Remitly’s revenue growth continued to outpace the wider money transfer market in Q3. In the latest in our post-earnings call series, we speak to CEO Matt Oppenheimer about how the company’s data-led marketing strategy is driving revenues for the money transfer player.

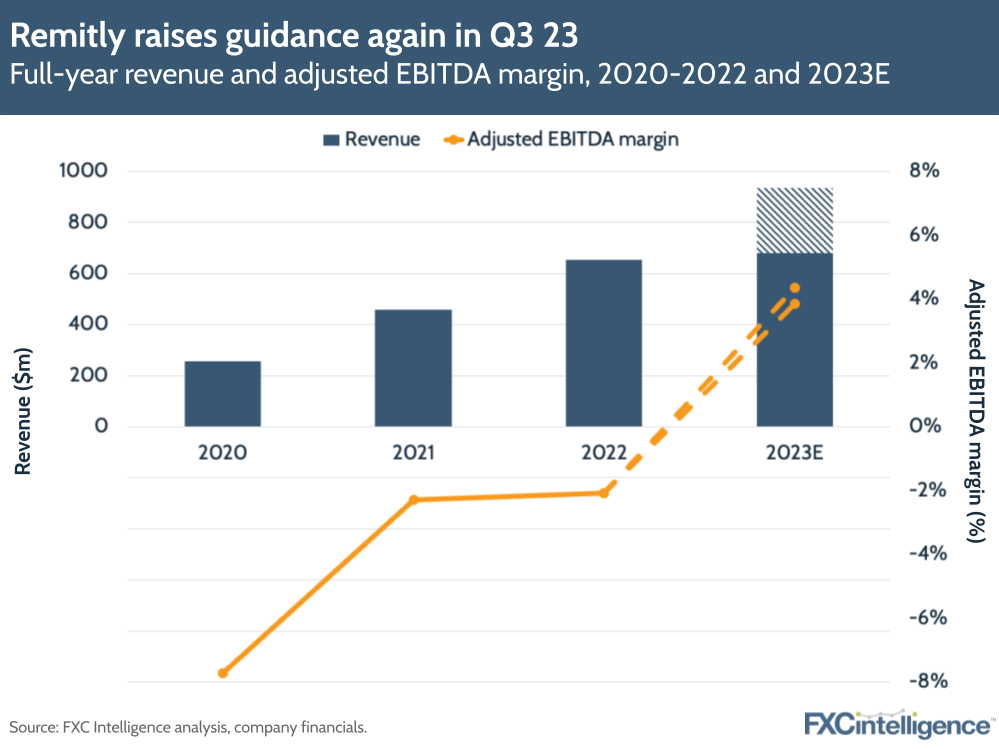

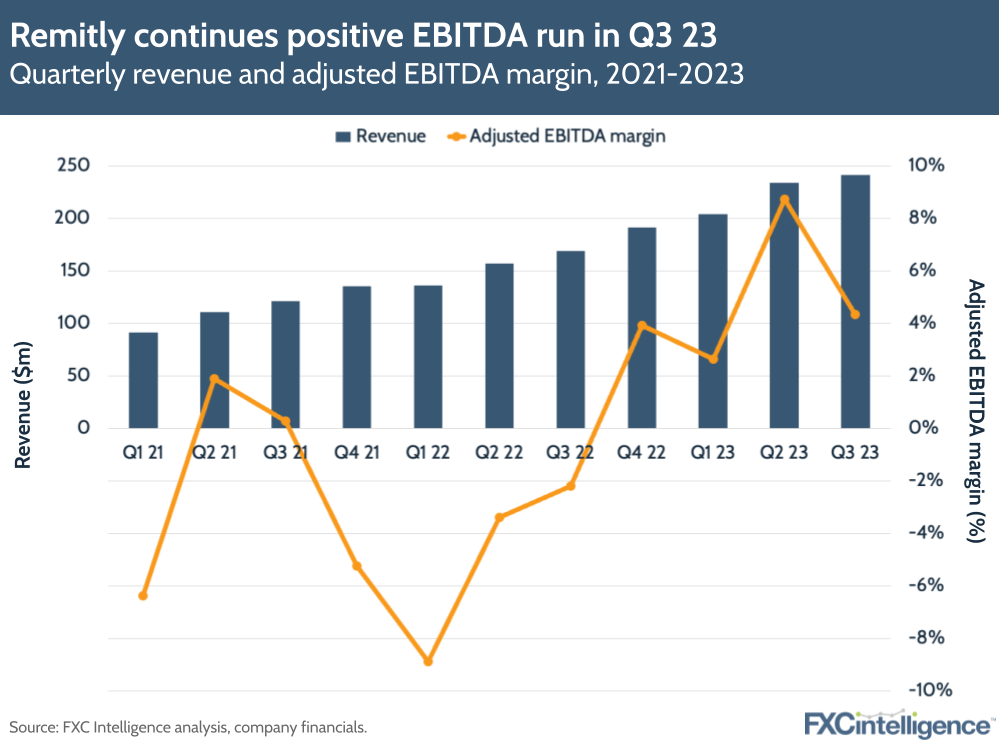

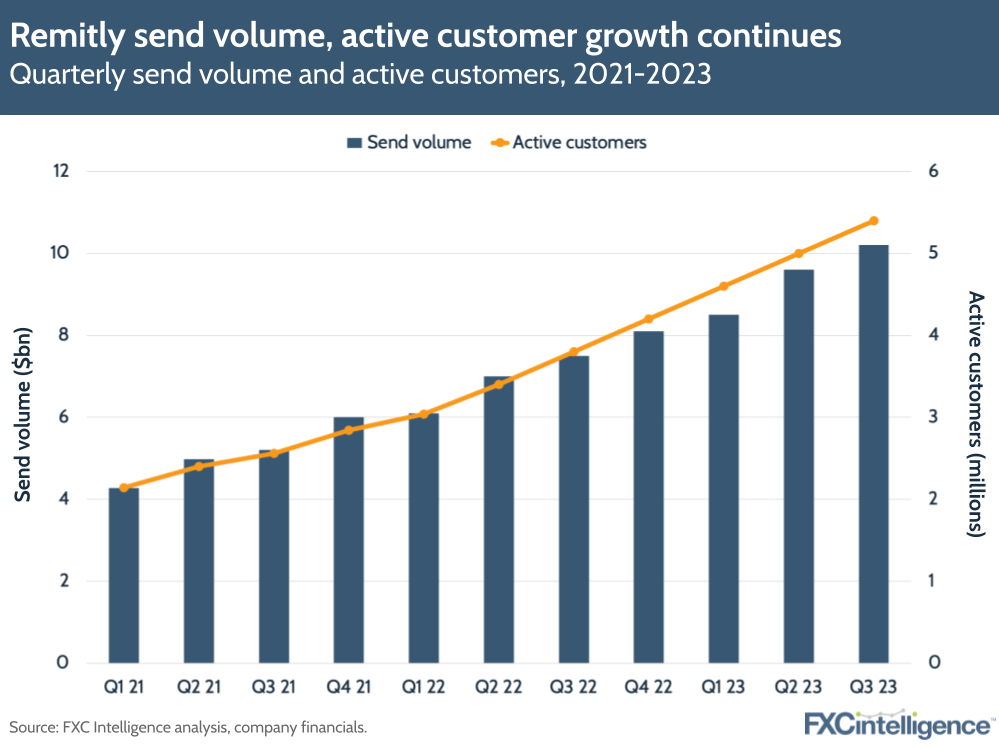

Digital remittances player Remitly reported a 43% rise in revenues to $241.6m in Q3 2023. Adjusted EBITDA was once again positive at $10.5m, compared to -$3.7m last year, and the company has once again seen revenues driven by growth in active customer numbers, digital transactions and diversification as it expands and ramps up its marketing efforts.

Active customers were up 42% to 5.4 million, pushing send volumes up 36% to $10.2bn. Referrals and integrated marketing campaigns are driving new customer acquisition but also costs, with the company making a slightly higher net loss this year at $35.7m – compared to $33.1m in Q3 2022.

There were also some key partnership updates during the quarter, including a tie-up with Mastercard to integrate Send and Cross-Border Services as well as a renewed Visa Direct deal. These partnerships are growing Remitly’s payout options, which currently span four billion bank accounts, 460,000 cash pickup locations, 1.2 billion mobile wallets and door-to-door delivery in some areas.

For 2023, the company now expects 43-44% revenue growth of $935m to $943m (up from the previous outlook of $915m-925m), as well as an adjusted EBITDA of $36m to $41m (up from $33m-40m). We spoke to Remitly Co-Founder and CEO Matt Oppenheimer to find out more about how the company is driving revenue through its customer acquisition strategy.

Remitly’s revenue and customer growth drivers in Q3 2023

Daniel Webber:

