payments system in the US is a major milestone. But how will it change payments in the US, and could it support cross-border payments in the future?

The US is ramping up its adoption of instant payments, also known as real-time payments. Since 2017, hundreds of US banks have signed up to The Clearing House’s Real-Time Payments (RTP) Network, which processed around 1.8 billion transactions last year and is set to grow significantly in the coming years. Meanwhile, instant P2P payment apps such as Venmo and Cash App have become a mainstay for US consumers.

This month, the US Federal Reserve is launching FedNow – a new interbank clearing and settlement service that facilitates instant payments 24/7, 365 days a year. The hope is that a larger number of US financial institutions than ever before will be able to create new payment products with FedNow, thereby enabling instant payments for consumers and businesses.

This report takes a closer look at FedNow and its anticipated impact in the US, as well as its cross-border potential, with comment from several industry experts.

What is FedNow?

FedNow is a new service that banks and credit unions can use to send money to each other, with funds settling and clearing instantly – 24/7, 365 days a year. This separates the system from Automated Clearing House (ACH) and Fedwire (the Federal Reserve’s system for large payments), which only operate during certain time periods.

FedNow is not a payment method or a new currency, despite many in the US speculating that the service is a move from the Fed towards a CBDC. Rather, the service is more akin to a new payment rail that banks and credit unions can tap into in order to enable faster payments for their customers.

To achieve this objective, banks may also collaborate with other payment providers. US-based Fiserv, for example, recently said that six of its clients were in the FedNow Pilot Program, with another 20 committed to adopting the new instant payments system from the July launch.

It’s not currently known how many financial institutions across the US will adopt FedNow at launch (the Fed did not respond to our request for comment for this report). However, FedNow has been designed to be accessible to all financial institutions in the country.

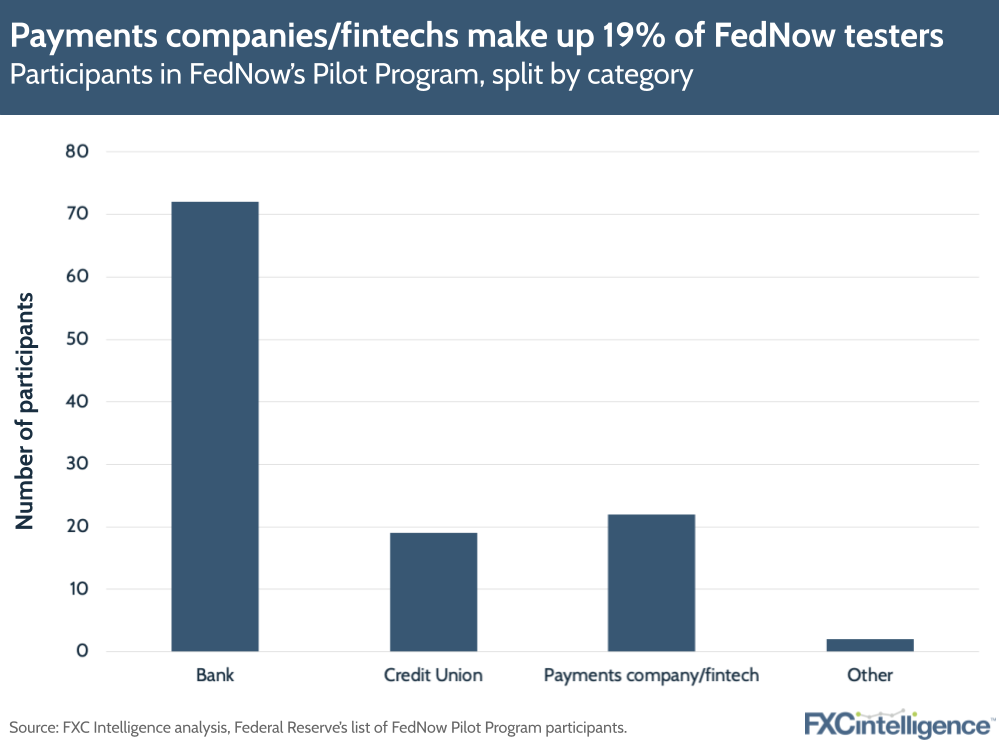

Launched in 2021, the FedNow Pilot Program included more than 120 participants, from major banks such as Goldman Sachs, BNY Mellon and JP Morgan Chase to smaller regional banks and fintechs such as Juniper Payments, ACI Worldwide and Finastra.

