The B2B cross-border payments industry has enjoyed a positive year to date, with key players posting strong results throughout 2025. We take a look at some of the key trends and activities throughout the year so far.

2025 proved to be a good year for the majority of players in the B2B cross-border payments industry, with many reporting strong revenue growth in the first three quarters of the year. We also saw a number of acquisitions within the space, while many companies began rolling out a range of stablecoin-enabled products and services.

This year, we refined our market sizing report, which outlines that the B2B cross-border payments market had a global size of $31.7tn in 2024 and is set to grow by 51% to $47.8tn in 2032. Compared to consumer money transfers, which had a global total addressable market (TAM) of $2tn in 2024 and are set to grow to $3.1tn in 2032, it’s clear that the biggest opportunity belongs to B2B payment providers.

To find out how the B2B industry has performed in 2025, we take a look at some of the space’s key players’ performance in the year to date, alongside some key trends.

How did key B2B players perform in 2025?

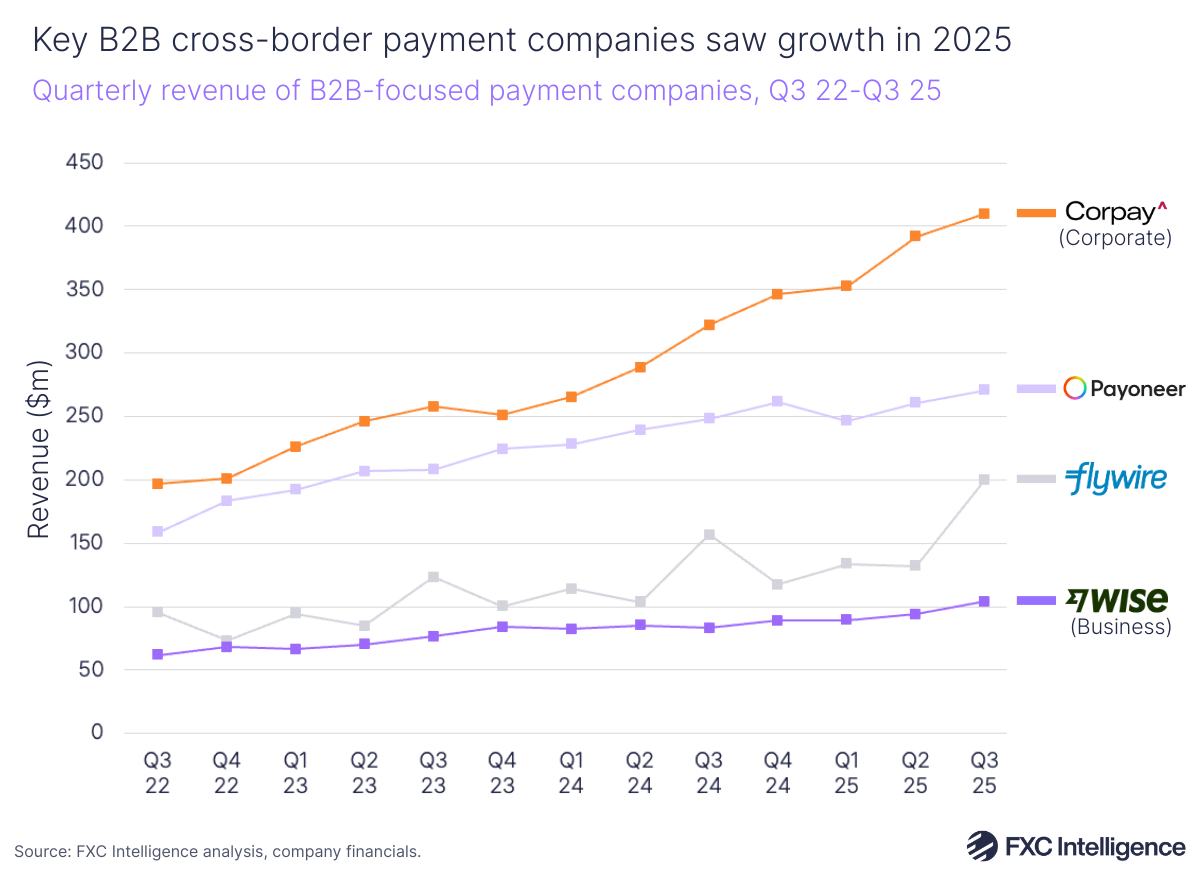

The majority of B2B players reported revenue growth in 2025, with payment provider Corpay continuing to report the highest revenue of all of the corporate payments companies we track. For Q1 to Q3 2025, it saw its total corporate payments revenue grow 32% versus Q1-3 2024 to reach $1.15bn. Corpay attributed this growth to record sales performance, particularly in APAC, Canada, Europe and the UK – although growth in the US slowed in the latter part of the year due to the impact of tariffs.

