As PayPal reaches month six of its transformation project under CEO Alex Chriss, we explore how Xoom has been impacted so far, with insights from PayPal’s Q2 2024 earnings and beyond.

PayPal may have enjoyed a strong run of success during the pandemic, but in the years that followed it has struggled to maintain growth and when incoming CEO Alex Chriss took the helm last August, he joined a company in need of transformation.

Two earnings seasons ago, Chriss characterised 2024 as a “transition year” as he outlined the first steps in a multi-year plan for change at PayPal, and in the company’s latest earnings this week, he reminded analysts and investors that the company was only half a year into this plan. However, with good initial results, he was also positive about the company’s position.

“I feel really proud that we are stronger today than we were six months ago, and we will be stronger six months from now than we are today: we’re executing against our game plan,” said Chriss in PayPal’s Q2 2024 earnings call.

“This will be measured in quarters and years, so it’ll be a long game, but six months in, we are on the right trajectory.”

This attitude was welcomed by investors, with the company’s share price rising on the results, but it also speaks to a period of change that is reaching not only the company’s checkout business, but also areas of its P2P payments that it has long neglected, namely Xoom. Acquired by PayPal in 2015 for $890m, the consumer remittance brand initially saw investment under its new parent, however when the pandemic hit PayPal shifted focus and Xoom was deprioritised.

Now, however, there are signs of renewed interest in the brand as part of a wider bid to grow all parts of PayPal, with the company consistently naming it in earnings materials since the start of 2024 – the first time it has done so since 2020.

But six months into the company’s multi-year transformation project, are there signs that Xoom is benefitting? We explore key earnings data and beyond to find out.

