2025 has seen stablecoins move from a fringe element to one of the biggest topics in cross-border payments. We look at how the technology has risen this year, aided by key charts and data.

There are few topics that have received more attention within the payments industry this year than stablecoins.

After years of being on the periphery for most of the industry, 2025 has seen the blockchain-based technology achieve a level of mainstream acceptance that would previously have been hard to imagine – although there were signs from the outset of the year. 2025 began with interest in stablecoins already on the rise, aided by Stripe’s October 2024-announced $1.1bn acquisition of stablecoin infrastructure player Bridge. However, this was nothing on what would follow.

In the first quarter of the year, the technology was largely evident in thinkpieces and the occasional funding round, but interest began to heat up in Q2 as the passing of a US regulatory framework on stablecoins became an increasingly real possibility. The CEOs of major US banks indicated their own interest in the technology, regulations permitting, while some non-bank fiat-based players also began announcing their own offerings in the area.

When the GENIUS Act was signed into law on 18 July this year, the day after we published our landmark State of Stablecoins report, it truly opened the floodgates for stablecoins in cross-border payments. Companies from across the industry started taking not only very real interest, but also action. Some cemented products or solutions already in the works, while others announced plans to move into the space.

As we close out the year, the majority of major cross-border payments companies have some form of stablecoin-based solution, and many more are working on the technology. Meanwhile, stablecoin infrastructure providers have grown from minor parts of the industry to significant contenders – with fascinating implications for how the industry may evolve in the future.

In this report, we look over some of the most compelling charts, graphics and visualisations to bring you the story of stablecoins in cross-border payments in 2025 – and begin to consider what’s in store for 2026.