Payoneer also continued to report steady growth for the first three quarters of 2025, with revenue increasing 9% YoY to $778m. During our post-Q3 earnings discussion, CEO John Caplan explained that just shy of a third of this revenue comes from customers receiving over $250,000 a month in volume, driving 27% B2B revenue growth.

Of the companies we analysed, Flywire reported the second-highest growth rate in the first three quarters of 2025 – 24% YoY to $465.5m. The company explained that B2B grew at multiples of overall company revenue growth in Q3, which it said was a reflection of demand for its invoice-to-cash capabilities.

Wise reported rapid growth of its business segment throughout 2025. The company saw YoY business revenue growth outpace consumer revenue in both Q2 (10% vs 9%) and Q3 (25% vs 10%), while for the year so far it achieved 15% YoY growth in business revenue with $287.7m.

The B2B companies adopting stablecoins

Throughout 2025, stablecoins have dominated much of the discussion surrounding the broader cross-border payments space, with many companies leveraging the emerging technology to reduce costs and speed up settlement.

This was no less true in the B2B space. For example, Corpay teamed up with Circle to embed USDC into its cross-border payment rails, giving businesses access to 24/7 settlement and programmability. In Q3, Corpay Group President Mark Frey told us that the company is currently developing its stablecoin and digital currency infrastructure, explaining that these efforts have not yet resulted in a boost to its bottom line, although the company expects this to eventually change. Looking to the future, Corpay says it plans to leverage stablecoins to offer its corporate customers “always-on, 24/7 payments”.

Visa later announced plans to launch a stablecoin prefunding pilot, enabling businesses to pre-fund Visa Direct with stablecoins instead of fiat to cover payouts. Nium became one of the first companies to participate in the pilot, with plans to offer its business customers faster settlement times as a result. Visa says it expects to further expand the pilot in 2026.

In November, Flywire laid out plans to partner with BVNK to launch a pilot programme enabling clients to offer USDC and USDT as payment options.

Some companies also opted to leverage what many view as an alternative solution to stablecoins – tokenised deposits. Earlier this year, Payoneer partnered with Citi to use the bank’s tokenised deposit platform for treasury transfers to speed up settlement by moving funds between its accounts via blockchain tokens.

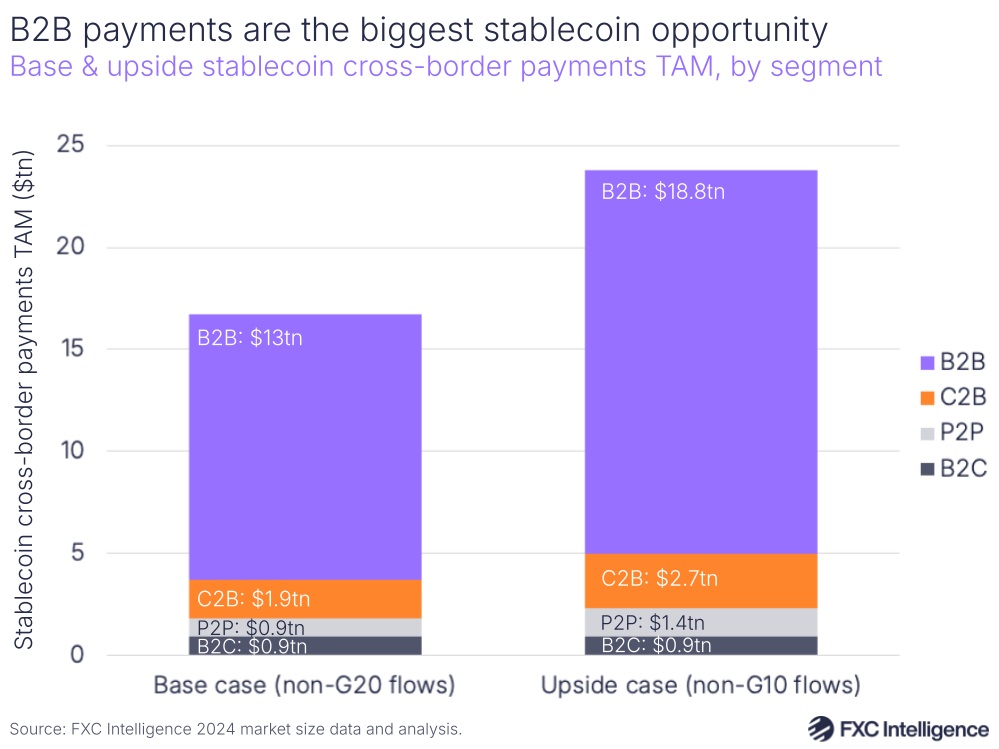

In our industry primer on stablecoins, we identified that the B2B space remains the biggest opportunity for stablecoins. Examining flows passing through non-G20 markets, we found that B2B accounts for $13tn out of the total TAM, significantly higher than the $1.9tn for C2B payments and $0.9tn for both P2P and B2C payments. Meanwhile, in the upside case, the opportunity is even greater for B2B at $18.8tn.