PayPal sees promising early results: Q2 2024 highlights

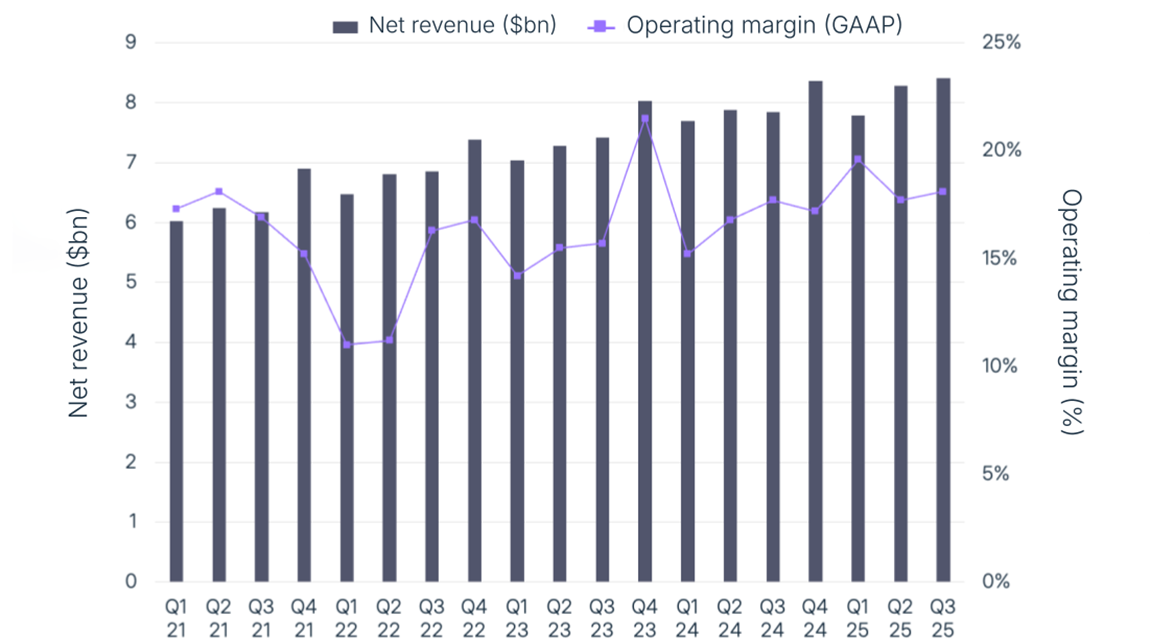

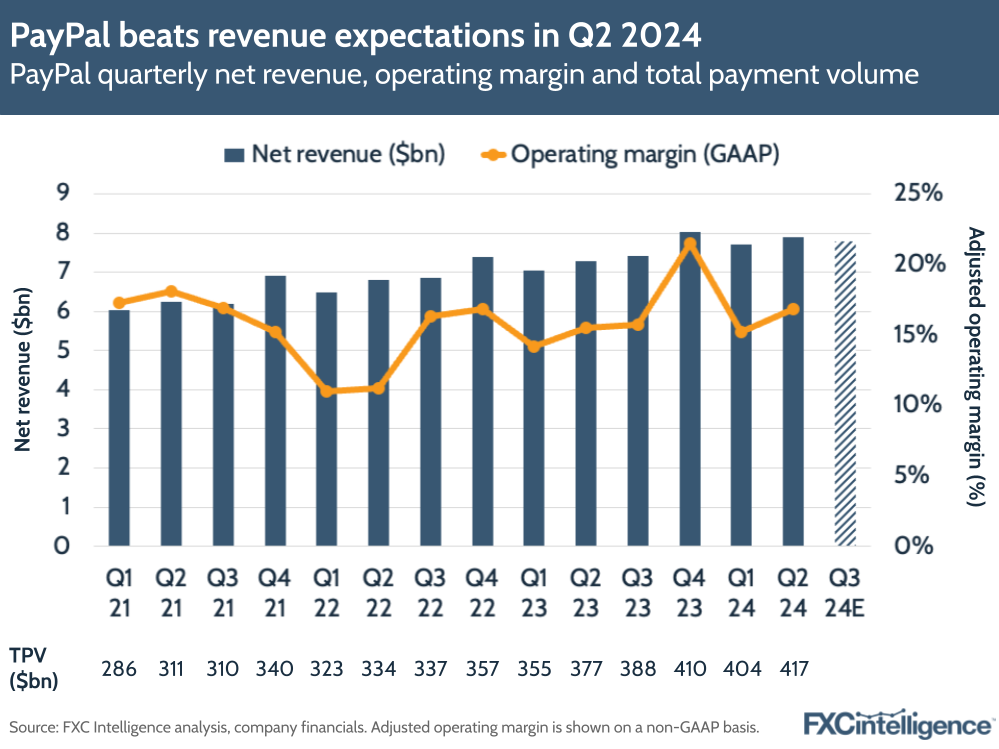

While PayPal touted Q2 2024 as continuing its ongoing transformation plan, reminding analysts that many results would be seen for months or years yet, on the top line results were strong, with Chriss saying the company was “on the right track”.

This was led by an 8% overall increase in net revenues to $7.9bn, while the company saw its GAAP operating margin expand 126 basis points to 16.8% and its non-GAAP operating margin expand 231 basis points to 18.5%.

Here, PayPal beat is Q1 2024 projections for the quarter. Notably, this was driven by global growth, with both US and international net revenues – which account for 58% and 42% of the business respectively – seeing 8% YoY increases.

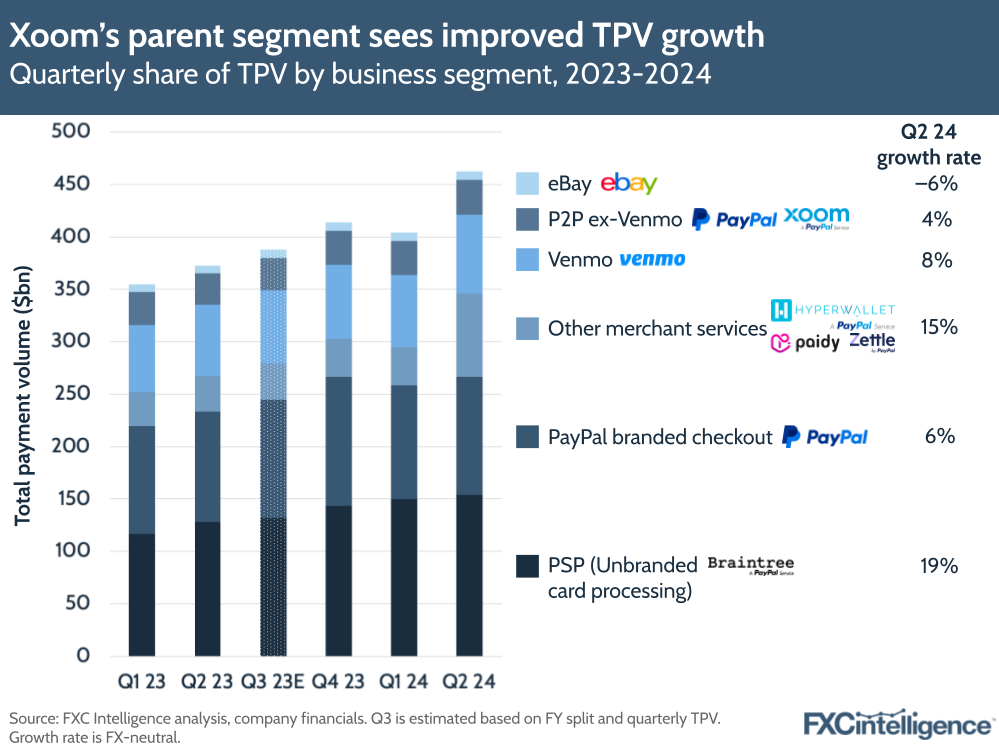

Total payment volume (TPV), meanwhile, saw an 11% YoY growth to $417bn, producing a 1.89% take rate – two basis points lower than Q1 2024 and 5 basis points lower than Q2 2023.

Here, much of the growth was driven by the company’s unbranded card processing segment, predominantly Braintree, which grew 19% on an FX-neutral basis and is now the company’s largest contributor of TPV. The smaller other merchant services division, which includes Hyperwallet, Zettle and Paidy, had the next highest TPV growth rate, at 15%.

The company’s US-based domestic payments brand Venmo, which saw an 8% TPV growth, was also cited as a strong driver of top-line results, as was PayPal’s branded checkout.

