After numerous delays, Swift began the migration of its system onto the new ISO 20022 standard on 20 March 2023. Here’s what happened, what it means for cross-border payments and an update on how financial institutions are adapting to the change.

March 2023 was a transitional month for banks, as Swift finally began the migration of its cross-border payments system onto ISO 20022 – the global standard that aims to standardise how payment messages are sent worldwide.

Under ISO 20022, financial institutions are changing the payment messages they send and receive via Swift from the legacy MT (message type) format to the new MX (message type XML) format, which is more transparent, holds more data and is expected to boost interoperability between banks.

In a nutshell: if banks are all sending messages that are structured in line with Swift’s cross-border payments and reporting (CBPR+) guidelines, the communications behind these payments will be more efficient, more transparent and ultimately lower costs.

In this piece, we explore everything payments professionals need to know about ISO 20022, including what it is, the challenges involved and what this transition might mean for cross-border payments. We also find out how many financial institutions are now sending and receiving ISO 20022-compliant messages via Swift, and explore how this has changed since last year.

Note: This article was updated in June 2025 with additional information to provide further context on how financial institutions are faring with ISO 20022 adoption. It was originally published in February 2023, using comments provided by experts from Lloyds, HSBC and Deutsche Bank in late 2022.

What is ISO 20022?

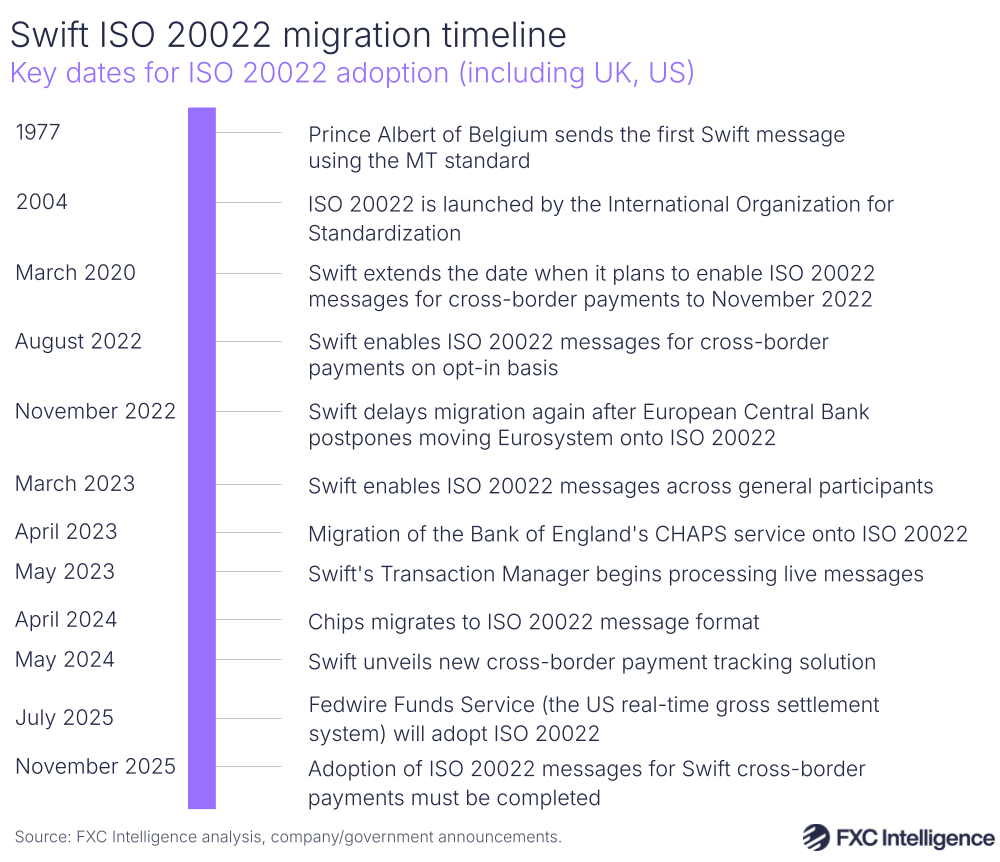

ISO 20022 is a global standard for financial messaging systems worldwide. First introduced in 2004 by the International Organization for Standardization (ISO), it has now been adopted by more than 70 countries across their payment systems. Financial institutions will replace existing payment messages (a mainstay of the former ISO 15022 standard) with new ISO 20022-compliant MX messages across payment schemes, open banking, APIs and more.