Acquisitions in 2025

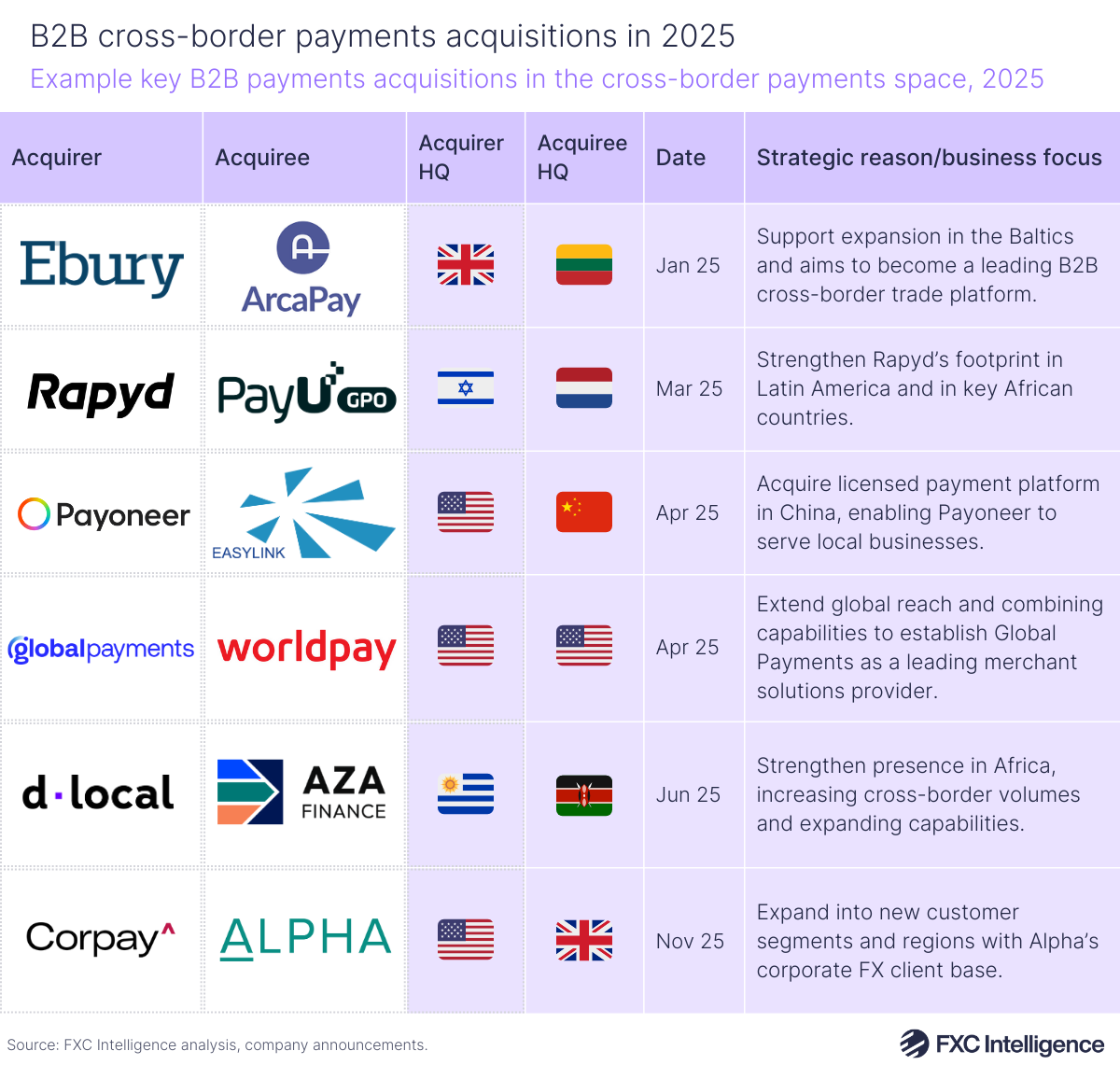

Many B2B players chose to acquire other companies in 2025, as they looked to strengthen business capabilities or expand into new markets.