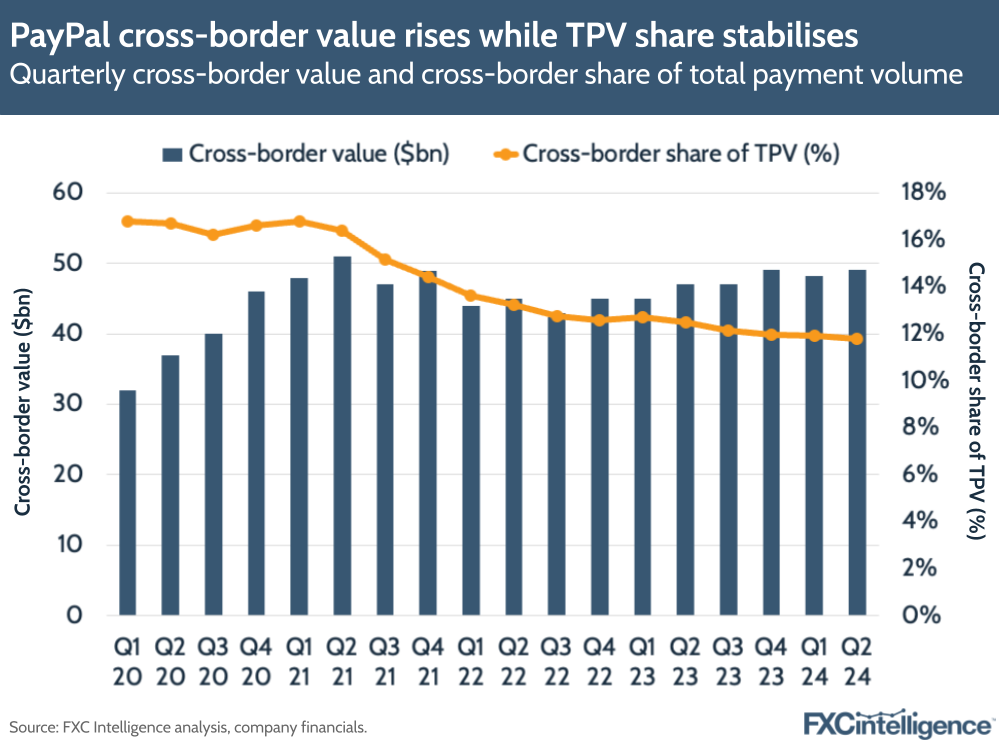

Cross-border TPV in particular saw 5% YoY growth, or 6% on an FX-neutral basis. This was in particular driven by intra-European corridors, while softness in UK-EU proved to be a headwind.

However, cross-border share of TPV has continued to decline. While it was down by only 15 basis points on Q1 2024, it was down 70 basis points on Q2 2023 and is the lowest it has been since the company began reporting this metric in 2017. This speaks not to poor growth in cross-border, but more that domestic – and in particular US domestic – volume has grown at a faster rate, suggesting that this is an ongoing opportunity for PayPal.

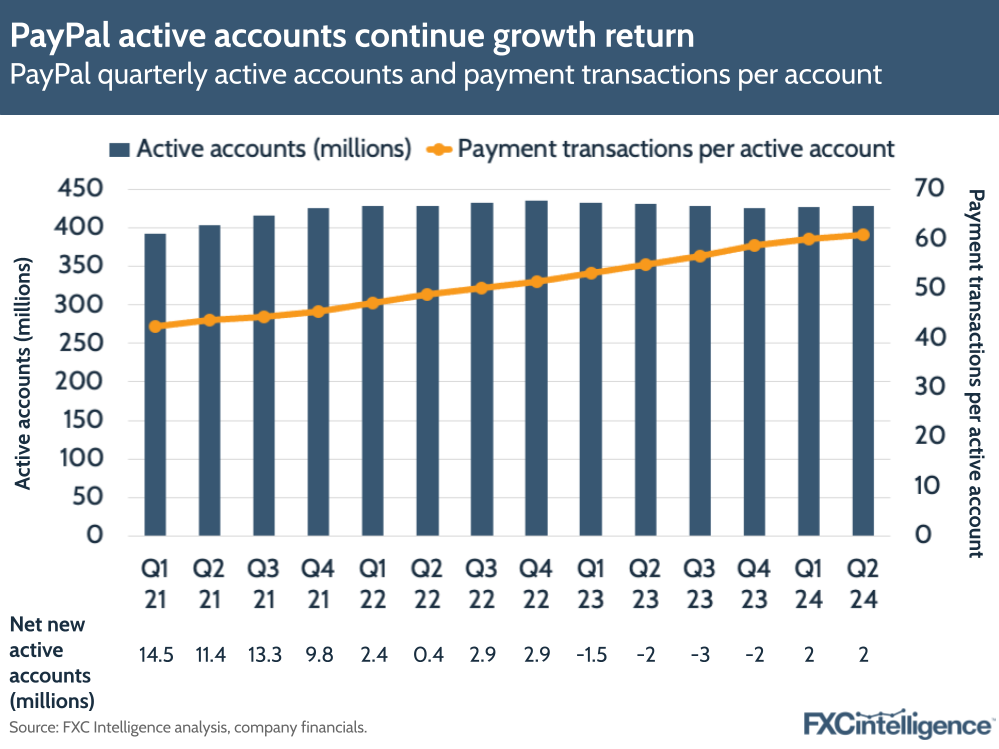

Active accounts, meanwhile, have rebounded from the company’s first period of quarter-on-quarter decline, with PayPal seeing two million net new active accounts in Q2 2024 compared to Q1 2024. While it is still two million accounts below its Q2 2023 numbers, it suggests PayPal’s period of shedding low-value accounts has come to an end.

Meanwhile, the company has focused primarily on growing the number of transactions per active accounts as it looks to increase revenue per user. Here the company saw a 1.5% improvement on Q1 of this year, and saw an 11.3% YoY increase.

Earnings insights for Xoom: P2P growth

Looking to Xoom, while PayPal does not break out numbers for Xoom alone, as of this year it has begun breaking out its TPV by business segment, which includes P2P ex-Venmo. According to the company, this “primarily comprises PayPal P2P volume, with some contribution from Xoom”.

Here, there is evidence that the company’s refocus on both Xoom and the wider division is beginning to yield some results. While not yet growing at the rates of some of PayPal’s bigger segments, P2P ex-Venmo did see 4% growth YoY on an FX-neutral basis in the quarter, accounting for 8% of the company’s TPV.

This makes this the strongest growth quarter for the division since at least 2022 (PayPal has only released figures for Q1 2023 onwards), and only the third published quarter where the company has reported growth in P2P ex-Venmo, with much of 2023 seeing YoY declines.

Here the company cited the growth coming from “increased engagement among [the] existing user base”, with Chriss noting that the company was “more positive than three months ago” on P2P.

“P2P is an essential acquisition and engagement tool for us, and we are returning it to growth,” he said.

“We suffered declines through 2023, but over the past few quarters we have seen an improvement driven by product enhancements such as new global withdrawal capabilities, better risk decisioning and more cross-border activity.”