Growing cross-border payments interest in stablecoins

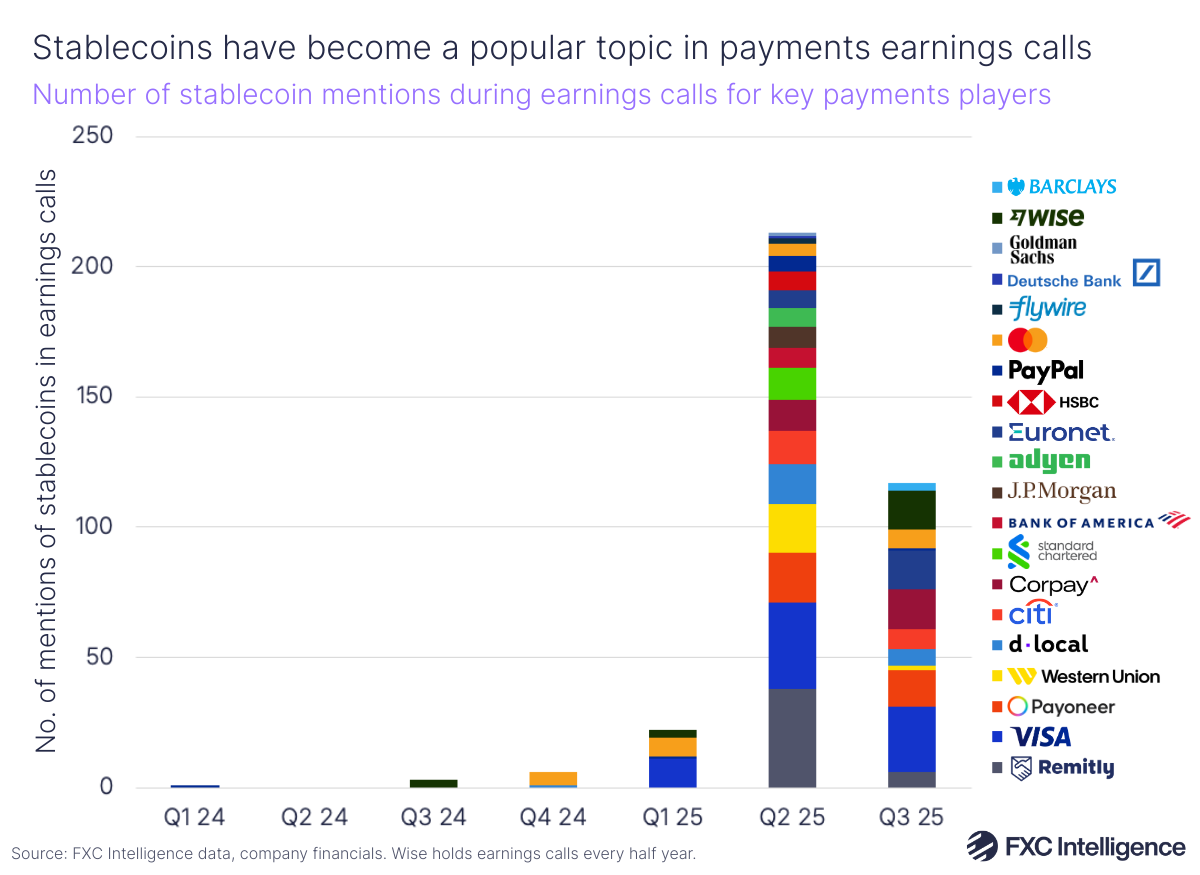

If there was any doubt about whether interest in stablecoins has truly grown this year among cross-border payments companies, it can be easily dispelled by how frequently the topic was discussed in the earnings calls of major payments companies.

Our analysis of the number of mentions of stablecoins during such calls shows that while the frequency of discussion had begun to rise from late 2024, during the industry’s Q3 2024 earnings, this jump was more pronounced from the earnings calls for Q1 2025, held as the GENIUS Act was making its way through Congress and growing numbers of companies were beginning to make hesitant moves or secure partnerships with infrastructure providers.

However, discussion truly surged in Q2 2025 calls, following not only the passing of the GENIUS Act but a blockbuster IPO for USDC stablecoin issuer Circle. Many players saw stablecoins mentioned in their earnings calls for the first time that quarter, with a significant number already outlining market-ready or near-market ready products.