For cross-border payments, it has been touted as having some very specific benefits, namely improving security, enabling deeper analysis of payments and making them faster and less costly. The Swift migration onto the ISO 20022 is one of many major ongoing payments projects worldwide that have been launched since the start of 2023.

Why is Swift only adopting the standard now?

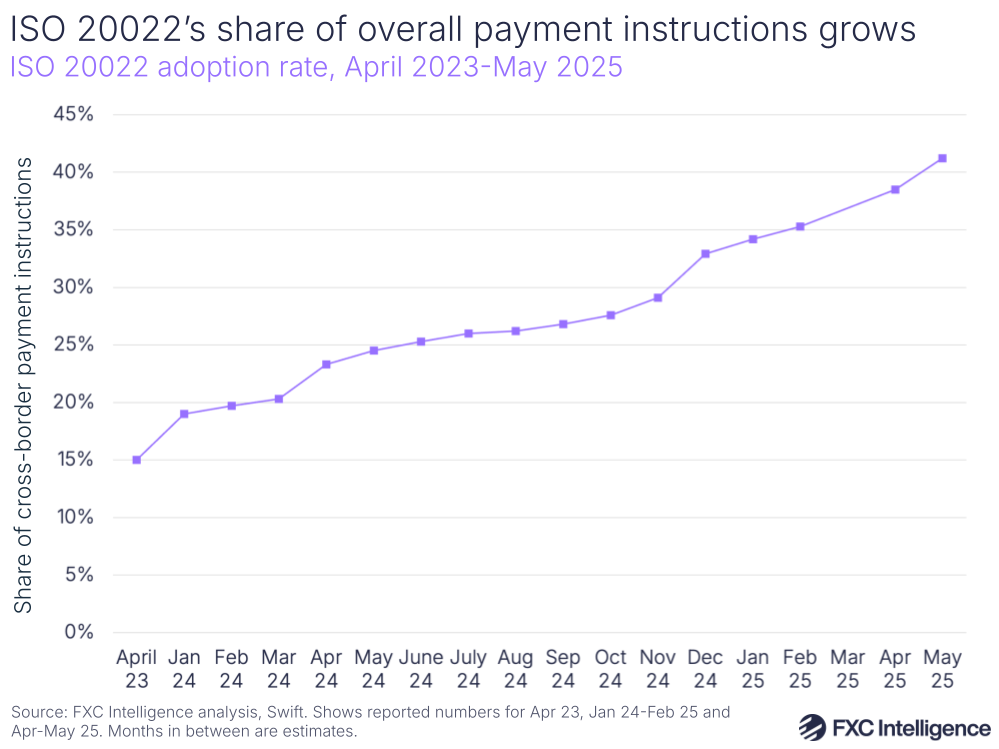

Since 2004, many banks have already adopted ISO 20022 for financial messaging across their high-value payments systems worldwide. In 2020, Swift claimed that by 2025, 80% of high-value transactions would be cleared and settled using the new standard; however, as we explore in more detail further on, the share of cross-border payment instructions being sent using ISO 20022-compliant messages hit just 41.2% in May 2025.

The difficulty of updating legacy systems has meant that some banks have moved faster with their adoption than others. Banks still using older systems aren’t set up to receive the high-data MX messages, which can result in data being truncated. If payment origin information is lost, that could end up delaying cross-border payments or leading to additional manual checks.

Financial institutions on the Swift network therefore requested the organisation to encourage ISO 20022 adoption by migrating its own messaging service onto the new system. Swift’s migration onto the standard will specifically affect organisations that currently send or receive Swift MT messages to make cross-border payments.