Signs of Xoom’s refocus

For Xoom in particular, there is evidence of a prior prolonged lack of investment, with areas such as social media remaining unchanged from 2020. However, while it is still early in the process of reviving the Xoom brand, there are signs that PayPal has begun to increase its focus on improvements and other changes to improve competitiveness.

There are signs that Xoom has been adjusting its pricing to increase its competitiveness, particularly on some of the traditional remittance corridors where we have seen marked pricing changes in recent months relative to the wider market. Xoom has traditionally priced a fair amount above market averages, making this a decisive move.

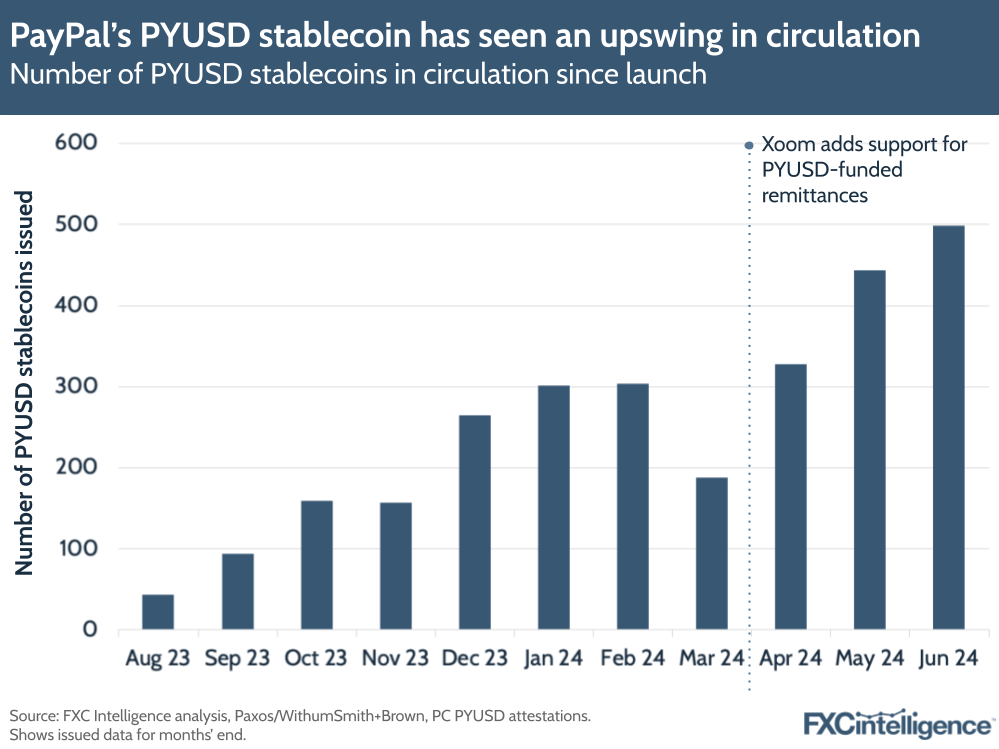

For US customers, as of April the company has now also made it possible to fund remittances with PayPal’s US dollar-backed stablecoin PYUSD. Customers who use this service also have their transaction fees waived – these fees are one of two elements that make up the overall charge to send a remittance, and which we previously estimated to account for around 25% of Xoom’s overall pricing.

While this service is only one of several uses for PayPal’s stablecoin, which was first launched in August 2023, it is notable that the number of tokens issued has risen at a faster rate since the feature was added.

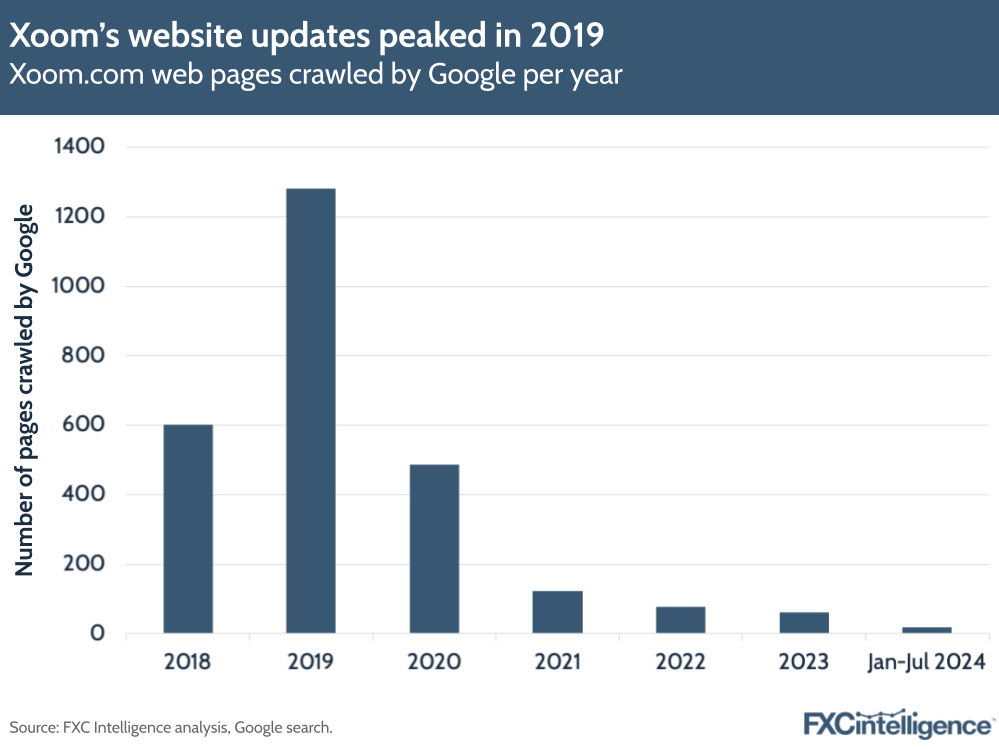

Website updates

While much of the work on Xoom is happening behind the scenes, we can look for signs in a number of key areas, including updates to the company website, as shown through Google crawls. Although not a perfect measure, changes to a page or the addition of a new page on the company’s website will generally trigger a Google crawl, giving a sense of how frequently the company is making changes.