When looking at some of the named participants in the programme, it’s clear that banks have been the frontrunners, but the strong presence of payments companies highlights the role that they’ll be playing in helping banks and credit unions to implement FedNow into existing or new real-time payment solutions for businesses and consumers.

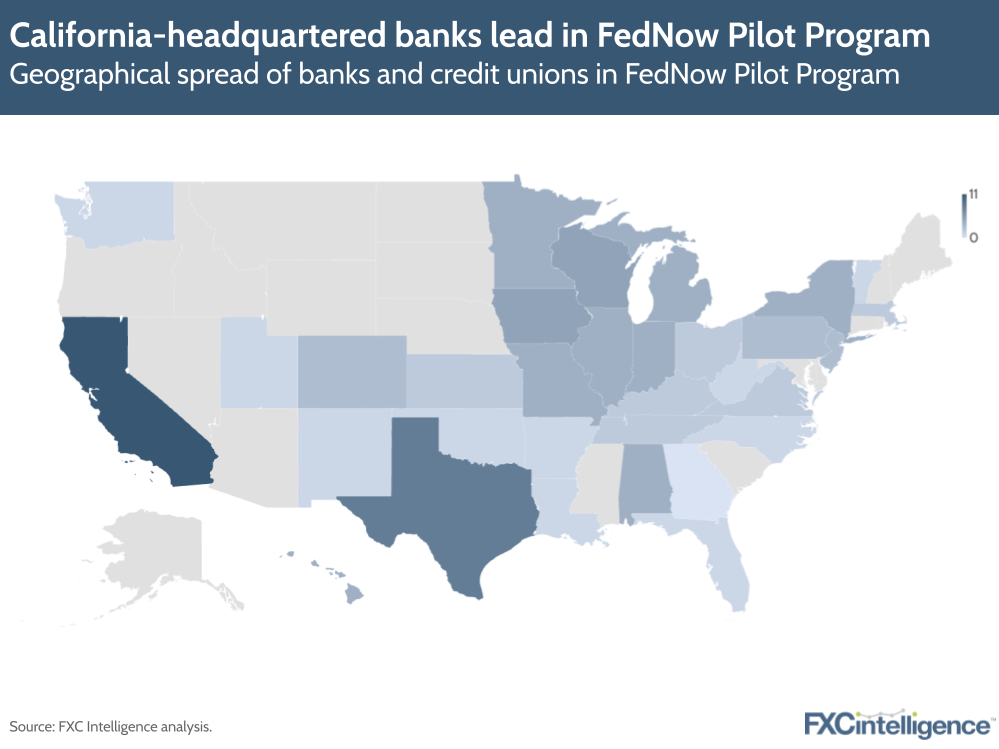

The graphic below shows where the headquarters of banks and credit unions in the FedNow Pilot Program are based. Though it should be noted that several big banks in the programme have branches across the country, this gives a sense of how far FedNow has taken a foothold across the US, as well as how much further it has to go in terms of adoption.

Why has the US taken longer to introduce instant payments than other nations?

Despite being one of the biggest payment markets globally, the actual system for moving money in the US is still slow. Most of the time, it will take anywhere between one and three days for funds to appear in a recipient’s account after a payment is made.

This is because most payments are made via the Federal ACH system, which since the 1970s has grouped payments together in batches that are then paid in intervals, rather than at the moment of payment. ACH was used to make 30 billion payments in 2022, trumping RTP’s 1.8 billion transactions, as well as Fedwire’s 196 million transfers.

The lack of a federal solution to slow payments has spurred the development of apps like Zelle – a P2P payments service developed by several US banks and run on the RTP network. Many have speculated that FedNow is a response to the success of these private challengers, which have disrupted the payments status quo in America.

“People and businesses were fine with cash and cheques, and even PayPal didn’t really move the needle,” says Mark Hewlett, Chief Operating Officer at business FX provider Universal Partners. “It’s only when Zelle and Venmo came along that the Fed saw a need to accelerate the rollout.”

James Simcox, CPO of Equals Money, says that FedNow could be a manoeuvre to create a more level playing field for banks, as well as a way for the Fed to combat fraudulent transactions via private apps – a growing concern in the US.

Having said this, asking banks to move from their current legacy systems takes time, and FedNow will be optional for banks to join at the start. However, leaving banks to make the decision themselves has led to slow uptake in Europe. For this reason, the EU Commission recently proposed new legislation that is set to make instant payments in euros mandatory for banks across the European Union and European Economic Area.