When will ISO 20022 go live?

From August 2022, Swift began enabling ISO 20022 messages for cross-border payments businesses starting on an ‘opt-in’ basis. In March 2023, migration began more widely across Swift’s participants. This means that, from March 2023, financial institutions sending and receiving messages through Swift needed to have updated their systems so they can at least receive MX payment messages, or translate MX into MT during the transition period, which lasts until November 2025.

Until November 2025, banks will still be able to send messages on the existing MT standard. From November 2025 onwards, all banks will need to be able to send and receive MX messages using Swift.

The migration in March 2023 coincided with another key event for banks in Europe. Monetary authority Eurosystem replaced its existing TARGET2 real-time gross settlement system (RTGS) with a new RTGS called T2, which is using the new ISO standard to make European payments more secure and efficient.

Why are MT messages being replaced with MX messages?

First introduced by Swift in 1977, the MT messaging standard has since become the dominant standard for payment messages worldwide. But over 40 years later, the world of payments looks very different.

Financial regulations have become more stringent, requiring all payment instructions to be screened against a sanctions list. In addition, businesses can now use technology to gleam more valuable insights about where payments are coming from and being sent.

In response to these changes, MX messages offer more transparency overall. The standard MT103 message used for cross-border transfers is made up of a variety of fields, defined by a number. Experts who have been using legacy banking systems for years might be able to easily understand these tags, but for newcomers it can be like trying to decipher an alien language.

“If I say to you what goes in Field 50 of an MT103, most human beings won’t have a clue what that means,” says Nick Mellish, Head of Design and Payments Scheme Compliance for Next Gen International and High Value Payments at Lloyds Banking Group. “On the other hand, if I ask you what goes in the originator name field, it’s pretty obvious that it’s the name of the person that originated the payment.”

Swift wants to phase out MT messages for cross-border payments and replace it with MX messages, which are based on the XML coding language. These messages contain more data, are more structured and are easier to read. They are also able to support non-Latin alphabets, which has become increasingly important given high cross-border payments activity across Asia.

What have financial institutions been doing to prepare for ISO 20022?