Using this measure, we can see that in general Xoom made the most changes in 2019, and saw a dramatic drop-off in 2021 onwards – in line with a decline in other marketing efforts.

However, we also see some signs of increased work in 2024 so far.

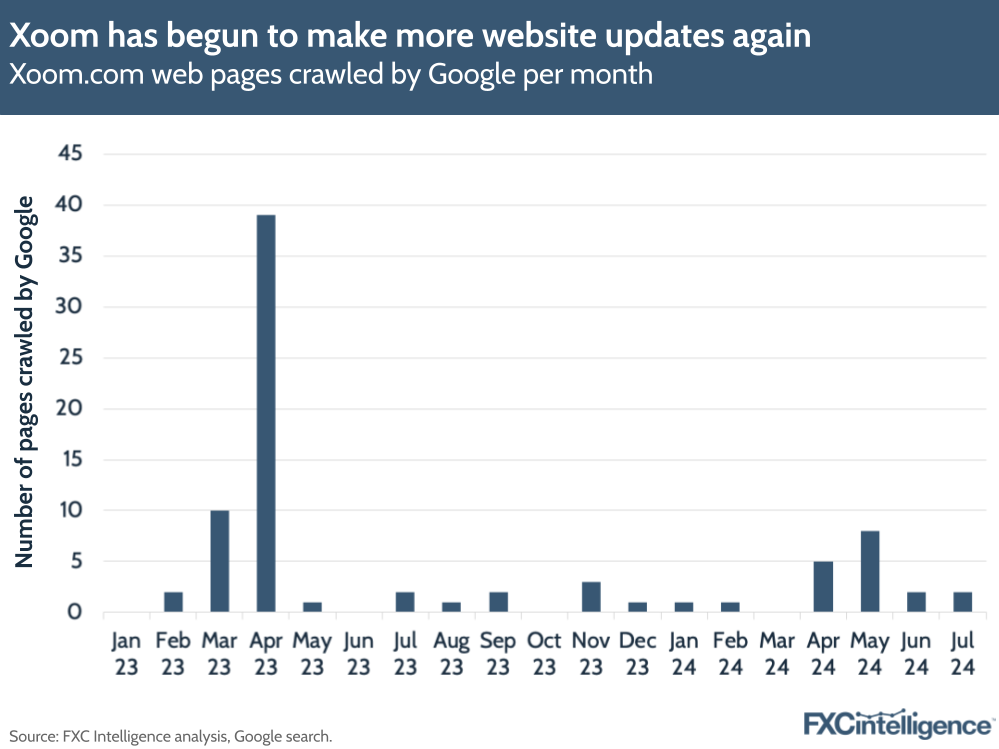

Looking just at pages crawled since the start of 2023 on a monthly basis, we do see an uptick in the number of pages crawled in the past months – in line with a refocus on the brand. While so far many of these have focused on minor adjustments and updates to legal-related pages, they speak to a renewed interest.

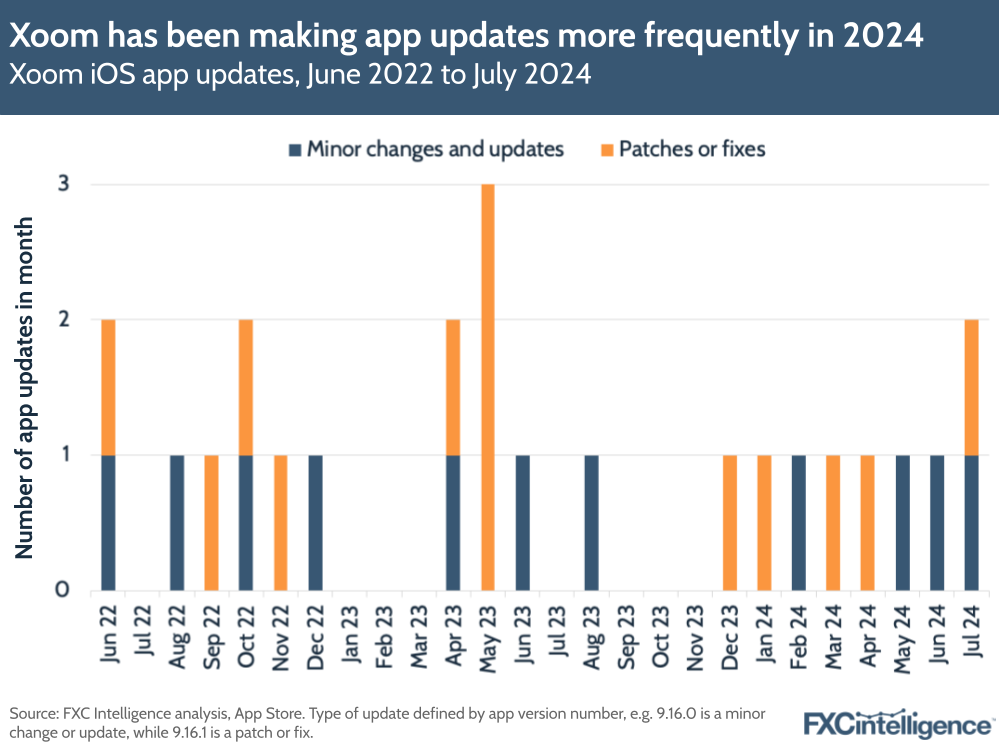

App updates

There are also similar signs in updates to the company’s iOS app. Looking at version history data shows us all the updates that have been made for the past two years and while there hasn’t been a major new release of a rebranded or reworked app in that time, there is evidence of an increased pace of updates in recent months.

