Neobanks have been transforming the financial landscape in many parts of the world, not least in major countries in Africa.

In recent times, emerging markets such as Africa have been rapidly evolving in digital-first financial services, including digital banking and payments, despite limited economic resources.

In particular, African startups offering technological innovations for the finance industry are increasingly operating solely online, with companies catering to a wide range of applications having emerged across the continent. Key services include current and savings accounts, ecommerce checkout, money transfers, fundraising, investments, payments, donations and loans, although different fintechs are focusing on different areas. However, they are united in serving demand that has traditionally been unmet in the continent.

In the last 10 years, Africa recorded huge smartphone penetration, which created a thriving ecommerce market and expanded payment services. However, one of the biggest challenges in the continent has been low financial inclusion and access to credit. About 95 million Africans are still unbanked or under-banked.

For a long time, traditional banks focused more on large corporations and high net-worth individuals, leaving low-income earners and small businesses unattended. This has been exacerbated by rigid legacy systems and a risk-averse culture, with traditional banks accumulating high operational and customer acquisition costs that are passed on to the customers.

Neobanks are changing this narrative. The fintech revolution is providing cheaper alternatives to traditional banks that better cater to the wide range of needs of a previously under-served customer base. Using advanced analytics and AI, neobanks are riding on the back of the fast smartphone penetration in Africa. They offer customer-centric digital financial services that are customised for mobile devices, with plug-and-play functionality and responsive interfaces at little or no cost.

The growth of neobanks in Africa

Africa’s financial industry has improved greatly as a result of neobanks, which have compelled the industry to become more competitive. Neobanks have been the proponents of financial infrastructural development in Africa, which is bringing digital acceleration and transformation to the continent and enabling it to step beyond the bounds of the traditional banking system. They are helping consumers adapt swiftly to the new-found financial opportunities and solutions technology is enabling, which were almost impossible with legacy banking.

This process began with mobile money in 2007 when M-Pesa introduced phone-based P2P money transfers. Other players from the telecommunication space, such as Orange, Airtel, Tigo and MTN, joined with additional services such as bill and merchant payments and remittances.

African fintechs plugged into this and started adding neobank services. While most African fintechs do not refer to themselves as ‘neobanks’, they are offering neobank-like services that primarily cater to the continent’s tech-savvy young population.

Kuda Bank (Nigeria), Tyme Bank (South Africa) and a host of others offer digital banking, while the likes of FairMoney (Nigeria) and Kopo Kopo (Kenya) offer digital lending. Meanwhile Xeno (Uganda) and Carbon (Nigeria) champion investment, while 7aweshly (Egypt) helping African youths become more financially mature.

Some of Africa’s most successful fintechs are also building links with the continent’s global diaspora. Flutterwave (Nigeria) links businesses to other markets around the world; Chipper Cash (Uganda) allows users to transact across the continent and beyond and Eversend (Uganda) provides a variety of financial services via its multi-currency app.

Such developments have not gone unnoticed by investors, with both venture capital and private equity majors, including Sequoia Capital and Jeff Bezos, taking a keen interest in the African market. According to Disrupt Africa, in 2021 the continent attracted $883bn in investment, with South Africa, Nigeria, Kenya, Uganda and Egypt being the major neobank hubs.

Furthermore, international competitors are also seeing potential in the growth, and are looking to extend their services to the African market. Chief among these is Revolut, which in January 2022 announced it would soon be launching in South Africa as part of a global expansion plan.