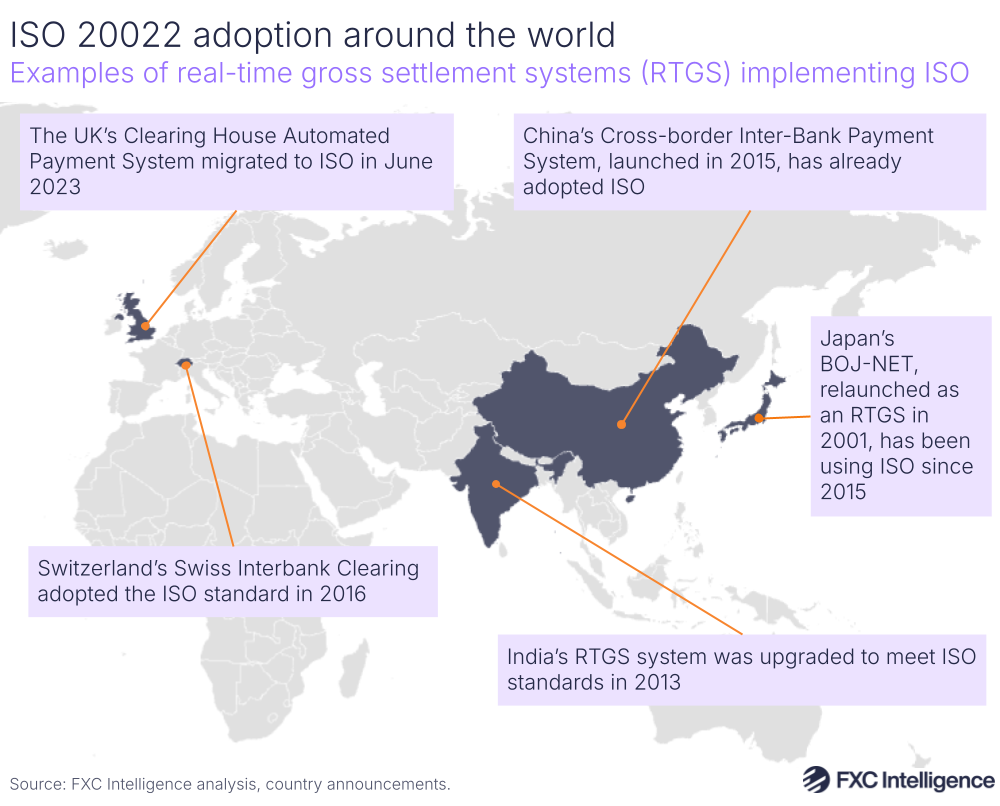

Banks and payment schemes worldwide have already been adopting ISO 20022-compliant messages, with some of the biggest examples including SIC in Switzerland; SEPA credit transfers and direct debits in Europe; and the FedNow scheme in the US.

For the Swift migration, banks have been upgrading their messaging interfaces so they can receive MX messages, which means ensuring that tags and fields in the new ISO format are understood by their screening systems. They have also been configuring their connectivity to FINplus, the new and upgraded service operated by Swift over which banks exchange information. Finally (and most importantly) they have been testing to make sure everything works properly.

As many financial institutions were not immediately able to both send and receive MX messages over the period, they needed to be able to process both MT messages and MX messages. For many banks, this means having a system in place that enables MX messages to be translated into MT messages, and Swift and other third-party fintechs have been helping banks to implement these systems.

What are the benefits of ISO 20022 adoption for cross-border payments?

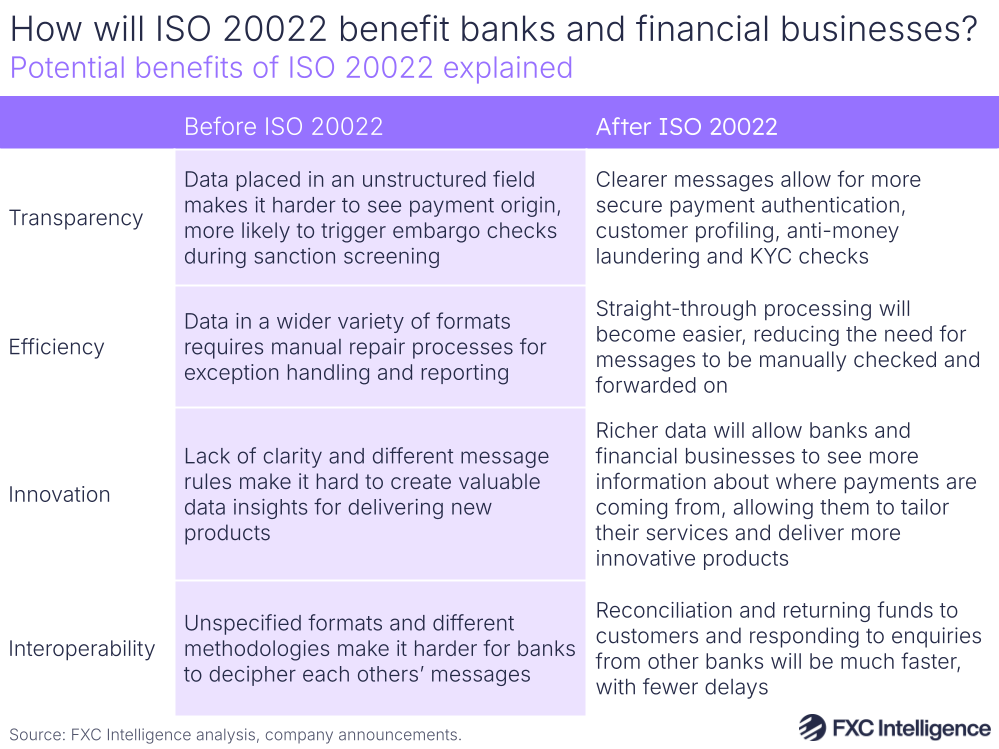

Advocates of ISO 20022 say that its benefits include better cost-effectiveness, along with greater interoperability, efficiency and security. For the most part, this boils down to one key benefit: transparency.

