HSBC has launched Zing, a new multicurrency and money transfers product in the UK market that is designed to rival the likes of Wise and Revolut. We look at how Zing’s offering compares to the wider market.

In the money transfers sector, the start of 2024 has seen the headlines dominated by the launch of HSBC’s standalone consumer product Zing. Positioned to rival the likes of Wise and Revolut, Zing offers a combined multicurrency wallet and money transfer service, and is initially available to customers in the UK.

With the global consumer-to-consumer cross-border payments market set to grow at a CAGR of 5.9% between 2024 and 2032, and a new generation of customers looking for digital-first multicurrency and money transfer services, there is the potential for products such as Zing to thrive. But how is the company positioning against potential rivals, and where is it differentiating itself?

In this report, we review Zing’s offering against its main competitors, as well as providing a breakdown of the app’s features and capabilities.

Zing’s place in the money transfers market

Zing is positioning itself as “the worry-free international money app” for consumers, highlighting security, a flexible experience and “radically transparent” payments as its three main pillars. Its focus on developed markets, as well as its branding, also indicate that it is initially pursuing the younger expatriate market.

With both multicurrency card features and the ability to send money within the app, the company is positioning itself to primarily rival Wise and Revolut, both of whom have similar offerings, but is also likely to be hoping to take share from other players in the money transfer market.

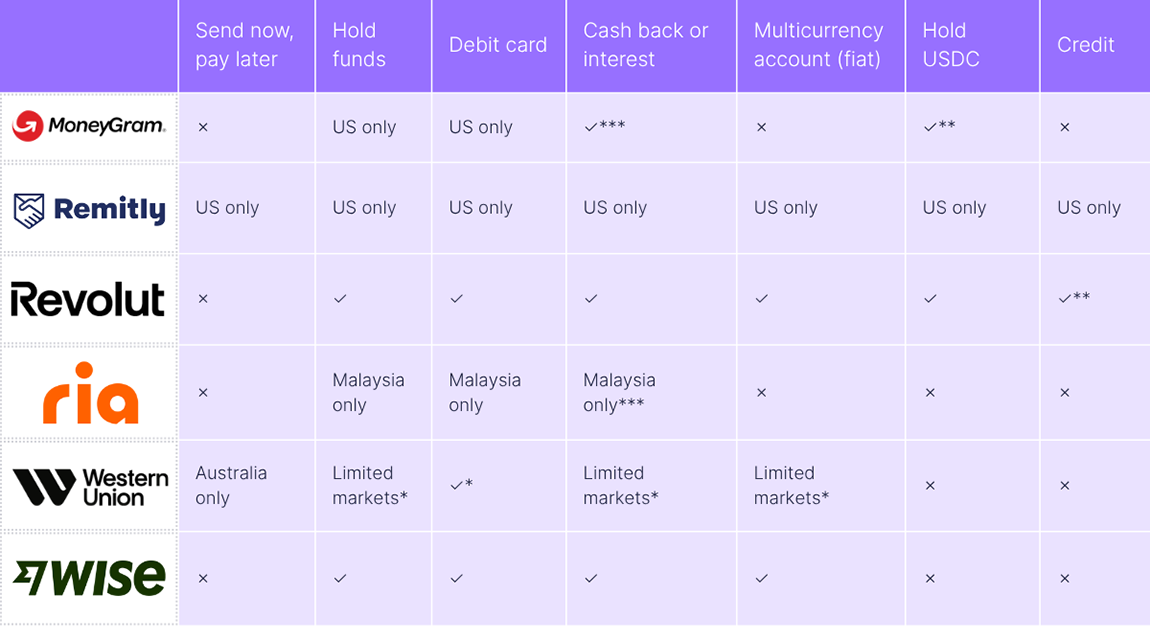

Comparing multicurrency offerings

As a multicurrency player, Zing enables users to hold money in pound sterling (GBP) as well as nine further currencies:

- AED – United Arab Emirates dirham

- AUD – Australian dollar

- CAD – Canadian dollar

- EUR – European Union euro

- HKD – Hong Kong dollar

- JPY – Japanese yen

- NZD – New Zealand dollar

- SGD – Singapore dollar

- USD – United States dollar

This is a smaller number than those offered by Revolut (30+) or Wise (40+), but does represent some of the world’s biggest currencies, as well as many of the key money transfer corridors for expats based in the UK, with South Korea being the main missing exception.