Over the two year period, there have been 13 minor changes or updates – that is, additions or changes to features or text within the app – and 13 patches or fixes – that is, changes to fix bugs and other minor issues. However, a higher density of the minor changes and updates have occurred in the past six-month period than in any other six-month period over the past two years, and while this is not yet a significant enough difference to speak to a strong uptick in investment, it does add to the evidence of an increased brand focus.

Impact on Xoom’s web traffic

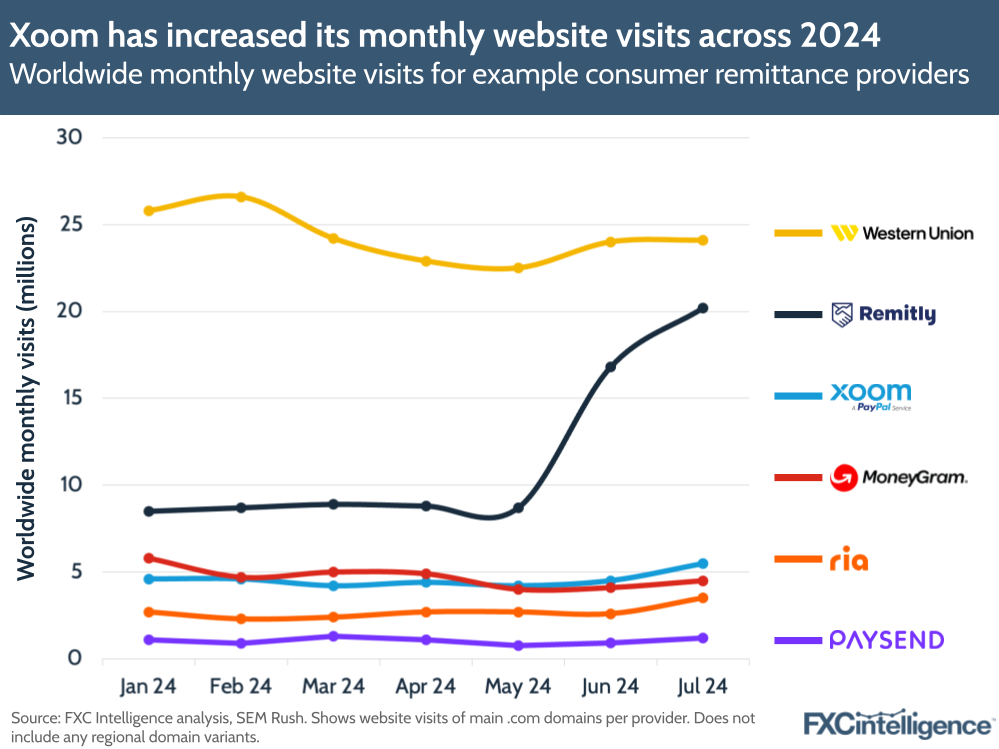

While there is some evidence of increased investment in Xoom, there are also signs that this is beginning to pay off in terms of the amount of traffic the company is attracting to its website.

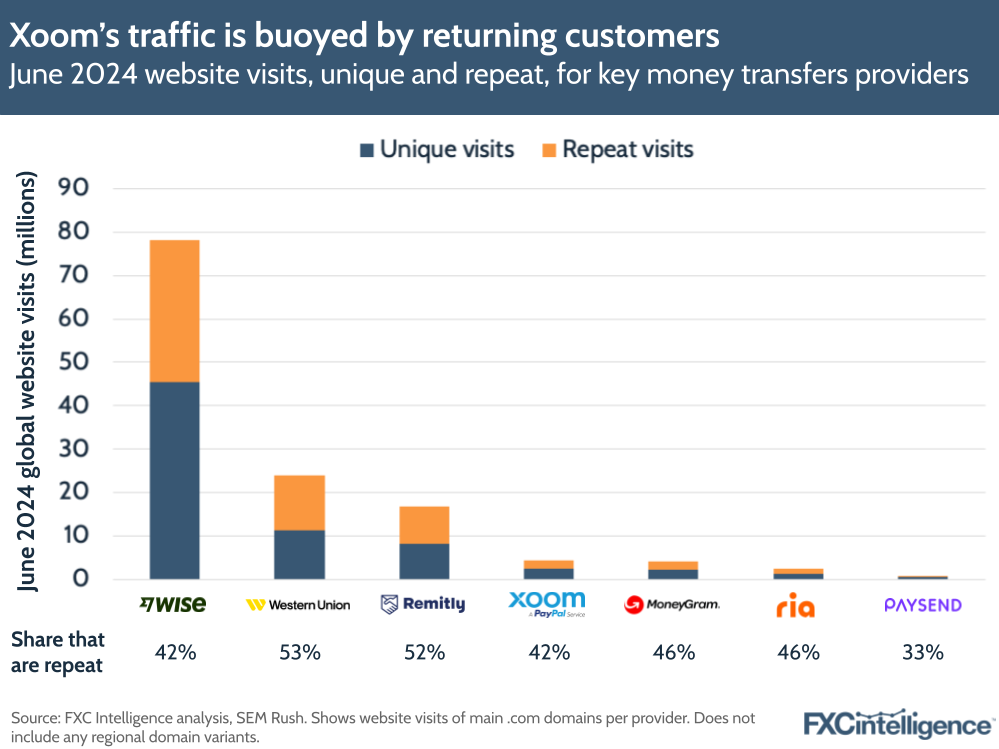

While the Xoom website is not attracting the levels of traffic enjoyed by Western Union (24 million global visits in June 2024), the traditional market leader, or Remitly (16.8 million visits), the fastest growing remittance player, it has seen its global monthly website visits rise enough that it has been outperforming MoneyGram, the next biggest in terms of web traffic, since May. While MoneyGram received 4.1 million visitors in June, Xoom had 4.5 million. Notably, all were outstripped by the more consumer and SME money transfers-focused Wise, which had 78 million visitors.

