Digital money transfer player Wise is known for its low costs and highly competitive approach, but how does its business model really work? We spoke to Wise CFO Matt Briers to find out.

Wise, one of the biggest companies in digital money transfers, is well known for its long-term mission of zero money transfer costs. However, exactly how the company differs from its rivals when it comes to its business model today is often far less clear – and is key to understanding how Wise is approaching its longer term goals.

Having made its public markets entry in a rare direct listing on the London Stock Exchange in July 2021, Wise has consistently grown over the last few quarters, with its most recent results, Q1 23 (Q2 22 in calendar time), being particularly strong. Revenue climbed 51%, with volume growing by a similar amount.

“In the last quarter, we moved just over £24bn of volume, which is a really big number,” says Matt Briers, CFO of Wise. “I don’t think there’s any standalone companies that move more money than us now.”

Wise’s annual run rate has now passed that of Western Union, and with it continuing to grow at 40%, it’s set to widen the gap further in the coming years. Only some of the larger corporate-focused players such as Convera move more, but Wise is catching them too.

“If you look at the quantum that we’ve grown, 40% of £24bn is about £10bn: we’re adding £10bn year-over-year [per quarter],” he adds. “That number, as well, is bigger than most of the other players.”

In the US, the company is seeing growth notably above this, while in the UK, where it has operated for the longest, revenue growth still remains at around 30% – a figure that, says Briers, “actually makes me scratch my head”.

Critically, while Wise may be the biggest standalone consumer-focused company in terms of annual run rate, it still represents a very small market of the total overall market globally – Briers says around 3-4% for consumer money transfers and “a fraction of a percent” for small businesses.

Much of the rest of the market is dominated by banks, and they continue to be where the majority of Wise’s customers come from.

“There’s still just so much more to go after,” he says. “Prices aren’t really coming down that much in the industry; international payment speed is still pretty terrible.

“We’ve solved much of that problem, and we’ve got a really beautiful way to use the product, whether for personal or business. That’s driving our growth, and given the size of the market, I don’t really see it slowing down anytime soon.”

How pricing shapes Wise’s business model

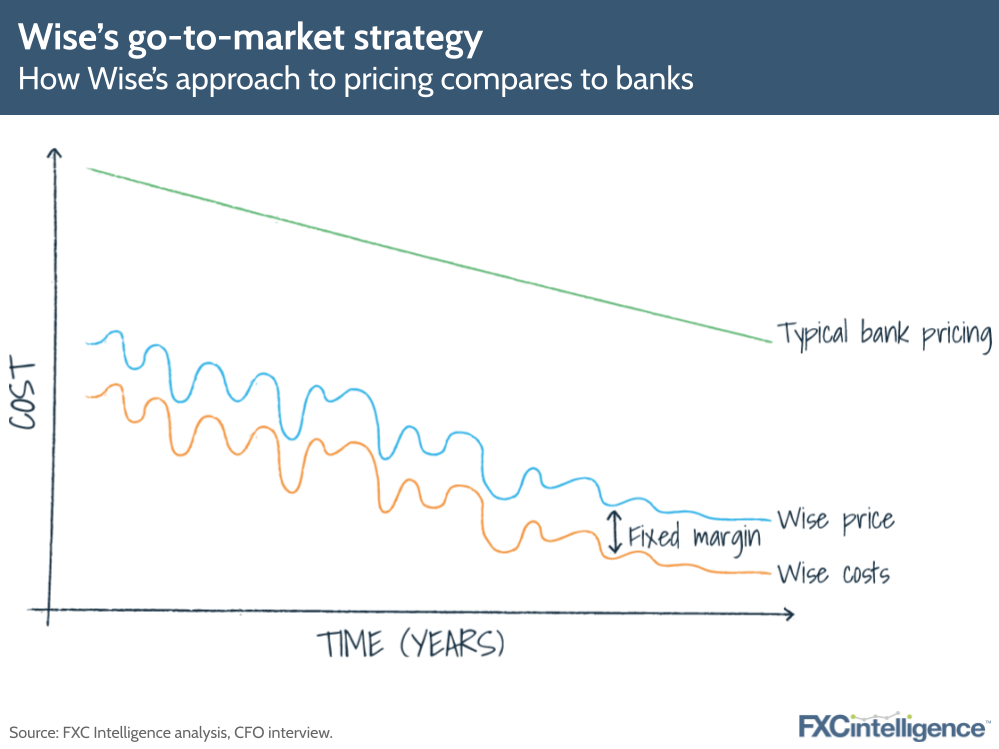

Wise’s long-term mission to make pricing free attracts interest and – at times – incredulity in the industry. In reality, this is more of a mission statement, as Wise’s prices have most recently been stable and in some cases rising (we explain why below). However, it also has a focus on convenience and speed, aiming for instant transfers. Together these form a framework to continue to iterate to “drive down” costs, and is paired with a mentality that “if something can be done cheaper, then it probably will be done cheaper”.