In January, Ebury, the international payments and FX risk management company, announced plans to acquire ArcaPay. The acquisition completed in September, with Ebury saying the move should support its expansion in the Baltics, while bolstering its aims to become a leading B2B cross-border trade platform.

In March, Rapyd completed the acquisition of PayU Global Payment Organisation. The company said the acquisition enabled it to offer card acquiring in Mexico, Brazil, Argentina, Chile, Colombia and Peru, while expanding its market access into Africa in key countries such as Nigeria and South Africa.

Corpay also completed the acquisition of B2B cross-border FX solution provider Alpha Group in November; a move it says will help it unlock new geographies in continental Europe, while enhancing its position in Canada and Australia.

Overall, the main driver behind the majority of acquisitions in the space appeared to be geographic: either expanding into a new region or strengthen the acquiring company’s existing presence in certain markets.

No progress in making B2B payments cheaper

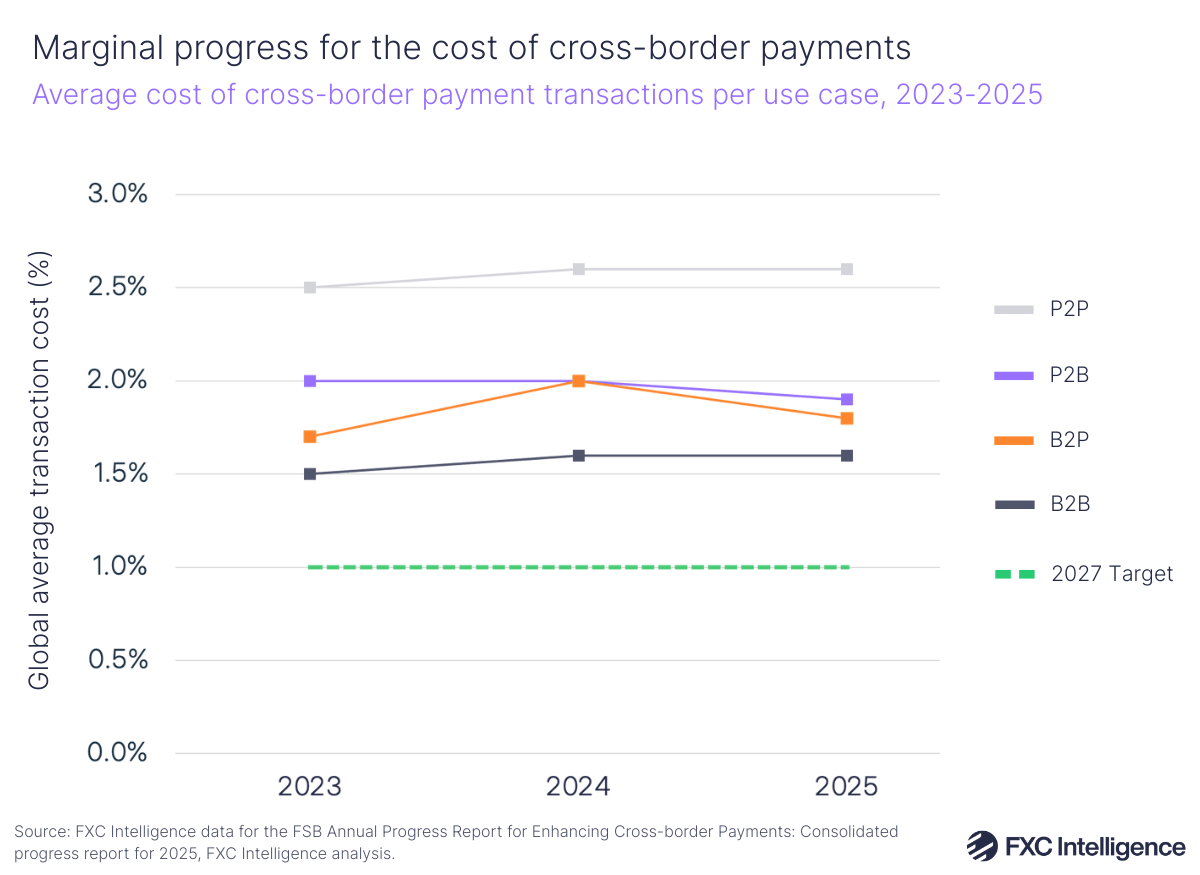

Our analysis of the FSB’s G20 Roadmap for Enhancing Cross-Border Payments report highlighted that all use cases, including B2B, failed to hit the G20’s target to ensure that the global average cost of cross-border payments is no more than 1% by the end of 2027.