Xoom has also seen consistent month-on-month growth in most months this year, seeing visits increase by 7% in June versus May. This is a far cry from Remitly’s 93% month-on-month growth, however the company has been undertaking significant marketing spend that has buoyed this, and it is higher than any other major rival apart from the lower-traffic Paysend, which rose by 22%.

Traffic sources

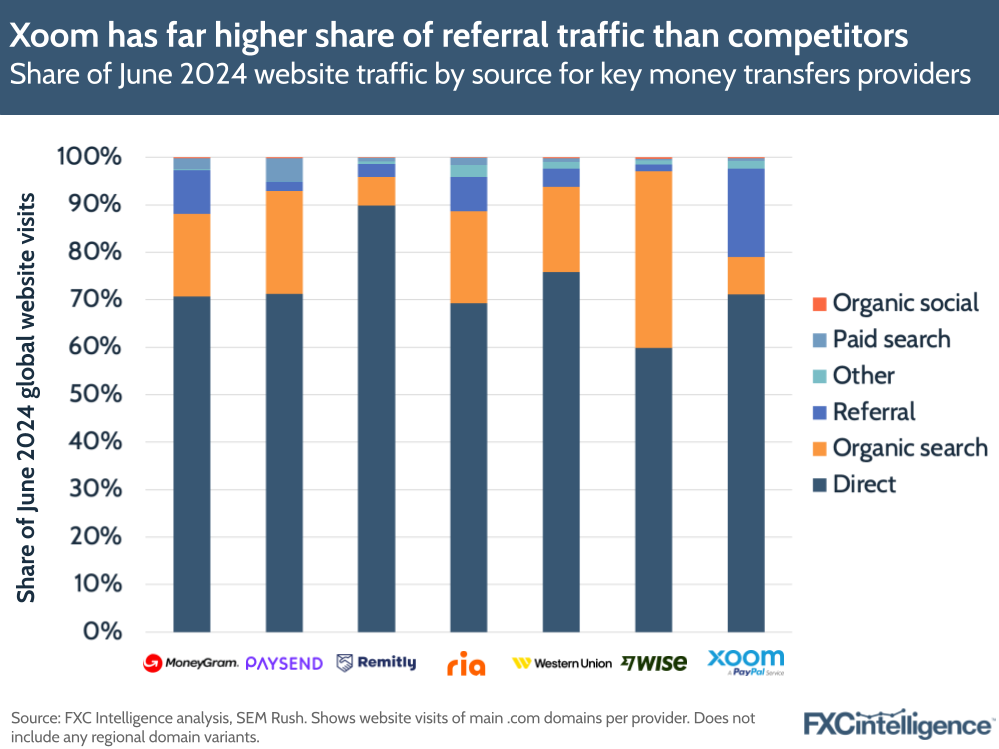

While PayPal has stated that much of its current uplift in the P2P ex-Venmo segment is from existing customers, it is notable that Xoom had a lower share of repeat visits than many of its rivals. While it matched the level of repeats of Wise, out of those assessed only Paysend had a lower share of traffic that was repeat visitors, at 33%.

However, when reviewing the share of visitors from different sources, Xoom stands out for two reasons. Firstly, it has one of the lowest shares of organic search, accounting for 8% and second only to Remitly’s 6%.

While the latter is likely a result of a rise in other forms of traffic from Remitly’s recent elevated marketing spend, this reflects an area that Xoom does not yet appear to have focused on and so presents a potential opportunity for future growth.

Secondly, Xoom has the highest share of referrals by some way, accounting for 19% of June’s traffic. This is twice that of MoneyGram – the next highest – and is significant because it reflects the unique position Xoom is in relative to customers.