What were the key drivers for Remitly’s growth in Q3?

Matt Oppenheimer:

Ultimately, it is the grit, the tenacity and the non-discretionary need of remittances. Sometimes it can be countercyclical, but that is foundational. In today’s world, most businesses and most customers are not like that. So that’s one.

Secondly, we’re getting the return on some of the investments that we’re making around new customer acquisition, geographic expansion and creating a frictionless remittance experience and complementary new product. Those investments, combined with the fact that there is this macro shift to digital remittances and we’re still only 2% of the overall market, means that we’re continuing to grow and deliver nice results.

Why Remitly is growing faster than other money transfer players

Daniel Webber:

What do you think is helping you grow at a rate that is much faster than the overall remittance market?

Matt Oppenheimer:

There are two elements to answer your question. One is, if you look at what our customers care about, it’s trust. I used to think it was about speed and price, and those things do matter. But think about our customer base, who are providing their name, address, tax ID and then a big chunk of their hard-earned money. That takes a huge leap of trust, especially in a digital world.

Then you look at the difficulty of delivering remittances reliably. Maybe your fraud systems are not finely tuned enough with things like machine learning, meaning that you cast the net too wide and in an effort to prevent fraud loss or bad actors from a compliance standpoint, you put really good customers through a bad process. That applies to the disbursement network, payment acceptance, FX, treasury, cash management – all of those things mean that most remittance companies out there are not as reliable as they should be with a customer base where trust is paramount.

