In the latest in our Post-Earnings call series, we spoke to CEO Skander Malcolm about the company’s record-breaking FY 23 results and how its recent acquisitions (including Firma, TreasurUp and new addition Paytron) will continue to drive growth.

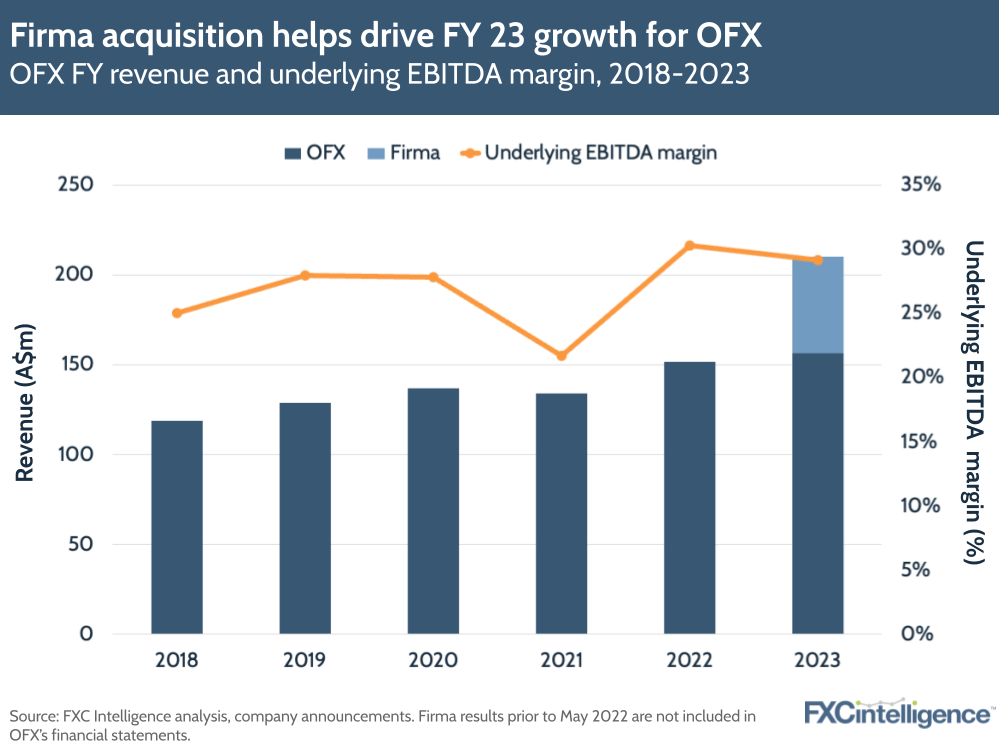

Australian money transfer provider OFX saw its share price rise on the back of strong results for fiscal year 2023. Net operating income increased by 45.6% YoY to A$214.1m, while underlying EBITDA climbed 40.3% to A$62.4m, driven by OFX’s integration of Canadian corporate FX player Firma (acquired last year).