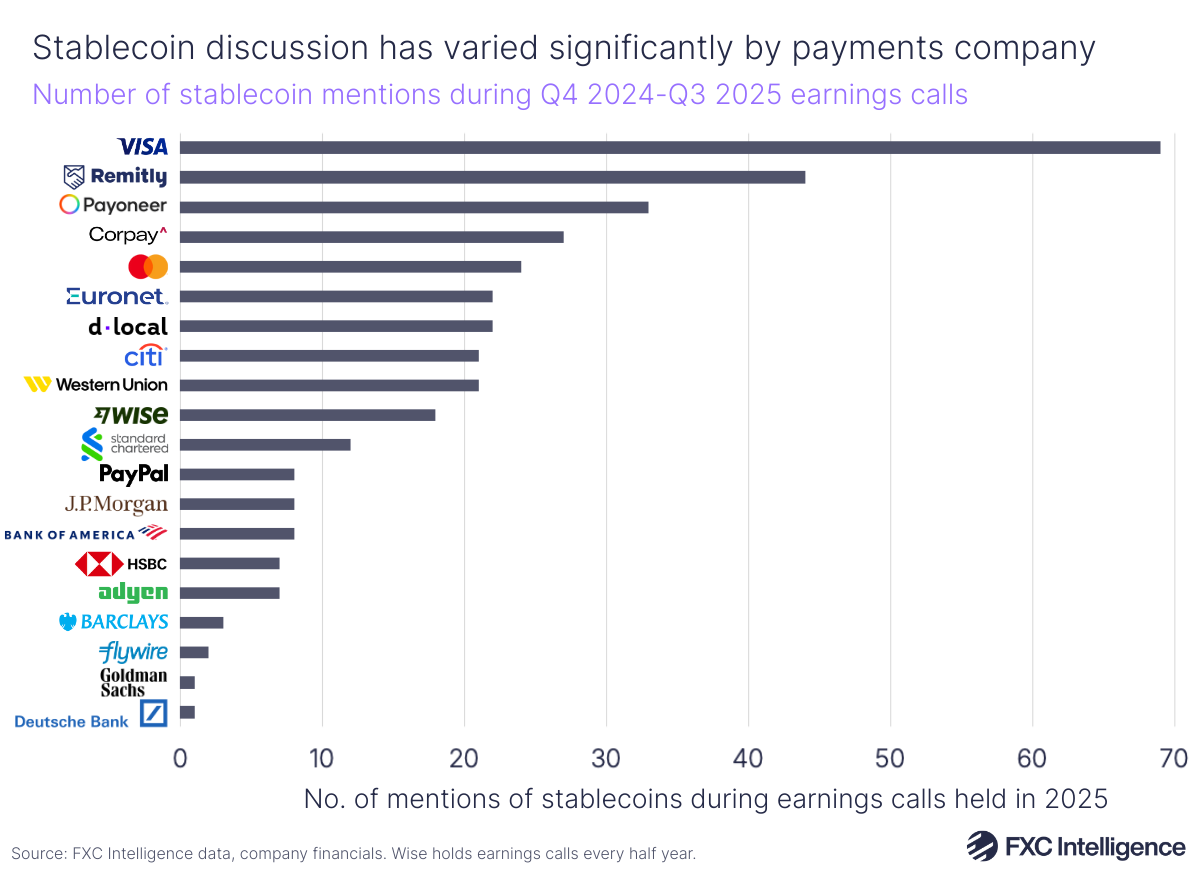

Across the past four earnings seasons, a small number of companies have emerged as being particularly vocal about stablecoins. Visa and Mastercard both had products ready from before the passing of the GENIUS Act, and have continued to announce further solutions since – likely a response to concerns that stablecoin-based networks may pose a threat to their business model.

Meanwhile, Remitly has made significant moves into the space following the GENIUS Act’s passing, building consumer-focused stablecoin wallets into its newly announced Remitly One membership programme. Corpay similarly has added a number of USDC-based solutions focused around wallets and 24/7 FX. Payoneer has discussed the potential of the technology and shared plans to add wallet functionality for customers in 2026, but has not yet gone so far as to announce a formal product in the space.

Funding and investment gains momentum

While stablecoin interest was mounting at the public end of the industry, there was also considerable movement in venture capital too. Over the course of the year, well over a billion dollars has been invested in companies related to stablecoin-based cross-border payments, and while millions have been put into companies at early or relatively early stages, some of the biggest payouts have been for more established players. In November, Ripple saw its valuation reach $40bn with a $500m investment, while October saw payments-focused blockchain Tempo, a joint project from Stripe and crypto venture firm Paradigm, raise $500m.

While there has been some variation in the types of players attracting interest from investors, providers of stablecoin payments infrastructure have been some of the most invested in, with many of these players partnering with or even being potential acquisition targets of fiat-based cross-border payments companies.