That is where we’re differentiating. If you look at the scale that we have now, we have more data to feed into our machine learning models. We have a better machine learning team on the risk side. We have a high-quality, culturally aligned team, with partners across the globe.

They’re doing direct integrations to be able to do things like account number validation, where our customer is entering in their recipient’s bank account and routing number, and we can validate that before the transaction’s actually submitted. Or, if that bank goes down, we can reroute the transaction because we’ve got multiple different routes to the end destination.

The punchline is, trust is paramount. Delivering a reliable experience is incredibly hard and the way to solve that is having scale and a digital-first approach, because you start getting this flywheel that is really spinning now and adding a lot of value to customers. And then, with those customers, we’re building a word of mouth and brand that is starting to really accelerate.

Daniel Webber:

Is this why your pricing has been relatively stable? Because people will pay for a financial service they trust?

Matt Oppenheimer:

Since we’ve shared public data until today, our take rate has always been between the 2-2.5% range. So we take a bunch of costs out of the system compared to a legacy player, which is great, but once you’re in that kind of new equilibrium that I call it, customers care about a reliable experience first and foremost, and that’s something we’re proud to deliver.

Remitly’s marketing strategy

Daniel Webber:

How is Remitly approaching marketing?

Matt Oppenheimer:

We think about marketing from a unit economic lens first: What’s the customer acquisition cost? What’s the lifetime value? We’ve shared in the past that there is a five-year value to the customer acquisition cost that we pay. I caveat it at five years, because if you actually look at our cohorts, most are well beyond five years, but we use five years as an industry standard. That’s the foundation.

Then the way that we execute it is much more sophisticated than a lot of the competition. It’s focused on the middle to bottom of the funnel, which means things like performance marketing, and we can measure that not only on an aggregate basis, but broken out by marketing channel, geography or corridor.

There’s a lot of precision so that we can optimise the customer acquisition cost we’re willing to pay with the corresponding lifetime value. As we’ve found ways to expand, this happens naturally. There’s a lot of referrals and word of mouth, given that we had 5.4 million quarterly active customers last quarter, and that’s growing quickly. You get this word of mouth with that reliable, trusted service, and huge negative word of mouth if you don’t do that, which I think some of our competitors face.

We’re going to continue to do some integrated brand campaigns. An example of that could be very focused in the City of Miami, in things like public transit in the neighborhood where our customers live. The airport in Miami serves a lot of Latin American countries where our customers are travelling to and from. We’ve done that in a variety of cities and we’re excited to continue to make those investments because what you see is still measurable.

When people talk about integrated marketing campaigns or top of the funnel, they think it’s not measurable because a lot of companies do not measure it. For us, you can geofence the impact and you can see it pretty quickly with things like more efficient performance marketing, but then it also has a longer tail because you’re building that brand to where, when you meet the customer at the point of purchase, you see a more efficient conversion.

Lifetime value versus customer acquisition costs

Daniel Webber:

How are you thinking about the amount of money you are spending on marketing as you scale?

Matt Oppenheimer:

It’s important to recognise first that the vast majority of our marketing spend is going towards new customer acquisition. The second component is that we have a lot of metrics to measure the performance not only on the average customer acquisition cost (CAC), but also the marginal CAC, the marginal customer lifetime value (LTV) and the marginal payback. You see stability on the LTV side, so CAC is where you can vary that. As long as there’s a lot of metrics and measurement around that, and control around that, then I think it is a very high return on investment and you see it in the overall growth of the business.

What’s exciting is the marketing we’re spending in Q4 will have a payback. We’ve shared in the past that our payback is less than 12 months, so you will see that return quickly. Whether you are looking at internal rate of return, LTV to CAC, or net present value with an increased cost of capital, what you still see is favourable returns from a profit standpoint when it comes to our marketing spend, and we’re excited about continuing to deliver those great returns to our customers and to our shareholders.

The impact of promotional rates

Daniel Webber:

Do you count promotional rates (i.e. cheaper initial rates for customers) within your marketing spend?

Matt Oppenheimer:

That is definitely included in our marketing expense. A question I sometimes get asked is this: it’s great to know the lifetime value of a customer on a precise level (i.e. marketing channel, corridor), but how do you operationalise that? How do you actually pay the right amount from a customer acquisition cost with lifetime value?

We vary the promotion we’re willing to give that customer with the lifetime value that we expect, based on the data that we have and the segment of customer that we’re actually reaching. And so there’s a lot of science that goes into that, and it’s been key to our success.

Daniel Webber:

Anything else you would like to add?

Matt Oppenheimer:

The investments that we’re making outside of marketing are also showing a return, both in terms of our customer retention because of the frictionless product that we’re building, but also customer support as a percentage of revenue improved 230 basis points year-on-year. That’s a signal that there is less friction in our project.

We’re just getting started there because we still have a huge amount of opportunity to drive down friction, improving costs for us as a business. We’re excited about what that holds for the future as well.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.