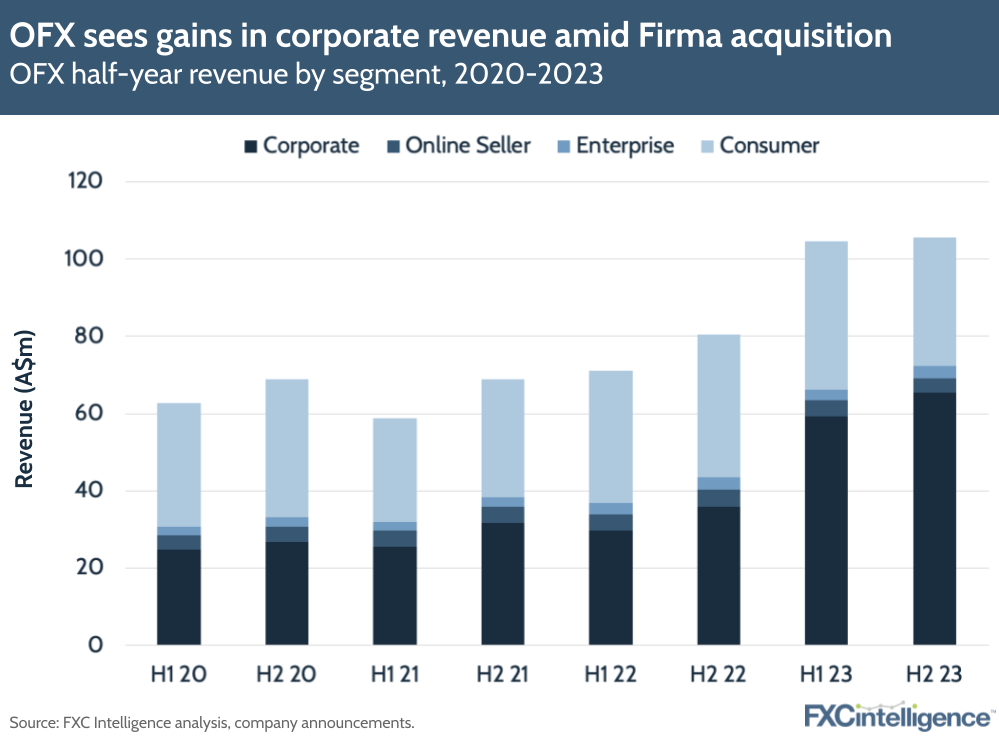

OFX’s total revenue grew by 38.6% to A$210.3m, with recently acquired Firma accounting for A$53.7m (25.5%). Organically (i.e. excluding Firma), OFX’s revenue for the year increased by 3.2%. Firma helped drive OFX’s B2B segment, which covers corporate payments as well as online sellers and enterprises. Corporate, which makes up around 90% of OFX’s B2B revenue, grew almost 90% YoY to A$124.6m (growth was 11.1% excluding Firma), while online seller revenues fell by 6.9%.

OFX also announced it will be acquiring B2B payments provider Paytron, with the sale expected to close in July. The company hopes the acquisition will increase the value from B2B clients beyond spot payments (currently 90% of the business), while also providing new revenue streams and increasing transaction processing, among other benefits.

Consumer growth was more muted at 0.3%, to A$71.6m, with an uncertain economic backdrop leading to a drop in high-value transfers (e.g. for property). As the company has pivoted to B2B, its number of active consumer clients has gone down, but the company has seen growth in consumer transaction sizes and margins.

Looking to 2024, the company projects a net operating income of between A$225m-243m and underlying EBITDA of between A$63m and A$74m. To break down the company’s results and future growth strategies, we spoke to OFX Managing Director and CEO Skander Malcolm.

How OFX’s strategy is evolving

Daniel Webber:

How is your strategy evolving now that Firma is settled in and a new acquisition has been announced?

Skander Malcolm:

The strategy that we’ve been sharing with the market for the last four or five years has been focusing on four segments, three of which are B2B and one of which is B2C. We’re making sure that we’re clear about how we can improve the client experience and operate in geographies where we see a lot of headroom to grow, but particularly the focus is on B2B. As part of driving that client experience in B2B, we’re making a more concerted effort to drive revenue beyond spot transactions.

You saw the investment in TreasurUp, which was [to facilitate a] product and features capability around risk management. Then you saw the acquisition of Firma, which was B2B and North America, and now you’ve seen the acquisition of Paytron, which is client experience at B2B. That’s what our investors are particularly interested in, that’s where they see strong long-term returns, and that’s absolutely where the team is focused around growing value from that segment.

OFX’s positioning in the B2B space

Daniel Webber:

Given B2B is a very large, fragmented space, how do you see yourselves positioning in a medium to long term?