Although B2B payments boasted the cheapest global average transaction cost in the most recent report, at 1.6%, it still remained higher than the average cost in 2023 (1.5%).

In 2025, only one use case succeeded in getting closer to the target than it was in 2023: the average cost of P2B cross-border payment transactions fell from 2% in 2023 and 2024 to 1.9% in 2025.

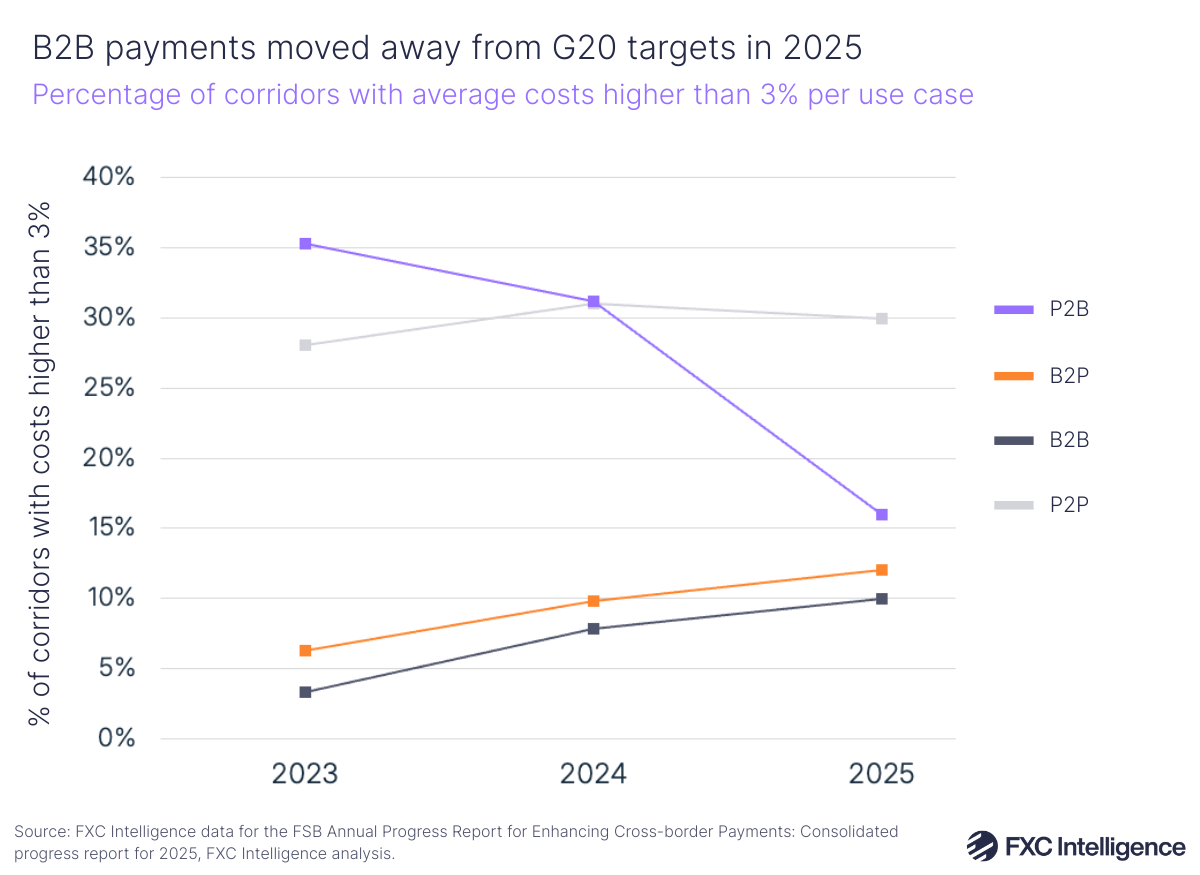

The G20 is also aiming to have no corridors with costs exceeding 3% beyond 2027. While the B2B use case led the way with the lowest share of corridors that charged more than 3%, it actually moved further away from the target for the second year running. Only 3.3% of B2B corridors charged more than the target in 2023 but this rose to 10% in 2025.

B2P saw a similar trend trend forming, while P2B emerged as the only use case that sat closer to the target in 2025 than 2023, falling from 35.3% of corridors charging more than 3% to 16% two years later.

The FSB said that greater efforts need to be made to ensure that its international policy work results in genuine real-world benefits for businesses and consumers alike across the globe. While its findings show that B2B payments have failed to make much progress towards its targets, it is clear that many major players are rapidly developing, utilising emerging technologies such as stablecoins to not only improve efficiency but also to drive costs downward – which should result in progress in the near future.