Industry moves take stablecoins beyond the hype

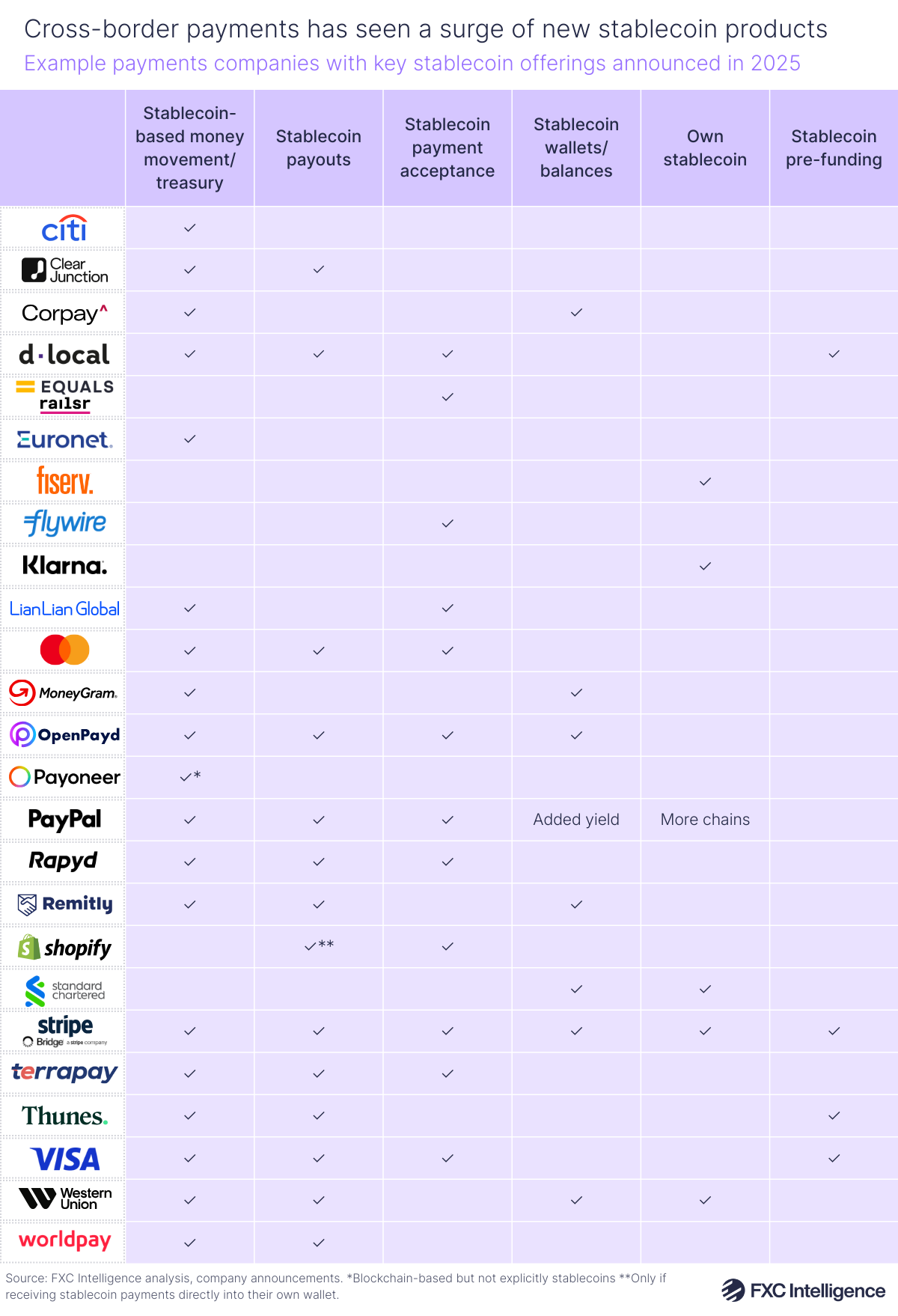

As the industry began to get its head around stablecoin-based payments, one of the most common questions was around where it could provide a genuine benefit. The potential largely lies in emerging markets, although there are also opportunities around out-of-hours settlement.

One of the biggest initial areas of discussion has been the use of stablecoins and the blockchains on which they move as the network for cross-border payments, with the ‘stablecoin sandwich’, in which a transaction starts and ends in fiat but is converted into and out of stablecoins in between, seeing particular focus.