Skander Malcolm:

We’re very focused on what we would call a flow business within B2B (moving and protecting money). We are less interested in what we would call a balance sheet side or banking side of B2B.

We want to help clients move money more quickly and more safely, as well as give them enhanced integrations to software platforms and everything else that makes the movement of money easier and safer. We’re typically targeting small, mid-size corporates and investing in things like payments engines, better reporting, risk products and faster payments – things that allow SMEs to do the job much more simply.

We focus on those areas because members of the management team have a lot of experience in lending and leasing, so we understand what’s required, but we haven’t built a team that had those capabilities, so to go onto that side of serving B2B needs would not be a good use of the talent that we have.

The second reason [for this focus] is that we’ve spent a long time investing in technology teams, risk and compliance frameworks, and skills and capabilities to create credibility with those types of clients, as well as with our banking partners, to take on more scale. Those are the reasons why we’re really pushing deeper and deeper into the B2B payment space.

How OFX is competing on consumer transfers

Daniel Webber:

Where do you position yourself in the consumer market, and how are you competing with others (e.g. low-cost providers) in this space?

Skander Malcolm:

We do like the consumer segment that we focus on, and they typically use us for higher value transactions. The average transaction values (ATVs) that we typically work with are somewhere around A$21,000. The main competitors are at around A$2,000 or less, so they are very different business models. To make our business model work, we deploy technology so that clients can access the information they need and put in place limit orders or forward contracts if they want to.

But what they love is a combination of that technology, a very competitive price and the ability to talk to someone. When they are larger value transactions, you’d be surprised that even sophisticated individuals want to talk to someone, just to make sure that it’s the best time to do a transaction that they might only do once or twice a year or even less. They love that when they talk to our people, they get an authentic, straightforward person who can help walk them through it. It’s easy to use, it happens quickly and can satisfy their need at that time.

Frankly, that [consumer] business is really valuable to OFX. We’ve got terrific equity in it and we’ll keep playing in that space because clients want us to, and there are things that we could do to grow it, but in a true investor sense, we have to take what capital we have and put it against the best opportunity, which is really B2B.

OFX’s acquisition goals in FY 24

Daniel Webber:

What are you focusing on for the next year? Are there particular types of acquisitions you’re going to be still thinking about?

Skander Malcolm:

In terms of what we have on our to-do list, number one is completing our Firma integration. We are going region by region. The Australian region is now live on the OFX platform and it’s operating well. It’s a really good technical integration there as well as the staff and all of the clients in the service delivery. Next will be the UK, then New Zealand and then Canada. We’ve done a lot of the integration from a people and accounting perspective already. Many of those things have already been completed, but now the systems integration and the client migration is top of our list and we want to execute that through our fiscal year 2024.

We’re also very focused now on the Paytron acquisition. That’s a terrific team. They’ve built a nice platform that’s focused on B2B client experience. We’re going to be working with that team on an integration strategy and then we’ll telemarket on timing, but more or less in the first year they’ll be continuing to drive their client experience, uplifting their product and platform to be able to offer it to our Australian clients within a year. Then we’ll take it to the other regions and we’ve already got some plans in place, but we’ll spend a bit of time making more detailed plans in the next 60 days.

Apart from that, we’ve got a very detailed product roadmap across all our segments, so we’ll be continuing to execute on that. The obvious thing to say is that we’re seeing good traction in our corporate portfolio. We’ve said in our outlook that we would expect to grow that somewhere between 10% and 15%, notwithstanding some economic conditions. Clearly, the focus for us is to continue to support those clients and drive good economic outcomes from that segment.

Daniel Webber:

Anything else?

Skander Malcolm:

It’s obviously a particularly unusual set of circumstances right now externally, so it’s terrific to see that the team that we’ve built is operating superbly. The engagement scores are up and that helps me sleep well at night. We have a great team in place at the moment.

Daniel Webber:

Skander, thank you very much.

Skander Malcolm:

Thanks.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.