Banks have continued to see innovation and partnerships this year, particularly as the discussion around stablecoins and tokenised deposits moves into practical action. Below are some of the key trends for banks in cross-border payments in 2025.

Banks remain some of the most significant players in the cross-border payments space, accounting for over 90% of B2B cross-border payments in 2023. They are also legacy providers of payments infrastructure, with the largest banks finding it more challenging to innovate due to stringent regulation.

Cross-border payments stories in banking therefore often have ripple effects across the rest of the industry, as they highlight the movement of trends or technology into the mainstream. This year has seen banks increasingly form partnerships with other players in the cross-border payments space to extend their networks, release new products and tap into a growing demand for stablecoins and tokenised deposits.

As demand for more seamless, 24/7 payments has grown, banks have been moving to comply with new regulations and adopting new standards for payments, which in turn has increased the need for more secure fraud prevention and better transparency. Below, we’ve mapped out some of the key cross-border payments trends for banks in 2025.

Cross-border drives transaction growth for payments-focused banks

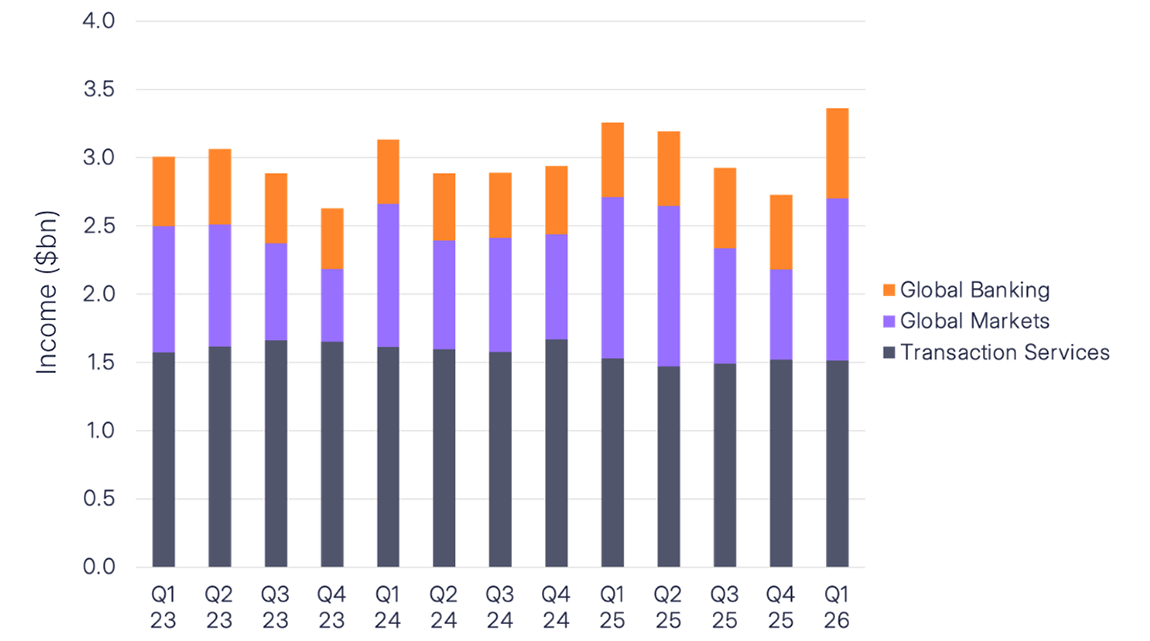

Cross-border performance is strengthening and becoming more important across banks that specifically reference metrics in earnings. For example, at an investor day earlier this year, Standard Chartered highlighted that it had increasingly focused on growing the number of products and services it offers through its Corporate & Investment Bank unit (CIB).

As part of this unit, it reported that CIB cross-border income had grown at an 11% CAGR between 2019 and 2024, with cross-border payments taking up 61% of its total income for the unit last year. The company has continually shifted its focus away from trade-only clients and towards multi-product clients, through which it is growing its revenues in transaction banking.