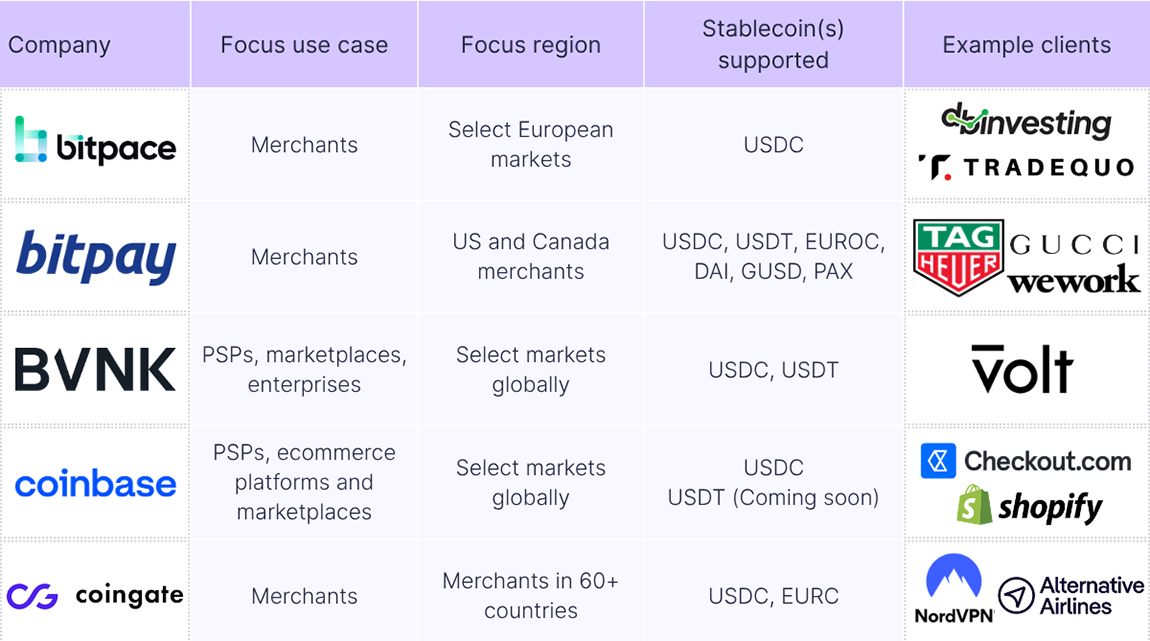

Among major payment companies who have already announced stablecoin products, solutions or offerings, this has been a major focus of use, with Corpay, Clear Junction and LianLian Global among those to make such moves.

However, one of the strongest initial forms of adoption is the use of stablecoins instead in internal treasury operations, which has significant cross-over with stablecoin-based money movement but is arguably easier to switch to at scale and presents fairly immediate operational gains for players. While not every company to make the switch has publicly announced that it has done so, among those that now use stablecoins for all of or part of internal treasury operations are MoneyGram, dLocal and TerraPay, while Payoneer is using blockchain-based token technology – but not yet explicitly stablecoins.

Stablecoin payouts, where merchants, contractors, loved ones or other recipients receive stablecoins into their own digital wallet rather than fiat currency have also seen growing adoption, particularly in markets with volatile fiat currencies, with Rapyd and Thunes among those to add the capability.

Others have also added the ability to accept payments, with PayPal’s Pay with Crypto being a notable example, while growing numbers are also adding their own wallet or stablecoin balance capabilities, including MoneyGram’s recent Colombia launch.

For many fiat-led players, stablecoins also provide an opportunity to serve as on and off-ramps, with growing numbers joining one of several stablecoin-based payments networks launched this year, including Circle’s Circle’s Payment Network (CPN) and Paxos’s Global Dollar Network. However, these remain fairly nascent, with Circle reporting in its Q3 earnings that CPN had enrolled 29 institutions since its May launch and is now processing annualised transaction volume of around $3.4bn.