As a consumer multicurrency offering, while Zing has fewer options than some of its rivals, it is otherwise a similar service, providing both the ability to hold money in a variety of currencies as well as the ability to send money to multiple other markets.

While Revolut and Wise are the clearest direct competitors, there are also a number of similar multicurrency products aimed at more mature expatriate customer bases. These include Barclays’ Foreign Currency Account and an alternative service from HSBC directly, its Global Money Account.

In both cases, these require customers to already hold a full account with the bank and act as add-on services to enable smoother cross-border payment services. As a result, these are more complex products for a different customer type and for the most part are not likely to be competing with Zing for customers.

Comparing money transfer offerings

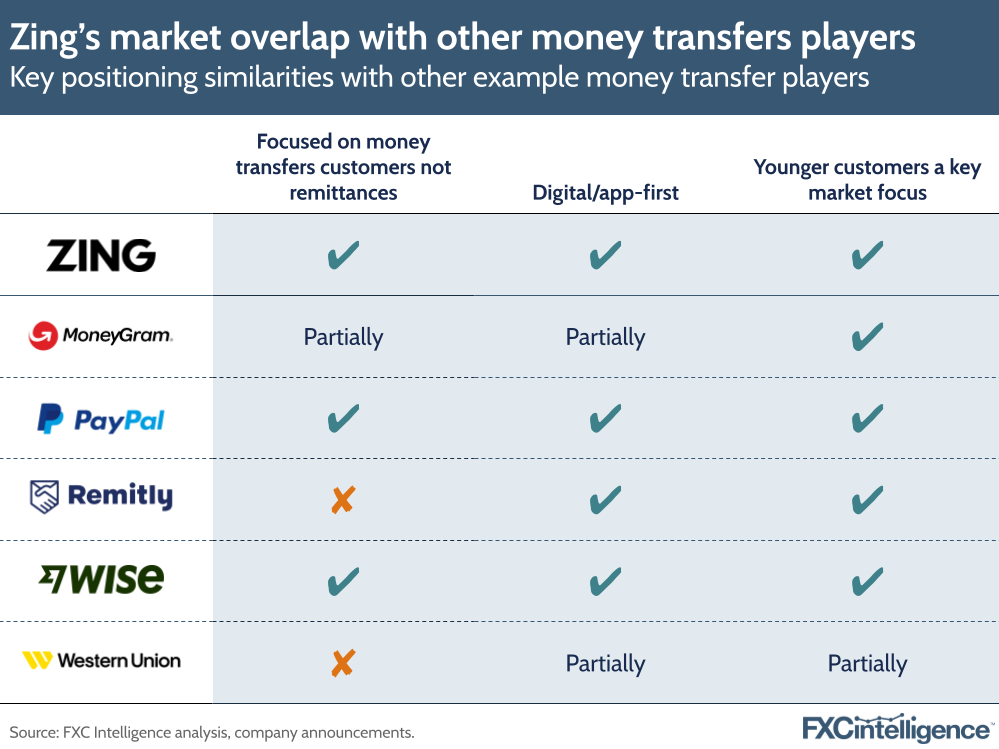

Within the wider money transfer market, there are a number of companies that Zing partially rivals. These companies do not provide the same combination of services for consumers, but do provide money transfer services that will be the primary product some customers are looking for.

Within these, there are players who have a greater or lesser overlap. Remitly, for example, has a similarly digital-led offering that is also aimed at younger consumers, but instead caters to remittance markets. MoneyGram, meanwhile, has traditionally served the remittance-focused retail market, but with its recent privatisation is pivoting to increasingly cater to the younger, money transfers-focused digital market in addition to its traditional customer base.

Western Union, by contrast, has a digital offering but remains largely focused on more traditional remittance requirements, while PayPal provides a simple online-only money transfer service that, like Zing, prioritises simplicity and digital access over low pricing.

Zing fees and pricing

On pricing, while Zing highlights a lack of hidden fees and says it offers “competitive rates”, our analysis suggests that the company is pricing at the upper end of the market. The company does not charge to open an account, add or redeem funds or send money to other Zing accounts in the same currency, nor does it have a monthly charge attached to accounts, but its currency conversion fees are generally higher than the market average.