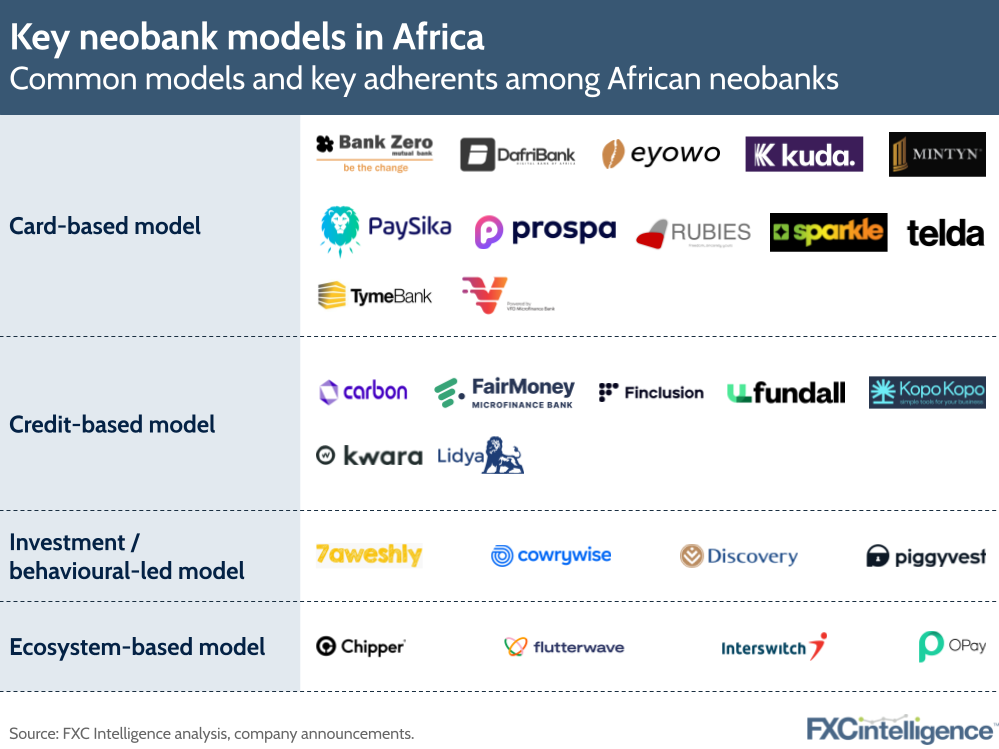

Africa’s four neobank models

There are four notable business models used by neobanks in Africa. These are:

- Card-based model: Most African neobanks, especially digital banks, offer debit cards to their customers. Their partnerships with financial service corporations such as Visa and Mastercard allow them to get paid an amount from the processing fees that merchants are charged. Most of them also offer their debit cards to their users free of charge, and many also provide discounts and offers from partner businesses to promote their use.

- Credit-based model: In order to promote financial inclusion, some neobanks are set up specifically to provide credit through digital lending to individuals and micro, small and medium-sized enterprises (MSMEs). They make revenue from the interest rates applied to those loans.

- Asset-based model: This model prioritises offering investments and digital trading services, such stock brokerage, crypto trading, saving in gold and long-term savings with high interest rates.

- Ecosystem-based model: This model creates a unified platform such as a marketplace or superapp that integrates solutions for several financial needs. These can include bill payments, remittances, investments and short-term lending.

Common neobank products

Many neobanks in Africa are focused on boosting financial inclusion by making cost-effective financial solutions available to Africans. They are creating better personalised customer journeys than traditional banks, with a focus on creating financial independence and a great customer experience that matches the needs of the customers. Common products include:

- P2P money transfers. P2P money transfers and bill payments is one of the most frequently needed financial services. Most fintechs offer this service through their apps directly or through the wallets on their apps. Some also offer credit for this purpose though soft loans and salary advances.

- B2B money transfers. Some fintechs are focused on providing small-scale business banking and e-commerce payment gateway services. These are typically provided to MSMEs that have limited financial structure, making it easier for them to stay in business since they get little support from legacy banks.

- International remittances. Most legacy banks in Africa make it tough to initiate cross-border payments or money transfers. especially for those that don’t have the foriegn currency as cash or have an account in that currency. Fintechs are helping Africans overcome this hurdle by offering virtual dollar cards, multicurrency wallets and platforms that increase the ease of cross-border transfers or payments.