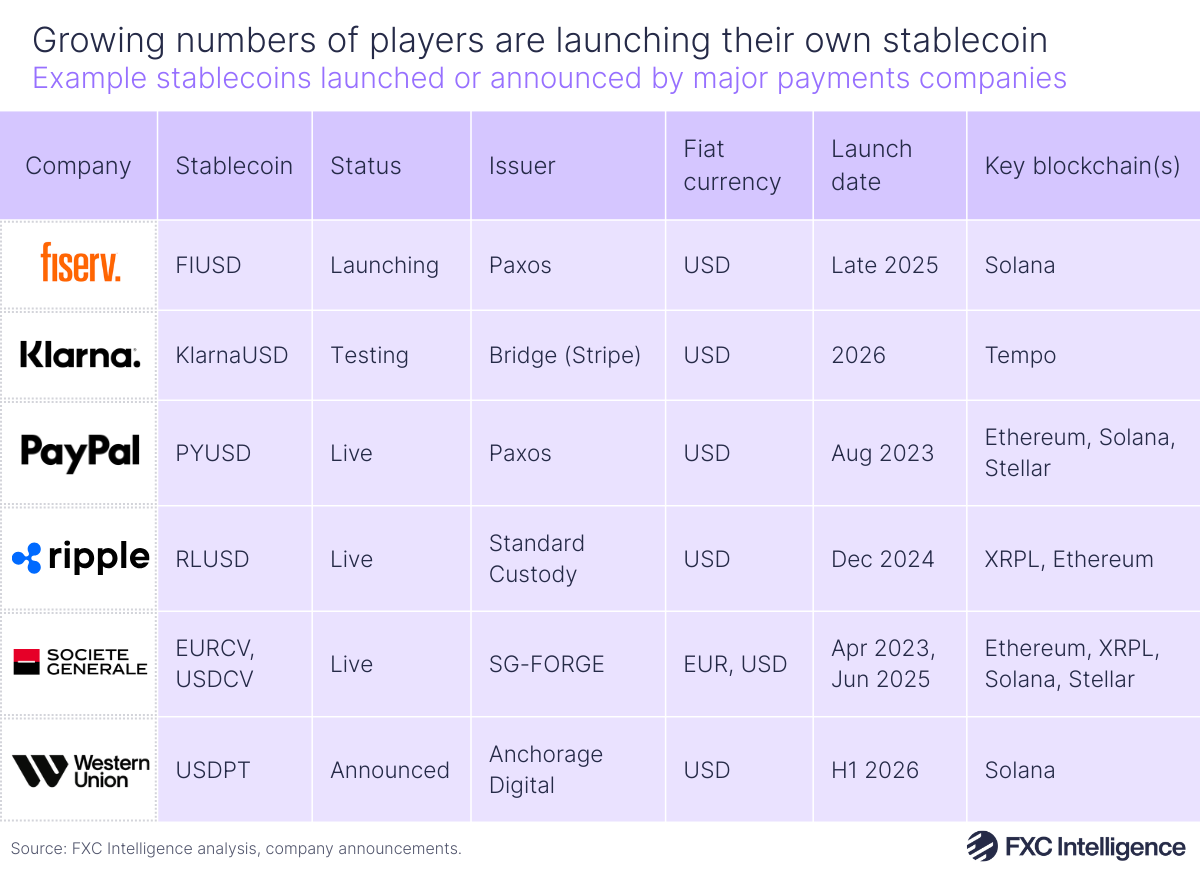

In the last few months, we’ve also seen growing numbers of companies announce their own stablecoin – a move that is not necessarily recommended for everyone using the technology, but which can bring benefits for those with sufficient scale.

Klarna and Western Union have been some of the highest profile launches of late, with WU being the only classic consumer cross-border payments company to make the move so far aside from PayPal, which launched PYUSD in 2023 and has since grown it to become the third-largest stablecoin globally after USDT and USDC.

With more announcements likely on the way, and full launches for many not expected until next year, we will have to wait to see how much of an impact this flurry of new stablecoins is likely to have.