Our own attempts to convert money initially saw GBP to USD charged at 0.75% of the amount being transferred on the day after Zing launched, however this has since dropped to 0.6%. Conversion prices for moves between Zing multicurrency wallets this week were priced at 0.6% for GBP-EUR, EUR-GBP, GBP-USD and USD-GBP, with all other pairs at 0.75%. There was no apparent change in percentage charged by send amount.

The company typically offers the same currency conversion rates for customers moving their money between different currencies within their account as they do for money transfers. Here rates do not appear to vary by send amount, but do vary by day, tracking above the market average for a given corridor. Customers are also charged an additional fixed transfer fee when money is being transferred to a third-party bank account.

For ATM withdrawals, Zing customers are able to make one international ATM cash withdrawal a month for free, with additional withdrawals charged at a rate of £2 each or the relevant wallet currency equivalent. Domestic ATM cash withdrawals are charged at £2 each.

This offering is relatively comparable with that of neobank Monzo, which is popular in the UK for use on holidays and other international trips as it includes a £200 fee-free withdrawal per month at international ATMs, or £400 within the European Economic Area. By contrast, Revolut provides free withdrawals in all ATMs at up to £200 per month, while Wise provides two free withdrawals per month.

How do these prices compare to other players across different currencies and dates?

Zing market positioning versus Wise and Revolut

Notably, while Zing offers many of the same consumer services and features as Wise and Revolut, albeit on a smaller scale, the company appears to be positioning itself to a younger customer base dominated more by Gen Z and younger Millennials. By contrast, Revolut and Wise have traditionally focused on Millennials and Gen X but have begun to also try to attract Gen Z customers over the last few years.

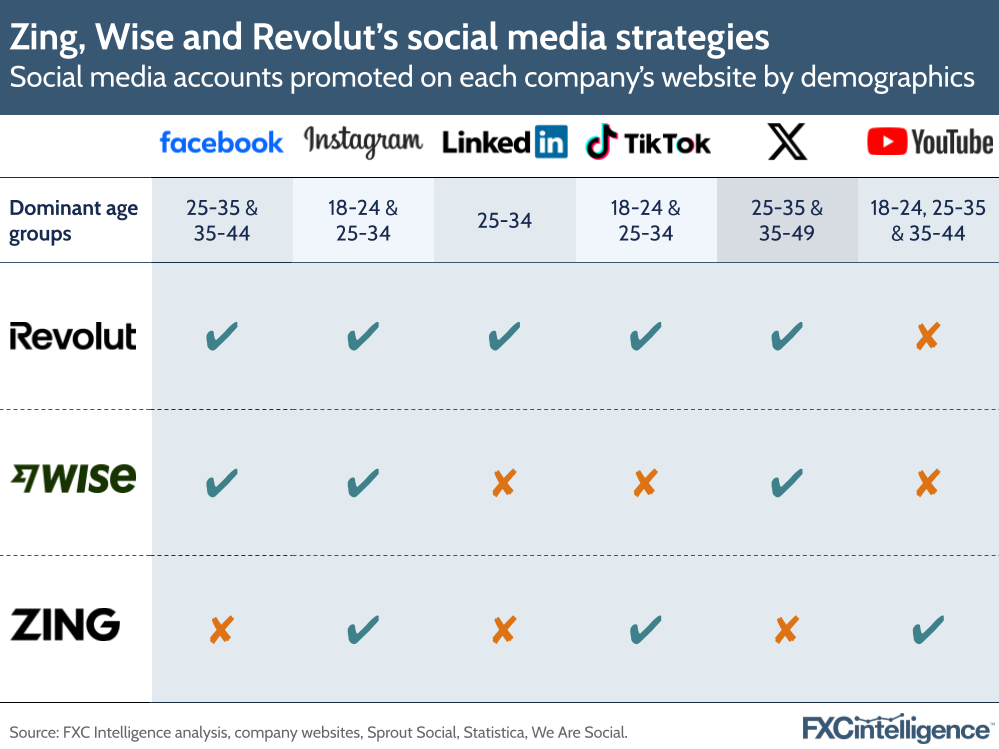

Zing’s younger focus is reflected in the company’s brand language, which uses chatty, simple phrasing, including the tagline ‘Do your Zing’. However, it is also reflected in the range of social media platforms the company is focusing its attention on and their respective demographics.

While Wise’s website links to its Facebook, Instagram and X (formerly Twitter) accounts and Revolut highlights Facebook, Instagram, LinkedIn, TikTok and X, Zing only links to Instagram, TikTok and YouTube.