Mandating US banks to adopt instant payments in a similar way could be a big challenge. “The US financial system is vast – covering 50 states, and complex,” says Marcus Treacher, Executive Chairman of cross-border liquidity network RTGS.global. “This complexity, combined with a unique blend of public and private sector involvement, requires careful planning for systemic changes.”

Nick Botha, Global Payments Sales Manager at fintech AutoRek, argues that US regulators may have wanted to observe the rollout of instant payments in other markets before introducing their own system. He adds that the fundamental barrier to early adoption in the US was the American financial services’ industry being “one of the most crowded and competitive markets across the global economy”.

“Developing and implementing an instant, nationwide payments system would require collaboration from a variety of stakeholders: banks, payment service providers, financial institutions and technology providers,” he says.

The potential impact of FedNow

According to the Fed, banks and payment companies will be able to use FedNow to support a variety of payment use cases, spanning A2A, B2B, B2C and C2B payments, as well as payments to and from governmental and financial institutions.

One of Fednow’s biggest benefits (should it be adopted en masse) is 24/7 settlement. Bank customers will no longer need to wait all weekend for their salary pay-out to clear. Meanwhile, businesses can receive cash for services faster, which they can then reinvest into their operations.

Dimitri Rodrigues, CTO of cross-border payment platform iBanFirst, explains that the new system would help speed up transactions for consumers so that they ultimately receive their goods faster, while merchants can reduce the time that stock spends in transit.

“Institutions and regulators will benefit due to an increased digitalisation of payments, leading to a more transparent level of financial oversight and greater consumer protection,” Rodrigues adds.

Treacher says that FedNow will offer new ways of managing liquidity to banks, helping them reduce costs and provide a greater range of services to customers. “Furthermore, instant payments can make it easier to comply with increasingly stringent regulatory requirements, and potentially open up opportunities for innovative financial products and services,” he adds.

Introducing instant payments to the US on a wider scale will take time, but its adoption could eventually lead to a change in the US consumer mindset. Simcox notes how instant payments in the UK led to a sharp rise in direct and debit payments, and a rapid decline in cheque usage.

This could also be the outcome in the US, though he believes card use will continue to increase in the country – particularly given the US’s obsession with card-to-card transfers. Mastercard Send and Visa Direct are both effectively forms of real-time payment, except instead of paying out to bank accounts, money is transferred directly to a users’ card.

“Cards are already the expected payment option across the world, so instant payments only furthers their benefits over other methods,” says Simcox.

Reduced cheque usage could lead to other fundamental changes to the American payment system. In BNY Mellon’s Q1 2023 earnings call, CEO Robin Vince spoke about how FedNow could help reduce the industry’s overall carbon footprint, as it may eliminate the need for a carbon-intensive KYC process associated with cheques.

The difference between FedNow and the RTP network

While FedNow is operated by one central bank, RTP is run by a consortium of banks (The Clearing House), which has said that it will work with the Federal Reserve towards interoperability of the two systems.

Both FedNow and RTP have the same outcome of clearing and settling payments in real-time but they have some key differences in process. FedNow will launch with a maximum limit for transactions of $500,000, while RTP’s max limit is $1m, which means banks looking to make larger payments will need to continue using the Fedwire system.

Crucially, RTP is a privately run system, owned and operated by The Clearing House, while FedNow is a federal system that is much more accessible to banks of all sizes across the US.

“The benefits of these schemes is that the terms for all participants are the same and the scheme costs are borne by the participants the same, usually through the flow of payments,” says Equals’ James Simcox.

According to The Clearing House, RTP currently reaches 65% of US bank accounts, with nearly 300 banking participants across the US. However, not all banks use the RTP network for both sending and receiving payments. Given that there are thousands of US banks, there is still some way to go for RTP when it comes to adoption.

Many of the banks that are adopting or have participated in the pilot for FedNow have previously been users of the RTP network, including BNY Mellon, Citi, Citizens Bank, JP Morgan Chase, Wells Fargo and many other regional banks.

BNY Mellon CEO Robin Vince also said in the Q1 2023 earnings call that the bank sees FedNow as being part of its existing real-time payments offering going forward, which includes other services like payment validation.

Comparing the US’s real-time payment systems to other countries

Though it has been in the space for several years, the US has still been behind other countries when it comes to implementing real-time payment systems, as shown in the graphic below.

While some systems have max limits for transfers, others ask participating financial institutions to set their own limits. Some systems are run by private banking associations, while others are developed and run by central banks, showing that it’s not just the US that has seen a public versus private divide in this space.