- Investment and financial management. Fintechs have also aided financial education and management through increased transparency and access to financial tools compared to legacy banks. These include periodic credit reports, expense analytics and budgeting tools. There are also opportunities to micro-save at high interest rates as well as invest in gold, stocks, assets and cryptocurrencies.

African neobank innovators in the cross-border payments space

A number of fintech organisations cater in particular to African cross-border needs, including Eversend, Chipper Cash and Flutterwave, which span consumer, B2B and merchant services.

On the consumer side, Eversend offers a financial super-app that allows easy online transactions with the lowest possible rates for African residents and Africans in the diaspora. This is done through mobile money as well as online and offline bank transfers.

SOLmate offers payment facilities to the unbanked population through its digital wallet, including enabling them to get paid and make online payments. Opay also offers a wallet-based service, providing support for international subscriptions, offline and online payments.

Some companies cater to both individuals and businesses, for example Chipper Cash, which offers both local and cross-border payments via its app. It also encourages investment in US stocks as well as cryptocurrencies, with support to buy and sell both.

Similarly, Interswitch offers omni-channel payment solutions such as Quickteller to individuals and businesses. Its coverage is enhanced through several international partnerships, such as with Finastra, American Express and Union Pay.

Meanwhile, Flutterwave offers a global payment platform service to merchants and payment service providers, which operates across over 33 African countries.

Challenges facing neobanks in Africa

Despite how much neobanks in Africa have grown, they are still faced with some challenges. These include limited services, a lack of physical presence, unfavorable regulations in host countries and stiff competition. Here are some of the biggest challenges that continue to impact neobanks in the continent

Regulatory challenges

Some African countries are resistant to some aspects of digital financial infrastructure. For instance, Egypt did not grant Tyme Bank permission to implement its initial expansion plan in the country because Egypt’s cybersecurity regulations do not permit a bank running on Amazon Web Services.

Looser regulations can also spark consumer concern. Neobanks, for example, are not required to get a banking license before they commence operations, which can create reluctance among potential customers. To overcome this, many fintechs now seek commercial licenses to assure their customers as well as expand their coverage.

Limited services

Neobanks often have fewer services compared to traditional banks’ comprehensive financial services. As a result, many neobanks’ customers still also have major accounts with the traditional banks where they can do more financial activities. However, companies are responding to this: several fintechs now offer multiple financial products and services through their superapps and partnerships.

Trust

Many Africans are still new to neobanks’ digital approach and mode of operation. While Gen Z and Millennials are relatively comfortable with a digital-only offering, older customers are wary of their lack of physical presence that a customer can visit if an issue arises.

Sustaining growth

As with fintechs in many parts of the world, neobanks in the continent face the challenge of scaling effectively so that they can move beyond the growth stage and become a sustainable brand that is ultimately profitable. Many companies in the continent are attracting strong valuations and customer interest but are not yet at that stage.

Fragmented market

With 54 countries and a wide variety of languages and regulatory standards, Africa is not a particularly unified market to grow across. Companies that wish to scale and interoperate across the continent need to find solutions that bridge these issues.

Competition

Traditional banks in Africa have recognised the competition that neobanks present, and many are starting to create digital products that are designed to mimic those offered by neobanks. These include offerings in areas such as bill payments and remittances, although established banks are also setting up full-service digital banks that act as sub-brands to their core company. Examples include ALAT, a digital bank from Wema Bank, and OneBank, a digital banking app from Sterling Bank, both of which are based in Nigeria.

Meanwhile, telecoms companies have also joined the fintech race in Africa. MTN Nigeria Communications and Airtel Africa, for example, recently received permission from the Central Bank of Nigeria to commence a full range of financial services, including digital banking, cross-border money transfers, bill payments, investment and microfinancing.

With so much competition and an increasingly crowded market, we can expect to see significant upheaval in the African neobanking space over the next few years.