These three have the youngest dominant age groups on their platforms, making them the most relevant platforms to focus on to speak to a Gen Z audience. These platforms also have a higher incidence of female users than X, Facebook and LinkedIn.

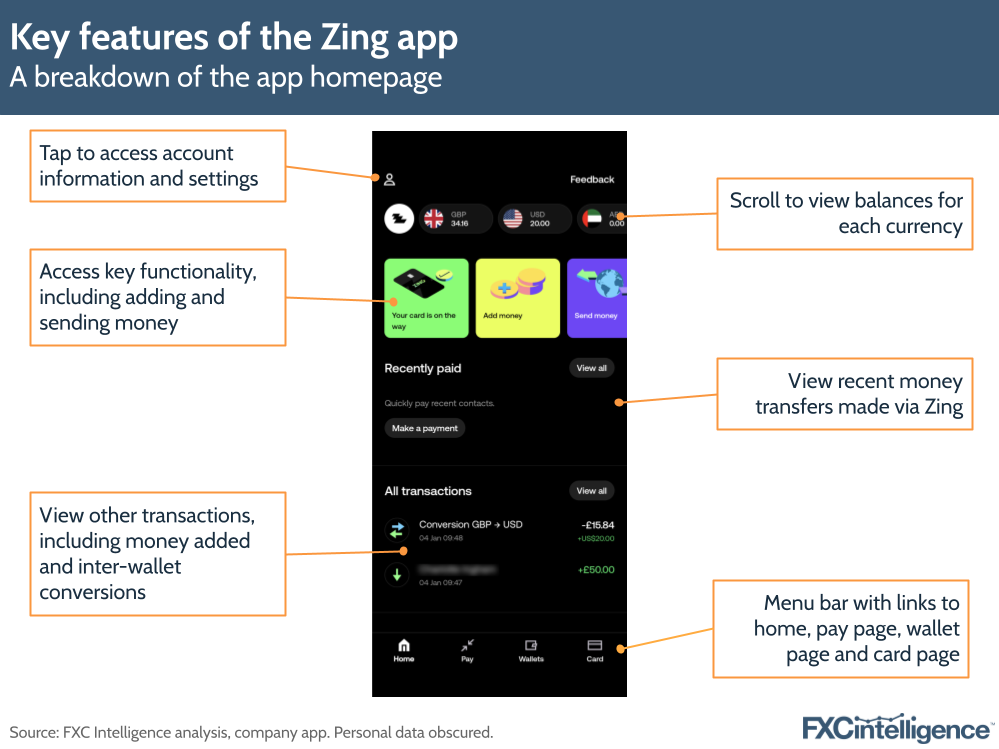

An analysis of Zing’s app

Zing’s app is designed to provide simple, clear access to its main features, with customers able to quickly add and send money as well as create new wallets for specific currencies instantly and move money between them.