Take the example of Cuba Avenue in Staten Island, New York. When someone living on this particular street submits a payment, it always ends up going through manual processing, potentially delaying the payment. This happens because the word ‘Cuba’ is included in the unstructured field in the MT message, and this word ends up triggering an embargo check during a bank’s sanction screening process.

On the other hand, ISO 20022-compliant MX messages require users to populate more dedicated address information for debtors (initiating the payment) and creditors (receiving the payment), such as building numbers, street, city and specific data fields. This extra clarity makes compliance and anti-financial crime checks much faster, with fewer delays and manual repairs required.

“Adding the ultimate debtor/creditor fields will enable the industry to quickly determine where the payment has originated from and where its final destination is – something that isn’t as easy as you would expect today,” says Christopher Gardner, Programme Manager at Deutsche Bank.

Previously, two banks in different countries would have a much harder time getting to the root of a payment issue, as the data they would be referring to would be in an unspecified format. However, with the new MX messages, both banks are on the same page, looking at the same fields, with the same set-up, making things much easier. This ‘being on the same page’ delivers a number of key benefits that can streamline payments, reduce delays and make payments safer.

According to Mellish, ISO 20022 is unlikely to affect the FX costs of global payments for customers, but may reduce operational costs for banks to handle payments. He explains how, in the immediate wake of the Russian invasion, a large number of Russian names were added to Lloyds’ sanction filters, raising the number of hits significantly, because they were part of unstructured messages. If both banks were sending ISO-approved messages, these spikes are less likely to happen, as the recipient and sender information is clear for all to see.

“[ISO 20022] just simplifies the whole thing, and that’s what allows you to drive those efficiencies because you don’t have that fallout, you don’t have to go back to the customers and it progresses faster,” says Mellish. “That should reduce operational costs significantly, which should reduce our overall cost to provide payments.”

Corporate payments are often complicated by competing standards and proprietary formats, which makes it harder for global companies to track payments. To try and mitigate this, Swift announced in May 2024 that it was helping financial institutions to offer white-label payment tracking services to customers through an API.

Swift worked with a group of 25 banks and 20 businesses to standardise payment tracking data, making it easier for corporates to access and understand information about payments they send and receive. One of the businesses involved was global pharmaceutical company Roche, which has already implemented Swift’s new corporate API channel.

“It enables us to enhance and accelerate our payments analysis, giving us a comprehensive overview at pace,” Stefan Windisch, Global Head, InHouse Bank at Roche, said in a press release. “It will allow us to refine our instructions, better identify inefficiencies and minimise erosion of value in cross-border payments.”

At the time of the announcement, Swift also reported that 89% of payments on its network now reach the beneficiary bank within an hour, which is ahead of the G20’s target of 75% settling in the end account within an hour by 2027.

The challenges with ISO 20022 migration

Moving everything onto the new ISO 20022 system is no easy task. For years, MT messaging has been part of the fabric of banks’ messaging systems. Banks must not only restructure their entire messaging interface to ensure they are able to receive and send new messages, but also have solutions in place so that they can translate MX messages to MT.

Deutsche Bank’s Christopher Gardner led the bank’s preparations ahead of two major events: the Eurozone’s TARGET2 migrating to ISO 20022 in March 2023 and the Bank of England’s Clearing House Automated Payment System (CHAPS) migration in June 2023. The European Central Bank postponed its migration, originally set for November 2022, to allow for more user tests. Facing pressure from members to align with this date, Swift also delayed its ISO migration to March 2023.

“We’ve got a lot of challenges to deal with on our technology stacks with regards to legacy applications,” said Gardner in September 2022. “That’s not just us, but in the industry, where you’ve got a lot of legacy applications on end-of-life hardware, databases or code that do not lend themselves to such wholesale change.”