Now that Wise has achieved scale, its approach is now to take a cost-plus approach to its pricing. Rather than charging a fixed percentage that would have undercut existing offerings, the company instead charges a sustainable margin that moves with its costs and maintains its profitablity (something investors want to see).

“We could have easily charged 1%, but we knew that ultimately somebody’s going to come in and be able to do it at a lower price point. We do that with the lowest unit cost we believe there is,” says Briers.

“It’s not many businesses in the world that have a 20% margin like we do.”

This approach is notable for being quite different from how many other businesses in the space operate, as it means that while prices are broadly reducing over the long-term, they fluctuate over the short-term as external factors raise and lower costs – mainly the costs of currency in the foreign exchange markets.

If the Wise business lead wants to reduce the price to consumers in a corridor, they have to prove that they can also lower costs so as to maintain Wise’s margin. Likewise, if costs go up for Wise in a corridor, forcing it to raise prices, the business leads have to communicate this to customers.

This push to only reduce prices if costs can be reduced too is part of the continually iterative culture of the company of finding ways to make a transfer cheaper. The assumption alongside this (which has broadly held true) is that if the price to the customer can be reduced, market share can continue to be taken.

“Are we going to be free in 10 years time? Highly unlikely,” he says.

“If we are, we would’ve found a very commercial way to do it. You can see over the last three years, with an incredible amount of effort in engineering, how hard it has been to even scale away our own unit costs.”

One area of potential benefit is the Wise account, which is allowing the company to extend its range of products and so increase customer stickiness, as well as earning interest flow income that may help it counter costs in other areas. However, over the next decade much of the source of cost-reduction will not be single large-scale initiatives, but by taking an interactive approach to tackle multiple points of friction that together make up the source of money transfer costs.

“Over 10 years, it’s all those little things that add up to lots of progress; they build an annuity of benefits over time,” he says. “You fix one thing, it makes payments faster. So you fix lots of little things.

“Every individual thing that we’ve built, anyone could have done. But when you add it all up and you try and do it all together in a quarter and present it to customers in a useful way, then you realise how hard it is. There’s not one silver bullet.”

Pricing and Wise Platform

While Wise’s biggest revenue generator is its personal money transfer customers, and to a lesser but growing extent its small business customers, it also has a growing platform business, Wise Platform, which allows it to provide its products for use by banks.

This has seen Wise offer this service primarily on a co-branded basis, although in some cases it is offered as a white-label solution. For banks, it is a way to offer a strong cross-border payments solution without needing to build their own solution, which Briers stresses is “really hard to do”.

“Banks are very busy, and they’ve got relatively old technology compared to us,” he says. “So prioritising this integration is not insignificant for us – we try and make that as easy as possible.”

However, pricing is a significant factor in banks’ decision on whether to adopt the platform, and even calculating how to approach this can be a challenge.

“If they’re charging 3% today and it costs them radically less than that – although it’s quite hard for them to work out how much this stuff costs them – they need to work out when they should offer their customers this at a lower price,” he says, adding that even with white label solutions, the company asks that banks be transparent about their pricing.

“If they ask for 2% as the price, we’re pretty resistant to that, because it just reinforces the problem in the industry. And, of course, there’s platforms out there that are quite happy to reinforce the problem.”

He sees this approach as “quite short-termist”, adding that the company instead focuses on showing banks how many of their customers are already switching to Wise.

“The idea is if a bank can integrate us, we will send those customers back to doing all of this activity back on their platform. That happens where we integrate with these banks, which is pretty cool.”

Here banks can charge a convenience fee, which he stresses the company is “totally happy with as long as it’s transparent”.

“Banks can say, ‘actually, we’re using Wise, and Wise payment is at 50 bits, and we’re charging 30 bits on top of that’. We are really happy with that because we recognise it costs money to run their app, their site or their own processes.”

The economy and an uncertain future

While Wise has a strong plan to continue reducing costs, it does so against an increasingly challenging landscape both for the money transfer industry and its core customer. First is the economy, which is facing significant international headwinds as inflation begins to bite.

Here Briers says Wise “hasn’t seen any change” in it’s business, although it has gained customers during the time – something that he attributes to the relative importance of money transfers to peoples’ lives compared to more discretionary things that dominate areas such as ecommerce.

However, on the business side, there has been an impact to send volumes.

“We don’t see impact on the number of active businesses, but we do see them sending more money, which means basically maybe their supply chains have just got more expensive,” he explains, adding that volume per customer has increased by around 10-15%.

Yet despite this, he is cautious about potential future impacts, particularly as the prospect of a recession looms.

“I’m not going to say we’re going to be fine – I think that’s very arrogant. This is going to be very hard next few years,” he says.

“But people are going to get more cost-conscious, and they’re going to get more aware of how they are going to save money on their bills.

“At the moment, seven or eight in ten don’t even know how much they’re paying with their bank. Hopefully people will start getting more aware of this and we’re well-positioned in that situation.”