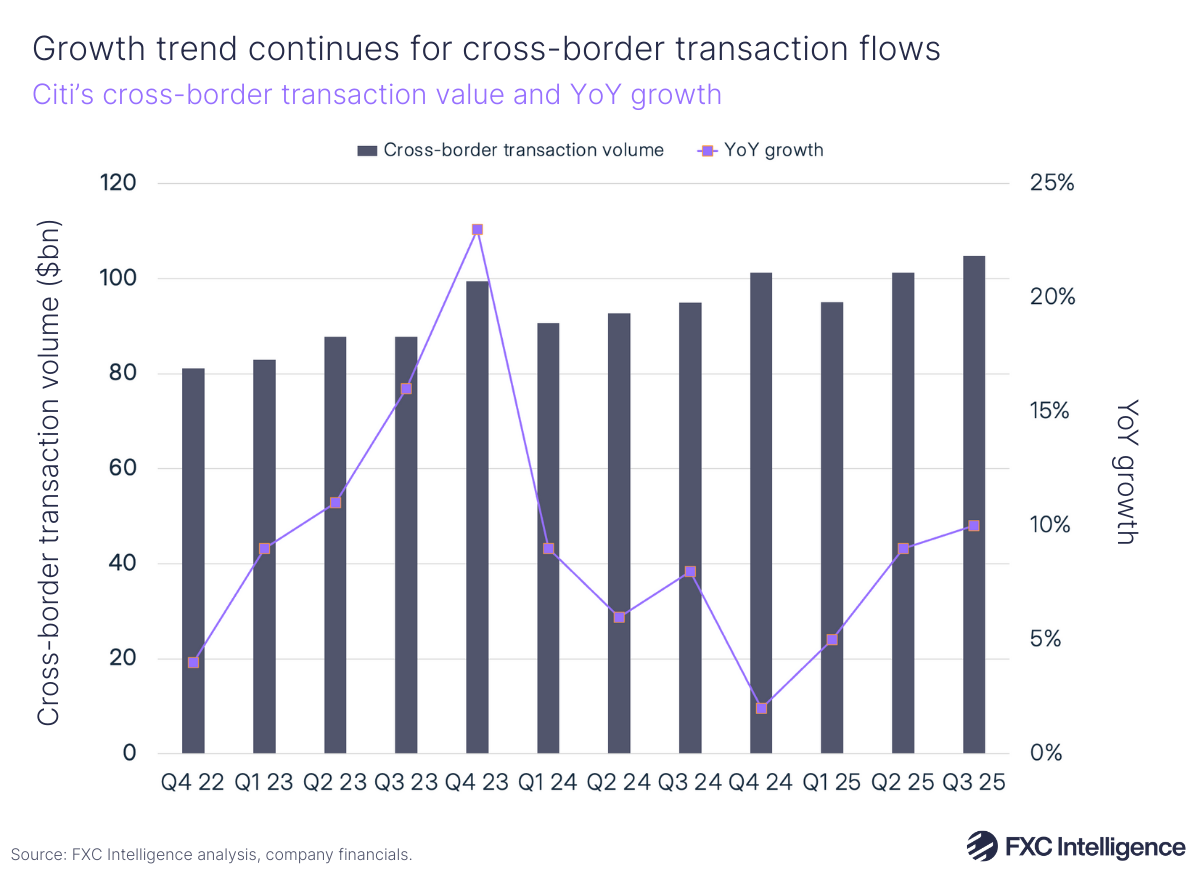

After noting slower growth in 2024, Citi has shown strong quarterly growth across 2025, with a rise in cross-border transactions being key to its overall Payments segment in its most recent earnings for Q3 2025. Citi CFO Mark Mason connected the rise to the bank’s moves to roll out digital products and services into new markets.

Earnings calls across other banks saw high levels of uncertainty over the extent to which US tariffs would impact their business, which is particularly relevant given their strong presence in the B2B payments space and how this connects to the import/export market.

Near the start of the year, our analysis highlighted that some banks expected the tariffs to lead to a wider economic downturn that would result in broader macro exposure for the banks. However, others suggested that shifts in flows or hedging activity in response to volatility could result in gains.

Reporting on tariffs among US banks has remained largely mixed in terms of performance impacts throughout the year, including in more recent earnings calls (taking place in October/November), though these banks haven’t always called out payments specifically. In its Q3 earnings call, Bank of America said that the company had seen good performance despite “uncertainties” around tariffs and rates, while Citi said that “increased clarity” around tariffs had led to growing CEO confidence. Meanwhile, Wells Fargo said that it had continued to see some middle-market companies being “cautious” while they await the outcome of the tariffs.