Vijay Lulla, Global Head of Currency Clearing at HSBC, says that banks should seize the opportunity to overhaul existing systems, instead of short-term solutions that will help them meet the guidelines but not actually benefit from opportunities from richer data. However, he adds that “this requires a substantial investment, which not many banks will be ready to invest in due to other conflicting priorities”.

At the core of the ISO offering is richer data, but Lulla says that the value of this data depends on whether banks’ corporate customers also make changes to the data they provide for making payments so that it contains more information on parties involved.

“Unless these changes are completed at source, the full benefits from structured and granular data will not materialise,” Lulla says.

Will banks/financial institutions adopt ISO 20022?

There is something of a ‘network effect’ surrounding ISO 20022. The real benefits from the scheme will only become apparent once banks have adopted the new scheme en masse, especially for cross-border payments, which rely on correspondent banking with several banks all in the chain.

While larger banks have been leading the charge, Gardner says that smaller banks may be slower to adopt the new schema, as the benefits might not yet be worth the investment.

“If you’re only doing 50 payments a day, the benefits of automation are not really going to matter to you,” he says. “If you’re doing 500 million payments a day, then automation is a big, big benefit. That’s where you have to weigh up the cost-benefit analysis.”

Banks such as J.P. Morgan, BNY and Lloyds have already made significant progress towards going live with ISO, with Swift also profiling the efforts of Barclays, the Bank of Cyprus, DBS Bank and Diamond Trust Bank. In April 2024, The Clearing House successfully completed its ISO 20022 implementation for CHIPS – a platform that clears and settles $1.8tn in domestic and global payments daily – having postponed its original migration date from November 2023.

As we’ve already seen, a number of banks and payment schemes have had to push back their efforts to join ISO. In June 2022, the US Federal Reserve announced that it would be delaying its implementation of ISO 20022 payment messaging by two years to March 2025 so that it can focus on FedNow. In February 2025, it pushed this date once again to 14 July 2025.

As mentioned earlier, timelines for migration are different across market infrastructures worldwide. That means banks could find themselves accepting MX messages from other banks across borders, only to have to translate them to less data-rich MT messages in their local markets, forcing them to truncate data. This, in turn, negates the benefits of ISO 20022.

Some countries aren’t expecting to go live with ISO 20022 across their domestic payments until 2026, so there will be a time period when they will only be receiving ISO MX from correspondent banks, but will have to translate these and any domestic payments into MT. A cross-border payment from a country that hasn’t updated its domestic payment system would then arrive with truncated data in its destination.

On a wider level, this means that the industry may not see the benefits of ISO 20022 until the vast majority of domestic payments markets go live under the standard.

How many institutions are sending ISO 20022 messages?