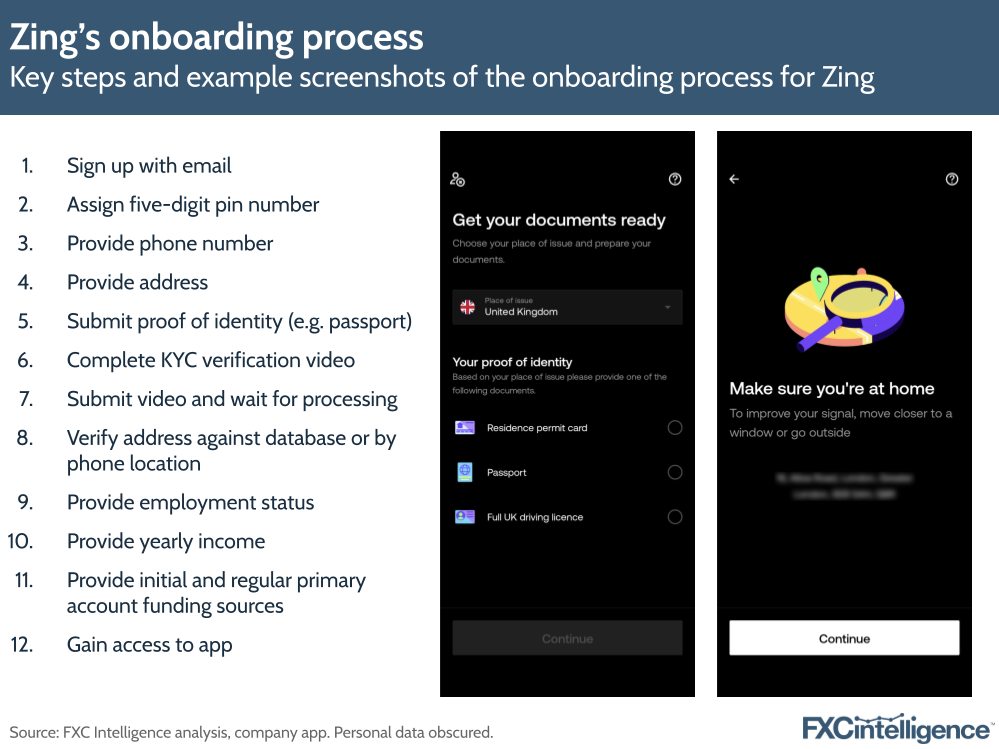

Sign-up and customer onboarding

The sign-up process is handled entirely within the app, and is split into multiple short screens, each requiring a single or small number of data points to be entered, before moving onto the next step.

KYC is also handled within the app, with customers required to take a photo of their proof of identity before recording themselves moving their head as instructed and reading out a number of prompts. For location, the app leverages location services to simplify the process.

Our sign-up on the app took less than 10 minutes to complete, although this is likely to vary depending on how long the verification process takes to finalise.

The decision to keep the amount of information per page small is likely to be an intentional choice to make the process feel simple and accessible, as is the in-app nature of the verification process.

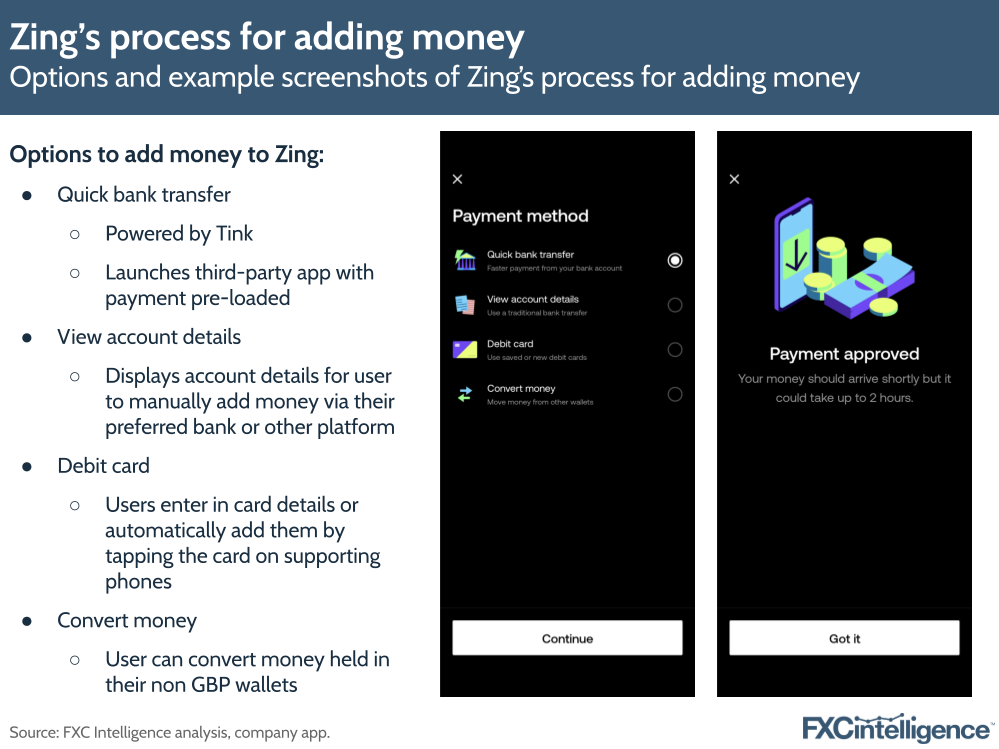

Adding money and currency conversion

Adding money to the app is similarly designed around simplicity, with the default option being a quick bank transfer. Powered by open banking player Tink, this sees users specify the amount of money they want to add within the Zing app, before choosing the bank they want to use for the transfer from a list.

From here, that bank’s app is launched pre-loaded with the details of the transfer for the customer to check and approve, before returning to the Zing app where the money appears. This final step can take up to two hours, although in many cases – including in our tests – was instant.