Banks partner with payments providers to boost networks

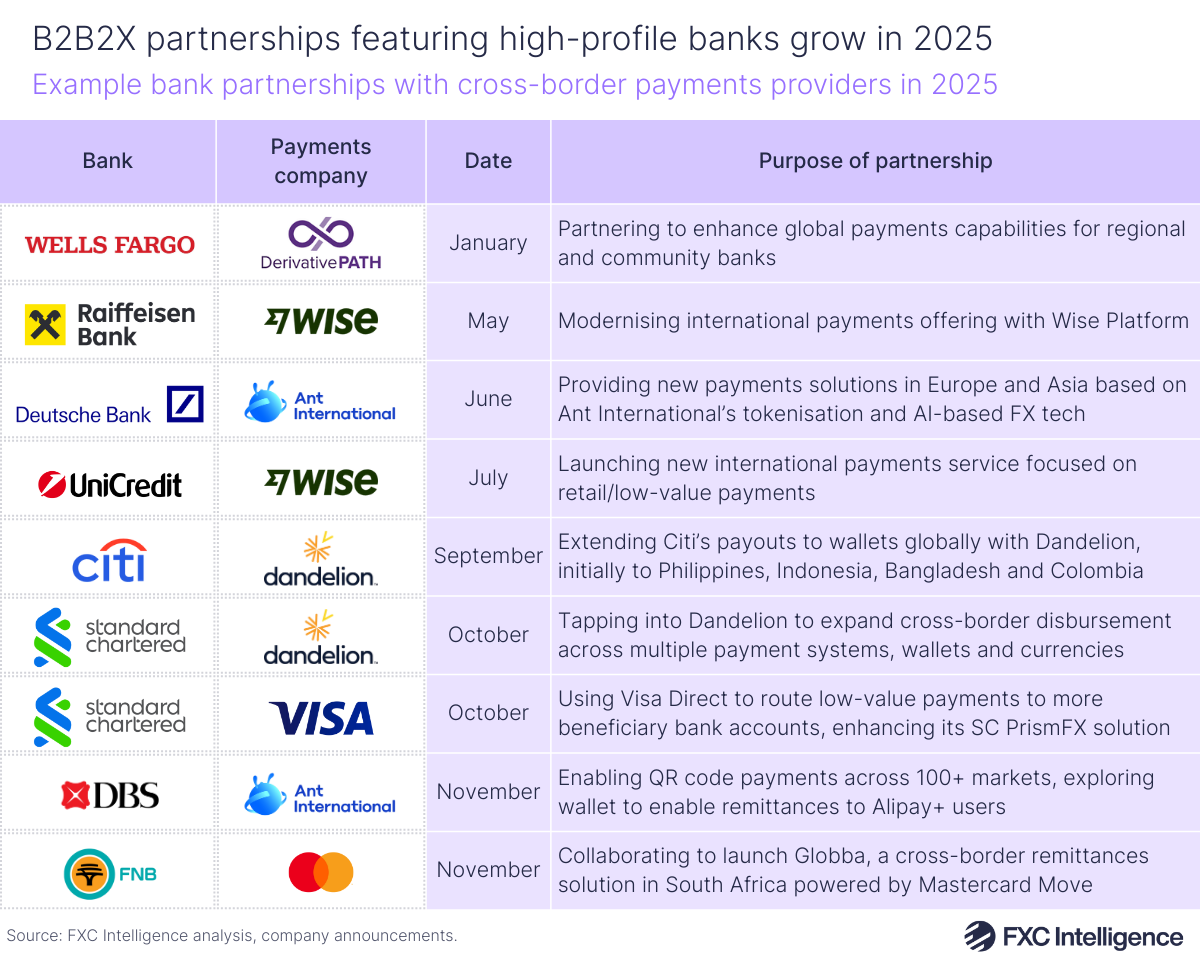

A number of banks partnered with cross-border payments providers this year to help build out their global payments networks.