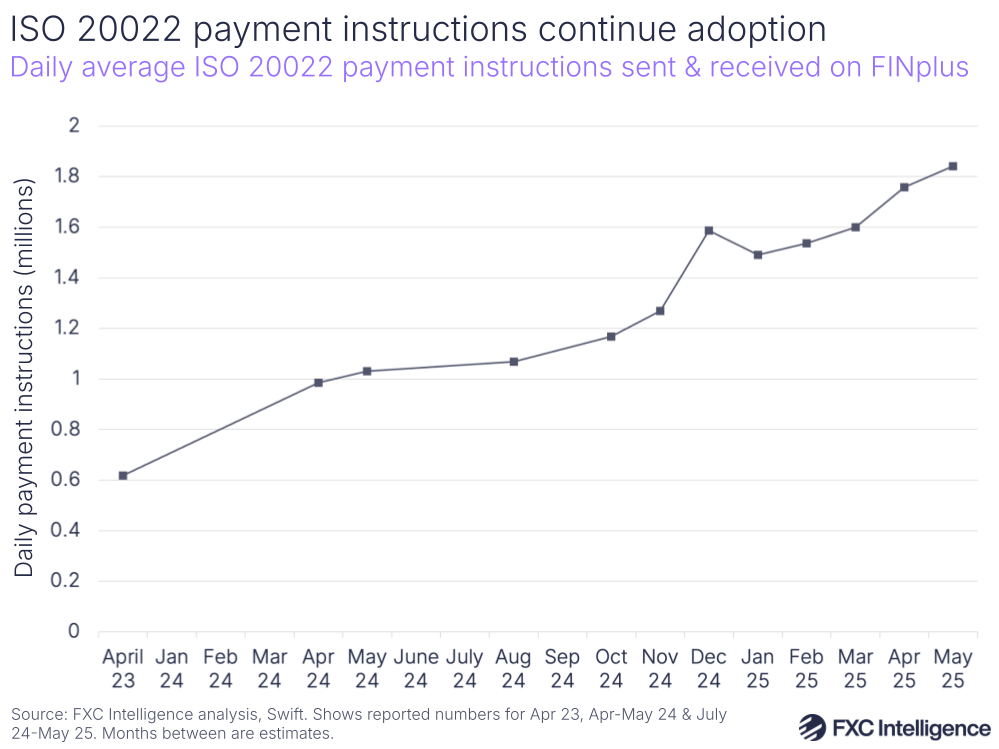

ISO-compliant traffic is growing on Swift’s platform. In May 2025, the number of daily average payment instructions being sent via the organisations’s FINplus service reached 1.8 million, up by 79% compared to May 2024 and three times as high as in April 2023 (the month after Swift went live with its brand new messaging format). Overall, the share of cross-border payment instructions being sent using ISO 20022 approved messages hit 41.2% in May.

Having said this, back in January, Swift forecast that ISO-compliant messages would account for 40% of traffic by the end of Q1 2025, 57% by the end of Q2, 74% by the end of Q3 and 86% by the November 2025 deadline. This spans payments activity for the top 175 originators using Swift’s platform, while the remaining 14% of messages in November spans smaller user activity, for which Swift has not provided a forecast.

The jump in adoption from May 2025 to June 2025 (from 41.2% to a projected 57%) would therefore need to be significant to stay aligned with Swift’s forecasts – as a point of comparison, adoption grew less than 3% between April and May – and the organisation could update these forecasts soon to reflect that adoption is taking longer than expected.

Swift also reports the number of 8-character Business Identifier Codes (BIC8s) being used to send and receive ISO 20022 messages on its platform. Each bank or financial institution is assigned its own BIC8.

The number of BIC8s sending international ISO 20022 messages on FINplus reached 2,300+ in May 2025, up from 1,180+ in May 2024, while the number of receiving BIC8s has grown from more than 5,740 to over 6,000. In addition, messages were sent from 180+ markets, up from 130+, while receiving countries grew slightly from over 210 to more than 220.

Swift claims to support more than 11,000 financial institutions worldwide, and while it’s unsurprising that the number of receivers is higher during the ongoing transition period, many banks still aren’t sending ISO 20022-compliant messages and pressure will continue to grow ahead of the November 2025 deadline.

Swift has also been launching new incentives to financial institutions making the transition, most recently a Data Quality Analytics tool that allows financial institutions to measure, analyse and optimise the data in ISO-compliant cross-border transactions. It has already shared numerous case studies in a bid to encourage more financial institutions to migrate as soon as possible.

However, the major incentive at this point will be the cost of not migrating. Banks that don’t migrate in time could see MT messages they are sending fail to go through, leading to disrupted payments and losses. Swift has said it will offer a conversion service for low-volume MT messages, but this will incur an additional charge.

Conclusion

Much is still unclear about ISO 20022 – in particular, the extent to which migrating to the messaging system will reduce delays, or the use cases for the additional data that will be most valuable for financial institutions and cross-border payments companies.

What is clear is that the Swift migration towards ISO 20022 is a monumental task, and it could take many years before it has the impact that proponents advocate. The sheer amount of time and effort involved in adapting for a new payment message makes it an overwhelming prospect for many financial institutions, and the question is whether they are willing to prioritise it when there are plenty of other challenges demanding their attention.

As more large banks transition to the new standard, the industry will watch closely to see whether they are reaping the benefits. However, as far as Swift migration is concerned, there is still a long road ahead.