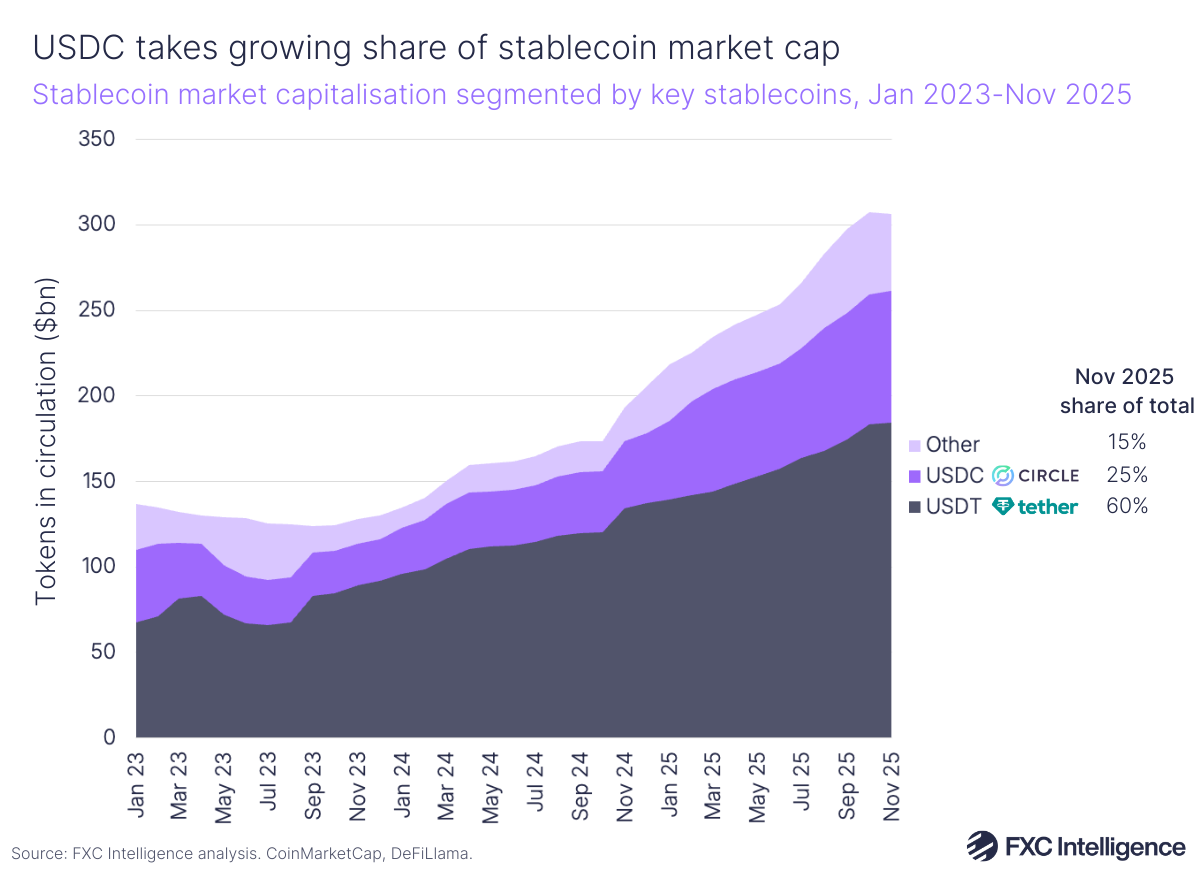

USDC vs USDT?

While more players are looking to launch their own stablecoins, the vast majority of the stablecoins in circulation globally are still made up of just two coins: Tether’s USDT and Circle’s USDC. USDT is the current global leader, however, the mix is beginning to change. While USDT closed 2024 with a 67% share of global stablecoins, at the end of November 2025 its share stands seven percentage points lower, at 60%. USDC, meanwhile, has seen its share climb from 20% to 25% over the same period, while all other stablecoins have grown from 13% to 15%. USDC is currently growing year-on-year at more than twice the rate of USDT, and has done so every month since February.

The biggest reason for this is likely to be the GENIUS Act, which among other things sets out specific definitions of what a stablecoin is, including requirements for how it is backed. USDC, with its regularly audited USD reserves in cash and cash equivalents, fits those requirements. USDT, which also includes several unconventional forms of backing among its reserves, including bitcoin and precious metals, does not.

While USDT’s higher liquidity means it remains very popular for stablecoin cross-border payments, particularly those between emerging markets, this distinction has seen many US-based players only touch USDC or other GENIUS-compliant stablecoins, which is likely to have driven up the stablecoin’s share. Tether is clearly conscious of the potential long-term impact of this, having announced the launch of its own GENIUS-compliant stablecoin, the all-American USAT, in September.