For example, we saw UniCredit and Raiffeisen Bank separately partner with Wise Platform – Wise’s white-label infrastructure solution for banks, which had onboarded more than 100 financial institutions as of its investor day in April this year. Citi and Standard Chartered also partnered with Dandelion – a B2B2X solution built on the back of Euronet’s extensive money transfer network – to expand their services.

Banks are building out networks to target different customers, endpoints and locations globally. While some (such as UniCredit) are looking to target their own customers with enhanced low-value retail payments, others are looking to increasingly serve corporate payments or are aiming to improve services for financial institutions. For example, Wells Fargo’s tie-up with cloud payments provider Derivative Path earlier this year aimed to enhance global payments capabilities available to regional and community banks.

Banks have also positioned global payments partnerships at the heart of new product launches. For example, Deutsche Bank partnered with Ant International to boost its presence in Europe and Asia, while First National Bank teamed up with Mastercard to launch Globba, a new remittances solution powered by Mastercard Move.

Several deals focused on wallets as endpoints, with some of these aimed specifically at emerging markets. Citi and Standard Chartered’s partnerships with Dandelion both focus on enabling payouts to wallets, with Citi initially focusing on regions where remittances remain significant, including the Philippines, Indonesia, Bangladesh and Colombia. Extending to emerging markets where banks aren’t traditionally as well connected to consumer payouts has been a key selling point for money transfer businesses working with them.

On the consumer side, banks moving to support digital methods are becoming more important as populations in developing countries increasingly come online. The World Bank’s Global Findex report published this year highlighted that the share of people who owned a bank account in 2024 stood at 79%, up from 51% in 2011, while mobile money account ownership has outpaced bank account ownership in some countries.

Stablecoins and tokenised deposits proliferate

The industry has seen a growing number of stablecoin-related announcements on the back of growing clarity around regulations relevant to payments – in particular, the arrival of the US’s GENIUS Act, which provides a regulatory framework and rules on how stablecoins can be backed, who can use them and who can issue them. Similarly, the EU’s Markets in Crypto-Assets (MiCA) came into force in June 2023 but became fully applicable at the end of December 2024.

While the benefits of stablecoins for cross-border payments – for example, the potential for faster, 24/7 settlement, lower costs and better transparency for payments – have seen banks responding to competitive pressure to move on the technology, some have instead seen tokenised deposits as being a key technology in the digital payments space.

Banks’ real use cases have often focused on tokenisation – i.e. the process of representing real-world assets as a digital token on a blockchain. While stablecoins are an example of this, they don’t cover the full spectrum. As we observed at Sibos this year, tokenised deposits remain a key interest to banks, particularly solutions that focus on treasury movements for existing clients.

Both tokenised deposits and stablecoins are examples of distributed ledger technology (DLT) – i.e. they are digital assets that exist on systems that share and record transactions across a decentralised network. However, while stablecoins are payment instruments backed 1:1 by fiat reserves, tokenised deposits are effectively digital representations of existing bank deposits (i.e. they don’t require banks to hold reserves elsewhere). While stablecoins are more often moved across public blockchain systems, tokenised deposits are used more often in private ledgers that focus on banks’ own treasury management purposes.

Several key banks have been providing this service for some time – for example, J.P. Morgan launched its wholesale blockchain settlement solution Kinexys in 2020 and Citi launched Citi Token Services for Cash last year to enable banks to move money between Citi branches globally 24/7 using tokenised deposits. This year has seen key expansions to these services, with other banks such as HSBC and Japan Post Bank also planning to roll out new products in the space.

During Citi’s Q3 2025 earnings, CEO Jane Fraser said that Citi currently sees tokenised deposits as a more suitable solution than stablecoins for enabling low-cost real-time money movement. She also said that she believes there is currently an “overfocus” on stablecoins, though the bank is still doing significant work in this area, such as providing on and off-ramp solutions for exchanges and cash management solutions to stablecoin providers.

Having said this, stablecoin announcements in the space – particularly regarding USD-backed stablecoins – have still ramped up this year. In July, French bank Société Générale announced plans to launch a USD-backed stablecoin, with the Bank of America and Citi also exploring the area. The goal appears to be to defend their transaction revenues against fintechs and other crypto companies, as well as positioning themselves for incoming regulation.