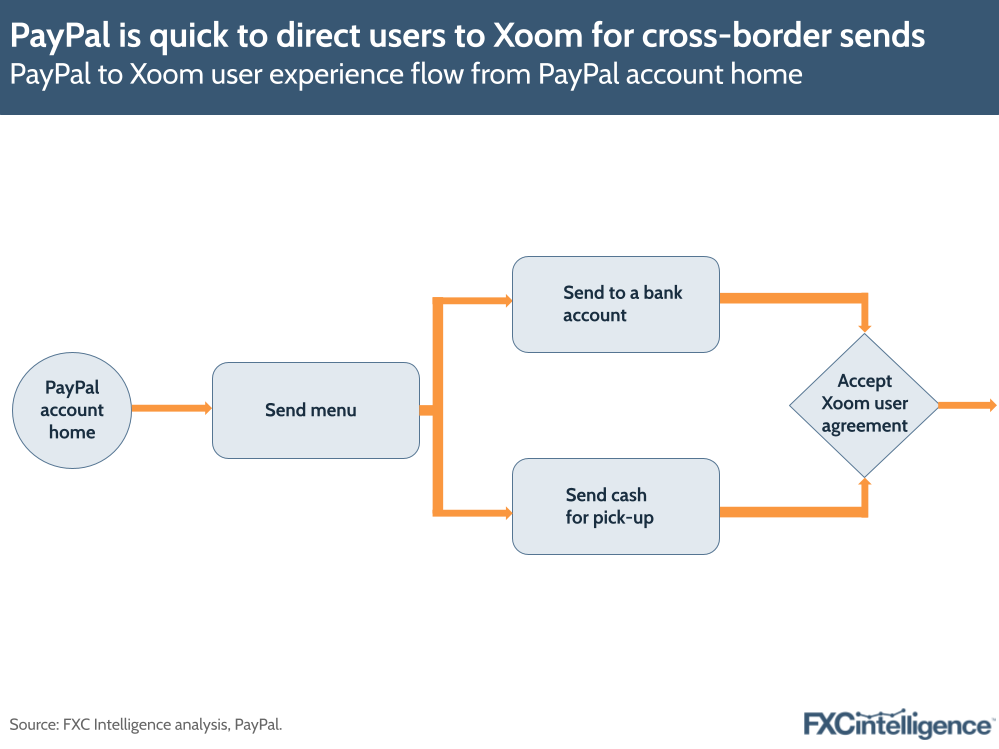

While only a small percentage of potential customers are finding the brand through search, many are arriving at the website via a referral. And more critically, 56% of this referral traffic is coming from PayPal itself as Xoom is part of the P2P payments flow for customers looking to send money beyond the PayPal ecosystem, such as to a bank account or for cash pick-up.

Geographic focus

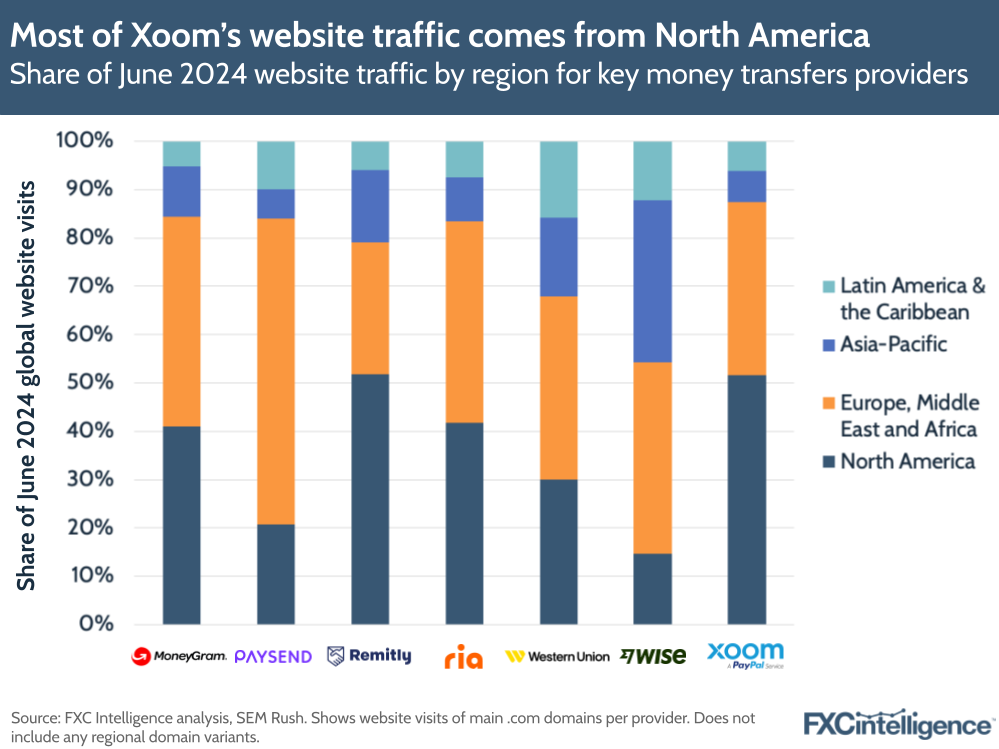

Finally, looking geographically, Xoom’s traffic has an interesting split versus competitors, which is particularly notable as geographic traffic is a strong indicator of the location of send customers, although it does not account for markets where there is a strong preference for app use over website use.

For Xoom, North America remains its dominant market, accounting for 51% of its June traffic. This is second only to Remitly, which had 52% of its website traffic originating in North America. Xoom also had little share of visitors in LatAm or APAC versus other players in the space – although this is likely due to the fact that it does not currently cater to customers in these regions.

On a country-level basis, the US accounted for 48% of Xoom’s traffic in June – the highest of any player we looked at and several percentage points above Remitly, the next closest, at 42%. Its next largest countries was Germany (29% of traffic), while Italy and Canada were the only other two send markets with more than 3% traffic share in the month. This means that not only is 90% of its traffic coming from less than a quarter of its send markets but 77% is coming from just two markets – the US and Germany.

This indicates that there are significant growth opportunities for Xoom in many of the markets it already serves, as well as opportunities further afield.

Next steps for Xoom

While still a small part of the wider PayPal business, Xoom is back in the spotlight for the company, and there are early signs that this is paying off, something that Chriss acknowledged of the wider P2P division in the earnings call.

“It is encouraging to see the initial impact of our initiatives related to price to value, as well as ongoing product enhancements in areas like P2P,” he said.

However, with only months having passed since the company began to reinvest in the brand, we can expect far more development of Xoom in the future – as reflected by comments from Chriss.

“Some of our efforts, particularly on the innovation side, are still early and will take time to scale, but we’re encouraged by the initial results and customer response as we begin moving from the test and pilot phases into launch,” he said.

“We will continue to invest in our experiences, pricing and marketing to drive enhanced awareness and engagement.”

While some areas such as pricing have begun to see some changes, Xoom has particularly strong opportunities in some of its under-focused markets, particularly in Canada and Europe outside of Germany, where it already has an established presence but is seeing lower levels of traffic.

It is also likely to have opportunities to further meet the needs of customers in the US and Germany where it has higher traffic, particularly by increasing its offering and competitiveness on popular corridors where it has lower market share.

Beyond this, Xoom has considerable untapped potential when it comes to marketing, including through search and social media, as well as more traditional campaigns. PayPal is only at the beginning of its journey to reinvest in Xoom, and there are considerable opportunities remaining – expect to see far more development in the coming months and years.