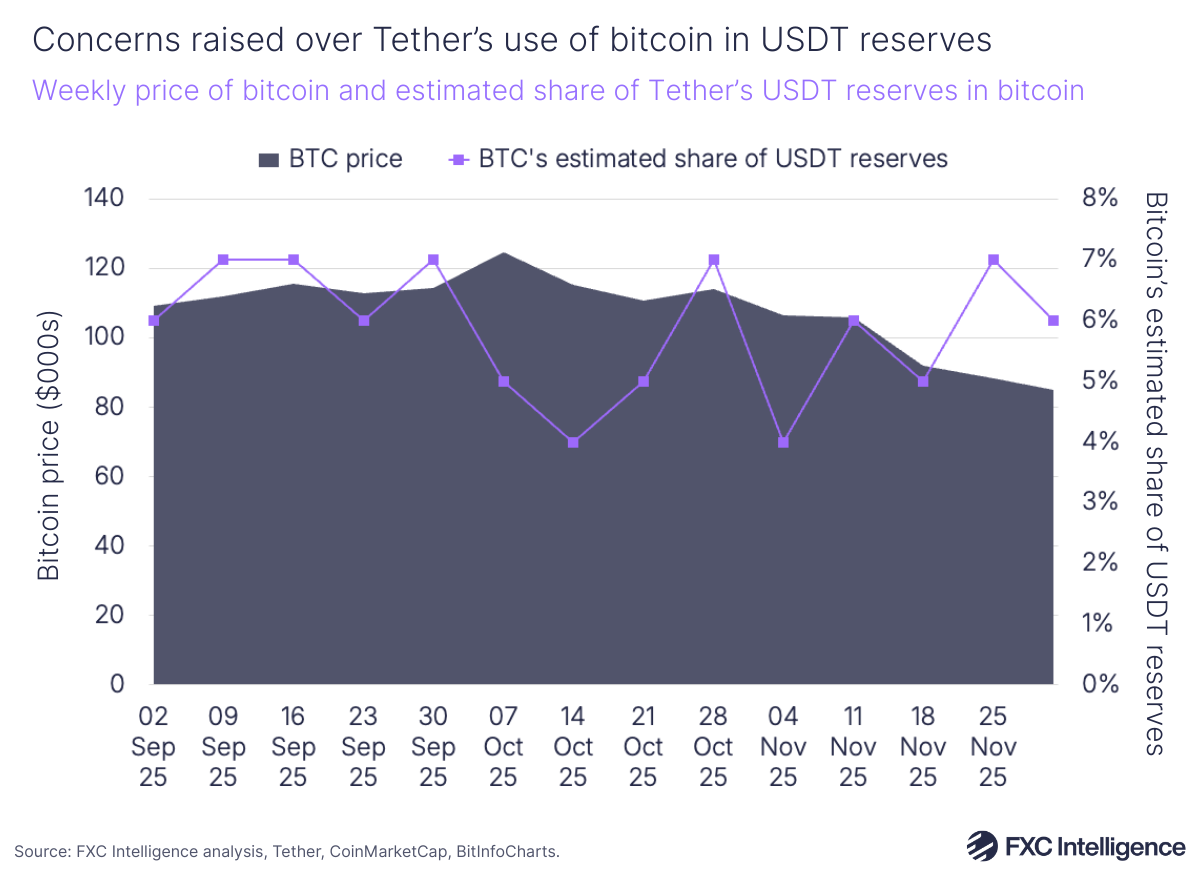

While USDT remains a key part of the stablecoin payments landscape, additional concerns have arisen over the last month that may cause further issues as the market matures. At the end of November, S&P Global Ratings downgraded USDT’s ability to maintain its peg to the US dollar from 4 (constrained) to 5 (weak). It cited “persistent gaps in disclosure” – USDT only publishes quarterly transparency reports, which are less rigorous than those of USDC – as well as the exposure to high-risk assets within the stablecoin’s reserves. While S&P cited gold, secured loans and corporate bonds as USDT reserve assets it had concerns around, its biggest focus of concern was USDT’s use of the cryptocurrency bitcoin.

“Bitcoin now represents about 5.6% of USDT in circulation, exceeding the 3.9% overcollateralisation margin, indicating the reserve can no longer fully absorb a decline in its value,” noted the authors of S&P’s Stablecoin Stability Assessment.

Bitcoin has seen its value decline over the past few months, while the share it has of USDT’s reserves appears to have climbed, creating a potentially significant risk that could be exacerbated by market panic if the cryptocurrency drops further. While USDT does retain considerable confidence from many quarters, such a risk does potentially expose the stablecoin to shocks similar to those seen in 2022 when several more experimental ‘stablecoins’ lost their fixed value to the US dollar.

Into 2026: Prospects for the year ahead

Stablecoins have been the subject of immense cross-border payments hype in 2025, and it is clear that such animated enthusiasm cannot sustain indefinitely. However, this does not mean stablecoins are set to sink into obscurity: quite the opposite.

As we look into 2026, engagement with the technology is likely to become more sophisticated and nuanced. This year, the market was working to understand what stablecoins really offered and how they could be effectively implemented. Next year, the attention is more likely to be on practical applications and tangible results.

We are likely to initially see treasury applications come into greater focus, but as the year progresses we will also see optimisations of infrastructure stacks as well as the initial results of an influx of new stablecoins.

In-development new blockchains are promising better alternatives for payments, while networks such as CPN are set to see greater adoption. Meanwhile, consumer and B2B solutions are likely to continue to proliferate. Amongst all this, the actual share of cross-border payments using stablecoins is going to climb, but at less than 1% at present, it still has a very long way to go.

With so many players and solutions entering the market, some will prove more effective than others, and 2026 will provide the first real test of the technology’s potential for longevity.