Later in the year, consortiums began emerging exploring the possibility of joint stablecoin launches. Citi and the Bank of America were joined by Goldman Sachs, Barclays and several other banks to explore the possibility of issuing a stablecoin focused on G7 currencies. A similar group of European banks – among them BNP Paribas, ING and Danske Bank – have now formally created a Netherlands-based company, Qivalis, with the intention of launching a euro-denominated stablecoin in H2 2026.

Blockchain – the specific DLT technology that provides the structure for including transactions in separate blocks – continues to be introduced at an institutional level. Swift announced in September that it was working with over 30 financial institutions to develop a shared digital ledger that will prioritise enabling real-time, 24/7 cross-border payments. This move by a legacy correspondent banking network is possibly one of the strongest signals that the banking sector is increasingly taking blockchain payments seriously.

Real-time payments and standards drive adoption

Linked to discussions around stablecoins has been a growing demand for banks to offer real-time payments.

Banks are increasingly seeing the need to support real-time payment networks in key markets, and though this is happening at varying rates globally, growing adoption in the US – typically seen as being behind when it comes to banking infrastructure – remains significant this year.

FedNow, the US’s instant payments platform, announced that it had seen more than 1,400 participating financial institutions join the system as of its two-year anniversary in July, though there are still more than 4,000 banks across the country. Separately, the RTP network – a separate real-time payments network launched in 2017 by The Clearing House – currently has more than 950 participants sending and receiving 107 million transactions valued at $481bn each quarter.