An alternative card payment-based method also supports the ability to populate the card details fields by tapping the card on the user’s phone, and there is also an option to view bank details to initiate a traditional transfer.

Once users have money within the account, they can opt to convert this into other currencies by opening a wallet for one of nine other currencies. These are created instantly, and can be closed instantly too when empty.

Moving money between currencies is an instant process, with the user given an outline of the charge for the transaction before they initiate it.

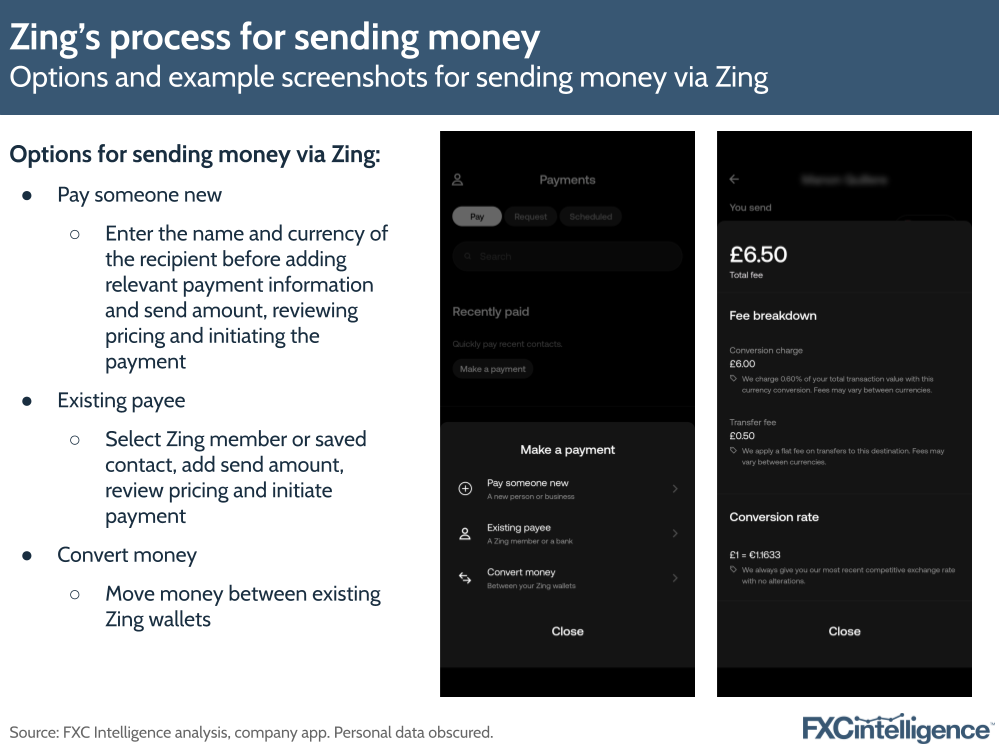

Sending and receiving money

Sending money via the platform appears to be designed to encourage repeatability, as customers create a contact for a recipient before they initiate a transaction. This process sees customers add the recipient’s name, currency and key account information, such as IBAN. If the recipient is a Zing user, the process is similar but simplified.

Once a contact is created, the customer can then see how much a money transfer to them will cost on that particular day, before initiating the transaction.

Significantly, customers can only view pricing for a corridor once they have loaded in a recipient for that corridor, unlike Wise, which provides this information up-front. If the corridor is one where Zing also has a wallet service, they can view conversion fees by checking this, but this will not include any additional fees and does not apply to the majority of the corridors Zing supports.

As a result, customers have to sign up, complete full KYC and add a contact, including their account details, before they have a full picture of how much a transfer will cost. This strategy may be a reflection of the fact that Zing does not appear to be trying to compete on price, but instead on simplicity.

Implications for the multicurrency and money transfers market

The launch of Zing indicates that while the consumer money transfers market is considerably more mature than the B2B cross-border payments market, there is still space for innovation and competition, particularly as Gen Z emerges as a stronger consumer category.

The relatively small number of players offering combined multicurrency cards and money transfers services also suggests that this is an area where there is more potential for product launches in the future.

Significantly, the fact that Zing is a product from HSBC indicates that such standalone products may be an effective approach for banks that have traditionally been losing market share to fintech. If Zing proves to be successful, we may therefore see other banks and traditional finance products look to tap into underserved markets through the launch of such niche apps.