Some real-time payment systems are now being linked with systems in other countries to enable instant cross-border payments, particularly in Asian markets that are attempting to reduce the use of the US dollar in currency exchange. For example, a recent link between Singapore’s FAST and India’s UPI systems enables instant transfers from a PayNow user in Singapore to a UPI user in India, with senders simply having to input the recipient’s mobile number.

There’s also the Bank for International Settlement’s Project Nexus, which aims to connect Europe’s TARGET Instant Payment Settlement (TIPS), Malaysia’s Real-time Retail Payments Platform and Singapore’s FAST. SWIFT, the Clearing House and EBA Clearing are also in the process of testing a system that will enable immediate cross-border payments from Europe to the US.

“We’re seeing most instant payment innovations coming out of the Asian markets because they haven’t been wedded to credit cards for the last 50 years, which affects that consumer journey,” says Simcox.

Will FedNow go cross-border?

Like most other real-time payment systems, FedNow is launching as a purely domestic service. Experts agree that the system needs to gain traction locally before it can be linked in with other payment schemes.

“There’s a number of direct central bank discussions taking place to link schemes (plus discussions facilitated by SWIFT and others) to improve cross-border interoperability, but we’re not expecting the Fed to be at the forefront in the participation of these for a number of years,” says Hewlett.

Treacher says that FedNow will offer opportunities to improve cross-border payments because of the prominent role that US dollars still play in these payments worldwide. However, he agrees interoperability with other systems will be the main challenge. “FedNow will need to achieve this to harness its full potential,” he adds.

AutoRek’s Nick Botha argues that only once the market has shown it is confident in FedNow can global regulators come together to understand what cross-border rails look like. Even then, enabling instant cross-border payments comes with unique challenges.

“Areas like data management and regulatory reporting across different jurisdictions need to be worked out in advance, as well as how to contend with regulations imposed by multiple economies,” says Botha. “Such factors are not impossible to overcome, though, and the potential for FedNow to facilitate seamless cross-border activity remains realistic. But it will require global participation to ensure its success.”

Similarly, Rodrigues says that authorities and clearing houses worldwide are likely to push the concept of FedNow being integrated in cross-border payments, but that it “will require considerable coordination and effort to ensure that the system is interconnected and fully compatible with various local instant payment capabilities”.

FedNow’s impact on cross-border payment companies

Having said that, FedNow could still be beneficial for private fintechs that specialise in delivering faster, more efficient cross-border payments. For these companies, being able to collect money into their accounts faster via local real-time payment rails helps speed up the delivery process for customers.

Jody Perla, Payoneer’s Managing Director for Global Payments and Banking Infrastructure, says she doesn’t see FedNow being “truly cross-border” in any form that’s dramatically different from what cross-border messaging platform SWIFT does today. “The play really is for these fintechs and other platforms that connect the dots to the last mile delivery around the world,” she says. “That’s really where the value is going to be unlocked.”

Having said this, Perla adds that Payoneer has customers all over the world who collect money locally in the US, but both the sending bank and the receiver need to have FedNow integrated for the company to see the benefits. What’s more, banks that have the capabilities to connect with FedNow and accept instant payments may not make those payment types available with every use case, such as significantly larger B2B money transfers.

“FedNow hasn’t come out with their rules about money service businesses, or correspondent banks and all these other things,” Perla says. “We need all the banks to support it for all the use cases.”

Perla believes that, just like RTP, peer-to-peer payment applications will benefit the most from FedNow initially, but for business payments (Payoneer’s focus), wider adoption, an expanded transaction limit and richer amounts of data will be important for the company to truly benefit from the new system.

For Payoneer, which regularly handles transactions over FedNow’s current maximum transaction limit, the goal will be to watch and see how FedNow is implemented before the company actively seeks to participate in it.

Next steps for FedNow

The US could drive FedNow adoption in two major ways: reducing pricing to encourage competition with other systems such as RTP or taking more significant policy measures to push banks to join.

As well as encouraging adoption amongst financial institutions, there is also the question around how RTP and FedNow will work together. Banks and payments providers that have already invested in RTP may choose to also join FedNow to widen the net of financial institutions they can send to, but maintaining both systems could be more costly for payment service providers.

For now, FedNow has the potential to support faster cross-border payments by speeding up the local movement of money in the US. However, even for this purpose, the majority of banks need to be on board first. When it comes to FedNow’s cross-border potential, there is evidently still a long road ahead.

“The necessity of ensuring safety, security and regulatory compliance in an economy as large and influential as the US’s can contribute to a more extended timeline,” says Treacher. “But as the saying goes, ‘better late than never’. And when America steps into the game, it tends to do so with impact.”