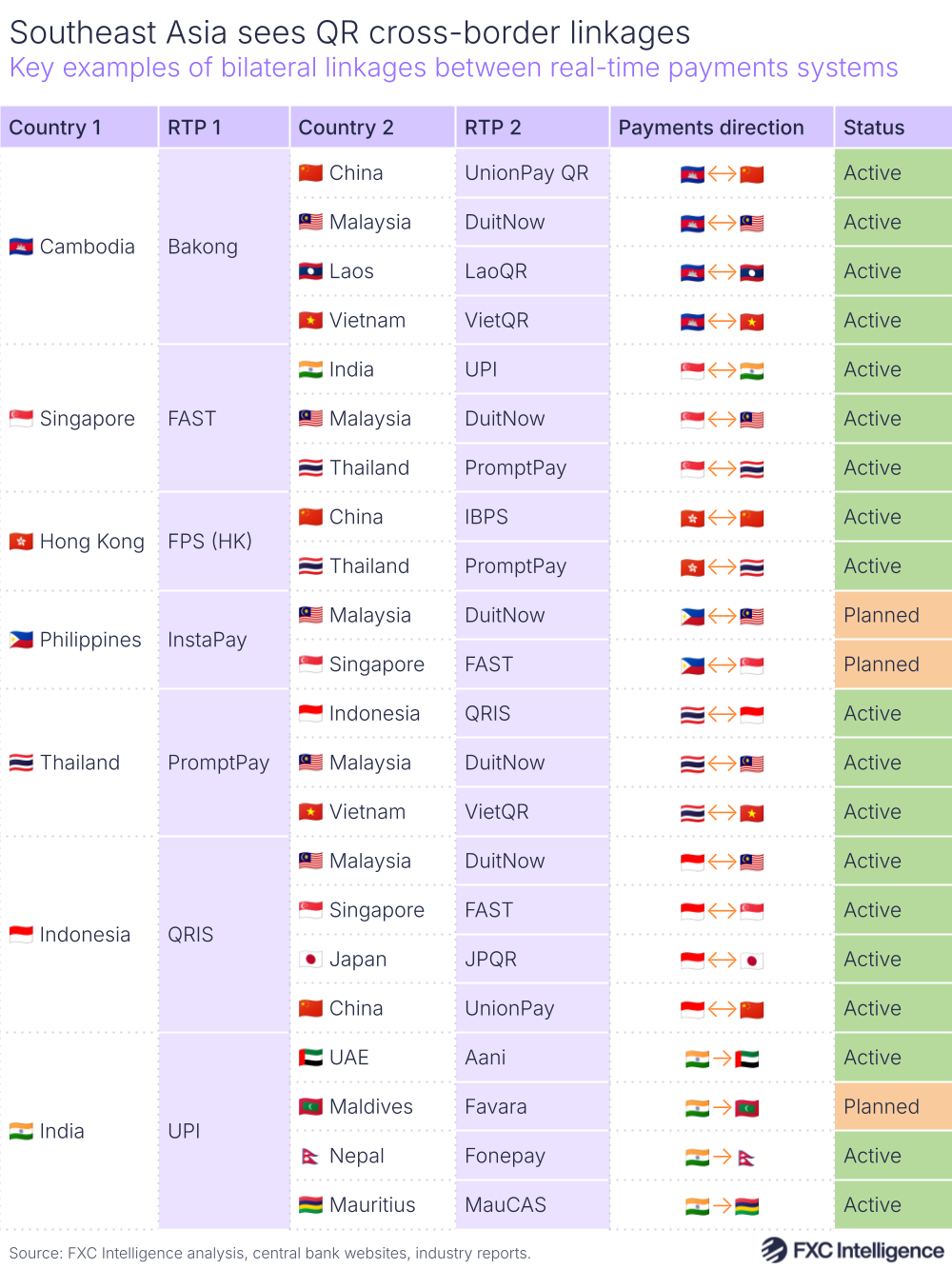

The US is a follower in a trend of real-time payments worldwide, with more than 70 real-time payment systems currently live globally. Significant attention in the industry has been paid to Pix in Brazil and Unified Payments Interface (UPI) in India – two instant payment networks that have had a massive impact on their home markets. UPI has continued to grow acceptance globally, having connected with other instant payments to enable Indian users to pay using UPI in other countries including France, the UAE and Singapore, as well as recent discussions around connecting with countries across the eurozone.

This reflects a wider trend of real-time payments systems being connected across Asia to enable instant cross-border payments. Though in many cases there are bespoke use cases, projects are ongoing to connect up instant payments more widely – for example, through the Bank for International Settlements’ Project Nexus.

The implication of this for banks has been a growing need to support real-time payments networks and instant payment networks, with “interoperability” between systems becoming increasingly important. This has also been reflected by Swift’s migration to ISO 20022 – a move that has required banks to move away from legacy infrastructure to support a new global messaging standard for cross-border payments.

AI powers fraud detection for banks

Aside from stablecoins, artificial intelligence (AI) has been another area where banks continued to move from hype to practicality in 2025. One of the biggest areas where this is of use, particularly for banks, is in automating fraud detection in payments – particularly for cross-border transfers, where payments cross multiple jurisdictions.

The biggest example of this has been Swift’s recent work alongside 13 international banks to use AI to create a system that is twice as effective at detecting fraud. The experiments saw ‘privacy-enhancing technologies’ being used to allow institutions to share fraud insights, as well as an AI model that was trained using each of the bank’s local data (not including customer information) to identify anomalous transactions across a dataset of simulated transactions.

In its own analysis for 2025, J.P. Morgan said that its deep investment in AI and machine learning played a large role in its cross-border flows. Specifically, the company has seen the technology decrease false positives and reduce the manual workload across its business.

What’s next for banks in 2026?

Interest in stablecoins and blockchain payments reached a critical point in 2025, but next year will be when many companies begin to implement or see the effect of digital assets on their payments businesses. Banks could begin to see the impact of stablecoins and tokenised deposits on their treasury movements and it is likely we will continue to see partnerships enable them to support the infrastructure that makes it possible.

As payments increasingly shift to real-time, banks will be challenged to ensure that they are complying with industry standards around AML and KYC. Aside from forming partnerships with payments providers to build out digital asset rails and expand their networks globally, we could see more effort being made and deals being formed to ensure that payments remain secure, seamless and transparent across borders.

Across both consumer and corporate money transfers, banks will continue to see a challenge from fintechs, the biggest of which are continuing to grow rapidly and in some cases (e.g. Wise, Revolut) even secure banking licences that are vastly extending their potential to offer new services for customers. Though banks have tried to launch new products to continue to compete in the space, these haven’t always proved successful (see Zing’s closure earlier this year). Next year could see greater consolidation and partnerships between players as banks continue to tap into innovation and offset other entrants to the space.